Understanding your Social Security benefits can mean the difference between a comfortable retirement and years of financial struggle, yet millions of Americans unknowingly leave money on the table. You can secure a stronger financial foundation by learning the nine crucial facts most pre-retirees misunderstand about the system. A recent survey revealed that only a small fraction of older adults could pass a basic test on claiming rules, putting their lifetime income at serious risk. Whether you plan to step away from work tomorrow or ten years from now, mastering these specific provisions empowers you to maximize your monthly checks, protect your surviving spouse, and better integrate these guaranteed benefits into your broader lifestyle and healthcare strategy.

A Snapshot of Today’s Retirement Landscape

Older adults today face a completely different financial environment than previous generations. With traditional pensions largely replaced by volatile investment accounts, guaranteed income sources carry unprecedented weight in your long-term planning. Recent economic shifts—including inflation spikes and subsequent cost-of-living adjustments—have exposed the fragility of fixed-income budgets. Navigating this landscape requires a tactical approach to your available resources.

The Social Security Administration continually adapts its policies, and staying informed protects you from unexpected shortfalls. Financial professionals frequently note that retirees who understand the nuances of their benefits report lower anxiety and a higher quality of life. As you balance varying mobility levels, shifting healthcare needs, and diverse family dynamics, optimizing your claiming strategy becomes a critical component of your overall wellness.

