Moving closer to family gives you the emotional support and deep connections needed for a fulfilling retirement, but acting without a strategy can drain your life savings. By carefully evaluating healthcare networks, state taxes, and housing markets before packing your bags, you secure both your financial independence and your family relationships. Nearly twenty-five percent of retirees relocate to be near adult children, yet many overlook the hidden costs of crossing state lines. You need to assess local living expenses, investigate neighborhood accessibility, and initiate transparent conversations with your relatives about boundaries. Building a solid relocation plan guarantees your new chapter brings joy rather than unexpected financial stress or strained family dynamics.

Current Retirement Relocation Landscape

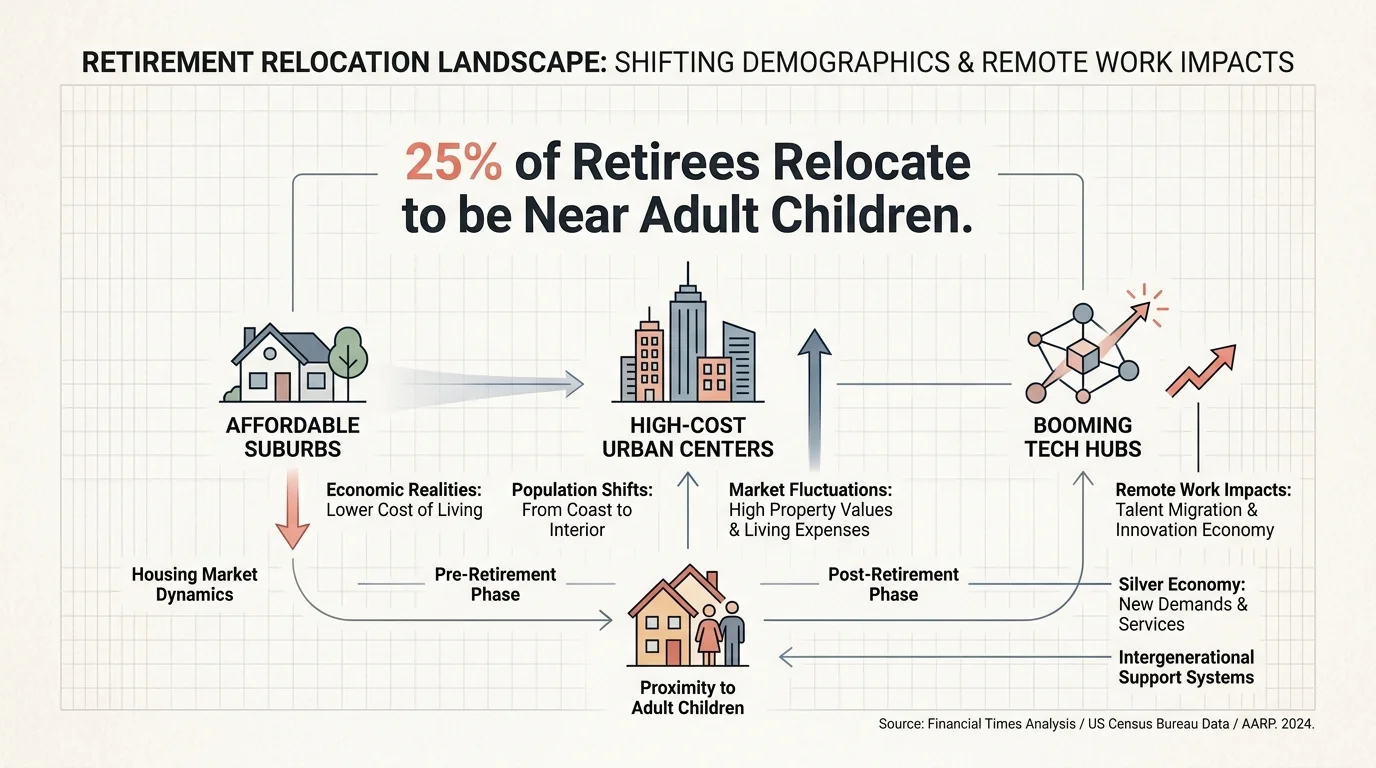

The current economic environment presents unique challenges for those considering a cross-country move. Inflationary pressures have permanently altered housing markets and daily living expenses, while the rapid rise of remote work has scattered families across the nation. You might find that your children no longer live in the affordable, quiet suburbs where they grew up; instead, they reside in high-cost urban centers, booming tech hubs, or rapidly gentrifying neighborhoods. Understanding the economic realities of their current zip code serves as a fundamental step in your relocation process. State legislatures continuously adjust property tax exemptions and pension tax laws to generate revenue, meaning the financial blueprint you created five years ago requires immediate and thorough revision. Taking aggressive control of your relocation strategy ensures you navigate these market fluctuations with absolute confidence and maintain your purchasing power.

