Retiring to a home where you can sip morning coffee while gazing over a tranquil lake is a dream you can realistically achieve. Trading urban sprawl for serene waterfront living reduces stress and encourages a physically active lifestyle, keeping you healthier as you age. Searching for the ideal waterfront haven requires balancing affordable property taxes, proximity to quality Medicare facilities, and recreational opportunities that align with a fixed budget. By analyzing housing data, state tax policies, and healthcare access, we identified eight premier destinations offering stunning daily lake views without compromising your financial security. You will discover practical strategies for funding your relocation, navigating regional insurance complexities, and selecting a vibrant, supportive community for your next chapter.

Current Trends in Scenic Retirement and Housing Markets

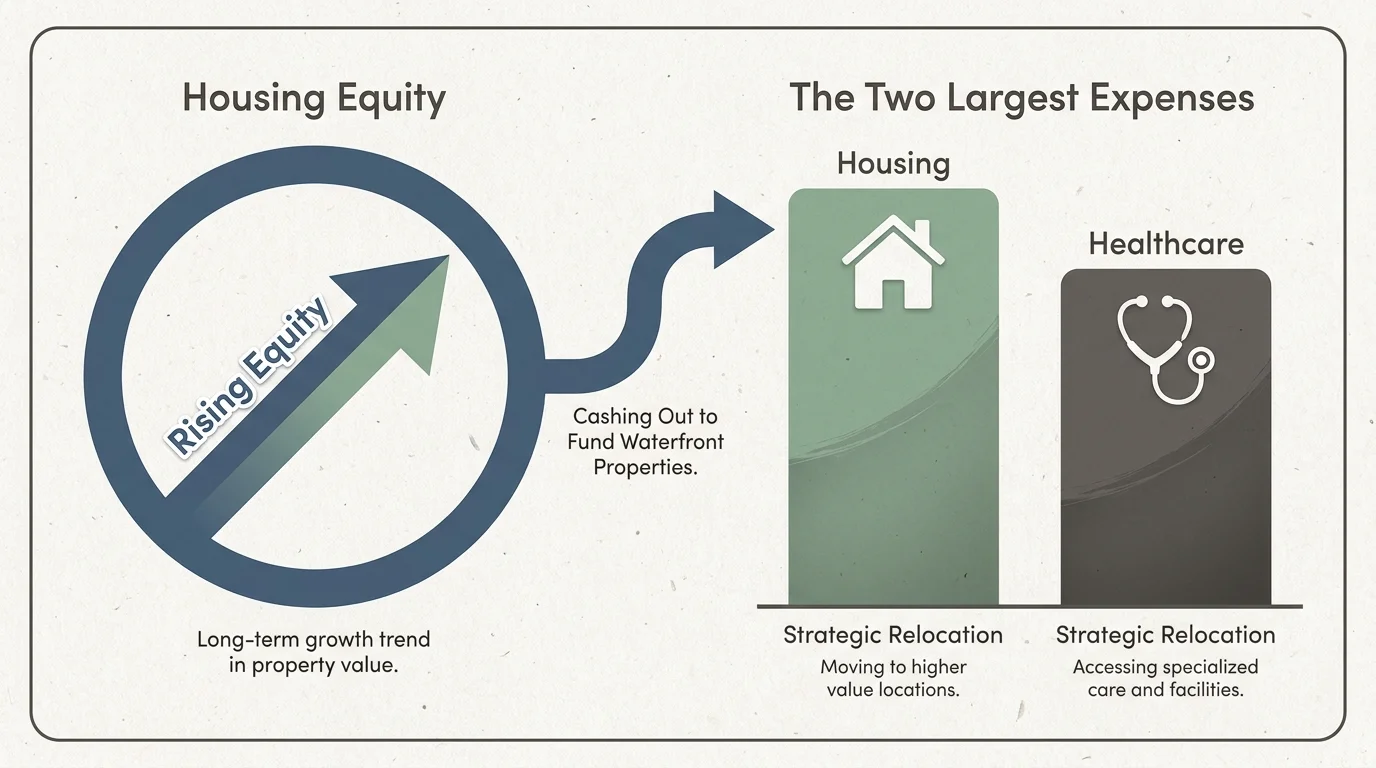

The landscape of retirement relocation is shifting rapidly as older adults seek tangible quality-of-life improvements over traditional resort living. With housing equity near all-time highs for Americans over 65, many pre-retirees are cashing out of primary residences in high-cost metropolitan areas to fund waterfront properties. You can leverage this accumulated home equity to secure a lakefront home while still preserving enough capital to generate reliable income for your golden years.

