Maximizing your retirement income requires navigating complex tax brackets, shifting Medicare surcharges, and volatile market returns before you officially leave the workforce. Asking your financial advisor the right questions will expose hidden vulnerabilities in your distribution strategy and secure your financial independence. A comprehensive pre-retirement meeting serves as the ultimate stress test for your life savings. You need clear directives on how to sequence your withdrawals, protect your assets from inflation, and shelter your income from unnecessary taxation. Transitioning from accumulating wealth to generating sustainable paychecks demands a rigorous approach. By demanding specific, data-driven answers from your planner today, you establish a resilient foundation that prevents the anxiety of outliving your money.

Income Alignment Strategies

1. How Can I Optimize My Social Security Benefits for Long-Term Income?

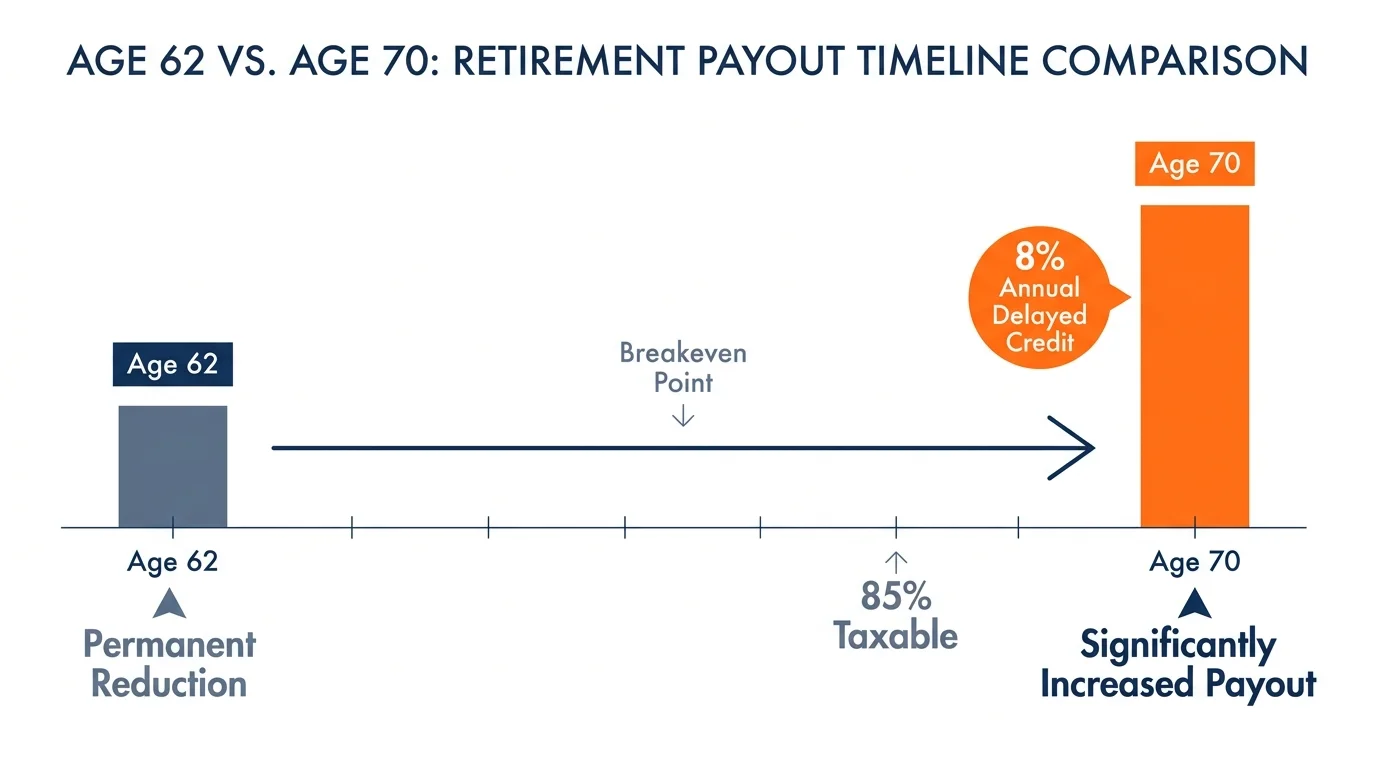

Securing maximum payout from government benefits requires precise timing. Claiming at age sixty-two results in a permanent reduction in your monthly paycheck. Conversely, waiting until age seventy grants an eight percent annual delayed retirement credit, drastically increasing guaranteed lifetime income. Ask your advisor to calculate your breakeven point based on health history and family longevity. If married, coordinating spousal benefits is essential; the higher earner should often delay claiming to maximize the survivor benefit. Your financial planner needs software to run scenarios so you visualize the dollar difference over a thirty-year horizon. Because benefits can be taxed up to eighty-five percent, your advisor must calculate how account withdrawals trigger taxes. Always consult a licensed professional to ensure projections align with your earnings record via the Social Security Administration.

