Maximizing your Social Security check requires precise planning, as this guaranteed monthly income forms the absolute bedrock of a secure retirement. Making an uninformed decision about when and how to claim your benefits can permanently reduce your lifelong payout and jeopardize your financial stability. With changing inflation rates and rising healthcare costs reshaping the American retirement experience, you must actively protect your financial resources. Understanding the exact mechanics of your benefit options allows you to bypass the critical errors that commonly derail otherwise solid financial plans. By taking a proactive approach to your claiming strategy today, you lock in the highest possible monthly payment while ensuring your lifestyle and health needs remain fully funded for decades to come.

A Snapshot of the Current Social Security Landscape

Recent data reveals that a vast majority of American retirees rely on their monthly benefits for at least half of their retirement income. This heavy reliance makes current economic headwinds—such as volatile inflation rates—especially significant for your budget. Policymakers debate funding mechanisms, but your focus must remain on optimizing the system as it operates right now. High interest rates require you to establish a robust income floor. Retirees from diverse cultural backgrounds approach intergenerational wealth differently, requiring tailored strategies that respect family dynamics. Moreover, seniors facing varying mobility challenges must factor in costs for specialized transportation. These personalized variables demonstrate precisely why a one-size-fits-all approach inevitably falls short.

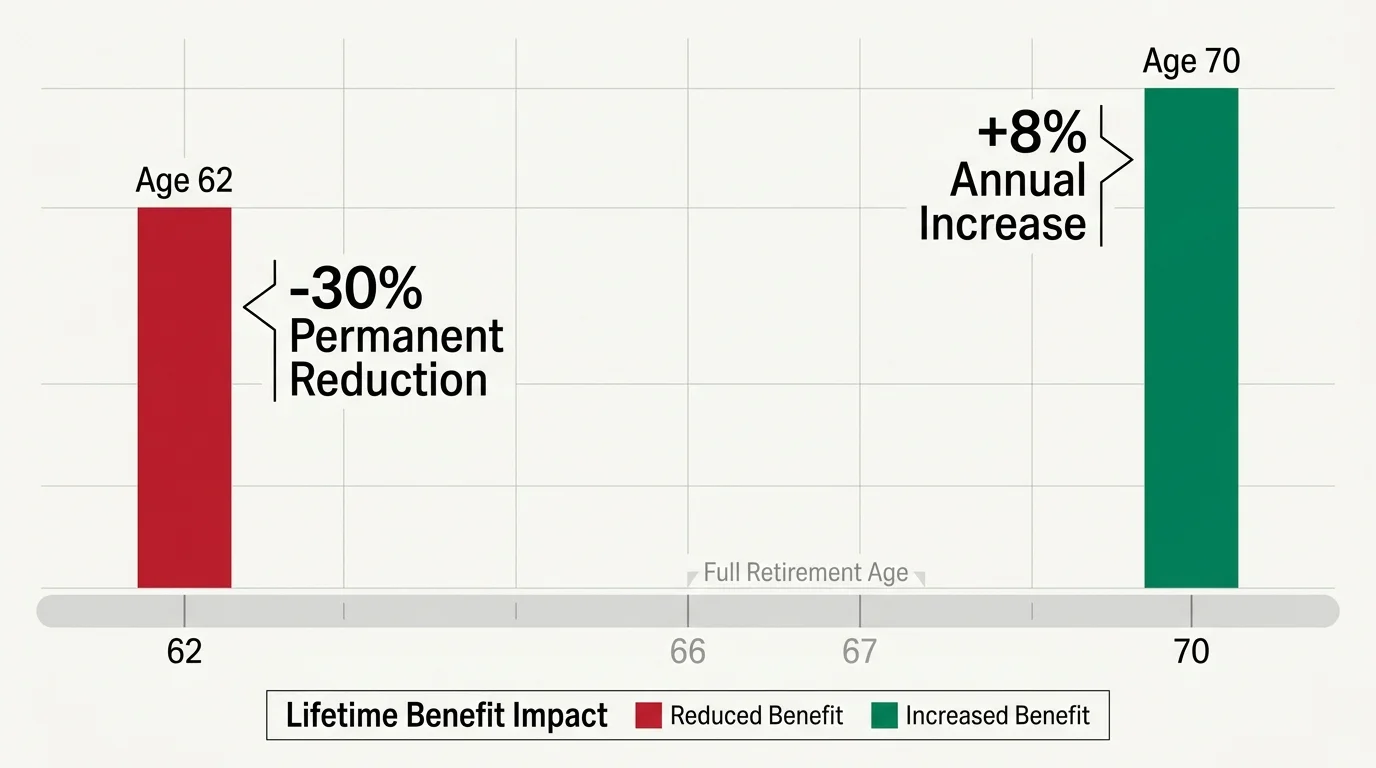

Mistake 1: Claiming Too Early Without a Long-Term Strategy

Filing for Social Security at age sixty-two remains a common and financially detrimental retirement income planning error. While immediate cash proves tempting, claiming early permanently slashes your monthly benefit by up to thirty percent. You must weigh this reduction against your family history of longevity and anticipated lifetime expenses. Delaying your claim until age seventy