1. Analyze Your Income and State Tax Liabilities

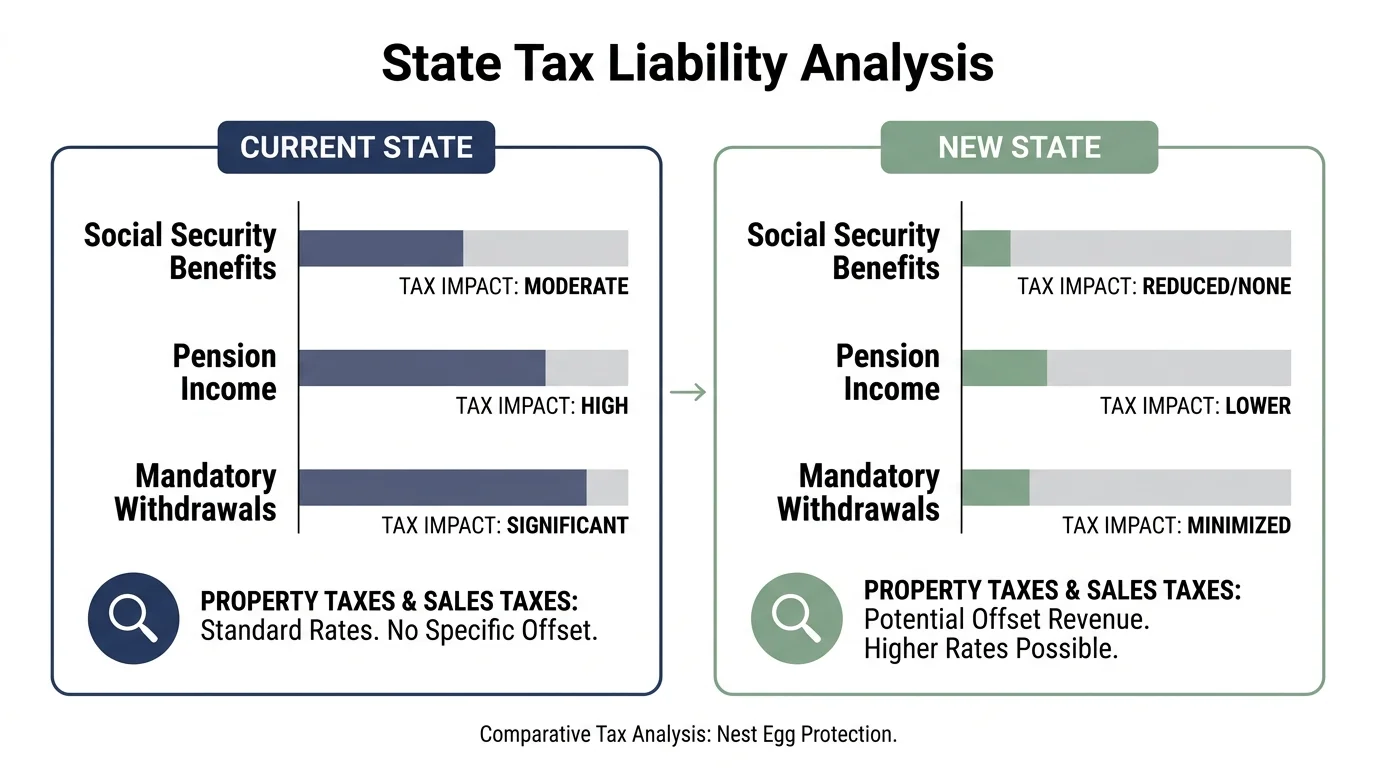

Moving across state lines alters your financial reality overnight. A state that lacks a personal income tax frequently offsets that missing revenue through exorbitant property taxes, vehicle registration fees, or high sales taxes on everyday goods. You must calculate exactly how your new state taxes pension income, Social Security benefits, and mandatory withdrawals from traditional retirement accounts. Reviewing the Internal Revenue Service resources for retirees gives you a baseline understanding of how domicile changes affect your federal and state tax filings. Furthermore, estate and inheritance taxes vary wildly from one jurisdiction to another, directly impacting the financial legacy you intend to leave behind for your children. Relocating without running a comparative tax analysis puts your carefully built nest egg at unnecessary risk. Sit down with a fiduciary financial advisor to model your post-move cash flow and verify that your portfolio can comfortably sustain regional economic differences.

