Leaving the workforce ahead of schedule looks like the ultimate financial victory until unexpected math and missing routines turn your dream into a source of stress. Recognizing the warning signs that you retired too early allows you to course-correct before minor miscalculations threaten your long-term security. Stepping away requires more than hitting a target savings number; it demands comprehensive readiness across your finances, health, and daily purpose. You must critically evaluate your income sustainability, access to affordable medical coverage, and social engagement. Identifying these critical gaps right now empowers you to adjust your strategy, protect your hard-earned nest egg, and reclaim your peace of mind for the decades ahead.

The Current Retirement Landscape and Market Realities

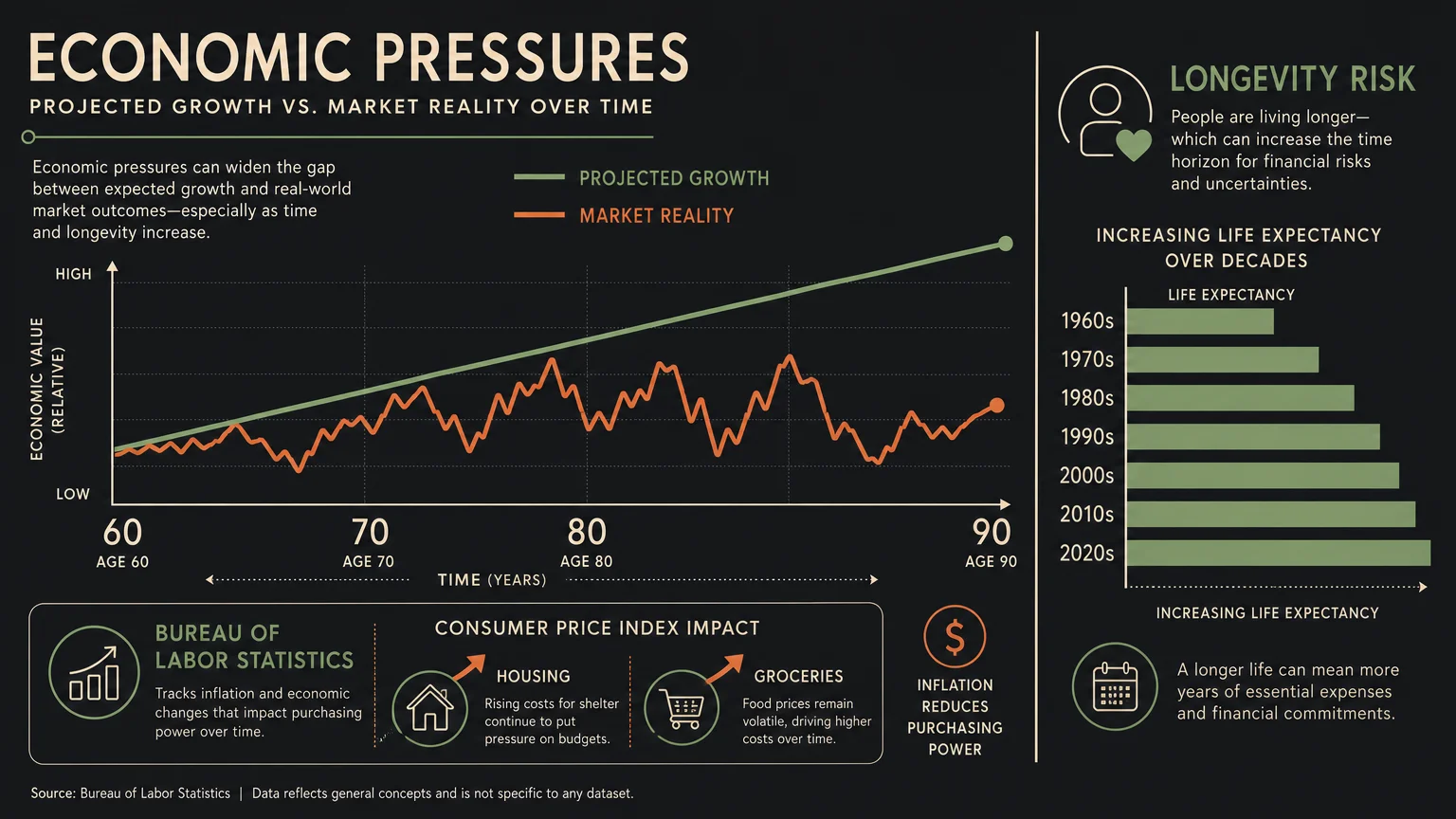

Navigating the transition out of the workforce requires a deep understanding of today’s complex economic realities. Over the past few years, shifting inflation rates and unpredictable market volatility have forced millions of pre-retirees and current retirees to rethink their financial timelines. When the cost of housing, groceries, and essential services climbs rapidly, your fixed income or portfolio withdrawals lose substantial purchasing power. Data from the Bureau of Labor Statistics frequently highlights the outsized impact that rising consumer prices have on older adults, particularly those who rely entirely on static income streams. If you left your career during a booming bull market, you likely projected a straight-line growth trajectory for your investments. However, prolonged periods of market stagnation or high inflation quickly erode the mathematical foundation of an early exit. You must continuously monitor these broader economic indicators to ensure your baseline assumptions remain valid. Ignoring these external pressures often leads to the first and most damaging miscalculations of premature retirement.

Beyond market dynamics, increasing life expectancy radically alters the math of leaving the workforce in your fifties or early sixties. Modern medicine allows you to enjoy a longer, more active lifespan, but funding an additional three or four decades without a steady paycheck requires immense capital. You face the daunting task of stretching your accumulated assets over a timeline that earlier generations never had to consider. When you combine longer lifespans with elevated living costs, the margin for error shrinks dramatically. A solid retirement plan must absorb these macroeconomic shifts and longevity risks without jeopardizing your daily standard of living.