guarantees an eight percent annual increase in your base benefit amount. This delayed strategy serves as powerful longevity insurance, ensuring you maintain substantial buying power deep into your eighties when medical costs peak. Analyze your complete financial picture before rushing to the filing office. Running the numbers with a qualified professional illuminates the safest path forward.

Mistake 2: Ignoring the Tax Bite on Your Benefits

Many pre-retirees falsely assume their government checks are shielded from federal income taxes. Depending on your combined income—which includes your adjusted gross income, nontaxable interest, and half of your Social Security benefit—you could owe federal taxes on up to eighty-five percent of your monthly payments. Failing to account for this tax burden creates severe cash flow shortages. You must proactively manage your taxable income by strategically drawing from traditional IRAs, Roth accounts, and taxable brokerage accounts. Reviewing the Internal Revenue Service guidelines allows you to smooth out your tax liabilities over multiple decades. Implementing a dynamic withdrawal strategy preserves your hard-earned benefits and shields your portfolio from rapid depletion, directly enhancing your daily quality of life.

Mistake 3: Overlooking Spousal and Survivor Benefit Options

Married couples frequently make the profound error of treating their benefit claiming decisions as isolated events rather than constructing a unified household strategy. Spousal benefits allow a lower-earning partner to claim up to fifty percent of the higher earner’s full benefit, altering the math of your retirement income planning. Furthermore, survivor benefits represent a critical safety net; when one spouse passes away, the surviving partner automatically inherits the higher of the two benefit amounts. If the higher-earning spouse claims early, they permanently handicap the survivor’s future financial security. You and your partner must map out mortality scenarios to ensure the surviving spouse retains a reliable income stream. You can verify your estimates directly through the Social Security Administration website.

