The new $6,000 senior tax deduction could dramatically reduce your federal tax burden, but it also sparks serious questions about the long-term funding of Social Security. Passed under the One Big Beautiful Bill Act, this temporary measure allows eligible adults over 65 to keep more of their fixed income right now. You might see a lower tax bill this year, freeing up cash for daily expenses and healthcare. However, because Social Security relies on taxes collected from benefit payments, keeping more money in your pocket today could inadvertently accelerate the depletion of the program’s trust funds. Understanding this complex balancing act helps you protect your retirement strategy against future legislative shifts and unexpected income gaps.

Snapshot: Understanding the New Legislative Landscape

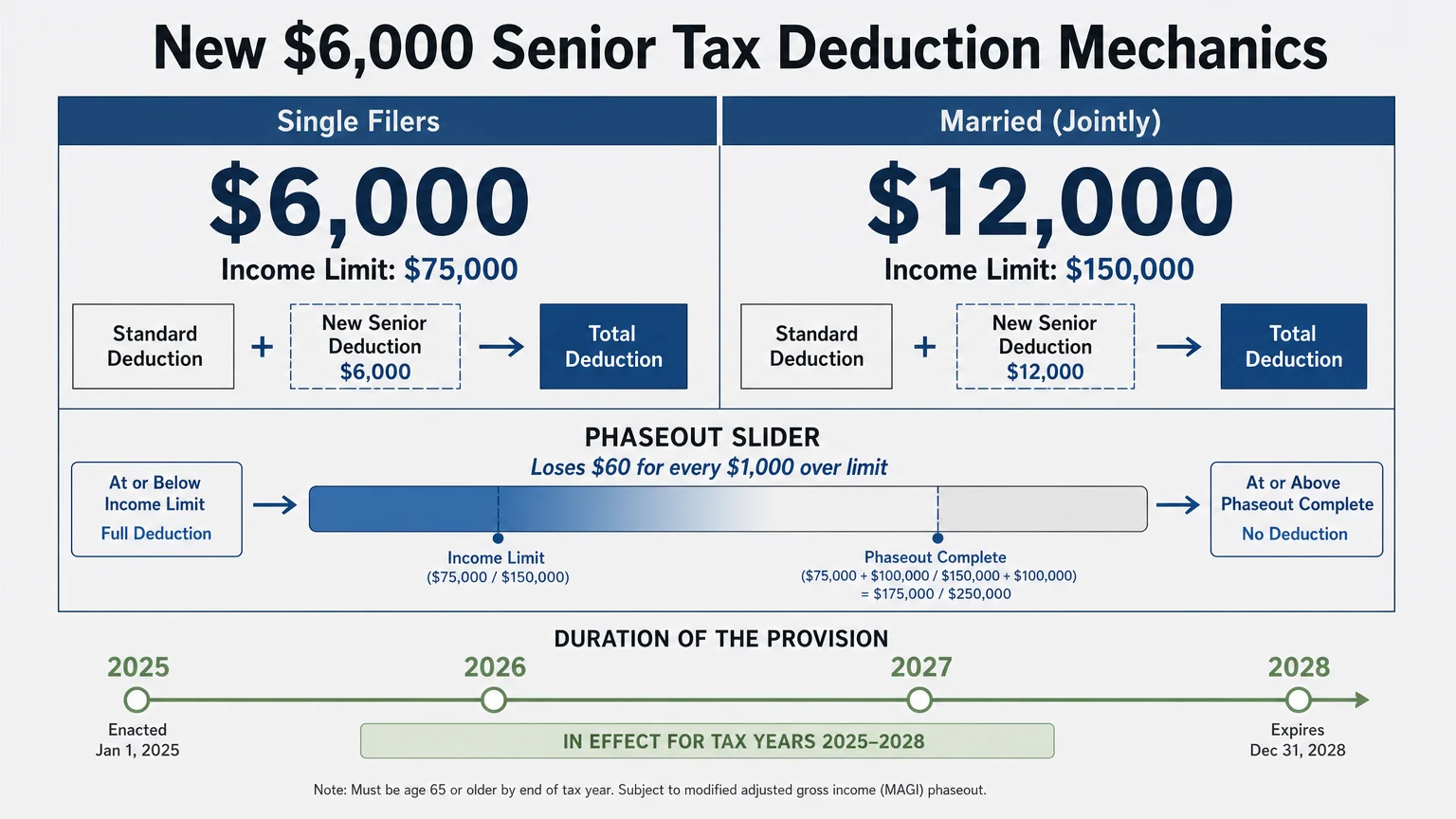

The tax landscape for older Americans shifted dramatically with the passage of the One Big Beautiful Bill Act in July 2025. Among its most prominent features is a new, temporary tax deduction exclusively designed for taxpayers age 65 and older. Valid from the 2025 through 2028 tax years, this provision allows an eligible single filer to deduct up to $6,000 from their taxable income. Married couples filing jointly can deduct up to $12,000 if both spouses meet the age requirement. Crucially, this benefit stacks on top of the standard deduction and the existing extra standard deduction already available to older adults. For the vast majority of retirees navigating fixed budgets, this legislative change represents one of the most substantial tax relief efforts in modern history.

