Women face a unique set of financial and biological realities that demand a custom-built retirement plan. You can secure a resilient, comfortable future by acknowledging these gender-specific hurdles and proactively designing a strategy to overcome them. Standard retirement advice often assumes continuous career trajectories and average lifespans, leaving women dangerously underfunded for the final decades of life. Because you live longer on average, experience more career interruptions for caregiving, and generally earn less during your working years, a generic financial roadmap will fall short. By adopting a female-focused approach to income generation, healthcare planning, and investment risk, you ensure your savings outlast your lifespan and support the lifestyle you deserve.

Current Landscape: Navigating Policy Shifts and Market Realities

Recent changes to retirement legislation directly impact how you build your financial safety net. The SECURE 2.0 Act pushed the required minimum distribution age to 73, and eventually to 75, giving your tax-deferred investments more time to grow. Additionally, higher catch-up contribution limits for older workers offer a crucial window to accelerate your savings if you entered the workforce late or took time off. Despite these positive policy shifts, persistent inflation continues to pressure fixed incomes. You need a strategy that embraces these new legislative tools while aggressively defending your purchasing power against rising living costs.

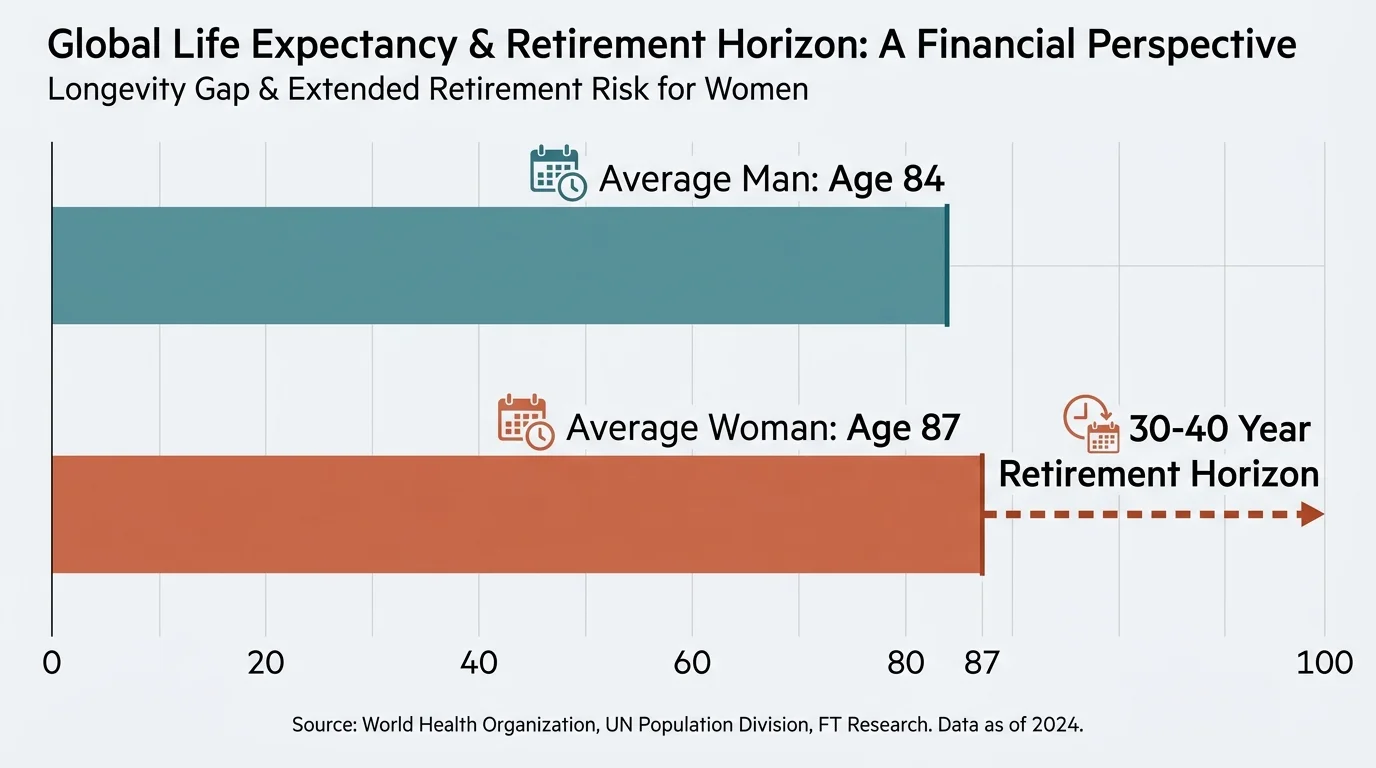

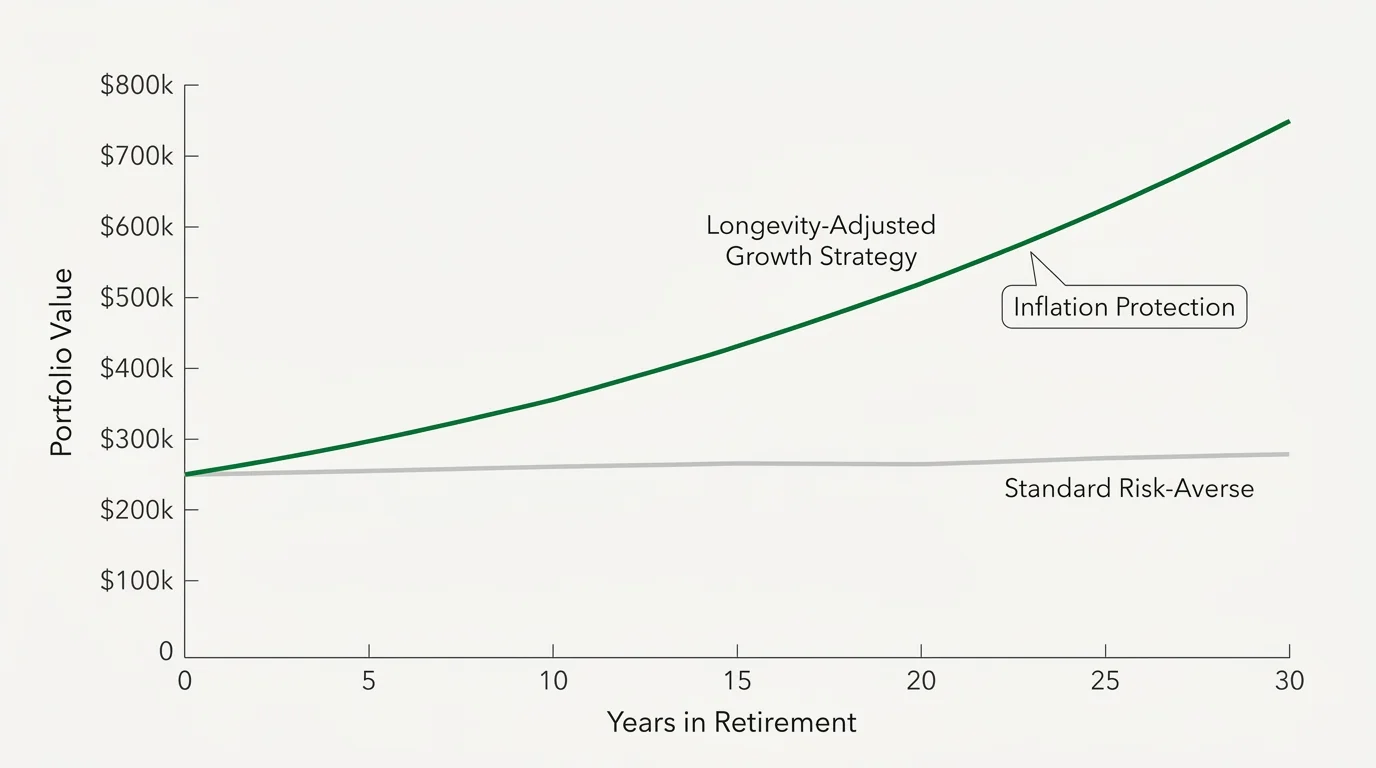

Reason 1: Longer Life Expectancy Requires a Stretched Portfolio

Actuarial data consistently proves that women outlive men. According to the Social Security Administration, a 65-year-old woman today can expect to live to nearly 87, while a 65-year-old man averages just under 84. These three extra years—often stretching into a decade or more—mean your money simply has to last longer. A retirement portfolio designed to deplete at age 85 works perfectly for the average man but introduces severe longevity risk for you. You must plan for a 30-year or even 40-year retirement horizon.