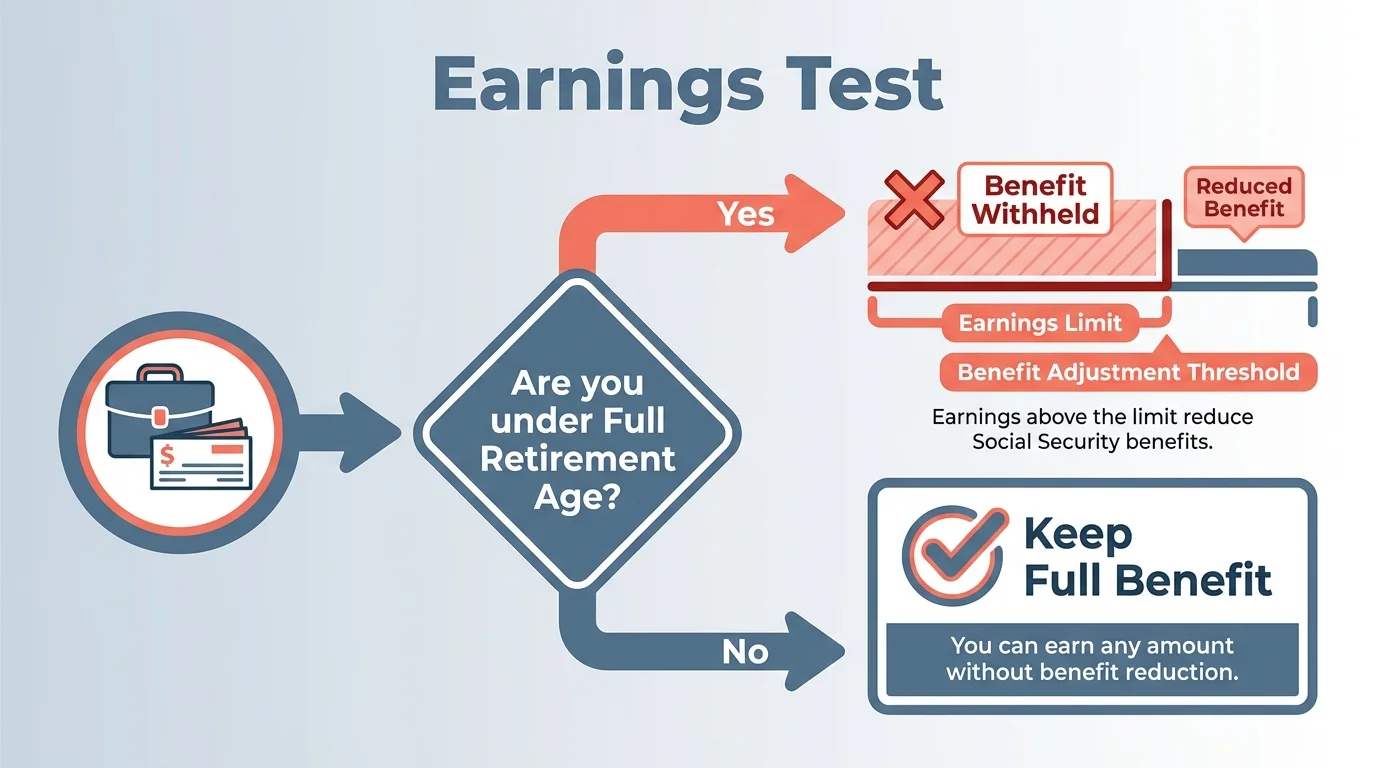

Mistake 4: Working While Claiming Without Understanding the Earnings Test

Maintaining a part-time job or consulting business during your early retirement years provides mental stimulation and valuable supplemental income. However, if you claim benefits before reaching full retirement age and continue to earn wages, you risk triggering the severe retirement earnings test penalty. The government automatically withholds one dollar of your benefits for every two dollars earned above a strictly defined annual limit. While these funds recalculate upward at full retirement age, the temporary cash flow disruption severely damages your budget. You must project your expected wage earnings and synchronize them perfectly with your claiming timeline. Recent Bureau of Labor Statistics data indicates older Americans remain in the workforce longer than ever before. Waiting to claim benefits often proves mathematically sound.

Mistake 5: Failing to Sync Medicare Premiums With Social Security

Your physical health and financial health remain inextricably linked throughout your retirement journey. Many retirees overlook that standard Medicare Part B premiums are automatically deducted from their monthly Social Security checks before funds hit their bank account. As healthcare costs steadily rise, these deductions systematically eat away at your cost-of-living adjustments, leaving you with substantially less net income than you modeled. Additionally, if your modified adjusted gross income exceeds certain thresholds, you face surcharges that further reduce your net payout. You must accurately forecast long-term medical expenses and factor these automatic deductions into your baseline fixed budget. Reviewing the official Medicare portal helps you avoid unwelcome surprises, allowing you to create a realistic spending plan reflecting your actual take-home pay.

Mistake 6: Treating Social Security as Your Sole Source of Income

Relying entirely on government benefits to fund your post-career lifestyle constitutes a recipe for financial stress. The system was designed to replace roughly forty percent of an average worker’s pre-retirement income, yet a startling number of seniors stretch these funds to cover one hundred percent of their daily expenses. You must purposefully build a diversified retirement income portfolio incorporating personal savings, workplace pensions, dividend-paying stocks, and potentially lucrative rental income. This multi-pillar approach provides a crucial financial buffer against unexpected home repairs, medical emergencies, and prolonged inflation. Take time to assess your fixed budget and determine exactly how much supplemental income you require. Viewing your monthly check as just one component of a broader ecosystem empowers you to navigate economic uncertainties confidently.