Economic indicators suggest that retirees prioritize locations offering a blend of natural beauty and financial prudence. According to official consumer spending data, housing and healthcare remain the two largest expenses for older adults. Consequently, the most desirable scenic destinations feature reasonable property tax rates and robust local economies. Remote work trends have also introduced younger professionals into these traditionally retiree-heavy markets, driving up property values but simultaneously encouraging towns to invest heavily in modern infrastructure, high-speed internet, and upgraded medical clinics.

Strategic Pillars for Lakefront Living

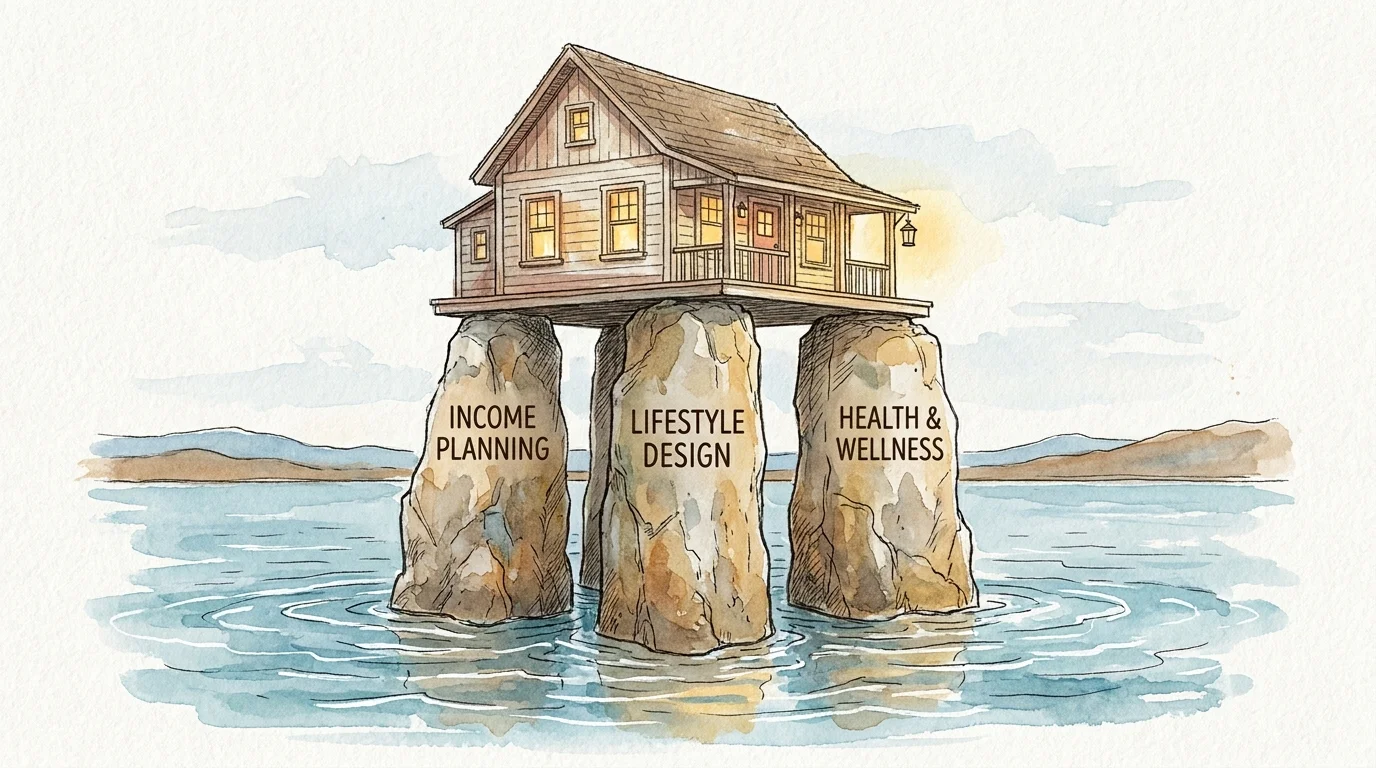

Securing your waterfront dream requires far more than finding a beautiful house on a great piece of land. You must build a comprehensive strategy that protects your wealth, enhances your daily life, and safeguards your physical well-being. Focusing on three core pillars ensures your move brings lasting satisfaction rather than unexpected stress.