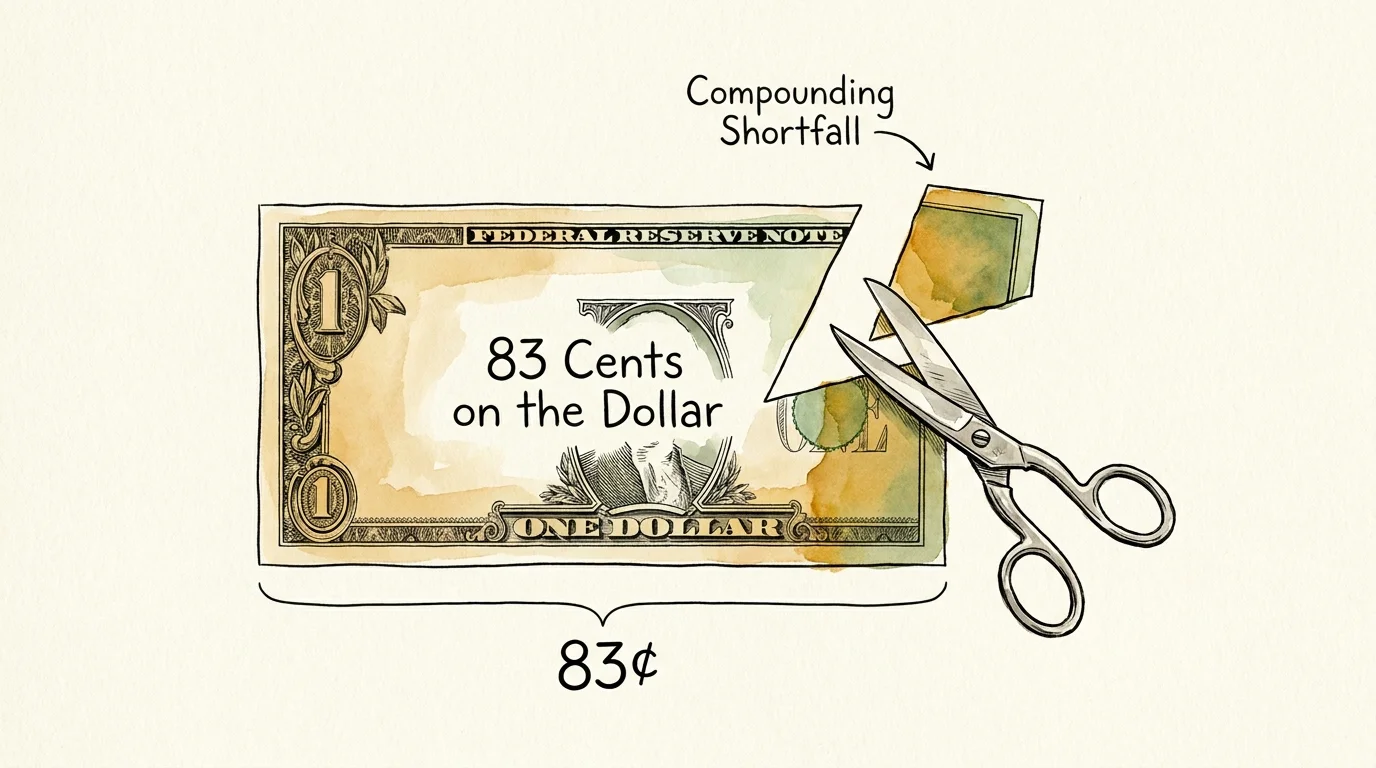

Reason 2: The Persistent Wage Gap Means Smaller Nest Eggs

Earning less during your prime working years dictates the size of your ultimate nest egg. Recent Bureau of Labor Statistics earnings reports indicate that women still earn roughly 83 cents for every dollar men earn. Over a 40-year career, this discrepancy compounds dramatically. Lower wages result in smaller employer matches, reduced 401(k) contributions, and lower overall compound growth. Recognizing this shortfall early allows you to aggressively utilize tax-advantaged accounts to bridge the gap.