However, lawmakers designed this benefit with strict income phaseout limits to ensure the relief targets middle- and lower-income households. If you file as a single adult, the deduction begins to phase out once your modified adjusted gross income exceeds $75,000. For married couples filing jointly, the threshold stands at $150,000. The phaseout rate is steep; you lose $60 of the deduction for every $1,000 you earn over the limit. This mathematical reality means higher earners could see the benefit vanish completely. Reviewing official tax documentation helps you determine exactly where your household income falls on this sliding scale.

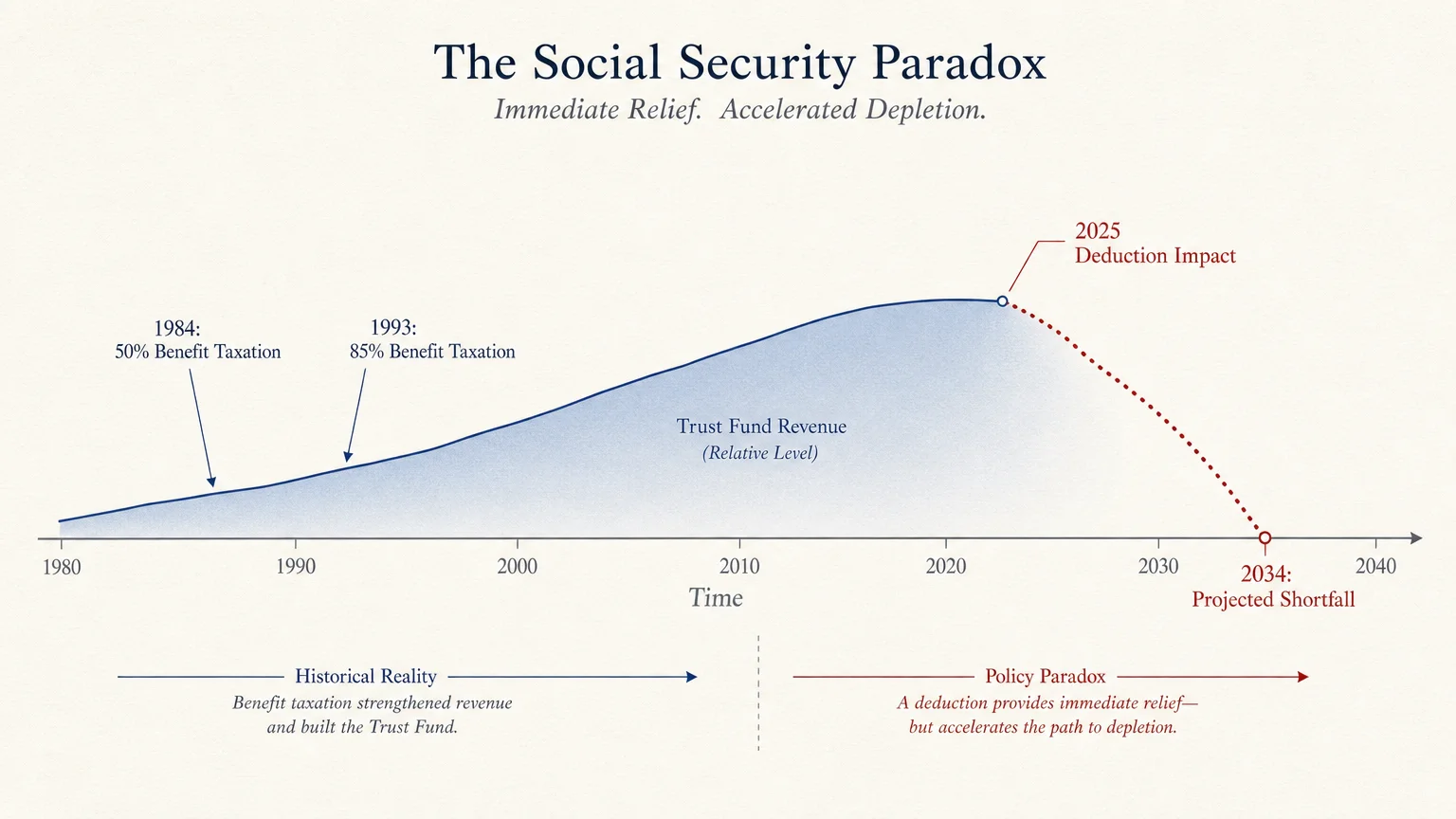

To grasp the profound impact of this deduction, you must understand how the government historically treats retirement income. In 1984, Congress began taxing up to 50 percent of Social Security benefits for higher earners; by 1993, that threshold jumped to 85 percent. For decades, this system quietly captured revenue to bolster the very program it taxed. Today, the new $6,000 deduction effectively shields this income, practically eliminating federal income tax on benefits for an estimated 88 percent of older Americans. Keeping that money in your bank account provides immediate financial relief, but it introduces a severe macroeconomic complication.

A portion of the income tax collected on Social Security benefits funnels directly back into the program’s trust funds. By significantly reducing the taxes you pay, the federal government collects less revenue. According to recent trust fund projections, the system already faced a shortfall projected to hit around 2034. Stripping away tax revenue could accelerate that depletion date, leaving future retirees vulnerable to benefit cuts. You now face a unique paradox: the very policy easing your financial anxiety today could undermine the foundation of your guaranteed income tomorrow.

Strategy Pillars to Navigate Changing Tax Rules

Adjusting to these new legislative realities requires a comprehensive approach. You cannot simply look at your tax return in isolation; you must evaluate how this deduction influences your broader retirement ecosystem. By focusing on income planning, lifestyle design, and health management, you can optimize your finances while safeguarding your future.

Income Planning and Tax Optimization

Because the $6,000 deduction phases out at specific income levels, managing your modified adjusted gross income becomes your primary defense strategy. If you plan to sell a piece of real estate, liquidate a stock portfolio, or withdraw a large sum from a traditional IRA, doing so in a single calendar year could spike your income. This sudden surge might push you over the $75,000 or $150,000 thresholds, completely wiping out your new tax benefit. Spreading those taxable distributions across multiple years allows you to maintain the deduction while still meeting your long-term financial goals.