Income Planning and Real Estate Realities

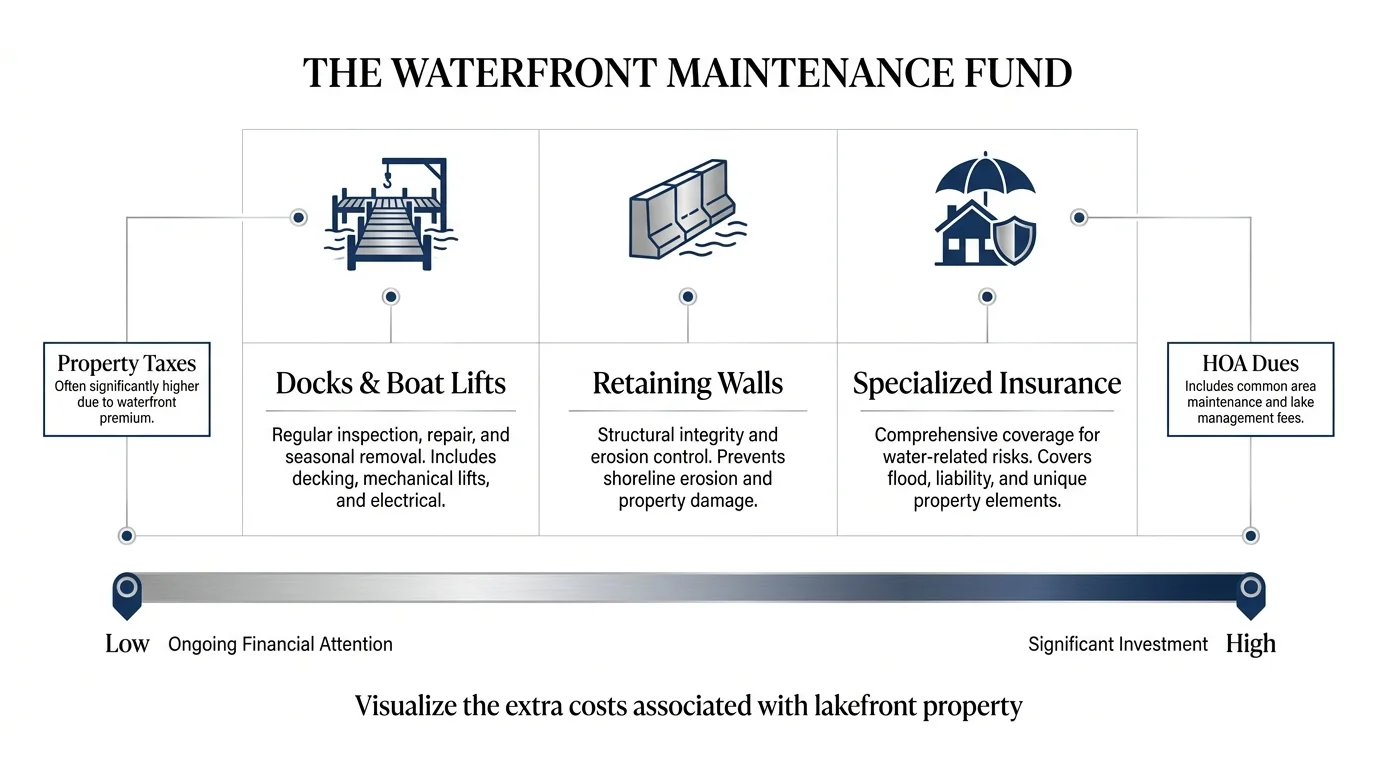

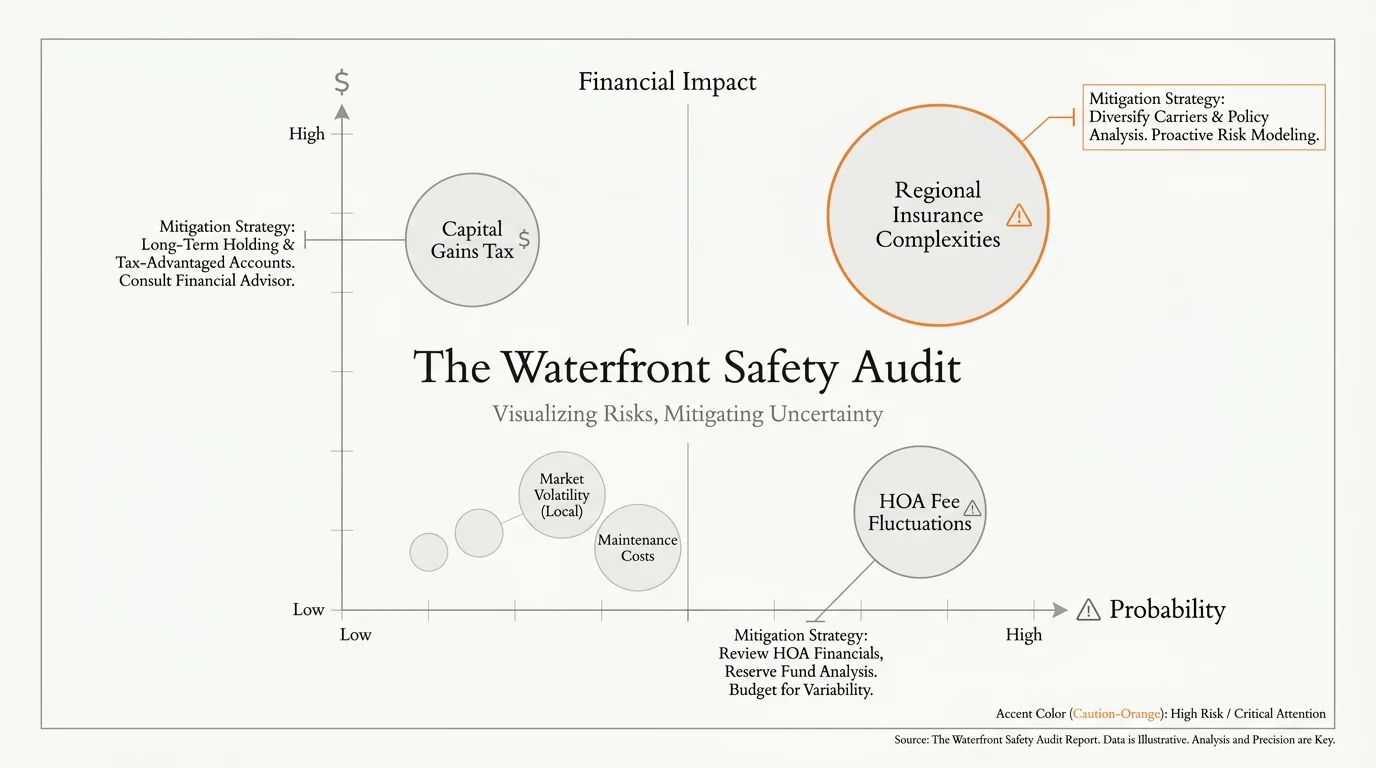

Waterfront real estate generally commands a premium, which means you need a robust income plan to sustain your lifestyle. Beyond the purchase price, you must account for fluctuating property taxes, homeowner association dues, and specialized insurance premiums. Before making an offer on a lake home, review federal tax guidance for older Americans to understand how capital gains from selling your current home might impact your overall tax bracket. Establish a dedicated maintenance fund for your new property, as docks, retaining walls, and boat lifts require ongoing financial attention that inland homes do not.

Lifestyle Design and Finding Your Purpose

While the view from your back porch provides immense joy, long-term retirement satisfaction relies on community engagement. You need to proactively design a lifestyle that prevents social isolation. Investigate the culture of the lake communities you consider. Look for active volunteer networks, local clubs, and civic organizations where you can share your skills. A successful scenic retirement integrates the tranquility of the water with a vibrant, socially connected daily routine.

Health, Wellness, and Proximity to Care

Living near water naturally promotes a healthier lifestyle. A growing body of research on blue space and aging demonstrates that proximity to aquatic environments lowers blood pressure, reduces anxiety, and encourages regular physical activity like swimming, kayaking, and walking. However, natural beauty must not distance you from essential medical services. You must verify that your chosen destination provides rapid emergency response times and features top-tier hospitals. Utilize federal databases to compare local care facilities to ensure you will receive high-quality treatment as your health needs evolve.