Reason 3: Caregiving Interruptions Erode Social Security Benefits

Society relies heavily on women to provide unpaid care for children and aging parents. Leaving the workforce for five to ten years creates zeroes on your earnings record. Social Security calculates your benefit based on your highest 35 years of earnings. When you replace several high-earning years with zeroes, your primary insurance amount drops permanently. You must actively plan around these Social Security Administration data on women to maximize your claiming strategy and compensate for caregiving penalties.

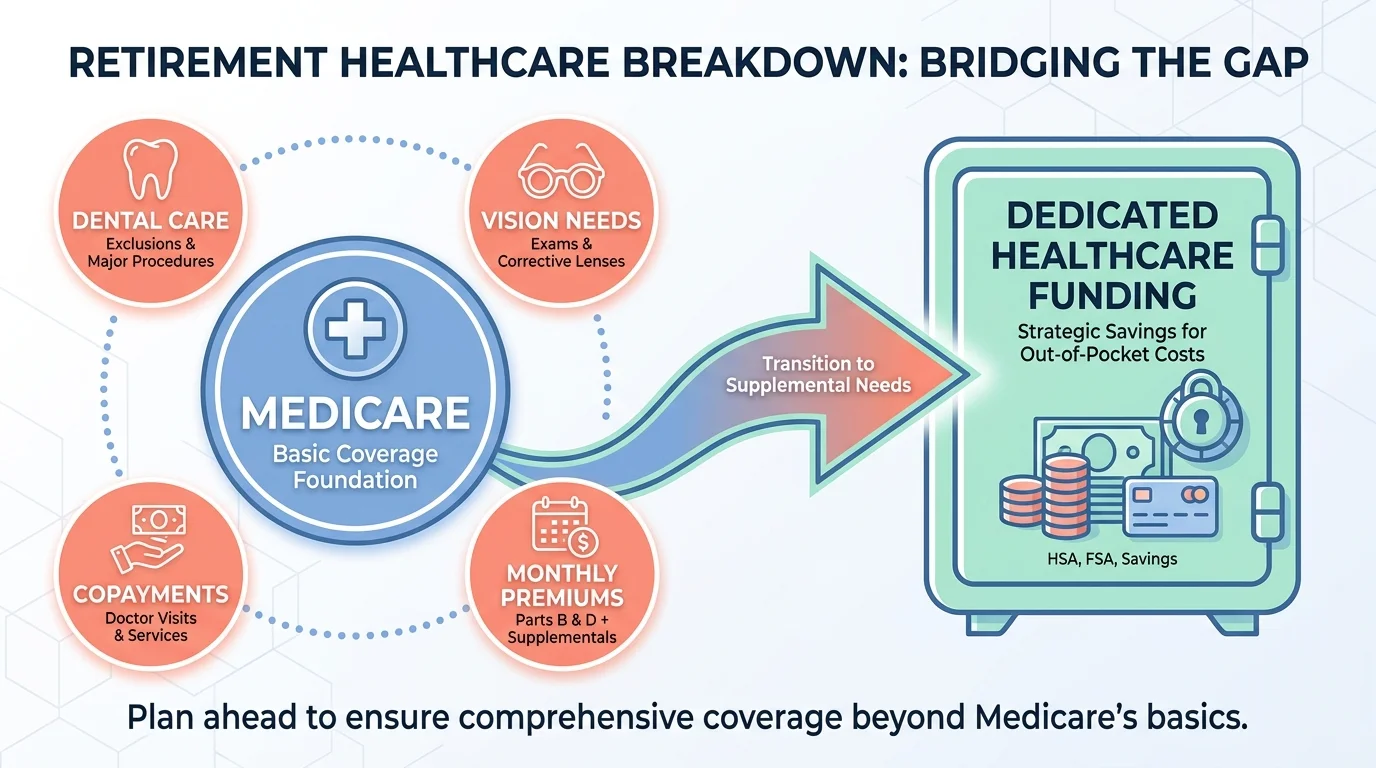

Reason 4: Higher Lifetime Healthcare Costs Demand Dedicated Funding

Living longer translates directly to spending more on healthcare. Financial institutions routinely estimate that a healthy 65-year-old woman will spend significantly more on out-of-pocket medical expenses throughout retirement than her male counterpart. Medicare covers a substantial portion of acute care, but it does not cover everything. Copayments, premiums, dental care, and vision needs add up quickly over a three-decade retirement. You must earmark a dedicated portion of your portfolio—often through a Health Savings Account—specifically for long-term medical expenditures.