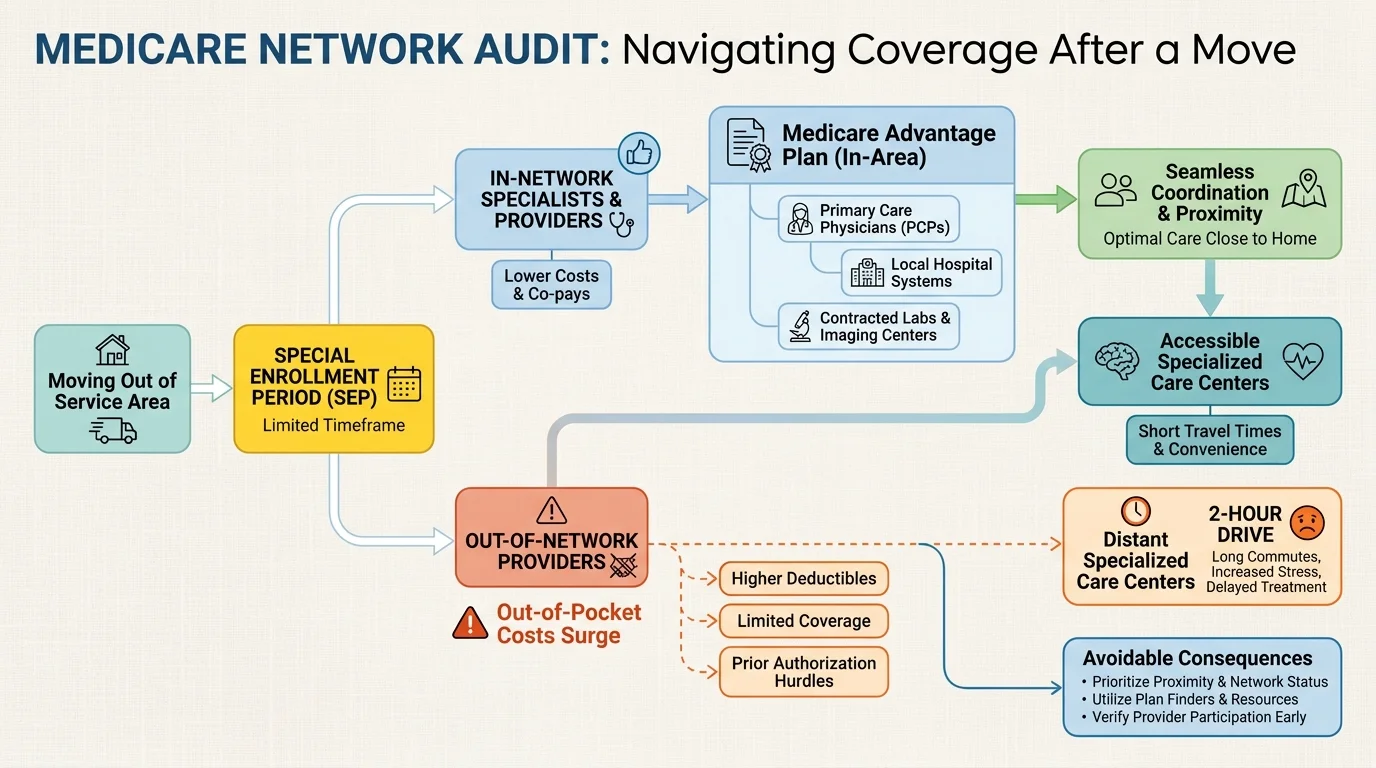

2. Audit Your Medicare and Healthcare Networks

Healthcare accessibility dictates the overall quality of your retirement years, especially as medical needs inevitably increase with age. If you rely on a Medicare Advantage plan, moving out of your plan’s established service area automatically triggers a Special Enrollment Period. You cannot simply assume your current robust coverage will transfer seamlessly to a new county or state. You need to consult the official Medicare network directories to verify that top-tier specialists, primary care physicians, and local hospital systems accept your specific insurance tier. Out-of-pocket costs surge dramatically when retirees unknowingly visit out-of-network providers in their new hometowns. Beyond basic insurance coverage, investigate the physical proximity of specialized care centers. Moving to a remote rural town to be near your daughter sounds idyllic, but a two-hour drive to the nearest cardiologist creates a severe logistical burden on both of you. Do not forget to research prescription drug coverage; formulary tiers vary by region, and your essential daily medications might cost significantly more under a new zip code’s pricing structure.

3. Establish Clear Boundaries and Expectations

Physical proximity to your children and grandchildren often leads to dangerous assumptions about your daily availability. You might envision weekly Sunday dinners and occasional holidays, while your adult children desperately need daily after-school childcare to maintain their demanding careers. You must initiate an open, honest conversation about boundaries before hiring a moving company. Define your role clearly and without apology. Explain your personal schedule, your desire to travel, and your actual physical availability for babysitting or providing ongoing financial support. Diverse cultural backgrounds influence family expectations differently; some cultures expect multi-generational living under one roof, while others prioritize independent households. Acknowledge your specific family heritage while fiercely advocating for your personal rest time. Fostering healthy intergenerational relationships requires highly transparent communication; unspoken expectations breed toxic resentment on both sides of the family tree. Treat this dialogue as an essential planning phase rather than an afterthought. Setting these firm ground rules early prevents emotional strain and ensures your family dynamic remains a profound source of joy.