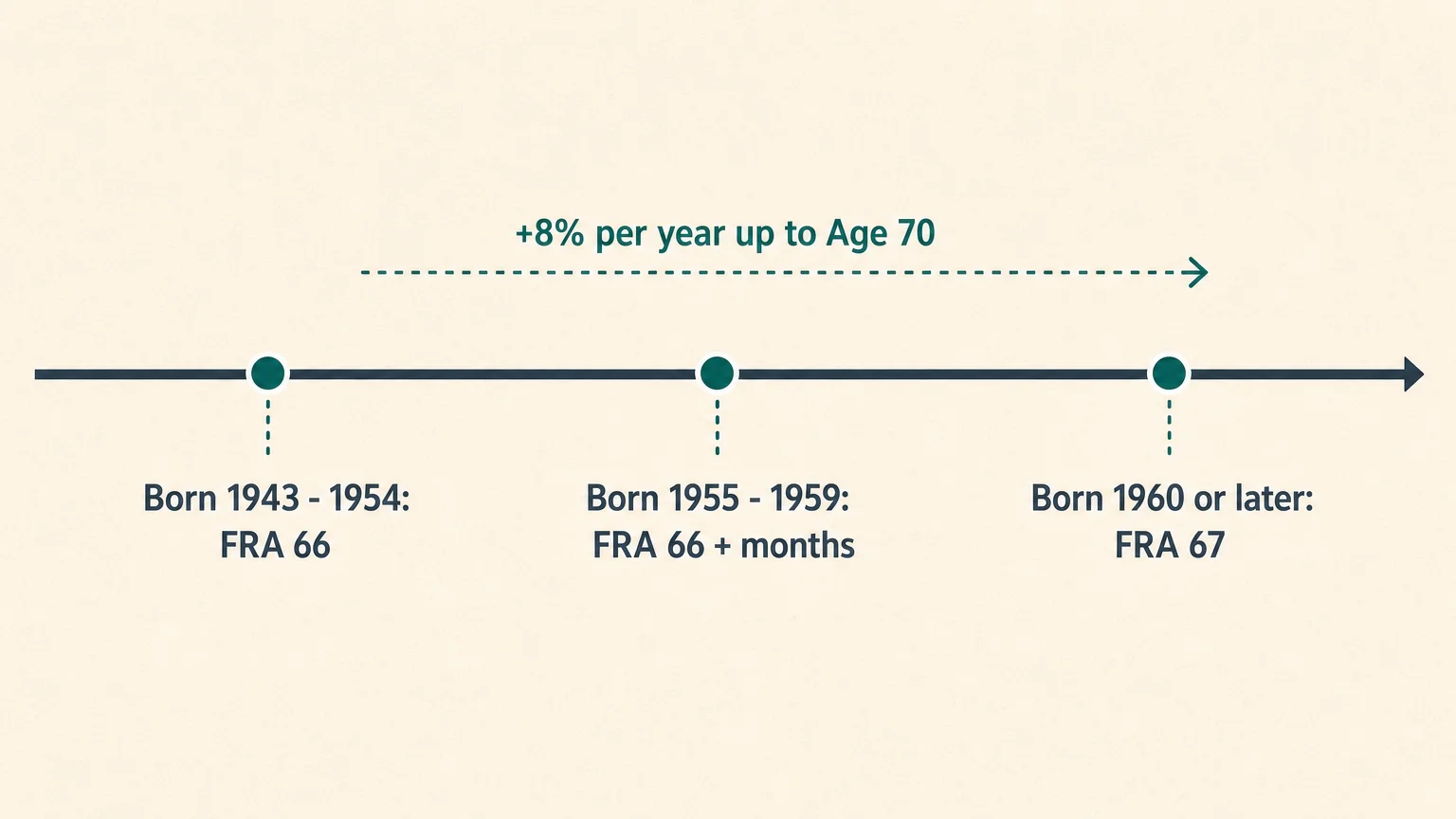

Fact 1: Your Full Retirement Age Is Not Automatically 65

For decades, age 65 served as the universal finish line for American workers. That milestone remains culturally significant, but it no longer guarantees your full, unreduced Social Security benefit. Congressional reforms gradually pushed the full retirement age higher, meaning your specific target depends entirely on your birth year.

If you were born between 1943 and 1954, your full retirement age is 66. For those born between 1955 and 1959, the age increases by two months for every subsequent birth year. Anyone born in 1960 or later must wait until age 67 to receive completely unreduced payments. Filing even one month before your exact milestone triggers a permanent reduction in your monthly check. Conversely, delaying your claim earns you delayed retirement credits, padding your future payouts by eight percent per year up to age 70.

