You have more freedom and choices today than any generation before you, meaning you can design a second act that aligns perfectly with your values and goals. The concept of a rigid stop-date followed by decades of leisure has completely vanished, replaced by dynamic phases of part-time work, entrepreneurial ventures, and vibrant community living. Twenty years ago, the landscape looked entirely different, with limited technological tools and rigid financial withdrawal strategies dictating how older adults spent their time. Now, groundbreaking shifts in policy, health care, and lifestyle flexibility are revolutionizing your options. By understanding these eight modern developments, you can strategically navigate your wealth and well-being to maximize the quality of your upcoming years.

A Snapshot of the Modern Policy and Market Landscape

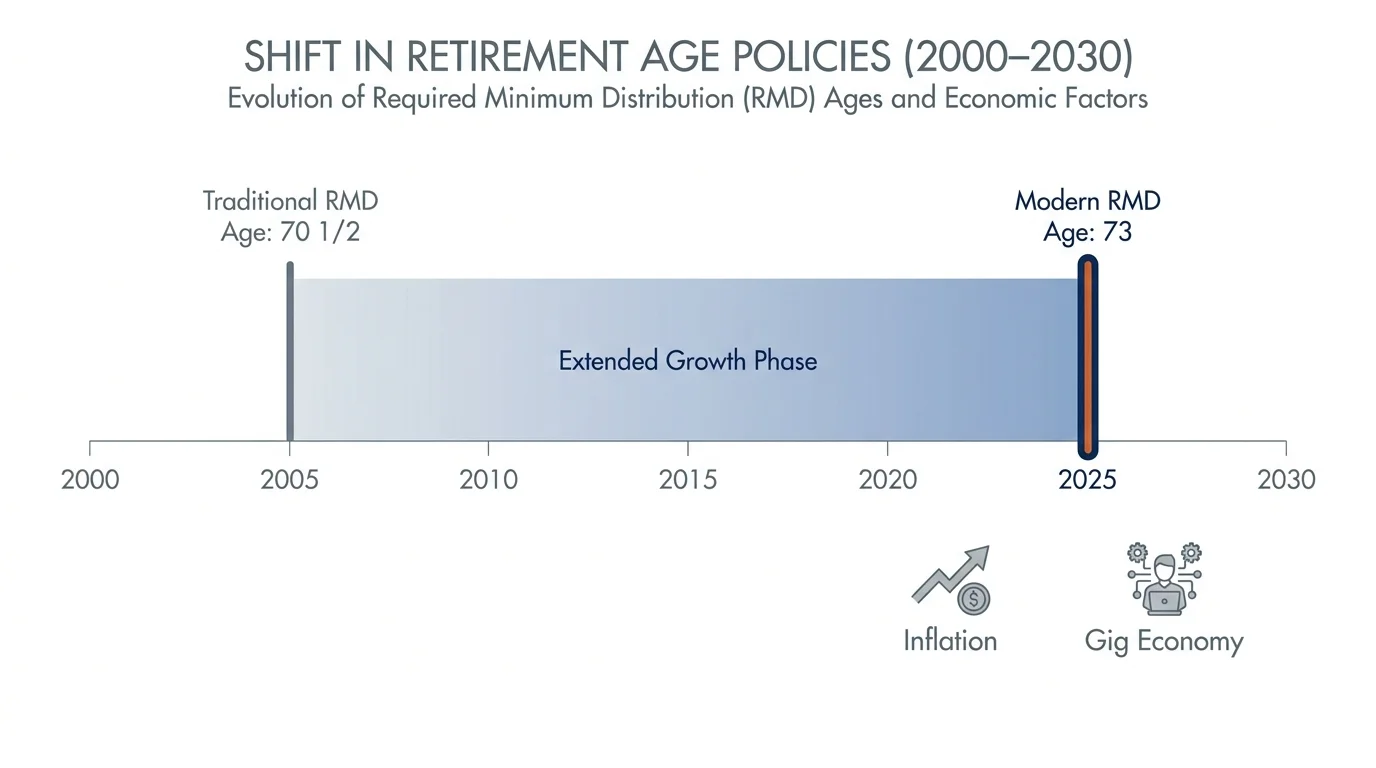

The financial framework supporting older adults has shifted dramatically since the early 2000s; today, modern longevity requires more adaptable financial and lifestyle blueprints. Legislative updates and sweeping economic shifts continuously rewrite the rules of wealth management. Recent legislation transformed the regulations governing your tax-advantaged accounts, pushing out mandatory distribution dates and allowing your money to grow tax-deferred for longer periods. For example, the Internal Revenue Service now dictates that Required Minimum Distributions begin at age 73, a significant leap from the traditional age of 70 and a half used two decades ago.