4. Research the Local Housing Market

Swapping your paid-off family home for a property near your children requires rigorous real estate research and highly realistic expectations. You face a major lifestyle choice between downsizing to a condo, renting an apartment, or purchasing a spot in a continued care retirement community. Analyze the current housing inventory, property tax assessment history, and average days on the market in your target neighborhood to accurately gauge affordability. Evaluate the long-term carrying costs of any new property, paying special attention to homeowners association fees, insurance premiums, and municipal assessments. Renting for the first twelve months offers a highly strategic buffer; it allows you to test the neighborhood vibe and assess your actual proximity to family without committing a massive portion of your liquidity. Interest rates currently fluctuate unpredictably, meaning securing a favorable mortgage demands pristine credit and significant cash reserves. Reviewing housing trends prevents you from overpaying in an unfamiliar, potentially inflated market.

5. Plan for Accessibility and Mobility Shifts

Your physical housing needs will evolve dramatically as you progress through your retirement years. The charming multi-level townhouse near your son might appeal to you today, but steep staircases and narrow hallways transform into insurmountable obstacles if your mobility naturally declines. You need to prioritize single-story living, walk-in showers, and minimal exterior maintenance from day one. Community infrastructure plays an equally vital role in preserving your long-term independence. Investigate the neighborhood’s walkability, access to public transportation, and distance to essential services like grocery stores and pharmacies. Examining AARP livability criteria helps you identify communities intentionally designed to support aging populations. Choosing a home equipped with universal design features—such as wider doorways and smart home technology—reduces the likelihood of requiring a second, forced move later in life due to physical limitations. Building a resilient living environment ensures you remain fiercely self-sufficient.