8 Lakefront Retirement Destinations to Consider

Finding the perfect balance of affordability, scenery, and supportive infrastructure requires looking beyond the most famous coastal cities. These eight lakefront destinations across the United States offer exceptional amenities tailored to older adults seeking a scenic, financially sustainable retirement.

Lake Keowee, South Carolina

Nestled in the foothills of the Blue Ridge Mountains, Lake Keowee boasts emerald-green waters and a remarkably mild climate that allows for nearly year-round outdoor recreation. South Carolina offers a highly favorable tax environment for retirees; the state completely exempts Social Security benefits from taxation and provides a generous deduction on other retirement income for residents over 65. The lake region provides a peaceful, secluded atmosphere, yet you remain just a short drive from Greenville. This proximity grants you access to Prisma Health’s extensive medical network and a thriving downtown cultural scene, perfectly balancing tranquil living with modern convenience.

Lake Martin, Alabama

Covering over 44,000 acres, Lake Martin is a premier destination for those seeking warm weather and southern hospitality without a massive price tag. Alabama features some of the lowest property tax rates in the nation, allowing your fixed income to stretch significantly further here than in many other waterfront locales. The surrounding communities prioritize a relaxed, community-focused lifestyle with numerous marinas, golf courses, and walking trails. Furthermore, you will find excellent lifelong learning opportunities and regional medical care nearby in Auburn, making Lake Martin an intellectually stimulating and physically safe environment for your later years.

Coeur d’Alene, Idaho

If you prefer towering pine trees, crisp mountain air, and a distinct four-season climate, Coeur d’Alene presents an exceptional retirement backdrop. While the real estate market here leans toward the higher end, the quality of life remains unparalleled. Idaho does not tax Social Security benefits, providing a measure of financial relief to offset the higher housing costs. The town itself features a highly walkable downtown area, vibrant arts festivals, and pristine lakefront parks. Healthcare is robust, with Kootenai Health offering comprehensive medical services directly within the community, ensuring you rarely need to travel far for specialized treatments.

Lake of the Ozarks, Missouri

Boasting more miles of shoreline than the coast of California, the Lake of the Ozarks remains one of the most affordable waterfront retirement destinations in the Midwest. The region caters heavily to active adults who want to spend their days boating, fishing, and golfing. Missouri has recently taken steps to eliminate state income taxes on Social Security benefits, further increasing the financial appeal of this massive reservoir. While the area experiences a surge of summer tourists, retirees often find quiet coves and year-round communities away from the main channels. The Lake Regional Health System provides dedicated care to the area, ensuring your health needs are met right on the water.

Lake Oconee, Georgia

Located midway between Atlanta and Augusta, Lake Oconee offers a distinctly luxurious approach to waterfront retirement. The area is famous for master-planned communities featuring world-class golf courses, private marinas, and extensive wellness centers. Georgia is incredibly welcoming to retirees, offering a substantial retirement income exclusion for residents aged 65 and older. This generous tax policy helps offset the cost of the premium real estate found along the shoreline. When complex medical needs arise, you can easily drive to Atlanta to access Emory Healthcare and other globally recognized medical institutions, providing ultimate peace of mind.

Deep Creek Lake, Maryland

For retirees who want to experience snowy winters and cool, breezy summers while staying close to East Coast family members, Deep Creek Lake is a magnificent choice. Tucked into the mountains of Garrett County, this destination provides a quiet, nature-focused lifestyle. You can spend your autumns hiking through vibrant foliage and your winters cross-country skiing. While Maryland has a reputation for higher taxes, the state has recently implemented targeted tax breaks to help retain retirees. The local hospital in nearby Oakland provides reliable standard care, while major medical hubs in Morgantown, West Virginia, remain highly accessible.

Lake Havasu, Arizona

Where the stark beauty of the Sonoran Desert meets the vibrant blue waters of the Colorado River, Lake Havasu City offers a unique haven for sun-seeking retirees. The area is famous as a winter sanctuary for snowbirds, but it supports a thriving year-round community of older adults. Arizona does not tax Social Security, and property taxes remain highly competitive. You will need to budget for significant air conditioning costs during the intense summer months, but the glorious, temperate winters make the trade-off worthwhile. Havasu Regional Medical Center serves the local population efficiently, ensuring you have immediate access to emergency and routine care.

