Understanding your projected 2027 Social Security payments gives you the clarity needed to secure a comfortable and resilient retirement. Recent data shows that nearly sixty percent of retirees rely on these monthly checks for at least half of their income, making accurate projections essential for your peace of mind. While exact figures depend on ongoing inflation and wage growth metrics, early economic indicators suggest a moderate cost-of-living adjustment may be on the horizon. Knowing what to expect allows you to bridge potential income gaps, optimize your retirement withdrawals, and design a lifestyle that matches your fixed budget. By taking control of your financial forecast today, you protect your independence and ensure your retirement years remain vibrant.

A Snapshot of the Current Policy and Economic Landscape

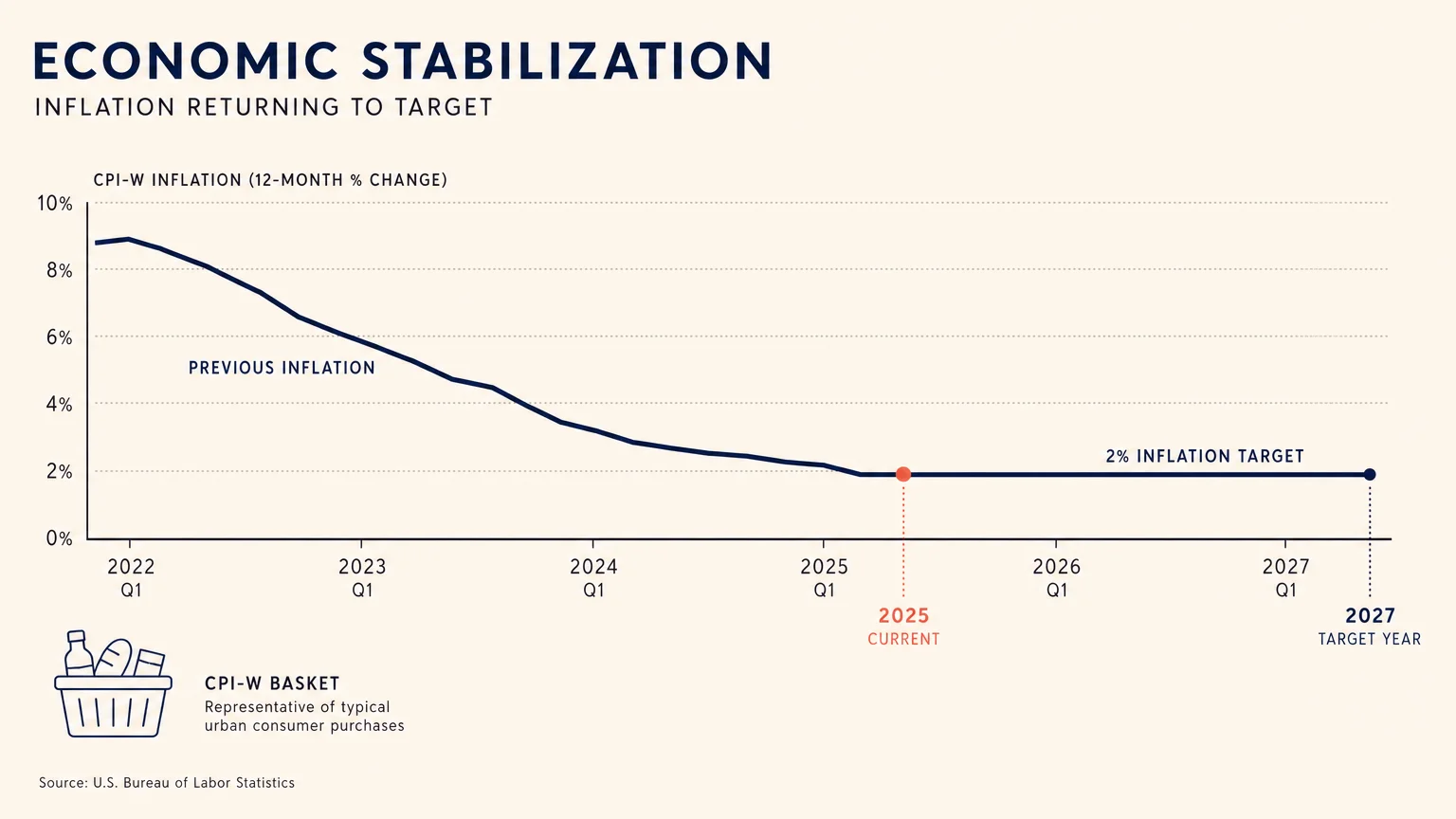

The economic turbulence of the early part of this decade fundamentally shifted how retirees view their fixed incomes. As we move through the current year and look toward 2027, inflation has largely cooled from its historic peaks, approaching the Federal Reserve’s long-term target of two percent. Because the federal government calculates the annual cost-of-living adjustment using specific economic data gathered during the third quarter of the year, stabilizing consumer prices point toward a modest increase for 2027 Social Security payments.