Warning Sign 1: Your Withdrawal Rate Outpaces Your Portfolio Growth

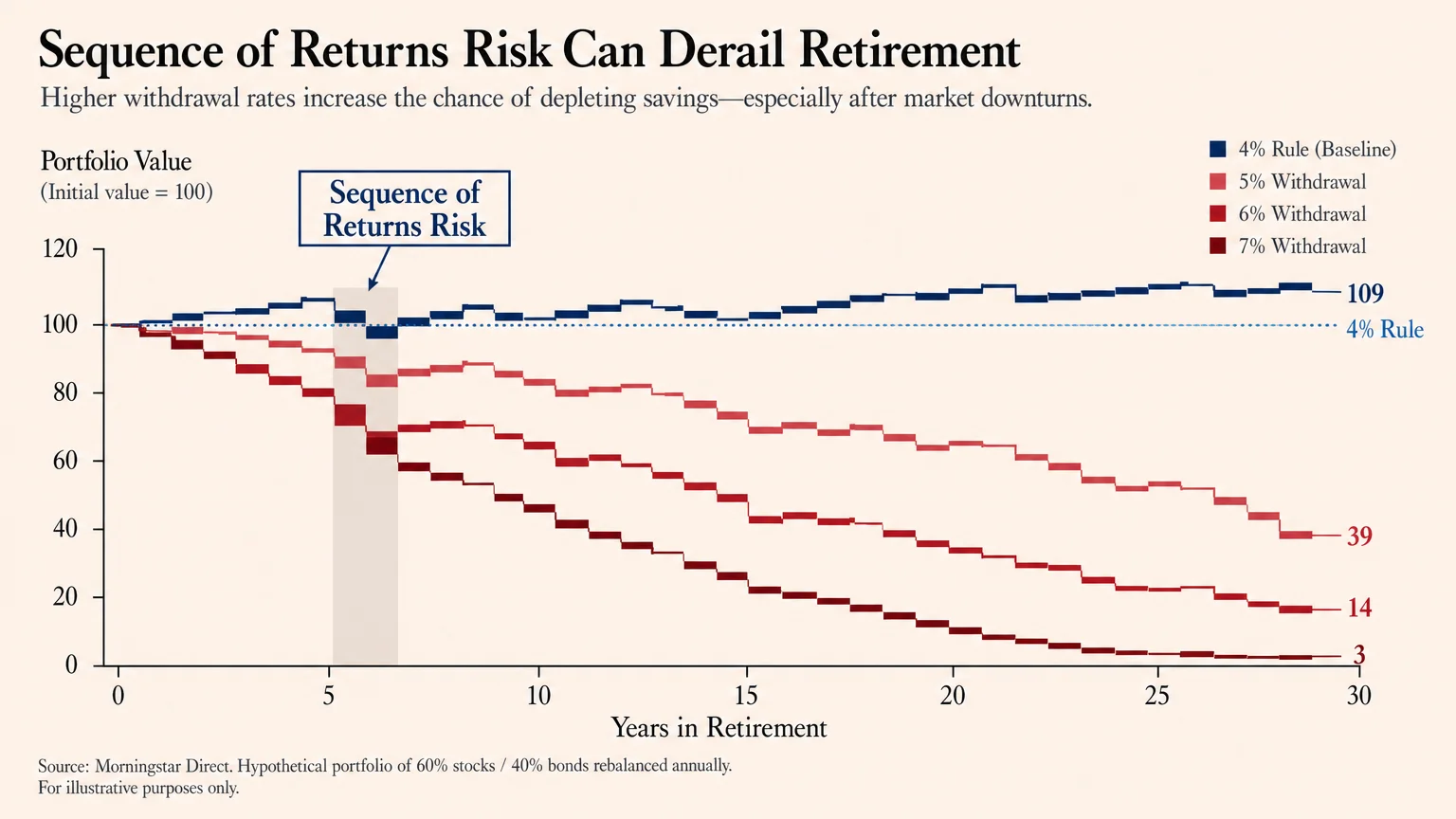

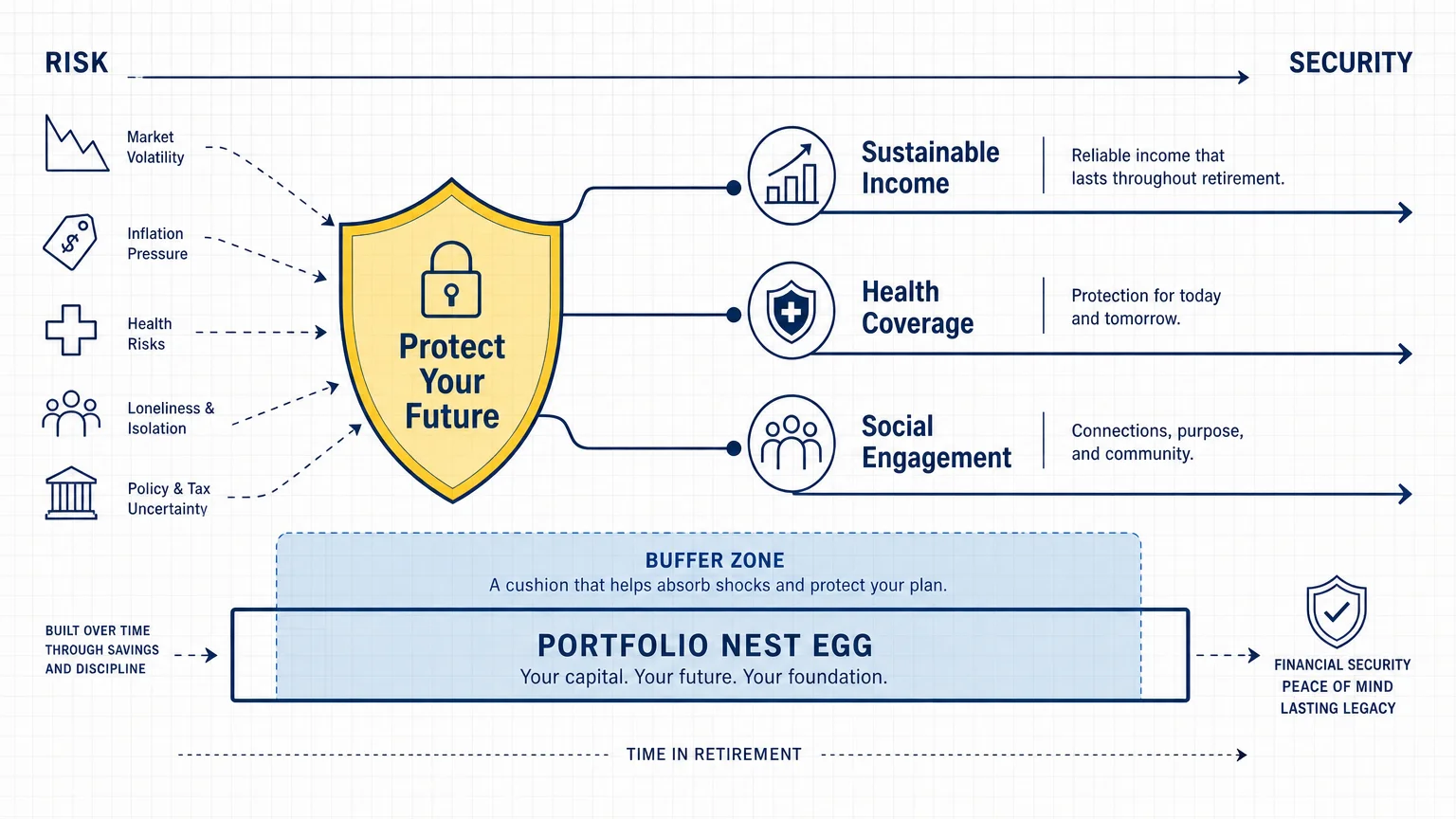

The most immediate and glaring indicator that you retired too soon appears in your monthly portfolio statements. Relying on an unsustainable withdrawal rate depletes your nest egg far faster than the market can replenish it. Financial professionals historically recommended the four percent rule as a safe baseline, but applying that same static metric to a retirement lasting forty years carries immense risk. If you find yourself consistently pulling five, six, or seven percent from your investment accounts just to cover basic household bills and property taxes, your financial foundation is actively crumbling. This aggressive drawdown exacerbates sequence of returns risk; if you sell off large portions of your portfolio during a market downturn, those assets will never benefit from the eventual market recovery.

Furthermore, an early exit often forces you to tap into tax-advantaged accounts before you reach the statutory age limits. Navigating the complex tax codes becomes a major hurdle when you desperately need cash