2. What Is the Most Sustainable Withdrawal Rate for My Investment Portfolio?

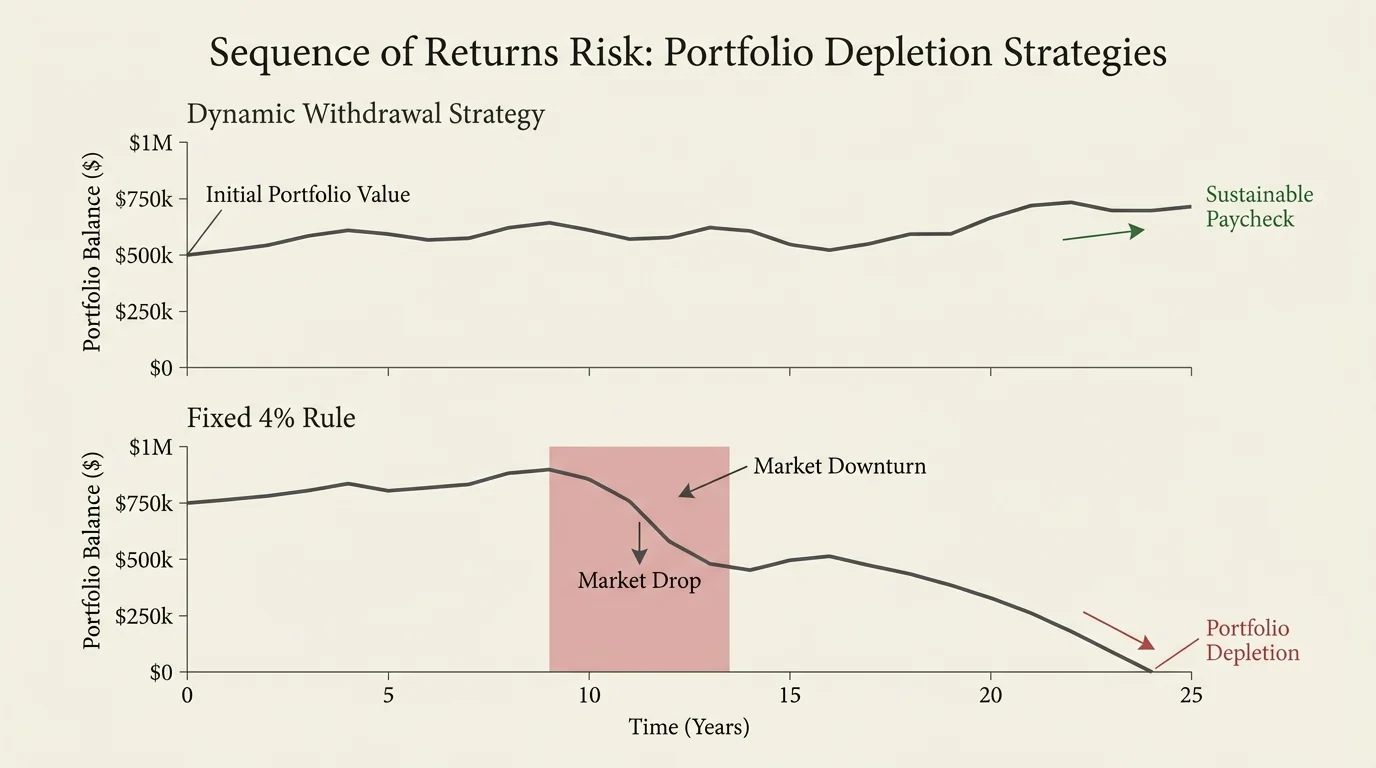

Ask your planner to define exactly how they generate your monthly paycheck when the stock market declines. The traditional four percent rule often fails to account for current market valuations and prolonged inflationary periods. Your planner should explain their mathematical approach to sequence of returns risk. If the market drops significantly during early retirement, withdrawing a fixed percentage can permanently cripple portfolio balances. A fiduciary advisor typically recommends a dynamic withdrawal strategy, adjusting distributions based on performance rather than following rigid formulas. You must understand whether they sell equities during downturns or rely on a dedicated cash buffer to fund living expenses while the broader market recovers. Demand a historical stress test of your asset allocation.