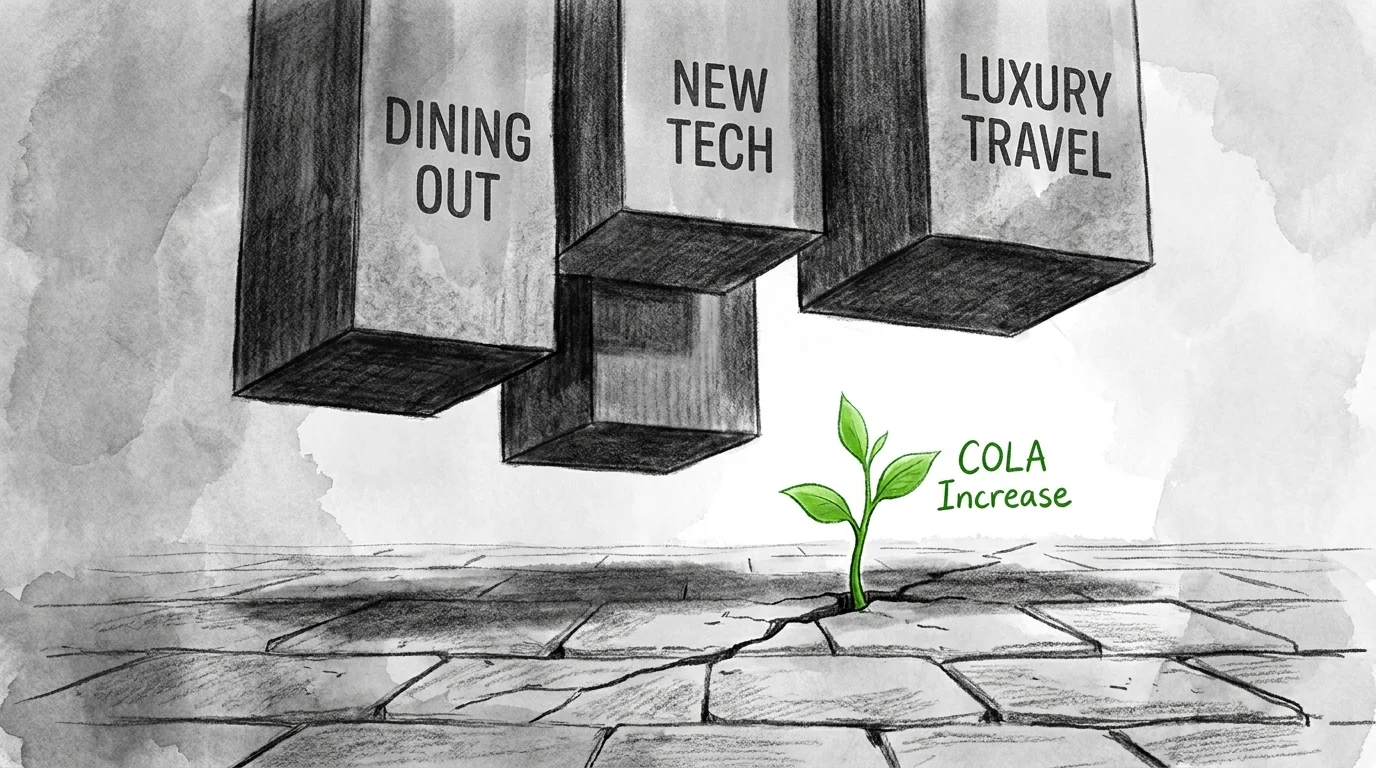

Mistake 7: Letting Lifestyle Inflation Consume Your Adjustments

When the government announces a generous annual cost-of-living adjustment, the psychological temptation is to upgrade your lifestyle or increase your discretionary spending. However, these vital adjustments exist specifically to help you keep pace with the rapidly rising costs of essential goods, such as healthy groceries, home utilities, and vital prescription medications. If you routinely channel benefit bumps into luxury purchases, you rapidly find yourself struggling to afford basic daily necessities. You must adopt a disciplined approach to your household spending and strictly allocate your increased benefits toward core, non-negotiable expenses. Tracking your monthly outlays allows you to cleanly identify exactly where your money goes and prevents silent lifestyle creep from eroding your financial stability. Purposeful lifestyle design guarantees you remain deeply secure.