flow. You can review the specific age requirements and penalty structures through the Internal Revenue Service, which clearly outlines the steep costs associated with premature distributions. Surrendering ten percent of your hard-earned money to early withdrawal penalties significantly damages your long-term sustainability. If you cannot fund your early retirement years through cash reserves, taxable brokerage accounts, or passive income streams without triggering these severe IRS penalties, you likely pulled the trigger on your career too soon.

Warning Sign 2: You Feel Isolated and Lack Daily Purpose

Retirement fundamentally rewires your daily existence, and stripping away the built-in socialization of a workplace often leaves an unexpected void. You might assume that endless free time automatically translates to endless happiness, but a profound lack of purpose serves as a major psychological warning sign. During your career, your job provided a clear structure, a dependable social network, and a distinct sense of identity. Once you leave that environment—often abruptly—the responsibility of manufacturing purpose falls entirely on your shoulders. Waking up on a Tuesday morning with absolutely no obligations might feel liberating for the first few months. Eventually, that novelty quickly fades into boredom and isolation; you must actively construct a new reality to thrive.

Gerontologists and behavioral researchers consistently note that older adults who lack a compelling reason to get out of bed face higher risks of cognitive decline and depression. If you spend your days passively consuming television or endlessly scrolling through the internet because you have no structured activities, you are experiencing a core symptom of premature retirement. Successful retirees actively design their lifestyle before they hand in their resignation letters. They cultivate deep hobbies, establish regular volunteer commitments, and intentionally build social circles outside of their former colleagues. You must treat your mental and emotional engagement with the exact same level of seriousness as your investment portfolio. If you feel entirely disconnected from your community and your sense of self-worth has vanished alongside your job title, it is time to rethink your daily routine and perhaps re-engage with the workforce on your own terms.