To understand what your checks might look like, you have to look at the mechanics behind the math. The adjustment is tied directly to the Consumer Price Index for Urban Wage Earners and Clerical Workers, which tracks the shifting costs of a specific basket of goods and services. Rather than the massive leaps seen in recent memory, financial analysts anticipate a return to normalized adjustments. A smaller adjustment signals that the broader economy is reaching a healthy equilibrium, meaning your daily expenses at the grocery store and the gas pump should stop climbing at a dizzying pace.

However, a smaller bump in your monthly check requires precision in your household budgeting. When your income rises by a modest margin, you must actively evaluate whether your personal rate of inflation aligns with the national averages. Retirees often spend significantly more on healthcare and housing than the urban workers measured by the official index. Understanding this macroeconomic transition provides the foundational context you need to optimize your retirement strategy before the new year arrives.

Income Planning: Navigating the 2027 Social Security Landscape

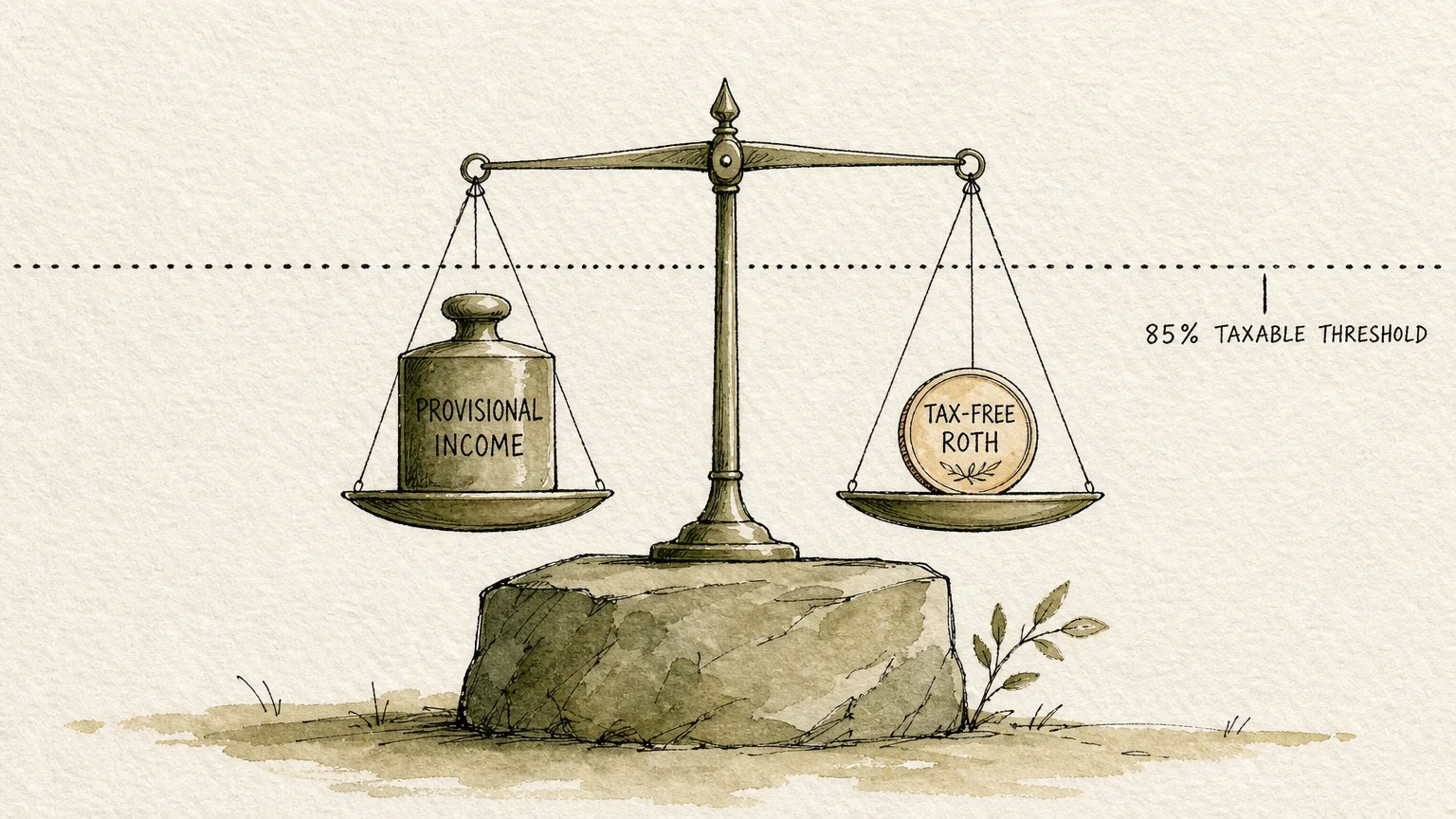

Building a robust income plan for 2027 requires you to look beyond the gross amount of your Social Security payment and focus heavily on your net spendable income. One of the most significant challenges modern retirees face is the taxation of benefits. The federal government established the base income thresholds for taxing Social Security back in the 1980s; because lawmakers never indexed these thresholds to inflation, a growing percentage of retirees find themselves owing federal taxes on their benefits each year.

If your combined provisional income—which includes your adjusted gross income, your nontaxable interest, and half of your Social Security benefits—exceeds specific limits, up to eighty-five percent of your payment may become taxable. As moderate cost-of-living adjustments accumulate over the years, they predictably push middle-income retirees over these stagnant thresholds. You can mitigate this hidden tax trap by strategically timing your withdrawals from traditional individual retirement accounts or leaning heavily on tax-free Roth accounts to keep your combined income below the taxation tripwires.

Certified financial planners routinely emphasize the importance of holistic withdrawal strategies. Many industry professionals advise treating Social Security as a steady foundation rather than a standalone financial solution. Analyzing your projected income streams eighteen months in advance allows you ample time to harvest capital gains efficiently or execute strategic Roth conversions during lower-tax years. By proactively estimating your future payments using official benefit estimators, you gain the exact data needed to harmonize your government benefits with your personal savings, ensuring you keep more of your hard-earned money out of the hands of the taxman.

Lifestyle Design: Stretching Your Monthly Benefits