Lake Champlain, Vermont

Stretching between New York and Vermont, Lake Champlain delivers unparalleled Northeastern charm. Retiring near Burlington gives you access to a progressive, deeply engaged community set against the backdrop of the Adirondack and Green Mountains. Vermont does carry a higher tax burden than many other states on this list, so you must plan your finances meticulously. However, residents consistently argue that the pristine environment, low crime rates, and robust civic services justify the costs. The presence of the University of Vermont Medical Center guarantees you receive some of the best, most innovative healthcare available in the United States.

Navigating Risks and Ensuring Financial Safety

Moving to the water introduces specific risks that you must manage proactively. Standard homeowners insurance policies do not cover damage caused by rising lake waters. You must evaluate the Federal Emergency Management Agency flood maps for any property you consider and purchase separate flood insurance if necessary. Additionally, you need to understand that retaining walls and private docks often require specialized liability coverage.

You also need to remain vigilant against financial exploitation. Scenic vacation destinations frequently attract sophisticated real estate scams targeting out-of-state buyers. Always work with licensed, locally established real estate agents and verify property deeds independently. Connect with fraud prevention networks to learn how to spot wire fraud during closing processes. Finally, review your healthcare coverage; ensure that your specific Medicare Advantage plan or supplemental policy is accepted by the rural providers surrounding your new lake home to avoid catastrophic out-of-network billing.

Expert Perspectives on Waterfront Retirement

Certified Financial Planners consistently emphasize the danger of sequence of returns risk for retirees purchasing expensive waterfront homes early in retirement. Liquidating a large portion of your investment portfolio during a market downturn to buy a lake house can permanently cripple your ability to generate long-term income. Experts recommend exploring mortgage options or bridge loans to maintain portfolio liquidity, even if you have the cash on hand.

Gerontologists offer a different, equally critical perspective regarding physical aging in place. They warn that beautiful multi-level lake homes perched on steep hillsides can become inaccessible as mobility declines. Health experts strongly advise purchasing single-level homes or ensuring a property can easily accommodate elevators, ramps, and widened doorways. Prioritizing universal design features from day one prevents you from being forced out of your dream home due to natural physical aging.

Frequently Asked Questions About Lakefront Retirement

Do lake homes require specialized insurance policies?

Yes, purchasing a home on the water almost always requires additional insurance considerations. Standard homeowners insurance explicitly excludes flood damage. You will need to secure a separate policy through the National Flood Insurance Program or a private carrier. Furthermore, if your property includes a private dock, boat lift, or seawall, you must ensure your policy includes specific riders covering these structures against ice damage, windstorms, and liability if someone is injured on your shoreline.

How do I budget for higher maintenance costs on the water?

Moisture, wind, and specialized waterfront infrastructure accelerate wear and tear on a property. Financial advisors typically suggest setting aside two to three percent of your home’s total value annually for maintenance, rather than the standard one percent recommended for inland homes. You need this expanded budget to handle regular deck sealing, dock repairs, retaining wall stabilization, and pest control management, all of which are amplified when you live directly on the water.

Are lakefront communities accessible as mobility changes?

Accessibility varies wildly depending on the topography of the specific lake. Reservoirs in mountainous regions often feature steep, terraced lots that require navigating dozens of stairs to reach the water. When shopping for your retirement home, you must prioritize properties with gentle slopes, zero-step entries, and main-level living suites. Look for communities that offer paved, flat walking trails and accessible community marinas to ensure you can continue enjoying the water regardless of future mobility challenges.

What tax implications apply to buying a retirement home in a different state?

Relocating across state lines shifts your entire tax landscape. You must establish legal domicile in your new state to claim its tax benefits, which usually requires living there for at least 183 days a year, updating your driver’s license, and registering to vote. Review how different states tax your federal benefits and pension distributions. Some states completely exempt retirement income, while others tax it heavily, dramatically affecting your monthly cash flow and long-term financial sustainability.

Take Your Next Step Toward Waterfront Living

Transforming your dream of a lakefront retirement into reality begins with gathering hard data rather than just browsing beautiful photos. Over the next forty-eight hours, pick one lake destination from this list and research its median home prices and local property tax rates. Compare those figures against your current monthly budget to see how a waterfront move aligns with your financial reality. By taking this single, concrete step today, you initiate the practical planning required to secure a beautiful, sustainable, and deeply rewarding retirement on the water.