Beyond federal tax codes, you now face a completely different macroeconomic environment. Inflation spikes challenge fixed incomes, while advancements in gig economy platforms offer immediate solutions for bridging wealth gaps. You must view your upcoming years not as a static finish line, but as a dynamic, evolving journey that requires proactive management and constant curiosity.

Trend 1: The Phased Transition and the Gig Economy

The traditional retirement party on a Friday followed by full-stop leisure on Monday is rapidly disappearing. Instead, you have the option to pursue a phased transition into your later years. Many professionals now scale back their hours gradually, moving from full-time employment to part-time consulting or freelance work within their respective industries. This deliberate tapering provides a critical mental transition, keeping your mind sharp and your social connections strong while reducing stress.

Simultaneously, the modern gig economy offers unprecedented flexibility. According to the Bureau of Labor Statistics, the labor force participation rate for workers aged 65 and older has grown significantly over the past two decades. You can drive for a rideshare service, tutor students online, or rent out a spare bedroom on a short-term basis. Earning supplemental income on your own schedule helps mitigate the anxiety of living entirely on a fixed budget while providing the financial cushion needed to delay drawing down your core investment portfolio.

Trend 2: Solo Aging and Intentional Co-Housing

Twenty years ago, aging without a spouse or adult children living nearby fell outside the mainstream dialogue. Today, solo aging represents a major demographic shift, prompting innovative solutions for housing and community support. You no longer have to choose between maintaining a large, isolating family home or moving into a clinical assisted-living facility. Intentional co-housing communities now bridge the gap, offering a vibrant middle ground.

In a co-housing arrangement, you typically own a private, fully equipped home clustered around shared spaces like a community garden, a large dining hall, or a fitness center. You share maintenance costs, tools, and social responsibilities with your neighbors. This layout allows you to split the heavy lifting of home upkeep while ensuring someone always notices if you deviate from your daily routine. For older adults navigating life on a fixed income, co-housing drastically reduces living expenses while curing the epidemic of isolation.

Trend 3: The Gray Divorce Revolution

The concept of gray divorce—couples splitting up after the age of 50—has surged over the last two decades. As life expectancies rise, many couples realize they want entirely different lifestyles for their remaining 30 years. While liberating for many, navigating a late-in-life divorce requires a radical restructuring of your financial trajectory.

When you divide a single nest egg into two separate households, your purchasing power drops. You must rapidly redesign your estate plan, update the primary beneficiaries on your life insurance policies, and rethink your withdrawal strategies. You should also consult a Certified Financial Planner to untangle complicated assets like primary residences and traditional IRAs without triggering massive, unexpected tax penalties. Restructuring your wealth intelligently allows you to build a resilient, independent foundation for your newly solo lifestyle.

Trend 4: Smart Home Technology and Aging in Place

You no longer need to uproot your life and move into specialized care simply because you live alone and worry about medical emergencies. Modern smart home technology actively monitors your environment and keeps you safe, significantly extending the amount of time you can age in place. Whether you possess full mobility or navigate the world from a wheelchair, voice-activated smart home systems allow you to control lighting, security, and climate control without physical exertion.

Sensors now track daily movements; if you typically wake up and walk to the kitchen by 8:00 AM, a lack of movement can trigger an automated alert to a loved one. Wearable technology, such as modern smartwatches, features advanced fall detection that automatically dials emergency services if you take a hard spill and remain unresponsive. These unobtrusive tools provide immense peace of mind, transforming your existing house into a responsive, supportive sanctuary.

Trend 5: Purpose-Driven Entrepreneurship

Starting a business at age 65 used to sound incredibly risky and exhausting. Now, low-barrier digital tools make entrepreneurship a highly accessible and rewarding path for older adults. Rather than stepping back entirely, you can use your decades of accumulated industry knowledge to launch a purposeful small business from your living room.

You can leverage platforms like Etsy to monetize a lifelong hobby, or you might use digital networking tools to offer fractional coaching services to younger professionals. This trend allows you to dictate your own hours and scale your efforts according to your physical mobility and energy levels. Furthermore, generating a small business income provides a crucial financial bridge, allowing you to delay claiming your Social Security benefits and permanently increasing your guaranteed monthly payout.