Projecting your 2027 Social Security payments empowers you to make intentional choices about your daily lifestyle and your living arrangements. When you know roughly how much steady income will hit your bank account each month, you can confidently design a life that maximizes joy while minimizing financial stress. Housing remains the largest single expense for most retirees, and your physical environment plays a massive role in both your economic and physical wellbeing.

Consider evaluating your current home for long-term accessibility and cost-efficiency. If a large portion of your projected 2027 income will go toward property taxes, rising utility bills, and demanding maintenance for a sprawling property, you might find profound freedom in downsizing to a community specifically designed for older adults. Alternatively, investing a portion of your current savings into permanent accessibility modifications—such as walk-in showers, zero-step entryways, and enhanced interior lighting—can help you safely age in place without relying on expensive assisted living facilities later.

Furthermore, lifestyle design involves aligning your spending with your deepest values and your cultural background. Retirees from diverse cultural backgrounds often prioritize unique family dynamics, such as multi-generational living or traveling frequently to visit relatives across the country. You can stretch your monthly benefits by adopting a mindful approach to shared resources. Embracing community-sponsored arts programs, utilizing senior transit discounts, and sharing utility overhead within a multi-generational household can drastically reduce your monthly burden. When you actively shape your environment to support your physical mobility and your fixed budget, you transform your Social Security checks from a mere survival mechanism into a tool for a deeply fulfilling lifestyle.

Health and Wellness: Anticipating Medicare Premium Shifts

You cannot accurately project your 2027 Social Security payments without accounting for the consistently rising costs of healthcare. For the vast majority of U.S. retirees, Medicare Part B premiums are deducted directly from their monthly Social Security checks before the funds ever reach their bank accounts. Historically, healthcare costs rise at a faster rate than general consumer goods, meaning your Medicare premiums often consume a disproportionate share of your annual cost-of-living adjustment.

As you forecast your 2027 budget, you must prepare for the likelihood that premium increases could offset a noticeable fraction of your gross payment increase. Reviewing historical data published regarding projected Medicare premium costs reveals a steady upward trajectory driven by the introduction of expensive new medical therapies and broader utilization of services. To protect your monthly cash flow, you should routinely evaluate your supplemental insurance policies and your prescription drug coverage during the annual open enrollment period.

High-income retirees must also watch out for the Income-Related Monthly Adjustment Amount, commonly known as IRMAA. This surcharge increases your Medicare Part B and Part D premiums based on your modified adjusted gross income from two years prior; therefore, your 2025 income directly dictates your 2027 Medicare premiums. If you plan to sell a large asset or execute a massive retirement account withdrawal, you must factor in how that income spike will reduce your net Social Security check two years down the line.