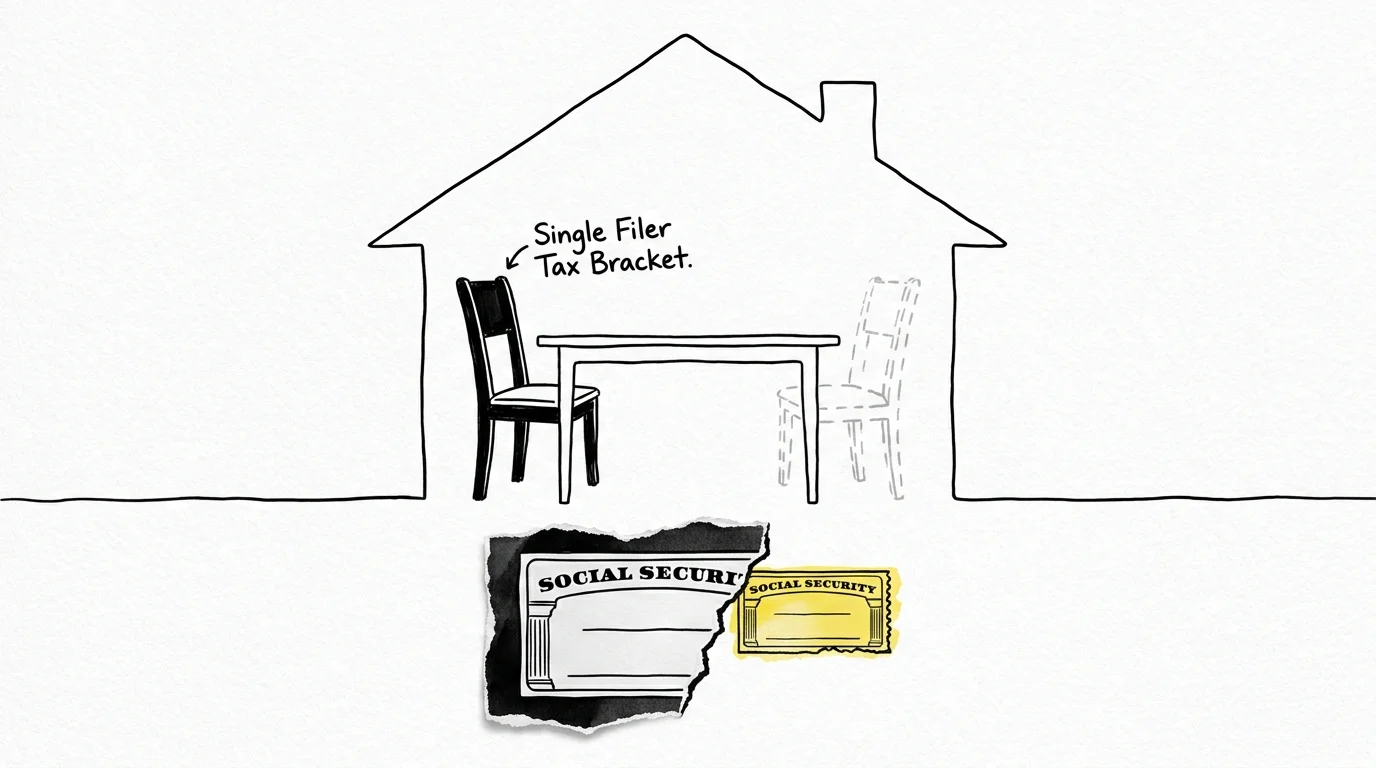

Reason 5: Surviving a Spouse Alters Tax Brackets and Income

The “widow’s penalty” catches many women off guard. When a spouse passes away, the household loses the smaller of the two Social Security checks. Simultaneously, your tax filing status shifts from Married Filing Jointly to Single. This status change shrinks your standard deduction and compresses your tax brackets. You might find yourself paying higher taxes on a reduced overall income. Implementing strategic Roth conversions during your married years can shield you from this sudden tax burden later.