3. Should I Incorporate Guaranteed Income Strategies Like Annuities?

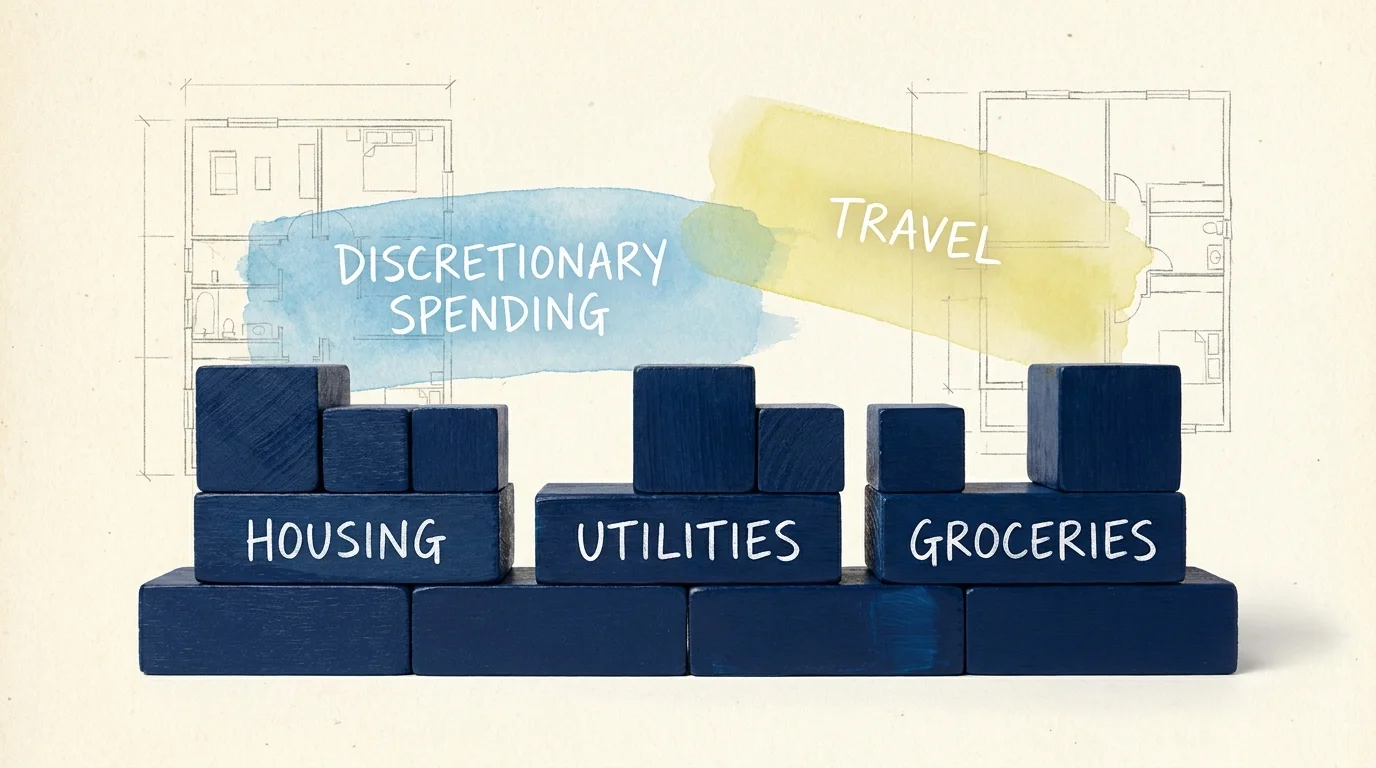

Securing a guaranteed income floor that covers essential living expenses—like housing, utilities, and groceries—drastically reduces financial anxiety. Ask your advisor if you should incorporate annuities or utilize pensions to build this rock-solid foundation. While some retirees possess robust corporate pensions, others must purchase their own income streams through fixed-indexed annuities. You need your planner to dissect administrative fees, surrender charges, and exact payout rates of any proposed product. Fiduciary planners compare multiple carriers and explain trade-offs between retaining liquidity and purchasing a lifelong income stream. Because inflation erodes purchasing power, guaranteed income discussions must include funding discretionary spending via market investments. Blending secure income with growth-oriented equities ensures you pay baseline bills while affording travel.