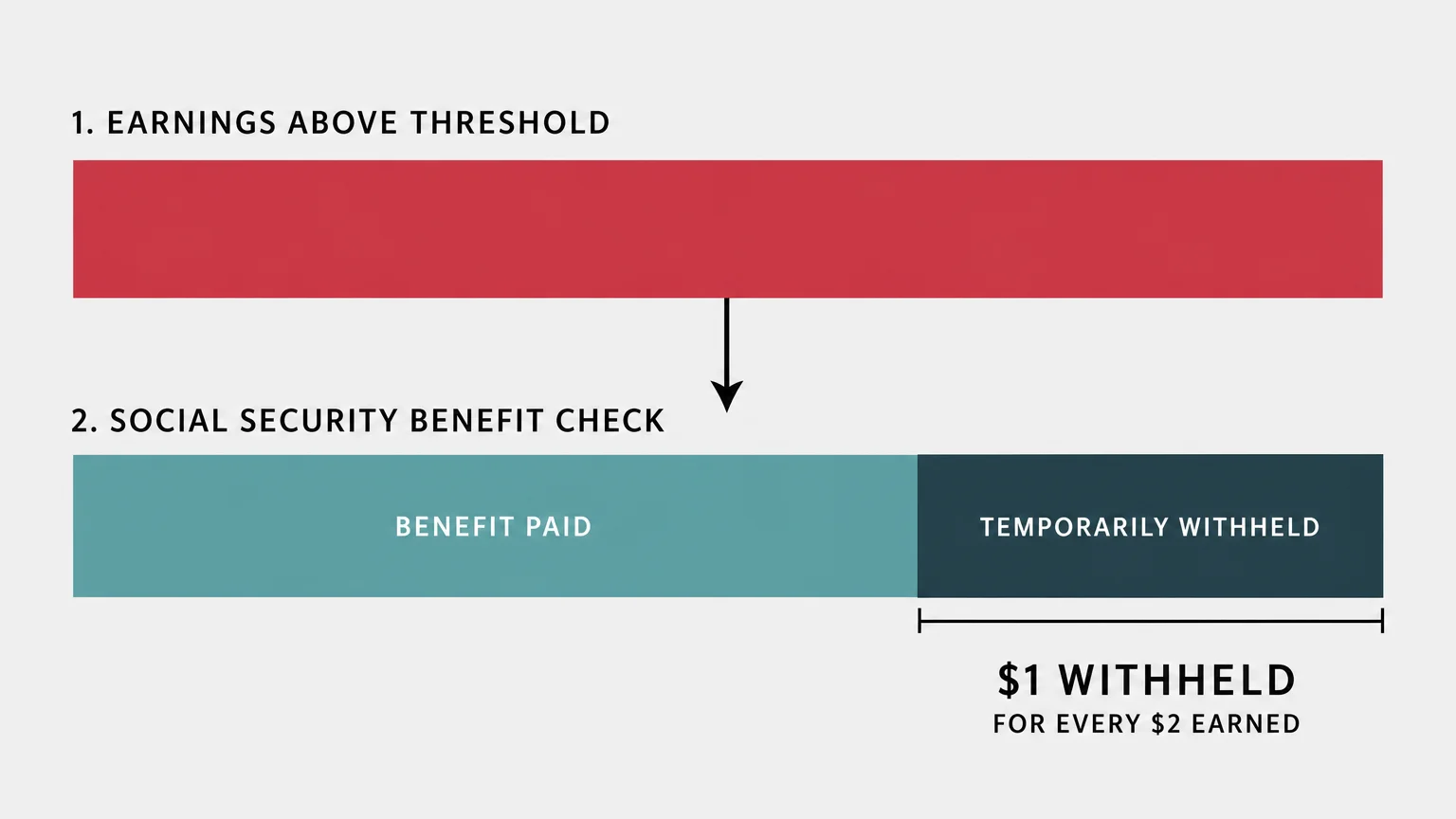

Fact 2: Earning a Paycheck While Claiming Early Triggers the Earnings Test

Many ambitious older adults attempt to transition into retirement by working part-time while simultaneously collecting their benefits at age 62. This strategy frequently triggers the retirement earnings test, a rule that temporarily reduces your checks if your wages exceed an annual limit.

For individuals claiming before their full retirement age, the government withholds one dollar in benefits for every two dollars earned above a specific threshold. Earning too much can result in months of suspended payments, causing frustration for those who rely on that steady cash flow. Fortunately, this withheld money does not vanish. Once you reach your full retirement age, the agency recalculates your monthly payment to account for those previously withheld months, permanently increasing your ongoing checks.