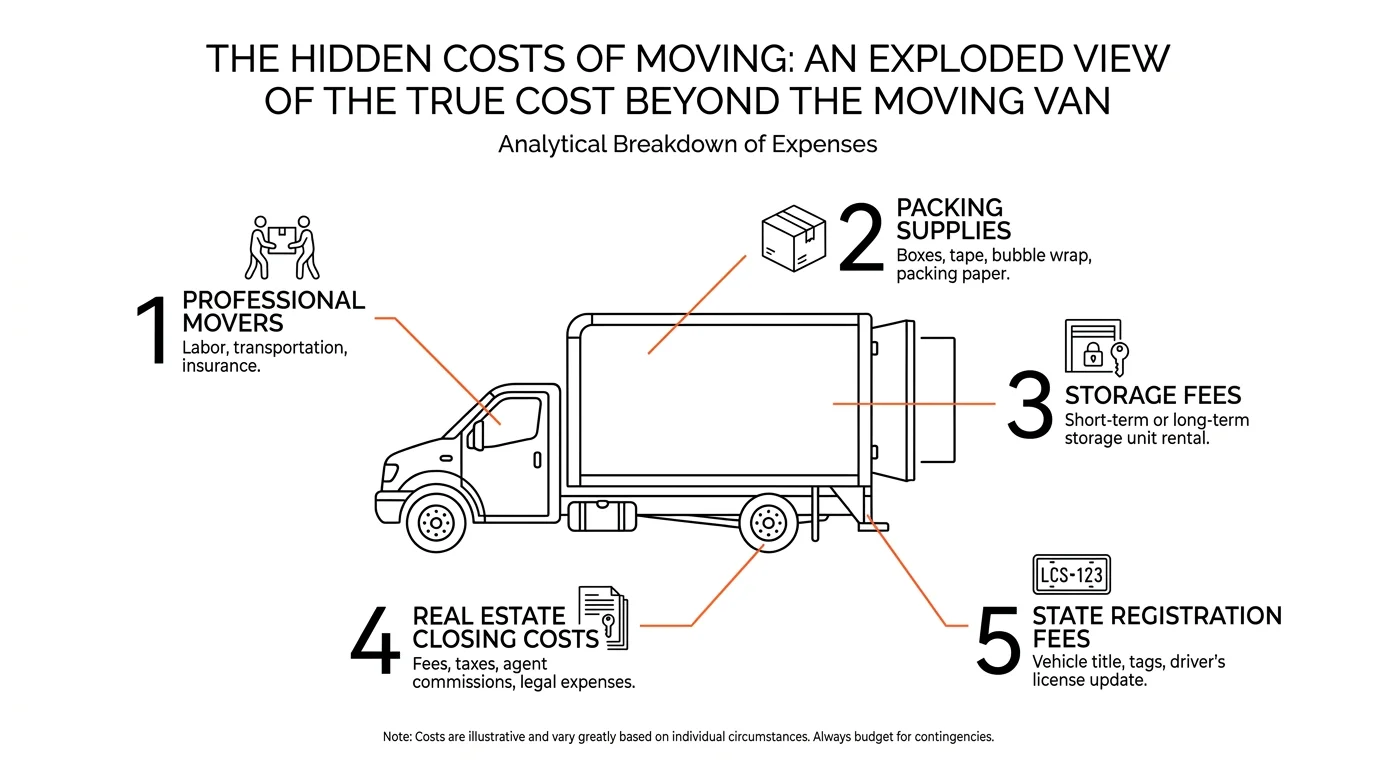

6. Calculate the True Cost of Relocation

The logistical expenses of moving an entire household across the country routinely exceed even the most conservative initial estimates. Packing materials, professional moving services, and specialty transport for vehicles or fragile family heirlooms accumulate with shocking speed. You must also budget heavily for utility deposits, new furniture scaled to fit a different floor plan, and immediate home modifications. For retirees living on strictly fixed budgets, even minor fluctuations in utility costs can disrupt months of careful planning. Cross-referencing your monthly budget against Bureau of Labor Statistics consumer price reports provides vital insight into regional inflation variations. Groceries, electricity, and gasoline cost significantly more in coastal cities compared to the Midwest or South. Failing to account for these hidden relocation expenses triggers a severe cash flow crisis during your critical first year in the new city. Request binding estimates from multiple carriers and build a fifteen percent contingency fund to protect your reserves.