Tax Efficiency and Healthcare Planning

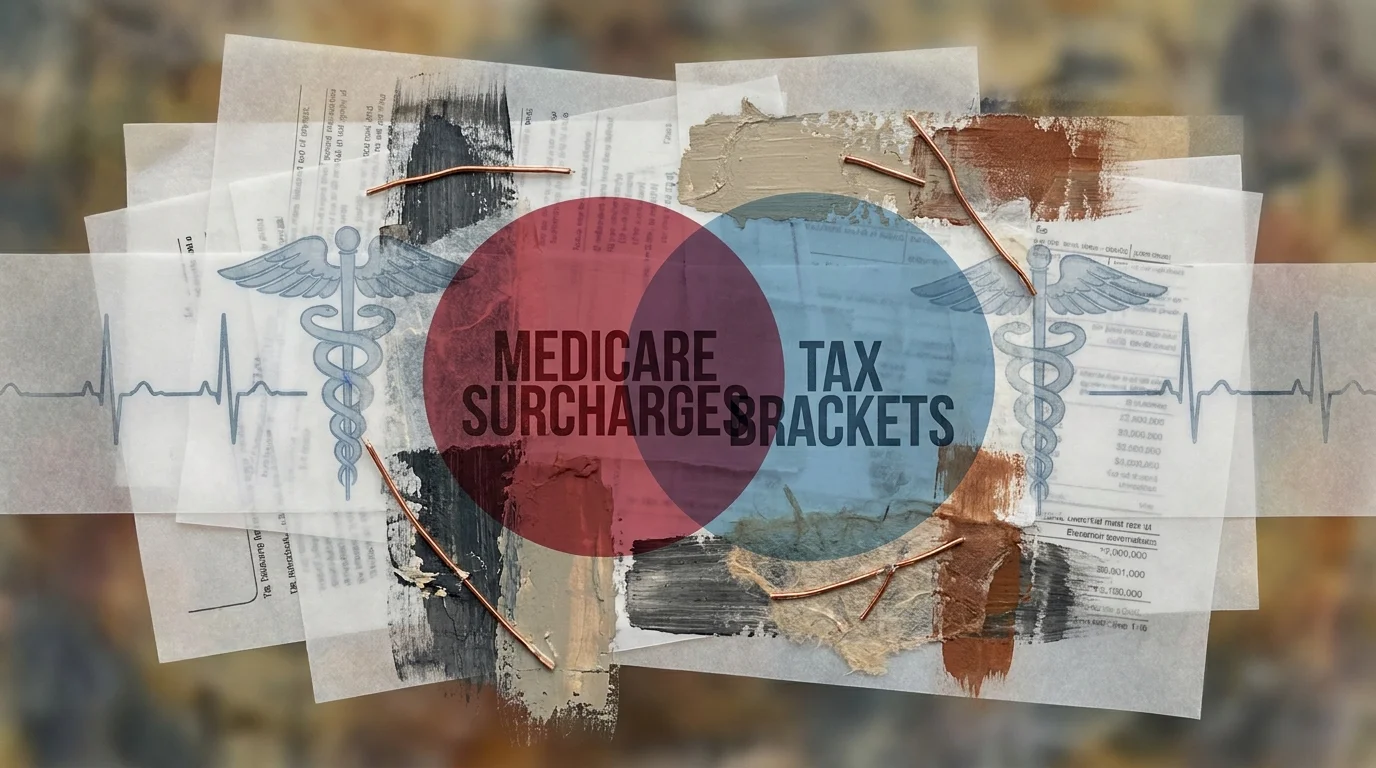

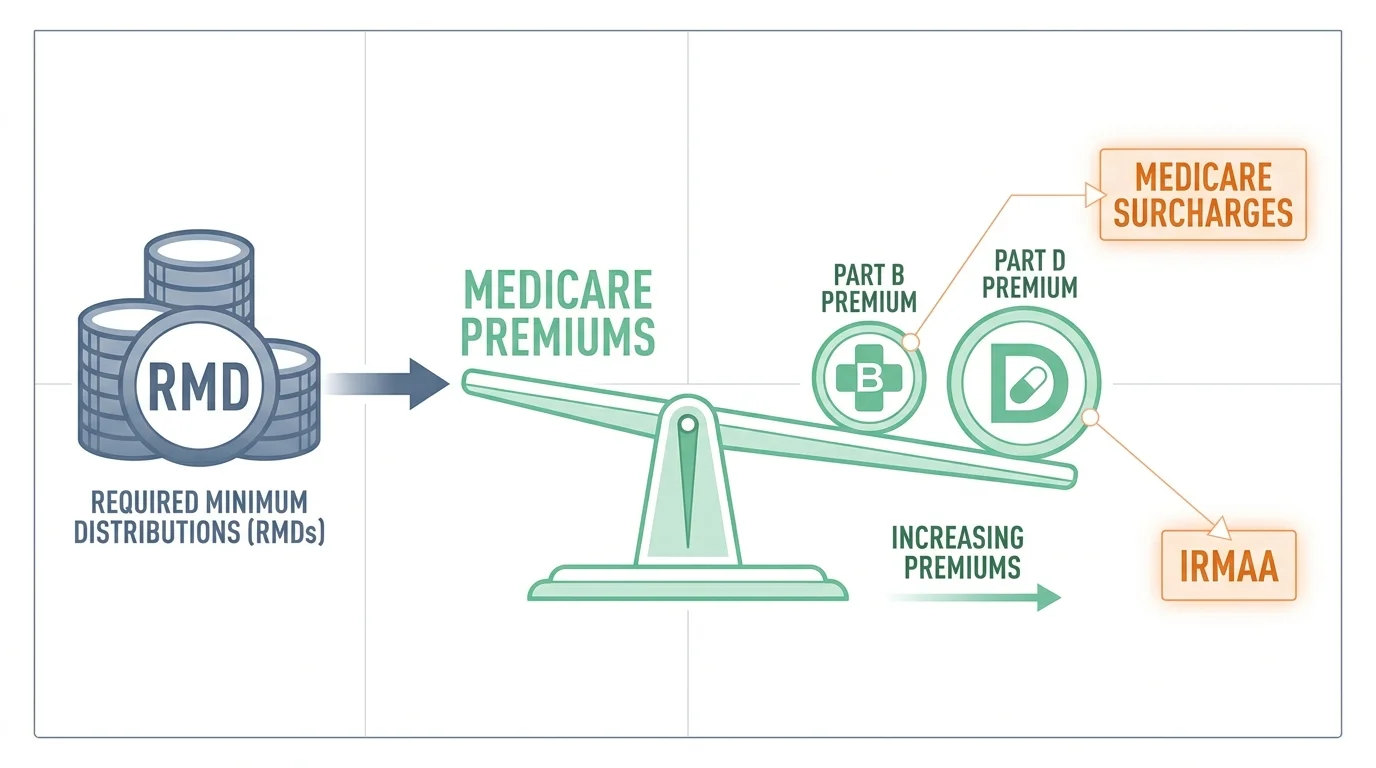

4. How Will Required Minimum Distributions Impact My Medicare Premiums?

Navigating healthcare costs requires meticulous tax planning regarding your federal Medicare premiums. Once you turn age seventy-three or seventy-five, the government forces you to take required minimum distributions from tax-deferred accounts. These mandatory withdrawals act as taxable income and artificially inflate your modified adjusted gross income. Ask your advisor how they plan to manage distributions so you do not trigger the Income-Related Monthly Adjustment Amount. This hidden surcharge can double or triple standard Medicare premiums. A skilled planner proposes proactive tax strategies, such as executing Roth conversions during early retirement when earned income drops. Paying taxes at today’s lower rates shrinks pre-tax balances, reducing future mandatory withdrawals and keeping you below the Medicare surcharge limits.