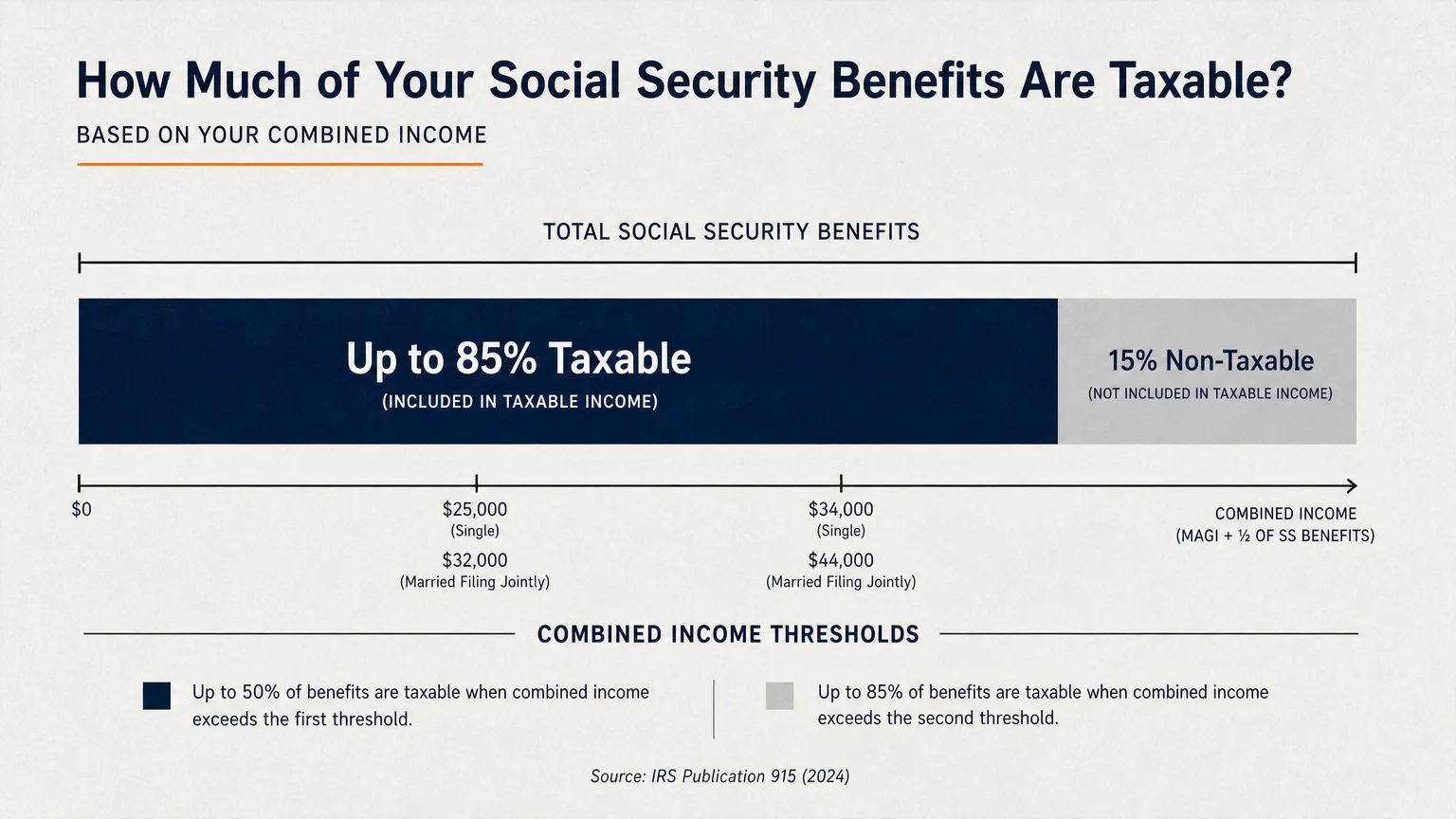

Fact 3: Uncle Sam Might Tax Up to 85 Percent of Your Benefits

A pervasive myth among pre-retirees suggests that Social Security payments remain completely tax-free. In reality, a significant portion of older adults pay federal income taxes on their benefits every year. The calculation relies on a metric called combined income, which adds your adjusted gross income, nontaxable interest, and half of your annual Social Security benefits.

If your combined income exceeds standard limits, you face federal taxation. Single filers exceeding the upper threshold might see up to 85 percent of their benefit exposed to regular income tax rates. Prudent income planning involves managing your withdrawals from traditional retirement accounts to keep your combined income as low as possible. You can explore the tax guidelines for seniors to better project your upcoming liabilities.