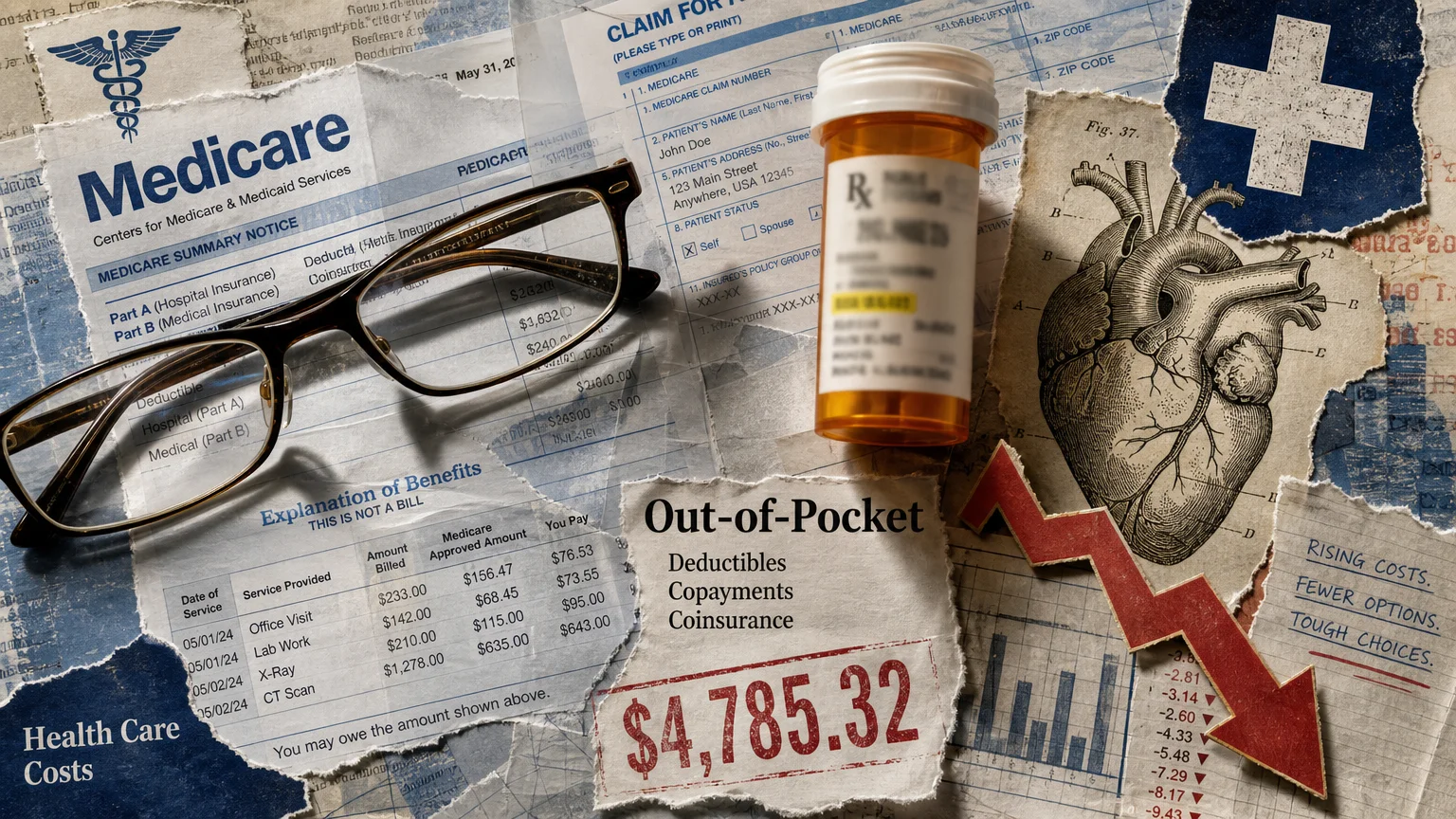

Warning Sign 3: Healthcare Costs Are Consuming Your Budget

Leaving your employer usually means leaving behind subsidized health insurance, and the extreme sticker shock of the private market catches many early retirees completely off guard. If your monthly premiums, high deductibles, and out-of-pocket medical expenses are aggressively eating into your discretionary spending, you face a massive red flag. Pre-Medicare individuals must navigate the Affordable Care Act marketplace or utilize expensive COBRA continuation coverage, both of which can cost thousands of dollars annually. When you underestimate the sheer velocity of healthcare inflation, a single unexpected medical event can derail your entire financial plan. A broken bone, a sudden chronic illness diagnosis, or a minor surgery can instantly drain the cash reserves you originally earmarked for travel and leisure.

You cannot simply ignore minor health issues to save money; delaying preventative care ultimately leads to catastrophic health and financial outcomes down the road. Understanding the exact timeline for federal healthcare benefits is absolutely critical to your survival strategy. You can explore the specific enrollment windows and coverage details directly through Medicare, which activates for most Americans at age sixty-five. If you retired at fifty-five, you face a rigorous ten-year gap where you must single-handedly bear the full brunt of medical insurance costs. If you failed to accumulate a dedicated healthcare war chest or a robust Health Savings Account to bridge this specific gap, your early retirement remains highly vulnerable to medical shocks.

Expert Voices: Navigating the Complexities of an Early Exit

Certified Financial Planner professionals and gerontology experts uniformly agree that a successful early retirement requires a holistic approach, moving far beyond simple asset accumulation. Wealth managers frequently observe clients who hit a specific net worth milestone and immediately quit their jobs, only to panic a year later when the harsh reality of funding their lifestyle sets in. These financial experts emphasize the importance of stress-testing your portfolio against multiple worst-case scenarios, including prolonged bear markets, localized real estate crashes, and hyperinflation. They strongly advocate for dynamic spending strategies, where you voluntarily reduce your discretionary withdrawals during bad market years to preserve your underlying principal.