You can also utilize specific tax vehicles to suppress your recognizable income. Qualified Charitable Distributions serve as an excellent tool for those over age 70 and a half. By transferring funds directly from your IRA to an eligible charity, the distribution satisfies your required minimum distribution but does not count toward your modified adjusted gross income. This maneuver allows you to support causes you care about while safely anchoring your income below the phaseout limits.

Lifestyle Design and Spending Power

Once you secure the deduction, you must decide how to deploy the resulting tax savings. Depending on your effective tax bracket, a $6,000 reduction in taxable income could translate to an extra $700 to $1,500 in your pocket annually. In an economic environment marked by fluctuating inflation, this additional cash serves as a vital shock absorber for your purchasing power. Tracking consumer expenditure data reveals that housing, food, and transportation consume the vast majority of a retiree’s budget. Reinvesting your tax savings into these foundational areas provides immediate stability.

Consider allocating these funds toward lifestyle enhancements that promote independence and cultural connection. This might involve purchasing ergonomic furniture, funding accessible home modifications like grab bars and walk-in showers, or simply ensuring you have the budget to participate in culturally resonant community activities. Financial flexibility directly correlates with your quality of life, allowing you to maintain purpose and joy regardless of your physical mobility or background.

Health and Wellness Funding

Health and wealth operate on a continuous feedback loop during retirement. The tax savings generated by the new deduction offer an excellent opportunity to fund preventative care that traditional insurance might not fully cover. You might use the extra funds to access specialized physical therapy, dietary counseling tailored to your cultural traditions, or out-of-pocket dental procedures. Investing in your physical well-being today often prevents catastrophic medical expenses down the road.

Furthermore, intentionally keeping your income below the deduction’s phaseout thresholds provides a hidden healthcare benefit. Medicare Part B and Part D premiums are tied directly to your income level through the Income-Related Monthly Adjustment Amount. If your income spikes, you lose your $6,000 tax deduction and face expensive surcharges on your monthly healthcare premiums. Consulting federal healthcare resources ensures you understand exactly how your tax strategy impacts your medical coverage costs.

Expert Voices on the Deduction and Trust Fund

Financial professionals generally view the new senior tax deduction as a powerful, albeit precarious, planning tool. Certified Financial Planner practitioners frequently advise their clients to embrace the immediate tax relief but warn against integrating it into permanent, decades-long financial models. Because the deduction expires in 2028, experts stress the importance of building adaptable withdrawal strategies. They encourage you to save the windfall rather than inflate your baseline lifestyle, ensuring you remain insulated if Congress allows the provision to sunset.