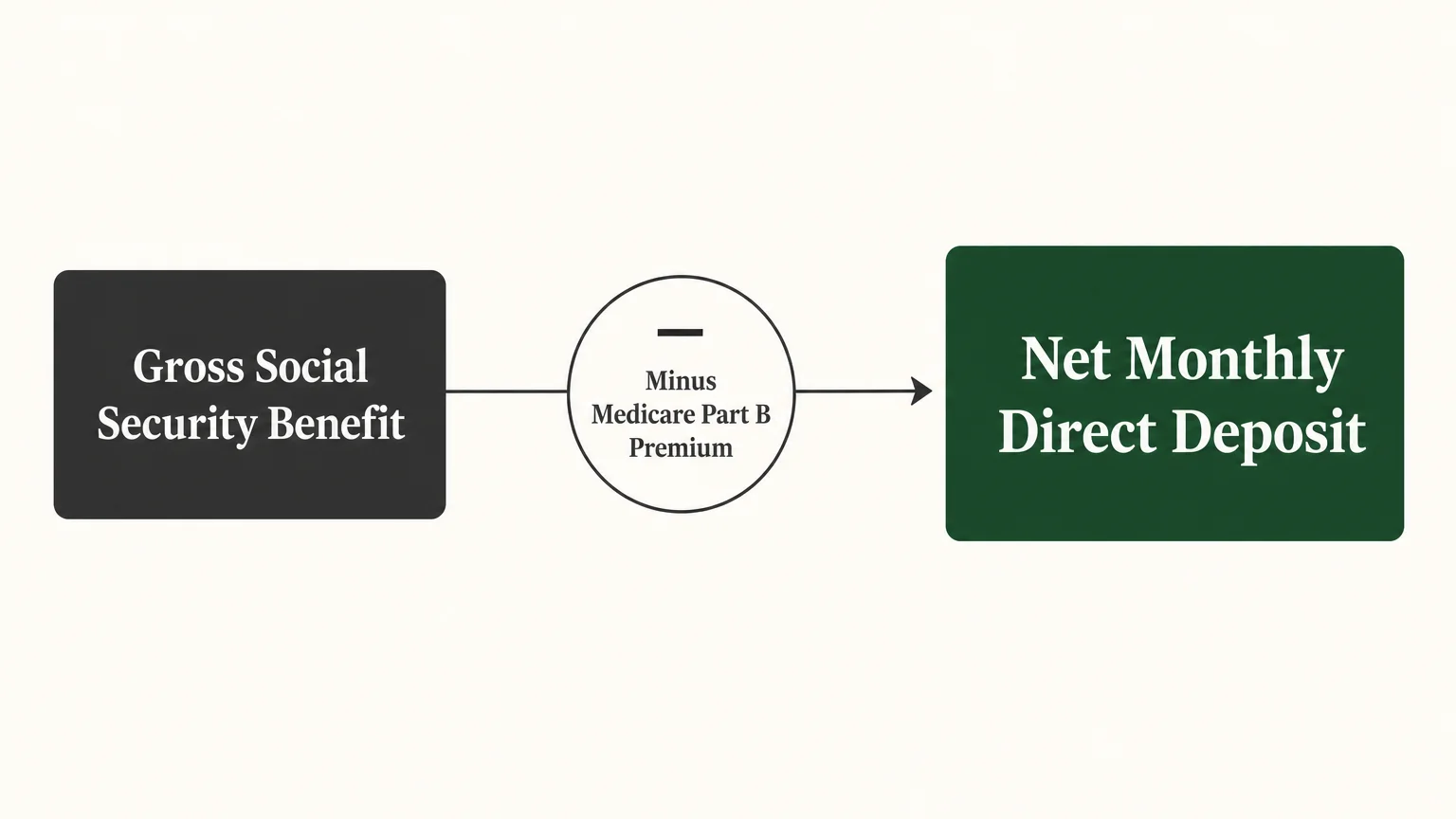

Fact 4: Medicare Premiums Will Shrink Your Net Monthly Payment

Healthcare costs command a massive share of the typical retirement budget, and the intersection between Medicare and Social Security often catches new claimants off guard. When you enroll in Medicare Part B, the government automatically deducts your monthly premium directly from your Social Security check.

This automatic deduction means your actual bank deposit will be noticeably smaller than the gross amount listed on your benefit statement. Furthermore, high-income retirees face additional surcharges known as the Income-Related Monthly Adjustment Amount. A successful financial plan must account for these mandatory healthcare deductions, especially since standard Medicare premiums historically rise at a faster pace than government cost-of-living adjustments. Anticipating this reality helps you build a more resilient monthly budget.

Fact 5: Spousal Benefits Do Not Grow After Full Retirement Age

Married couples hold a distinct advantage when designing their income strategy, but a critical rule governs those claiming strictly on their partner’s work record. A spousal benefit maxes out at exactly 50 percent of the primary worker’s full retirement age amount.

While the primary worker can increase their own payout by delaying their claim up to age 70, the spousal benefit stops growing the moment the claiming spouse reaches their own full retirement age. Delaying a purely spousal claim beyond that point simply forfeits months of income without delivering any corresponding financial reward. Coordinating these timelines requires open communication; the primary earner must actively file for their own benefits before their partner can initiate a spousal claim.

Fact 6: Divorced Retirees Carry Hidden Claiming Power

Ending a marriage does not necessarily sever your ties to your former partner’s earnings record. If your marriage lasted for at least ten consecutive years and you remain unmarried, you hold the legal right to claim a benefit based on your ex-spouse’s work history.

This powerful provision allows you to collect up to half of your former partner’s full retirement amount without their permission. Their current marital status holds no bearing on your eligibility; even if they remarried, your claim remains completely valid and causes zero reduction to the checks received by them or their new spouse. You merely need to demonstrate that both you and your ex-spouse are at least 62 years old, offering a vital financial lifeline.

Fact 7: Surviving Spouses Have Highly Flexible Claiming Options

Losing a spouse brings profound emotional and financial challenges, but the system provides specialized safety nets to protect surviving partners. Unlike standard spousal claims, survivor benefits offer unique flexibility that can dramatically enhance your long-term financial security.

