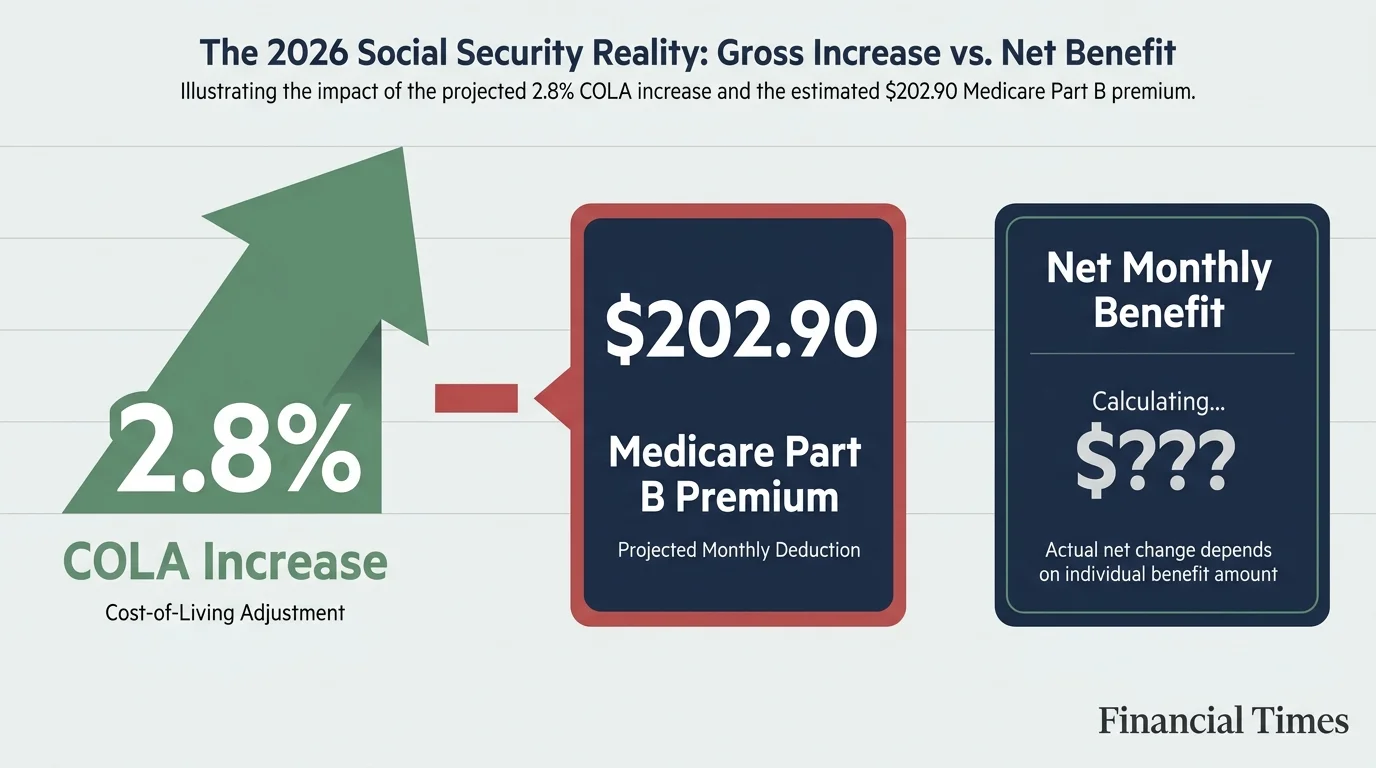

Your 2026 Social Security benefits come with critical updates that demand a proactive review of your financial strategy. With the recent 2.8% Cost-of-Living Adjustment bumping up checks, you need to know exactly how much of that raise actually stays in your pocket after Medicare deducts its new $202.90 monthly premium.

Understanding this year’s higher earnings limits and tax thresholds helps you avoid surprise benefit reductions and protect your fixed income. Whether you navigate full retirement or balance part-time work, examining these current figures guarantees you maximize your retirement benefits.

Taking just ten minutes today to calibrate your income plan against these specific metrics keeps your goals securely on track.

A Snapshot of the 2026 Social Security Landscape

The year 2026 introduces a distinct financial environment for beneficiaries relying on federal retirement programs. The Social Security Administration implemented a 2.8% cost-of-living adjustment this year, a modest increase designed to help your monthly payments keep pace with inflation.

While any increase provides welcome relief, you must view this adjustment through the lens of rising baseline healthcare costs. Specifically, the standard Medicare Part B premium climbed to $202.90 per month in 2026.

Because Medicare premiums are automatically deducted from your Social Security payments before the money ever reaches you, your net increase—the actual cash deposited into your bank account—might feel significantly smaller than the official percentage suggests.

Understanding this dynamic requires a shift in how you evaluate your purchasing power. Many retirees operate on fixed budgets, making them particularly sensitive to price fluctuations at the grocery store, the pharmacy, and the gas pump.

A gross increase in benefits provides a psychological boost, but your financial planning must center on the net yield. Furthermore, the maximum taxable earnings limit for Social Security increased to $184,500 in 2026.

This threshold dictates that individuals still active in the workforce pay Social Security taxes on a larger portion of their annual income. Conducting a thorough retiree benefits review right now ensures you do not overspend based on gross assumptions rather than net realities.