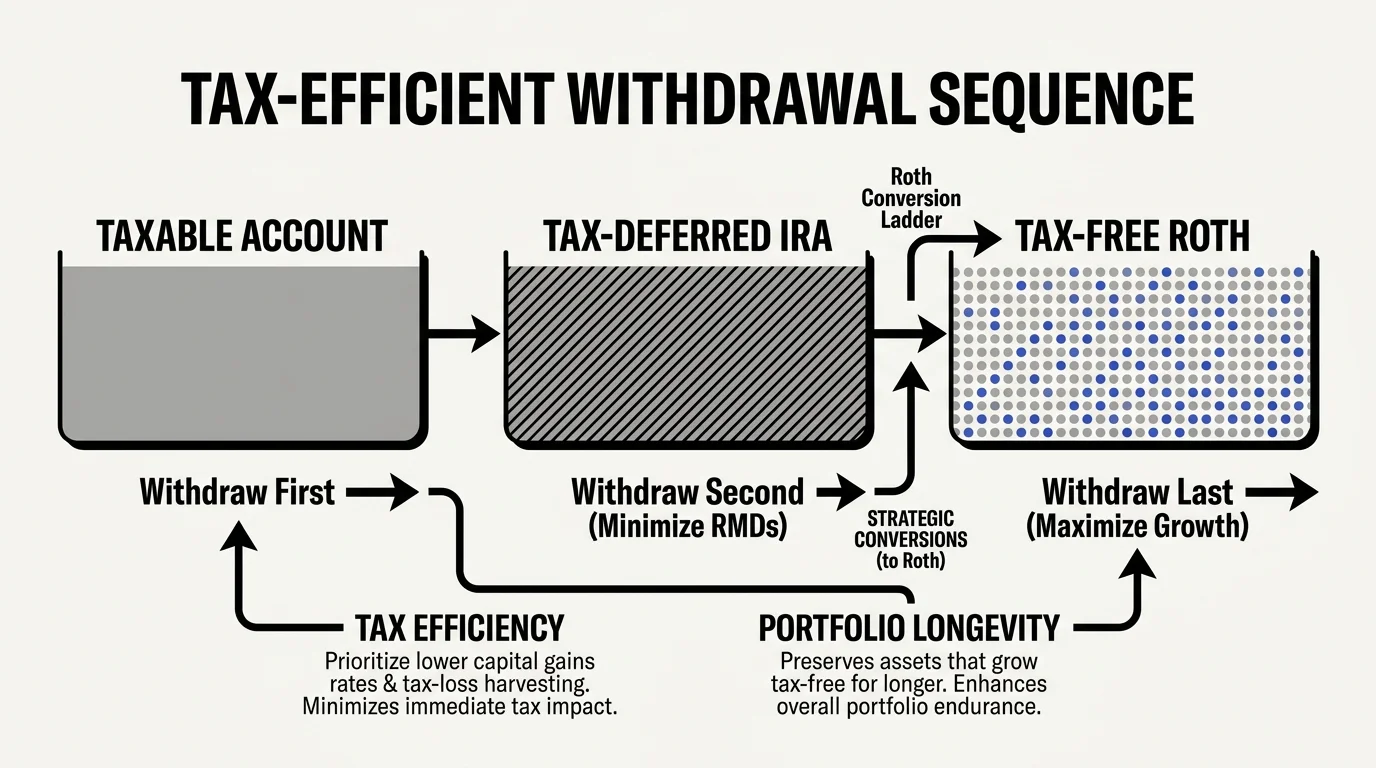

5. What Is Your Strategy for Tax-Efficient Withdrawals Across Multiple Accounts?

Your life savings likely sit in a combination of taxable brokerage accounts, tax-deferred accounts like traditional IRAs, and tax-free Roth IRAs. Your financial advisor must detail the exact sequence they use to drain these buckets. Liquidating assets in the wrong order easily propels you into a higher marginal tax bracket and triggers unexpected capital gains taxes. Ask about their process for tax-loss harvesting, a strategy involving selling targeted investments at a loss to offset taxes owed on broader gains. Additionally, ask about standard deduction planning and charitable giving strategies to lower your tax burden. A robust strategy continuously monitors Internal Revenue Service tax brackets to ensure every dollar pulled from your portfolio minimizes federal and state liabilities.

Asset Protection and Legacy Goals

6. How Do We Address the Risk of Long-Term Care Expenses?

Ignoring the cost of extended medical care is the fastest way to bankrupt a carefully constructed retirement plan. With the median cost of a private room in a nursing home exceeding six figures annually, ask your advisor how they intend to protect your portfolio from catastrophic health expenses. Many seniors falsely believe standard government programs cover custodial care; however, these programs generally only pay for limited skilled nursing care. Your advisor should present viable options ranging from traditional long-term care insurance to hybrid life insurance policies offering chronic illness riders. If you possess substantial wealth, discuss self-funding your care directly. This approach requires rigorously stress-testing investments to guarantee an extended illness will not impoverish your surviving spouse.

7. How Do You Protect My Portfolio Against Fraud and Excessive Volatility?

As you transition into retirement, preserving hard-earned capital becomes just as crucial as growing it. Ask your financial advisor to explain specific guardrails used to protect assets against extreme market volatility and external fraud. Your portfolio asset allocation must shift to match your new risk tolerance, heavily weighting high-quality bonds to cushion against sudden market crashes. Beyond standard market risks, cognitive decline makes seniors prime targets for sophisticated financial scams. A trustworthy planner establishes strict protocols for identifying suspicious withdrawal requests and requires naming a trusted contact person on major accounts. Independently verify your advisor’s background and disciplinary history using the FINRA BrokerCheck tool before giving them control over your savings.