Widows and widowers possess the rare ability to restrict their application to just one type of benefit while letting the other grow. For example, a surviving partner could claim a reduced survivor benefit at age 60, allowing their own personal retirement benefit to accrue delayed credits until age 70. At that point, they can seamlessly switch over to their own maximized payment. This dual-entitlement strategy shields vulnerable retirees from poverty and secures a robust income stream for their remaining years.

Fact 8: The Government Will Never Call to Suspend Your Number

Financial security involves more than just optimizing your claims; it requires vigilant protection against those attempting to steal your assets. Fraud rings constantly target older adults, utilizing sophisticated impersonation tactics to drain bank accounts.

You must remember that legitimate federal employees will never call you out of the blue to threaten arrest or claim your Social Security number has been suspended. They will never demand immediate payment via gift cards or wire transfers. Official communication always begins with a formal letter sent through the postal service. Should you receive a suspicious call, hang up immediately and report the incident to the Office of the Inspector General. Safeguarding your personal information remains vital.

Fact 9: Taking Benefits Early Does Not Mean You Failed

Financial media frequently champions age 70 as the ultimate goal for claiming, emphasizing the raw mathematical advantage of delayed credits. However, optimal spreadsheet math rarely accounts for the nuanced realities of human life. Taking your benefits at age 62 is not a failure; for many, it represents the most rational and practical choice available.

If you face chronic health conditions or possess a shorter-than-average life expectancy, claiming early ensures you receive as much money as possible while you can still enjoy it. Early claiming also makes sense if utilizing those funds prevents you from depleting your retirement portfolio during a severe market downturn. Ultimately, the correct age to file depends entirely on your personal health outlook and legacy goals.

Expert Voices on Modern Retirement Strategy

Navigating these complex regulations requires insight from professionals who witness the real-world impact of claiming decisions every day. Certified Financial Planner professionals consistently observe that a coordinated income strategy—one harmonizing Social Security, pensions, and personal investments—delivers the highest probability of lifelong success. They advise pre-retirees to view their guaranteed federal benefits as the foundational layer of their income floor, a stable base designed to cover essential living expenses regardless of stock market fluctuations.

Beyond the numbers, gerontologists remind us that financial security serves a higher purpose: maintaining your physical and mental health. A predictable monthly income drastically reduces chronic stress, a known contributor to cognitive decline. Experts agree that approaching your claiming decision comprehensively empowers you to design a fulfilling lifestyle.

Frequently Asked Questions About Your Benefits

Can I stop my benefits and restart them later?

Yes, the system allows for course corrections. If you change your mind within twelve months of your initial claim, you can withdraw your application entirely. You must repay all the money you and your family received. Alternatively, once you reach your full retirement age, you can voluntarily suspend your payments to earn delayed credits until age 70.

Does moving to a different state affect my base benefit?

Your federal payout remains exactly the same regardless of your zip code. However, your geographic location significantly impacts your net income due to varying state tax laws. A handful of states tax Social Security benefits at the local level. Factoring state-level taxation into relocation plans prevents unwelcome surprises.

Will my benefits decrease if the trust fund runs dry?

While the primary trust funds face a projected shortfall in the mid-2030s, this does not mean benefits will disappear entirely. Ongoing tax revenues collected from current workers will continue funding a significant majority of promised payouts. Congress possesses numerous legislative tools to bridge this gap long before any automatic reductions occur.

How do pensions from jobs that did not pay Social Security taxes affect me?

If you spent part of your career in a specialized sector—such as certain state or local government roles—and earned a pension without paying payroll taxes, two specific provisions may reduce your benefits. The Windfall Elimination Provision applies to your personal earnings record, while the Government Pension Offset reduces spousal or survivor benefits. Reviewing these rules early prevents you from overestimating your future household income.

One Step Forward

Knowledge serves no purpose without decisive action. You hold the power to shape your financial destiny, and clarity begins with understanding exactly where you stand today. In the next 48 hours, commit to downloading your most recent benefit statement directly from the government portal.

Creating your secure my Social Security account requires only a few minutes, giving you immediate access to your earnings history and personalized payout estimates. Verify that your past wages are recorded accurately, as errors could permanently diminish your future checks. Taking this single step transitions you into the active architect of your retirement security.