Reason 6: Different Investment Risk Profiles Impact Growth

Studies show women tend to prioritize capital preservation over aggressive growth, often holding a higher percentage of cash in their portfolios. While avoiding loss feels secure in the short term, avoiding the stock market poses a massive long-term risk. Over a 30-year retirement, inflation ruthlessly degrades the purchasing power of cash. You need a growth-oriented asset allocation early in retirement to ensure your portfolio outpaces inflation and sustains your lifestyle.

Reason 7: Long-Term Care Needs Fall Disproportionately on Women

Because women outlive men, they often provide end-of-life care for their husbands at home. However, when women eventually need care themselves, they typically live alone and must hire outside help or move to an assisted living facility. According to the Administration for Community Living, women use formal long-term care services at much higher rates than men. Factoring the cost of facility care or professional home aides into your financial plan is non-negotiable.

Reason 8: Gray Divorce Severely Fragments Retirement Assets

Divorce rates among adults over 50 have surged in recent decades. Splitting a single household into two drastically reduces your financial efficiency just as you approach the finish line. Dividing retirement accounts, selling a primary residence, and absorbing independent living costs can devastate a once-solid financial plan. You must evaluate your independent financial standing and secure proper legal guidance to protect your share of the marital assets via Qualified Domestic Relations Orders.

Reason 9: Inflation Hits Female-Centric Budgets Harder

A longer lifespan gives inflation more time to erode your wealth. If inflation averages 3 percent annually, the cost of living doubles every 24 years. Since your retirement could easily stretch beyond two decades, you will likely see the price of groceries, utilities, and property taxes double in your lifetime. Relying entirely on fixed-income investments like bonds guarantees a loss of purchasing power. You must maintain equity exposure to combat the silent thief of inflation.