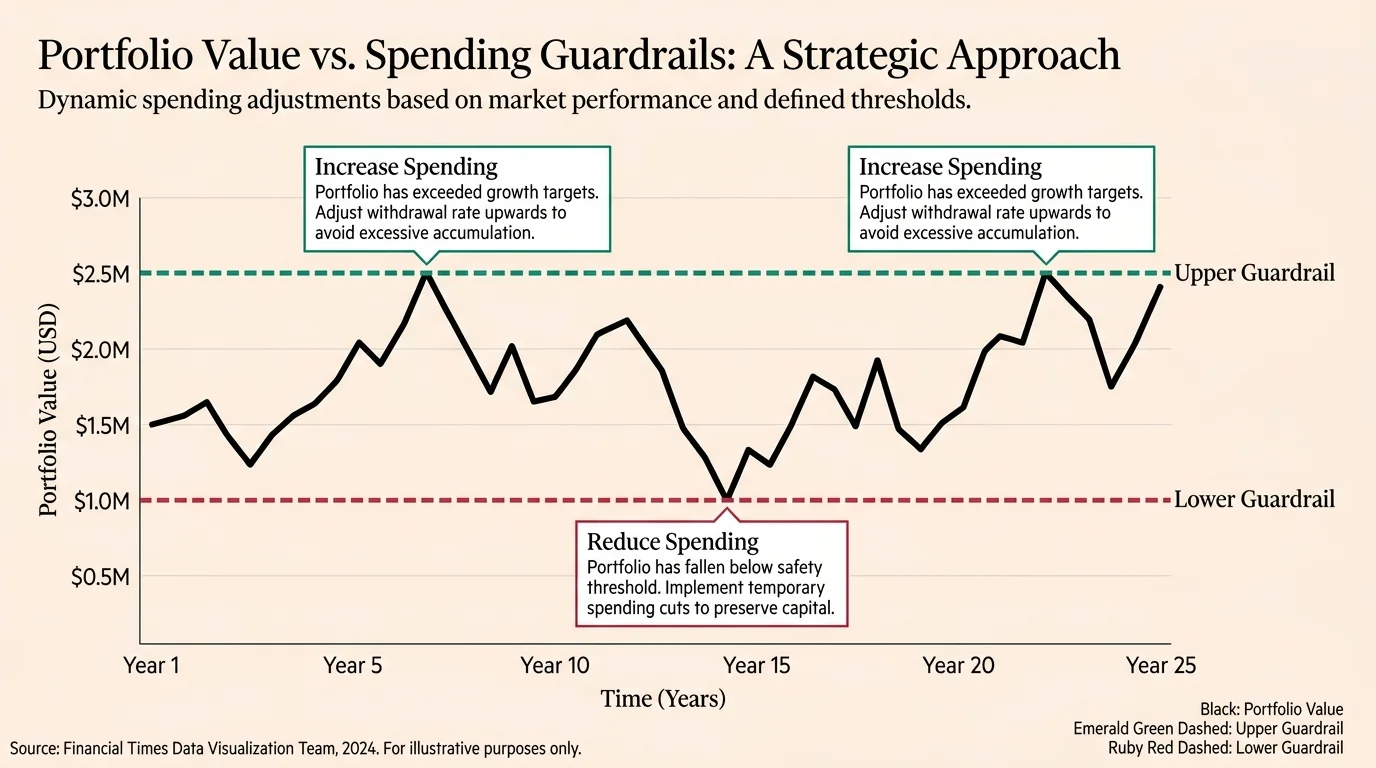

Trend 6: Dynamic Financial Withdrawal Guardrails

In the early 2000s, financial advisors largely relied on the strict four percent rule, advising clients to withdraw a set percentage of their portfolio and rigidly adjust it for inflation every single year. Today, sophisticated planning software and modern market volatility have rendered that rigid strategy obsolete. You must now implement dynamic financial withdrawal guardrails.

Dynamic strategies dictate that your spending adjusts based on the health of the stock market. If your portfolio drops significantly during a recession, you might skip your annual inflation raise or temporarily trim discretionary expenses like travel. Conversely, if the market surges, your guardrails signal that you can safely give yourself a raise. This flexible, realistic approach ensures you do not deplete your principal during economic downturns while allowing you to fully enjoy the fruits of a booming economy.

Trend 7: Geo-Arbitrage and the Digital Nomad Retiree

Moving south for better weather is a traditional concept; relocating across international borders to slash your living expenses is a distinctly modern strategy. With inflation squeezing fixed budgets, many retirees now leverage geo-arbitrage. By moving to a country or a specific domestic region with a significantly lower cost of living, you stretch the purchasing power of your U.S. dollars.

Retirees from diverse cultural backgrounds often return to their countries of origin, or adventurous solo agers purchase recreational vehicles to live as digital nomads. This lifestyle choice allows you to secure premium housing, regular travel, and a vibrant social life on a budget that would barely cover basic necessities in a high-cost American city. However, executing this strategy requires meticulous upfront planning regarding tax liabilities and international healthcare logistics.