Mistake 8: Falling for Phishing Scams and Benefit Fraud

As the digital landscape evolves, malicious actors target vulnerable retirees with highly sophisticated financial scams designed to intercept benefit checks. Criminals frequently pose as authoritative government officials, aggressively demanding immediate payment via retail gift cards or wire transfers to resolve fabricated issues with your personal account. You must maintain strict vigilance and recognize that legitimate federal agencies never call out of the blue to threaten benefits or demand untraceable payments. Always independently verify alarming correspondence by contacting the agency directly using officially verified phone numbers. Educating yourself on the latest fraud tactics serves as your first line of defense. The AARP fraud resources provide exceptional, up-to-date tracking of current senior financial planning scams and offer actionable advice to secure your sensitive information.

Expert Voices on Crafting a Resilient Retirement

Certified Financial Planner professionals and distinguished gerontologists uniformly agree that successful retirement planning extends far beyond basic spreadsheet calculations. Financial experts emphasize that benefit claiming errors often stem from an emotional desire to access money immediately, rather than a rational assessment of lifetime operational needs. Aging researchers consistently highlight that retirees who maintain a strong sense of daily purpose and remain physically active report significantly higher overall life satisfaction, regardless of their net worth. You must actively merge these two distinct perspectives by ensuring your foundational financial strategies directly support your personalized life goals. Engaging proactively with local community resources and seeking counsel from reputable financial advisors helps you build a comprehensive retirement plan honoring both your wealth and well-being.

Frequently Asked Questions

Can I change my mind after I claim my Social Security benefits?

Yes, you have exactly twelve months from the date of your initial claim to fully withdraw your application. If you choose this specific route, you must immediately repay every single dollar received based on your personal earnings record. This one-time do-over provides a highly valuable escape hatch if you realize you made a mathematically premature decision, but you must act quickly and prepare for the massive repayment requirement.

How do cost-of-living adjustments impact my overall retirement income planning?

Cost-of-living adjustments permanently increase your base benefit amount to combat the corrosive effects of widespread inflation. However, you should never blindly assume these administrative bumps will fully cover your individualized inflation rate, especially since seniors spend a highly disproportionate amount of their fixed income on rapidly inflating healthcare services. You must maintain a robust emergency fund and continue generating personal savings to offset specific price increases that directly impact your unique household budget.

What happens to my benefits if I decide to move abroad during retirement?

You can securely receive your monthly checks in most foreign countries, making international retirement a highly viable lifestyle choice. However, Medicare absolutely does not cover healthcare services received outside the United States, meaning you must secure comprehensive, private international health insurance. Always consult official government guidelines regarding your destination country to ensure your vital benefit deposits remain completely uninterrupted and accessible.

Do I automatically receive Medicare when I file for Social Security?

If you are actively receiving Social Security benefits when you turn sixty-five, you automatically enroll in Medicare Parts A and B without additional paperwork. However, if you strategically chose to delay your claim past your sixty-fifth birthday, you must proactively apply for Medicare during your initial enrollment period to permanently avoid devastating late penalties. You must strictly manage these distinct timelines to ensure continuous health coverage and protect your financial baseline.

Your Next Steps for a Secure Future

Taking total control of your retirement income begins with clear, highly decisive action that eliminates lingering uncertainty. Within the next forty-eight hours, commit to logging into your official online government account to review your most recent earnings statement and verify your projected benefit amounts. This simple, five-minute task clarifies your precise financial reality and provides the concrete data you need to accurately model your future income streams. Discuss these critical numbers openly with your spouse or a trusted financial professional to ensure your chosen claiming timeline aligns perfectly with your long-term lifestyle goals. By fiercely avoiding these common missteps and forcefully implementing a proactive strategy, you guarantee that your upcoming retirement years remain vibrantly healthy, financially secure, and profoundly fulfilling.

2 Responses

KibXBqXQGblJBDRAyo

No the biggest mistake the poor benefited would make is to think that it will be there for them until they die. Like it was promised a long time ago. And that was done for a reason. Not everyone reaches the top of the ladder. But a great majority hold the ladder. And guess what they are needed.