Three Pillars to Optimize Your Social Security Strategy

Achieving financial stability requires more than passively receiving a monthly deposit. You must actively manage your benefits across three distinct domains to successfully navigate these social security changes.

Income Planning: Working Without Triggering the Earnings Test Penalty

Many retirees choose to work part-time to supplement their fixed income, stay socially engaged, or pursue lifelong passions. If you claim Social Security before reaching your full retirement age, you must monitor your earned income meticulously.

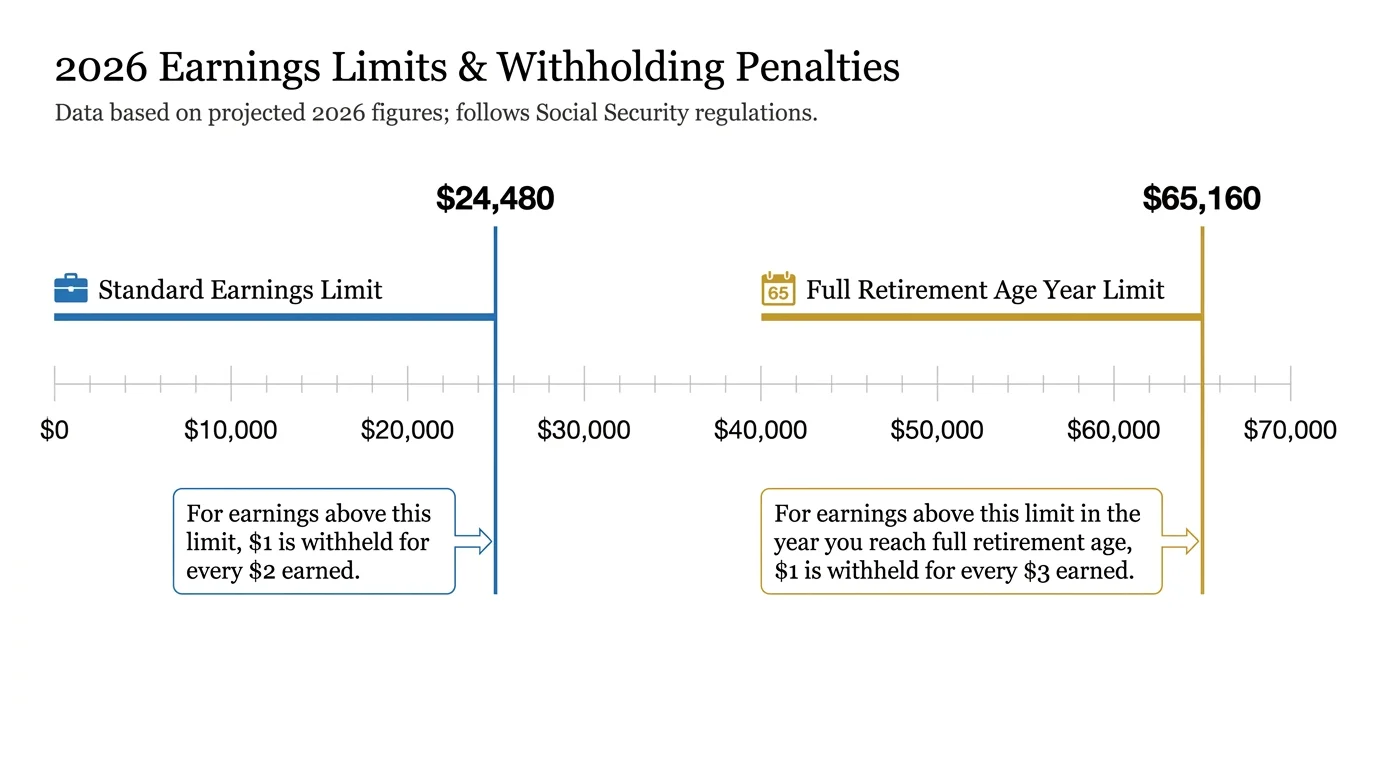

For 2026, the retirement earnings test exempt amount sits at $24,480 per year, or $2,040 per month. If your wages exceed this limit, the Social Security Administration withholds one dollar in benefits for every two dollars you earn above the threshold. This withholding can severely disrupt your anticipated cash flow if you fail to plan for it.

During the specific calendar year you reach your full retirement age, the rules become more forgiving. The earnings limit jumps to $65,160 in 2026, and the government withholds just one dollar for every three dollars earned above that higher limit.

Once you officially reach your full retirement age, the earnings test vanishes entirely. You can earn an unlimited amount of money without facing any benefit reductions based on your wages.

You must recognize that the withheld money does not disappear forever. The Social Security Administration recalculates your benefit amount after you reach full retirement age to account for the months they withheld payments, resulting in a permanently higher monthly check going forward.

However, managing your immediate liquidity requires you to predict these withholdings accurately. If you plan to accept a consulting role or pick up seasonal retail work, calculate your projected annual income immediately to avoid unexpected cash flow interruptions.