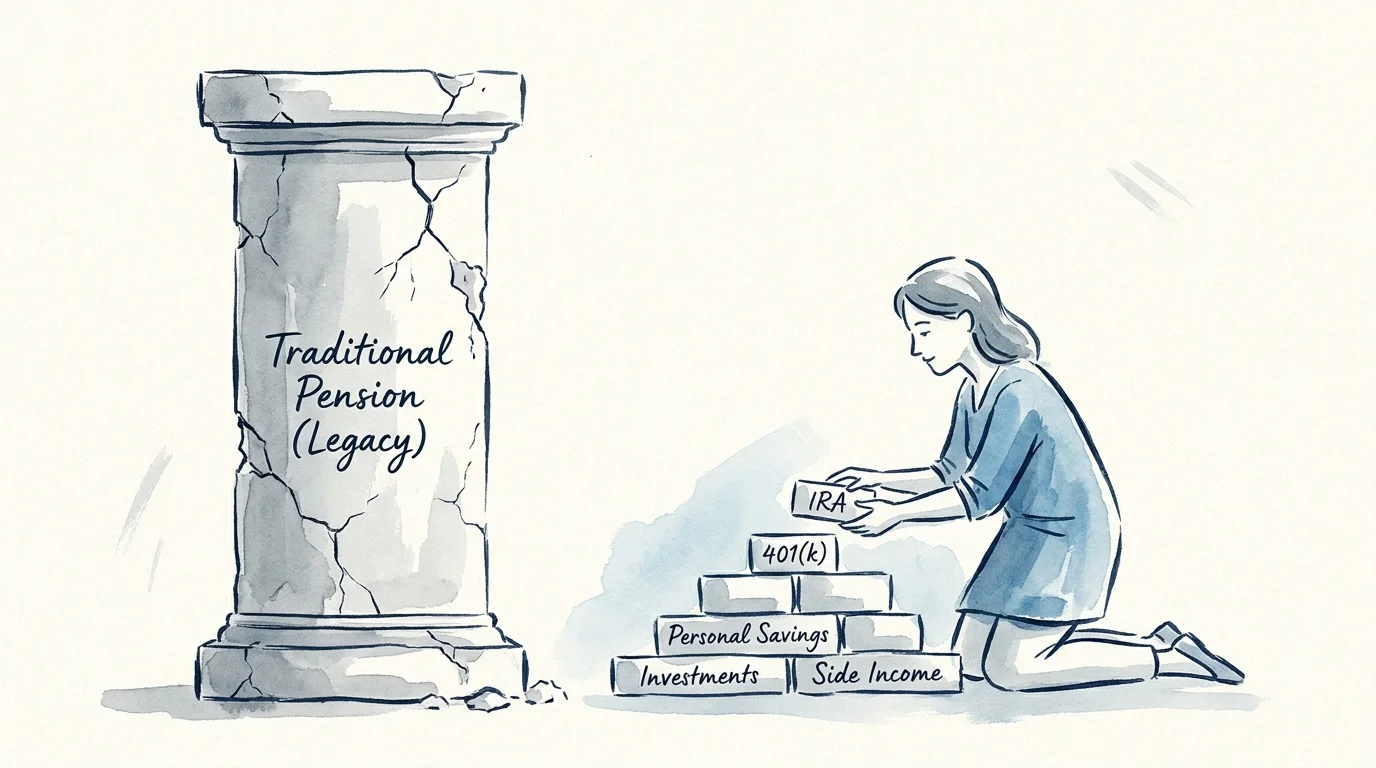

Reason 10: Fewer Pension Options Shift the Burden Entirely to Savings

Historically, women congregated in employment sectors—such as retail, education, and part-time roles—that offered fewer defined-benefit pension plans. Without a guaranteed monthly pension check to rely on, the entire burden of generating income falls on your personal savings and Social Security. This reality makes careful withdrawal strategies and portfolio management absolutely critical to your financial survival.

Strategy Pillars: Building Your Personalized Retirement Architecture

You can overcome these distinct challenges by organizing your plan around three core pillars. First, focus on robust income planning. Delaying your Social Security claim until age 70 provides a guaranteed, inflation-adjusted 8 percent increase in your benefit for every year you wait past your full retirement age. You might also explore guaranteed income products like fixed annuities to cover your baseline expenses, ensuring you never run out of money for essentials.

Second, prioritize intentional lifestyle design. Evaluate your housing needs realistically. Downsizing to a single-story home or a maintenance-free community reduces your fixed monthly overhead and protects you against mobility issues later in life. Building strong social networks and finding purposeful activities also staves off the isolation that often accompanies aging alone.

Third, integrate health and wellness into your financial plan. Invest time in strength training and preventative healthcare today to preserve your physical independence tomorrow. Review your Medicare Supplement or Advantage plans annually to ensure your coverage matches your current medical needs, preventing surprise bills from derailing your budget.

Expert Voices: Perspectives from the Front Lines of Wealth Management

Financial professionals who specialize in eldercare constantly emphasize the need for female-centric planning. “We see brilliant women step into retirement with portfolios built for a man’s lifespan,” says Sarah Jenkins, a certified financial planner specializing in gerontology. “They forget to account for the decade they will likely spend living alone. The mathematical reality requires us to focus on asset growth well into their 70s.”