From a gerontological perspective, researchers emphasize the psychological relief this tax break provides. Financial anxiety represents a leading cause of chronic stress among older adults, which can elevate blood pressure, disrupt sleep, and accelerate cognitive decline. Advocacy research highlights that when retirees feel confident about their monthly budget, their overall physical health stabilizes. The certainty of a lower tax bill translates directly into mental peace, proving that economic policy is inherently tied to public health outcomes.

Everyday retirees offer a more nuanced view, balancing personal relief with generational concern. Many older Americans express deep gratitude for the extra cash, noting it helps them afford rising utility bills and grocery costs. However, they simultaneously voice apprehension about the Social Security trust fund. Knowing that their immediate tax break could diminish the very system their children and grandchildren will eventually rely on creates a complex emotional landscape. This tension underscores the need for sustainable, long-term legislative reform.

Risks and Safeguards in the Current Environment

While the new tax deduction offers undeniable benefits, navigating the modern retirement landscape requires heightened vigilance. The intersection of changing tax laws and fixed incomes creates unique vulnerabilities that you must proactively manage.

The Hidden Benefit Cliffs

The 6 percent phaseout acts as a stealth tax bracket that can easily catch you off guard. If you earn exactly $1,000 over the limit, you immediately lose $60 of the deduction. Miscalculating a capital gain from the sale of a mutual fund or executing a Roth conversion at the wrong time could push you slightly over the edge, causing a cascading loss of tax benefits. You must meticulously project your year-end income before making any major financial moves to avoid tumbling off this benefit cliff.

Scams and Fraudulent Claims

Fraudsters constantly adapt their tactics to exploit new legislation, and the One Big Beautiful Bill Act is no exception. Scammers are actively calling older adults, offering to “activate” the new senior bonus deduction in exchange for a Social Security number, banking details, or an upfront processing fee. You must remember that the deduction applies automatically when you file your qualified tax return. The Internal Revenue Service will never call, text, or email you demanding personal information or immediate payment. Protect your identity by ignoring unsolicited communications and working only with verified professionals.

Healthcare Pitfalls

Feeling wealthier due to a sudden tax break might tempt you to cut corners elsewhere. Some retirees mistakenly view the extra cash as a reason to drop their supplemental health insurance, assuming they can simply pay for minor medical issues out of pocket. This line of thinking carries immense risk. You should always retain your comprehensive healthcare coverage; a single unexpected medical emergency can easily wipe out a $6,000 tax deduction and devastate your life savings.

Frequently Asked Questions

Do I need to itemize my deductions to claim the new tax break?

No, you do not need to itemize your taxes to benefit from this legislation. The $6,000 senior tax deduction is specifically designed to stack directly on top of the standard deduction, as well as the existing extra standard deduction for those over 65. You claim it on your standard tax return forms, making it highly accessible for individuals who rent their homes or have completely paid off their mortgages and no longer have significant interest to deduct.

Will this deduction permanently eliminate my taxes on Social Security?

The current legislation is strictly temporary. The deduction is scheduled to sunset at the end of the 2028 tax year unless lawmakers intervene and vote to extend it. While it successfully shields benefits from taxation for many retirees right now, you should plan your long-term financial strategy with the assumption that tax rates could eventually revert to their previous, higher levels.

How exactly does taking this deduction affect the Social Security trust fund?

A specific portion of the income tax collected on Social Security benefits is legally required to funnel back into the program’s trust funds. By significantly reducing the federal income taxes older Americans pay, the government collects much less revenue. Recent actuarial projections suggest that this reduction in incoming funds could accelerate the trust fund’s depletion date, placing additional pressure on Congress to enact comprehensive structural reforms.

What happens if my income exceeds the phaseout limits?

If your modified adjusted gross income surpasses $75,000 as a single filer or $150,000 as a married couple filing jointly, the deduction gradually decreases. Specifically, you lose $60 of the deduction for every $1,000 you earn over the threshold. Once your income reaches $175,000 as a single filer or $250,000 as a joint filer, the benefit disappears entirely, meaning you will face the standard tax rates on your retirement income.

Your Next Move

Taking control of your financial future requires immediate, focused action rather than passive observation. Review your most recent tax return or annual income statement to determine exactly where your modified adjusted gross income falls in relation to the new phaseout limits. Within the next 48 hours, schedule a brief consultation with a credentialed tax professional or use a reliable online tax calculator to run a mock projection for your upcoming filing. Identifying your exact income threshold today empowers you to make strategic withdrawal decisions, optimize your healthcare spending, and confidently navigate the evolving landscape of retirement taxation without jeopardizing your long-term security.