8. Does My Estate Plan Seamlessly Integrate With My Financial Strategy?

Your financial strategy remains dangerously incomplete if it does not seamlessly align with formal estate planning documents. Ask your advisor how they coordinate with an estate attorney to ensure assets transfer smoothly to heirs or chosen charities. Beneficiary designations automatically supersede instructions written in your last will. If you fail to update these critical designations after major life events like divorce, assets could easily end up with unintended recipients. Your advisor should conduct a comprehensive review of account titling, discussing benefits of setting up a revocable living trust to avoid the costly probate process. They must also calculate the impact of the step-up in basis provision, eliminating massive capital gains taxes for heirs upon your passing.

Frequently Asked Questions

How does part-time work affect my Social Security and taxes?

Continuing to work part-time during retirement introduces specific complications regarding government benefits and taxation. If you claim Social Security before reaching full retirement age and continue earning wages, you face the retirement earnings test. The government temporarily withholds a portion of your benefits if earned income exceeds the strict annual limit. Although you eventually recoup withheld funds after reaching full retirement age, the temporary reduction severely disrupts current cash flow. Furthermore, wages remain subject to standard payroll taxes and push overall income into a higher bracket where more Social Security benefits become federally taxable. Consult your planner to find the threshold where working part-time yields a net positive outcome for your budget.

What investments serve as the most effective inflation hedges during retirement?

Inflation poses a silent but devastating threat to purchasing power over a decades-long retirement horizon. To combat the steadily rising cost of living, your advisor should allocate a dedicated portion of your portfolio to specific inflation-hedging assets. Treasury Inflation-Protected Securities provide a government-backed guarantee that your principal will adjust upward alongside the Consumer Price Index. High-quality, dividend-growth stocks also prove vital, as companies with strong cash flows consistently increase dividend payouts to outpace inflation. Additionally, real estate investment trusts offer crucial exposure to tangible property, which historically retains value as rents rise. Maintaining an overly conservative portfolio consisting entirely of cash guarantees you will safely lose purchasing power as everyday household expenses soar.

How do I evaluate the fees my financial advisor charges?

Understanding exactly how your planner gets compensated is critical for aligning financial incentives with long-term success. Advisors typically charge a percentage of assets under management, a flat annual retainer, or an hourly rate for specialized consulting. Demand an itemized, written breakdown of all expenses, including underlying expense ratios of mutual funds selected for your portfolio. Hidden investment fees easily erode hundreds of thousands of dollars from compound returns over your lifetime. Ensure your advisor explicitly states in writing that they operate under a strict fiduciary duty, meaning they are legally obligated to place your financial interests above their own sales commissions. Research advisor firm structures and fiduciary definitions via the Securities and Exchange Commission.

What immediate steps should a surviving spouse take to secure their finances?

Losing a spouse is an emotionally devastating event carrying immediate financial ramifications. In the direct aftermath, a surviving spouse should avoid making irreversible financial decisions, such as selling a primary residence or liquidating large portfolios. The immediate priority is contacting the government to report the death and apply for survivor benefits, allowing the widow or widower to step into the deceased spouse’s larger monthly benefit amount. Next, work closely with your financial advisor to retitle joint banking accounts, claim relevant life insurance proceeds, and update your own outstanding estate planning documents. Transitioning from married filing jointly to single tax filing status often results in higher tax liabilities; your planner must rapidly adjust withdrawal strategies to account for this sudden shift.

Final Steps for Your Retirement Plan

Securing a comfortable retirement requires far more than merely hitting an arbitrary numeric target in your bank account. You must proactively manage the delicate transition from saving to spending by forcing your financial planner to articulate a cohesive, data-backed strategy. Do not accept vague assurances that your money will last; demand concrete mathematical models illustrating exactly how investments generate sustainable cash flow during turbulent economic climates. Gather your most recent investment statements, tax returns, and life insurance policies, and schedule a comprehensive pre-retirement review today. By aggressively tackling crucial conversations surrounding tax efficiency, healthcare risks, and optimal withdrawal sequencing, you empower yourself to make highly informed decisions. Taking control of your financial narrative right now ensures your senior years are defined by absolute financial confidence.