7. Build a New Social Network Outside of Family

Relying exclusively on your adult children for social interaction places an unfair burden on them and isolates you from a broader, supportive community. Your children possess demanding careers, robust social lives, and immediate family obligations that consume the vast majority of their time. You need to actively cultivate your own friendships and engaging activities to achieve a fulfilling, well-rounded retirement experience. Before you finalize your move, research local community centers, volunteer organizations, and specific hobby groups located in your destination city. Attend community board meetings, join local fitness classes tailored to seniors, or enroll in continuing education classes at a nearby community college. Integrating yourself into the local fabric provides a renewed sense of purpose and helps you build a diverse support system entirely independent of your relatives. A vibrant, independent social life enriches your mental health and makes the difficult transition to a new environment significantly smoother.

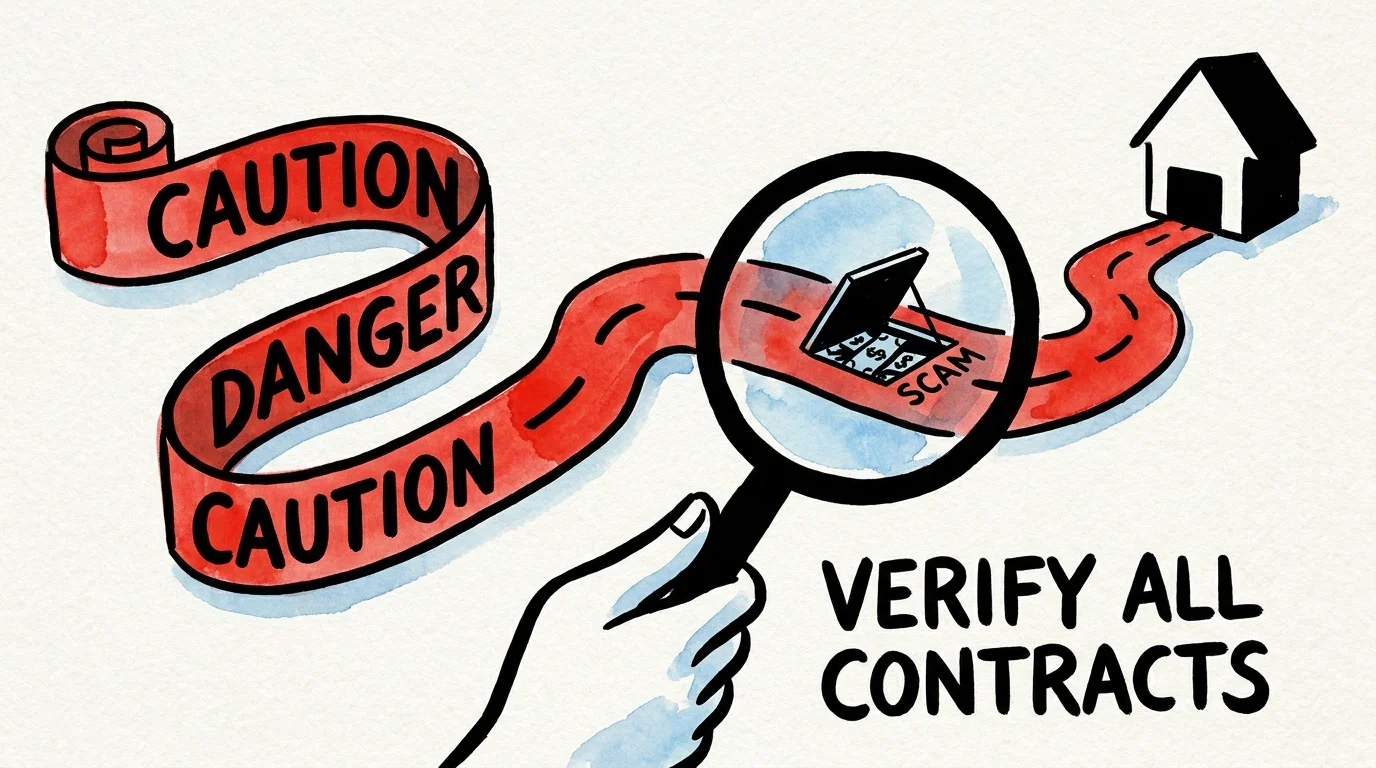

8. Guard Against Relocation Scams and Financial Pitfalls

Predatory moving companies and identity thieves frequently target older adults during the inherently chaotic relocation process. Scam operators regularly offer artificially low initial estimates, only to hold your household possessions hostage for double the price upon arrival at your new home. Protect yourself by reading verified customer reviews and checking all moving company credentials through federal databases before signing any contracts. Keep your vital financial documents, medical records, and valuable jewelry secured in your personal vehicle during the journey. Furthermore, monitor your credit reports continuously during the transition, as forwarded mail occasionally falls into the wrong hands. Adjusting your fixed income streams requires equal vigilance; utilize the Social Security Administration retirement portal to update your direct deposit information and mailing address to prevent delayed payments. Implementing strict cybersecurity safeguards shields your assets and ensures your relocation proceeds smoothly.

Expert Perspectives on Uprooting Your Life

Certified financial planners emphasize that cross-country relocation acts as the ultimate financial stress test for your retirement portfolio. Liquidating real estate and transferring assets forces you to realize capital gains, confront market volatility, and recalibrate your withdrawal strategies simultaneously. Wealth managers strictly advise against making hasty geographical changes simply because a new grandchild is born; they recommend waiting at least six to twelve months to ensure the child’s parents intend to remain permanently in their current city. Gerontologists highlight the profound psychological impact of leaving a long-term community behind. Decades of built-in social equity disappear the moment you cross state lines, requiring immense emotional resilience and extroversion to rebuild. Experts universally agree that maintaining a robust emergency fund and preserving a deep sense of personal autonomy determine the ultimate success of a late-in-life move.