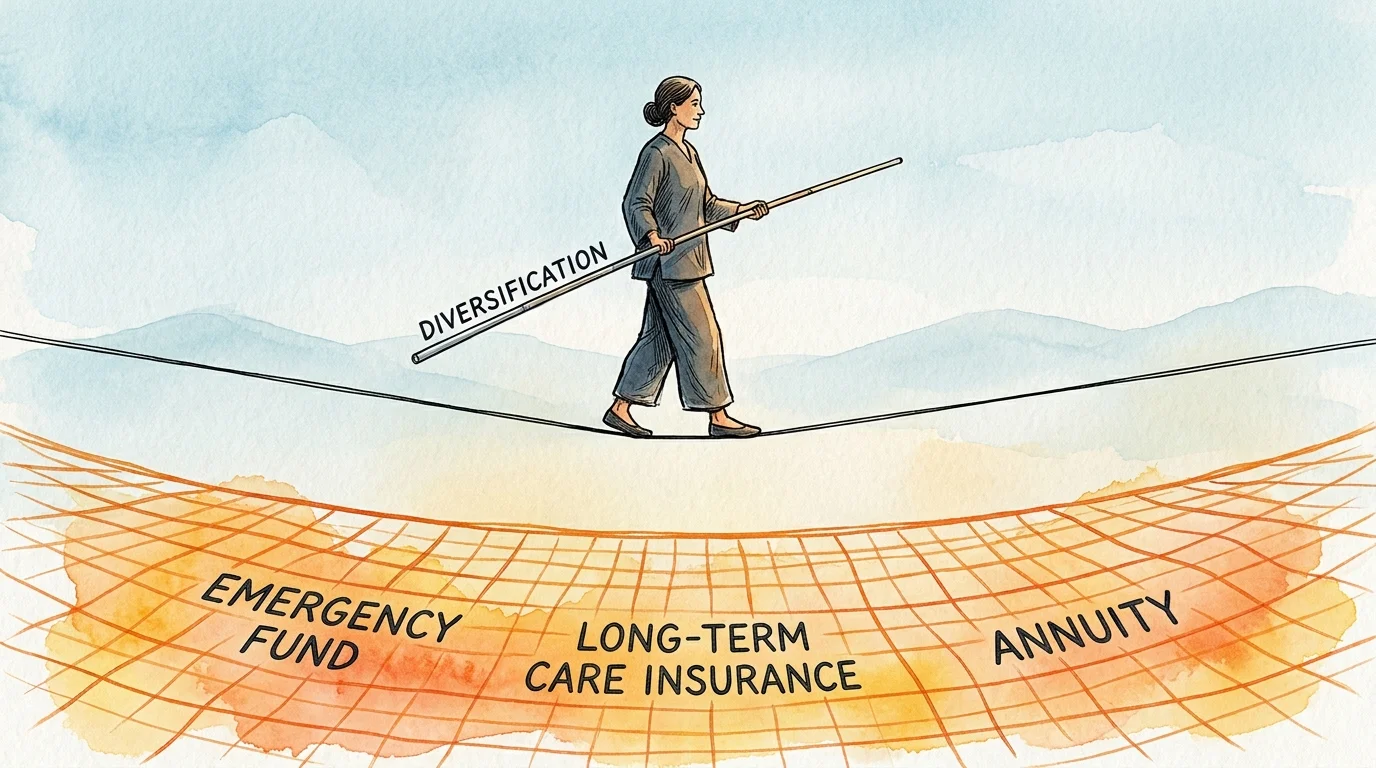

Experts also stress the importance of understanding sequence of returns risk. With smaller average balances, withdrawing money during a market downturn disproportionately damages a woman’s portfolio. Building a cash buffer equal to two years of living expenses provides a shock absorber, allowing your core investments to recover without locking in losses during a bear market.

Risks and Safeguards: Navigating the Hazards

Protecting your wealth requires vigilance against emerging threats. Older women living alone frequently become the primary targets for sophisticated financial fraud, ranging from romance scams to tech support phishing schemes. Always verify the identity of anyone requesting money or personal information, and freeze your credit reports to prevent identity theft.

You must also monitor the Medicare Income-Related Monthly Adjustment Amount cliff. A sudden spike in your taxable income—perhaps from selling a home or taking a large IRA distribution—can trigger massive increases in your Medicare Part B and Part D premiums. Work with a tax professional to smooth your income and avoid tripping these costly penalty thresholds.

Frequently Asked Questions

Q: Can I claim Social Security based on my ex-spouse’s work record?

A: Yes. If your marriage lasted at least 10 years, you are currently unmarried, and you are age 62 or older, you can claim benefits on an ex-spouse’s record. This action does not impact the benefits your ex-spouse or their current spouse receives.

Q: How do I catch up if I started saving for retirement late in life?

A: Take full advantage of the IRS guidelines on catch-up contributions. Once you turn 50, the government allows you to contribute additional funds beyond the standard annual limits to your 401(k), IRA, and Health Savings Account.

Q: Should I purchase a long-term care insurance policy?

A: Your need for insurance depends on your total asset base. If you hold significant wealth, you might self-fund care. If you possess moderate savings, a traditional or hybrid long-term care policy protects your nest egg from being wiped out by a multi-year nursing home stay.

Q: What happens to our joint retirement strategy if my spouse passes away?

A: You generally inherit your spouse’s retirement accounts tax-free. However, your tax filing status changes to single the year following their death. Reviewing AARP retirement research on survivor benefits can help you navigate the transition without triggering unnecessary tax liabilities.

Your Next 48 Hours: Taking Action Today

Reading about these strategies represents the first step; taking concrete action secures your future. In the next 48 hours, log into your online Social Security portal and review your primary earnings record. Verify that your earnings history is perfectly accurate and note your projected benefit amounts at age 62, full retirement age, and age 70. This simple, free exercise gives you the baseline data you need to start engineering a retirement plan that fully respects your unique female journey.

One Response

lQmgQpmRVcXsbUdbdouSRsQA