Trend 8: Telehealth and Medicare Advantage Evolution

Traveling to a physical doctor’s office for every minor ailment used to drain significant time and energy. The explosion of digital health services represents one of the most profound upgrades to modern aging. Telehealth appointments allow you to consult specialists, review lab results, and manage prescription refills directly from your laptop or smartphone. This accessibility proves especially critical if you live in a rural area or experience mobility limitations.

Furthermore, the healthcare insurance landscape has transformed. The official Medicare portal details extensive coverage for virtual care, and private Medicare Advantage plans have evolved to offer diverse supplementary benefits. Many of these modern plans now include allowances for healthy groceries, gym memberships, and non-emergency medical transportation. You must thoroughly review these options annually to secure the maximum benefits available for your specific health profile.

Expert Voices and Strategic Pillars for Your Future

Gerontologists continually emphasize that finding purpose proves far more critical to your longevity than simply finding leisure. Modern aging researchers note that older adults who actively engage in continuous learning, part-time work, or robust volunteering exhibit significantly lower rates of cognitive decline. You must prioritize mental engagement alongside physical health.

Financial professionals echo this need for adaptability. Certified Financial Planners stress that your income strategy must remain flexible enough to weather unexpected inflation spikes and prolonged market volatility. Maximizing your guaranteed income floor remains paramount. You should delay taking your government benefits if your health and savings allow it; you can strategize your unique claiming timeline via the Social Security Administration. Combining a delayed claiming strategy with a dynamic withdrawal rate builds an unbreakable financial foundation.

Safeguards: Navigating New Risks and Pitfalls

While the modern landscape offers incredible opportunities, it also introduces unprecedented risks. Financial fraud targets older adults relentlessly, and the tactics have evolved far beyond simple email scams. Artificial intelligence now powers voice-cloning technology, allowing scammers to impersonate the exact voice of your grandchild claiming they need emergency bail money. Organizations like the AARP Fraud Watch Network provide critical updates on these sophisticated phishing schemes. You must establish a family safe word to verify identities over the phone.

You also face modern legislative pitfalls, such as the Income-Related Monthly Adjustment Amount, commonly known as IRMAA. If you sell a highly appreciated home or execute a massive Roth IRA conversion, that extra taxable income could push you over an arbitrary threshold. Crossing this cliff triggers a significant surcharge on your Medicare Part B and Part D premiums. You must coordinate closely with a tax professional before making large financial moves to avoid unexpectedly slashing your monthly cash flow.

Frequently Asked Questions About Modern Retirement

How does working part-time affect my Social Security benefits?

If you claim Social Security before reaching your full retirement age, earning income from a part-time job or freelance gig can temporarily reduce your monthly benefit. The government sets an annual earnings limit; if you earn above that threshold, a portion of your benefits will be withheld. However, once you reach your full retirement age, you can earn an unlimited amount of money without facing any reductions. Furthermore, any withheld benefits are ultimately recalculated and credited back to you over your remaining lifetime.

What is the most significant hidden cost in modern retirement?

Health care expenses consistently rank as the most underestimated cost for older adults. While standard insurance covers a substantial portion of your medical bills, it does not always cover long-term custodial care, routine dental work, or comprehensive vision care. Additionally, unexpected inflation can drastically increase the cost of prescription medications. You must build a dedicated health care buffer into your financial plan, potentially utilizing Health Savings Accounts if you are still working, to absorb these out-of-pocket expenses without derailing your lifestyle.

How do I protect my savings from artificial intelligence scams?

You must adopt a zero-trust policy for unsolicited communications. Scammers now use artificial intelligence to craft highly convincing emails, text messages, and even voice calls that mimic government officials or your loved ones. Never provide personal information or authorize wire transfers based on an inbound call. If you receive a concerning message, hang up the phone, look up the official contact number for the institution independently, and initiate the call yourself. Establishing a secret family password also provides an immediate defense against voice-cloning emergencies.

Does traditional Medicare cover my health care if I move abroad?

Traditional Medicare generally does not provide coverage for medical care received outside of the United States. If you plan to leverage geo-arbitrage by moving overseas or if you intend to travel internationally for extended periods, you must purchase a robust travel medical insurance policy or a comprehensive international health insurance plan. Some specialized supplemental policies offer limited coverage for foreign travel emergencies, but you should never rely on them for routine medical care while living as an expatriate.

Your Next 48 Hours

Audit your immediate financial horizon today and identify one specific area where you can inject more modern flexibility into your plan. Log into your primary investment accounts, verify that your beneficiary designations accurately reflect your current family structure, and pull your latest government benefits estimate. Schedule a brief, structured conversation with your partner or a trusted financial advisor to discuss whether a phased work transition or a dynamic withdrawal strategy makes sense for your upcoming timeline. Taking one decisive action right now ensures you remain in complete control of your second act.