Frequently Asked Questions

How long should I wait to buy a home after moving to a new city?

Financial experts highly recommend renting for at least twelve months before purchasing a property in a new state. Renting gives you the necessary time to explore different neighborhoods, evaluate local traffic patterns, and confirm that living near your family matches your initial expectations. This vital waiting period protects your liquid assets from a rushed, emotionally driven real estate decision.

Does moving to a different state affect my Social Security payments?

Your base Social Security benefits remain the exact same regardless of which state you choose to live in. However, the specific way your benefits are taxed changes significantly based on your new location. Several states tax Social Security income, while others offer complete exemptions for retirees. You must consult a qualified tax professional to understand your new state liability.

What happens to my estate plan when I relocate?

Relocating frequently invalidates certain aspects of your estate plan because probate laws and advance directive requirements vary heavily by state. The power of attorney documents or healthcare proxies drafted in your previous state might face immediate rejection at your new local hospital. You need to hire an estate attorney in your new state to review and update your entire legal framework.

How do I manage the emotional toll of leaving my long-time friends?

Leaving a community you helped build causes legitimate grief and requires active emotional management. Acknowledge the loss rather than ignoring it entirely. Schedule regular video calls with your old friends and plan a visit back to your hometown within the first six months. Simultaneously, force yourself to attend local social events in your new city to begin building fresh connections.

Take Action Today

Your successful relocation starts with gathering hard data rather than relying on idealized daydreams. Within the next forty-eight hours, schedule a dedicated family meeting—either in person or via video call—to initiate a transparent conversation about boundaries, expectations, and real estate realities. Ask your children specific, direct questions about their long-term career stability and neighborhood dynamics. Taking this single, decisive step shifts your relocation from a vague wish into a concrete, executable plan that protects your financial security and thoroughly strengthens your family bonds.