On the lifestyle front, aging experts stress the psychological concept of retiring to something rather than merely retiring from a stressful career. Researchers who study life transitions point out that humans inherently thrive on moderate challenges and meaningful contribution. If you sprinted away from burnout without a clear vision for your next chapter, the sudden decompression can actually trigger intense anxiety. The consensus among these professionals is clear: an early exit demands rigorous emotional preparation. Building resilience means acknowledging that your initial retirement plan will inevitably require adjustments. By listening to those who study longevity and wealth preservation, you can implement effective safeguards that protect both your mental health and your bank account.

Crucial Risks and Safeguards to Protect Your Future

An underfunded early retirement introduces a dangerous element of desperation, making you highly susceptible to sophisticated financial risks. When you realize your portfolio is shrinking faster than anticipated, you might feel tempted to chase impossibly high yields or engage in highly speculative investments. Cybercriminals and fraudsters specifically target older adults who feel anxious about their dwindling resources. They present seemingly foolproof investment schemes that promise to double your income or eliminate your tax burden. You can educate yourself on the latest predatory tactics by reviewing essential resources from the AARP Fraud Watch Network, which tracks emerging threats against retirees. Safeguarding your nest egg requires you to maintain a healthy skepticism toward any opportunity that sounds entirely too good to be true.

Additionally, you must vigilantly monitor benefit cliffs related to your total household income. If you secure subsidized health insurance through the federal marketplace, drawing too much income from a taxable account can instantly push you over a crucial threshold. This mistake causes you to lose those subsidies and drastically increases your monthly premiums. You also face severe consequences if you claim Social Security at age sixty-two while simultaneously returning to the workforce. Earning over the annual limit will result in the temporary withholding of your benefits, confusing your cash flow and frustrating your attempts to generate extra money. Protecting your future requires a defensive posture; you must map out exactly how every withdrawal, part-time paycheck, and investment decision impacts your broader tax and subsidy ecosystem.

Frequently Asked Questions About Retiring Too Early

Can I return to work after officially declaring my retirement?

Absolutely. Returning to the workforce is a highly effective way to course-correct if you realized that you retired prematurely. Many older adults pursue consulting, freelance work, or part-time roles to generate supplemental income without the immense stress of a forty-hour corporate grind. This approach, often called a phased retirement or a returnship, allows you to preserve your investment portfolio while regaining a sense of daily structure and social engagement. You hold total control over how and when you re-enter the labor market.

What happens if I claim Social Security early but then change my mind?

The federal government provides a very narrow window for you to reverse this specific decision. If you file for your retirement benefits but realize you made a mathematical mistake, you have precisely twelve months from your initial approval date to withdraw your application. You must repay all the money you and your family received during that period. You can find the exact withdrawal forms and official guidelines through the Social Security Administration. Utilizing this do-over strategy allows your future benefits to continue growing until you reach your full retirement age.

How do I bridge the expensive healthcare gap before age sixty-five?

Bridging this gap requires careful financial maneuvering and proactive planning. Your primary options include the Affordable Care Act marketplace, joining a working spouse’s employer-sponsored plan, or exploring part-time jobs that offer medical benefits to hourly workers. You must carefully manage your modified adjusted gross income to qualify for premium tax credits on the marketplace. Thoroughly comparing out-of-pocket maximums and prescription drug coverage across different plans will prevent unexpected medical bills from destroying your monthly budget.

Does working a part-time job permanently reduce my early Social Security benefits?

Working while collecting early benefits does not permanently erase your hard-earned money. If you earn above the annual limit before reaching your full retirement age, the government temporarily withholds a portion of your monthly check. However, once you hit your full retirement age, your benefit amount is recalculated upward to account for the exact months where your payments were withheld. Understanding this mechanic allows you to comfortably earn active income without fearing that you have permanently surrendered your benefits.

Your Next Steps to Reclaim Your Retirement Strategy

Realizing that you may have stepped away from your career too soon is not a failure; it is simply a clear signal that your strategy requires an immediate update. You possess the power, the life experience, and the time to reshape your financial reality and build a lifestyle that genuinely supports your goals. Instead of ignoring the glaring warning signs, face the math and the emotional realities head-on. A slight adjustment to your withdrawal rate, a new part-time passion project, or a careful review of your healthcare options can dramatically shift your trajectory toward lasting stability.

Within the next forty-eight hours, commit to making one concrete change to fortify your future. Sit down with your recent bank statements and clearly map out your true monthly spending, or reach out to a fee-only fiduciary financial planner for an objective portfolio review. Taking decisive action today transforms your underlying anxiety into empowerment, ensuring that your retirement years remain a time of profound joy, security, and personal fulfillment.