Beyond navigating complex insurance premiums, investing in your daily physical health is arguably the most effective financial strategy you can deploy. Gerontologists overwhelmingly agree that adopting a proactive wellness routine reduces the frequency and severity of out-of-pocket medical expenses. Simple actions—such as engaging in supervised strength training to prevent debilitating falls, adopting a nutrient-dense diet, and maintaining strong social connections to ward off cognitive decline—yield massive economic dividends. By prioritizing preventative care today, you effectively insulate your 2027 Social Security payments from the devastating drain of unexpected medical emergencies.

Safeguarding Your Benefits: Risks, Scams, and Benefit Cliffs

While optimizing your income and health forms the core of a strong retirement plan, you must also play aggressive defense to safeguard your hard-earned benefits. The landscape of financial fraud evolves rapidly, and scammers frequently use the announcement of new benefit amounts as a psychological hook to steal your sensitive information. Criminals deploy sophisticated phishing emails and spoofed robocalls claiming that your 2027 cost-of-living adjustment requires immediate verification of your personal details or a small processing fee. The Social Security Administration will never call you demanding money, threatening arrest, or asking for payment via gift cards or cryptocurrency. You must remain incredibly vigilant, verify all communications directly through official channels, and consider freezing your credit files to prevent devastating identity theft.

Beyond external criminal threats, you must also navigate the systemic risks built into the benefits program itself, particularly if you plan to continue working while collecting your payments. If you claim Social Security before reaching your full retirement age and continue to earn income from a job or consultancy, you run the risk of hitting the earnings test cliff. For every two dollars you earn above a specific annual limit set by the government, the agency will temporarily withhold one dollar of your benefits.

Although you eventually receive this withheld money back in the form of higher recalculated payments after reaching your full retirement age, the sudden reduction in your monthly cash flow can wreak havoc on your immediate household budget. Before taking on part-time work or ambitious consulting gigs in 2027, you should consult with tax professionals to calculate exactly how your labor will impact your benefit checks. By understanding the intricate rules surrounding the earnings test and consulting official resources regarding taxable benefit thresholds, you avoid unpleasant surprises and maintain total, unwavering control over your financial trajectory.

Frequently Asked Questions About 2027 Social Security Payments

When will the official 2027 cost-of-living adjustment be announced?

The Social Security Administration traditionally announces the official adjustment for the upcoming year in mid-October. The agency calculates the definitive increase by comparing the average Consumer Price Index data from July, August, and September of the current year to the exact same period from the previous year. You can expect the official numbers for your 2027 payments to be released to the public in October of 2026, allowing you a few months to finalize your upcoming budget.

Will a smaller annual adjustment mean I am losing my purchasing power?

Not necessarily; the adjustment is specifically designed to match inflation, not outpace it. If the adjustment is smaller, it simply indicates that the prices of general goods and services are rising at a slower, more manageable rate. However, because seniors tend to spend a much larger portion of their overall income on healthcare—which predictably inflates faster than general consumer goods—many advocacy organizations tracking retirement security argue that the current calculation method does not perfectly capture the true, day-to-day expenses faced by older adults.

Can I change my withdrawal strategy after claiming my benefits?

While your initial claiming decision permanently locks in your baseline benefit percentage, you retain ultimate flexibility regarding your other retirement accounts. If your 2027 Social Security payments fall short of your living expenses, you can adjust your withdrawals from your individual retirement accounts, sell your taxable investments, or explore alternative income streams. You cannot easily pause your benefits once you reach your full retirement age, but you can always adjust the surrounding financial ecosystem to better support your lifestyle.

How do Medicare Part B premium increases interact with my exact payment amount?

A specific legal provision known as the hold harmless rule protects the vast majority of U.S. retirees from seeing their net Social Security check decrease from one year to the next strictly due to Medicare premium hikes. If the standard Medicare premium increase mathematically exceeds the dollar amount of your annual cost-of-living adjustment, your premium increase is capped. This vital rule ensures your net payment remains at least equal to the previous year, though it unfortunately means you will not see any increase in your actual take-home cash.

Your Next Step Toward Financial Confidence

Looking ahead to 2027 empowers you to transition from a passive recipient of government benefits to an active, engaged architect of your retirement. You possess the essential tools and the fundamental knowledge necessary to align your projected income with a lifestyle that brings you profound satisfaction and security. Achieving real financial clarity completely removes the paralyzing anxiety of the unknown, freeing up your valuable mental energy to focus deeply on your family, your physical health, and your personal passions.

Over the next forty-eight hours, commit to taking one concrete step to strengthen your financial foundation. Log in to your official Social Security portal to review your latest benefit statement, or schedule a brief, focused meeting with your financial advisor to discuss how potential 2027 tax brackets might heavily impact your overall withdrawal strategy. Taking immediate, decisive action builds unstoppable momentum. Your future self will deeply appreciate the diligent preparations you make today, ensuring your retirement remains exactly as you envisioned—resilient, vibrant, and entirely your own.