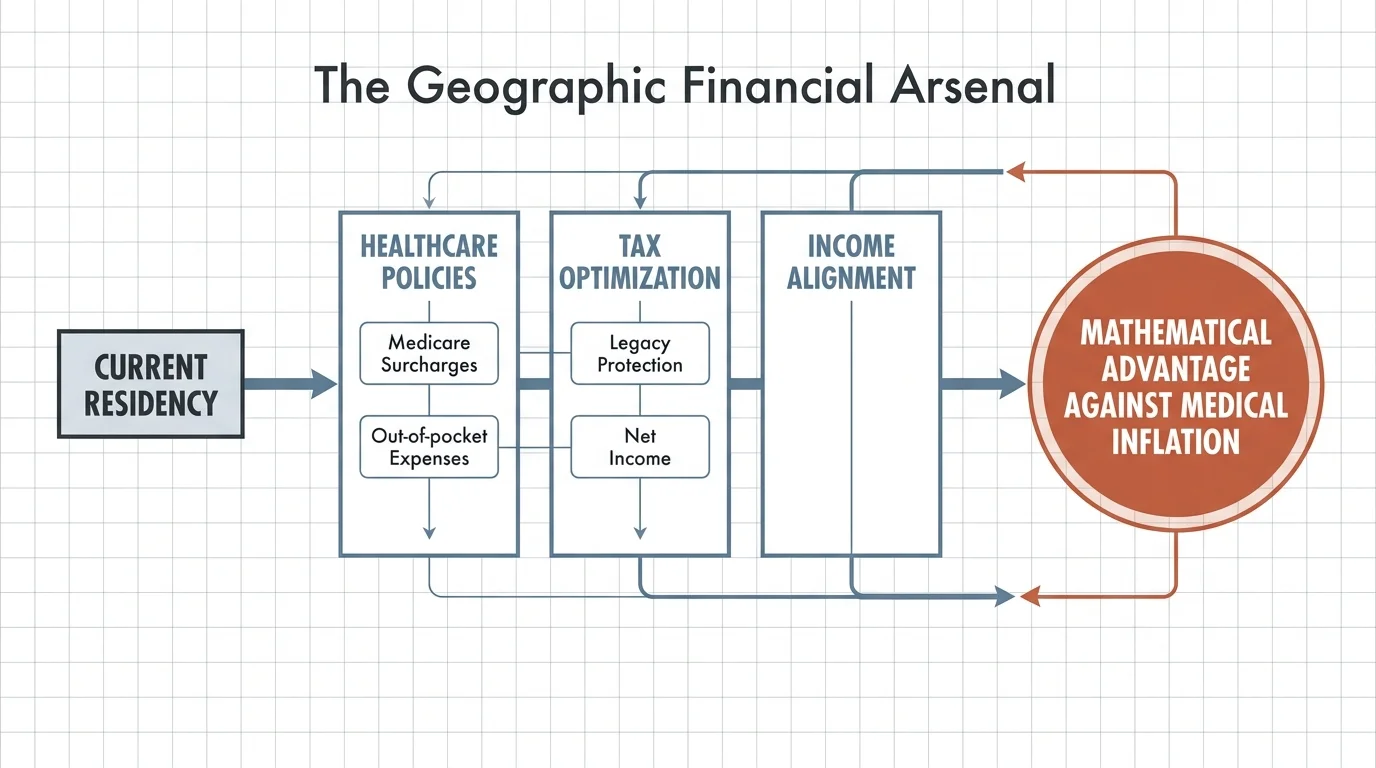

Relocating to a state with favorable healthcare policies can save you hundreds of thousands of dollars over a thirty-year retirement. Rising premiums, unpredictable out-of-pocket expenses, and Medicare surcharges routinely derail even the most carefully constructed financial plans. By understanding how specific states structurally reduce these burdens, you can preserve your investment portfolio and secure a higher standard of living. Evaluating geographic cost differences gives you a profound mathematical advantage against medical inflation. We will explore the leading jurisdictions for medical affordability alongside comprehensive income alignment, tax optimization, and legacy protection strategies. Your location heavily influences your net income, making strategic residency a powerful tool in your financial arsenal.

How Your Location Drives Healthcare and Tax Strategy

Hawaii

Exceptional life expectancy and strict employer mandates create a remarkably healthy risk pool, directly driving down retiree insurance premiums. While housing remains expensive, actual out-of-pocket medical spending is consistently among the nation’s lowest. Seniors prioritizing preventative care find that Hawaii’s systemic efficiencies offset the broader living costs, preserving capital.

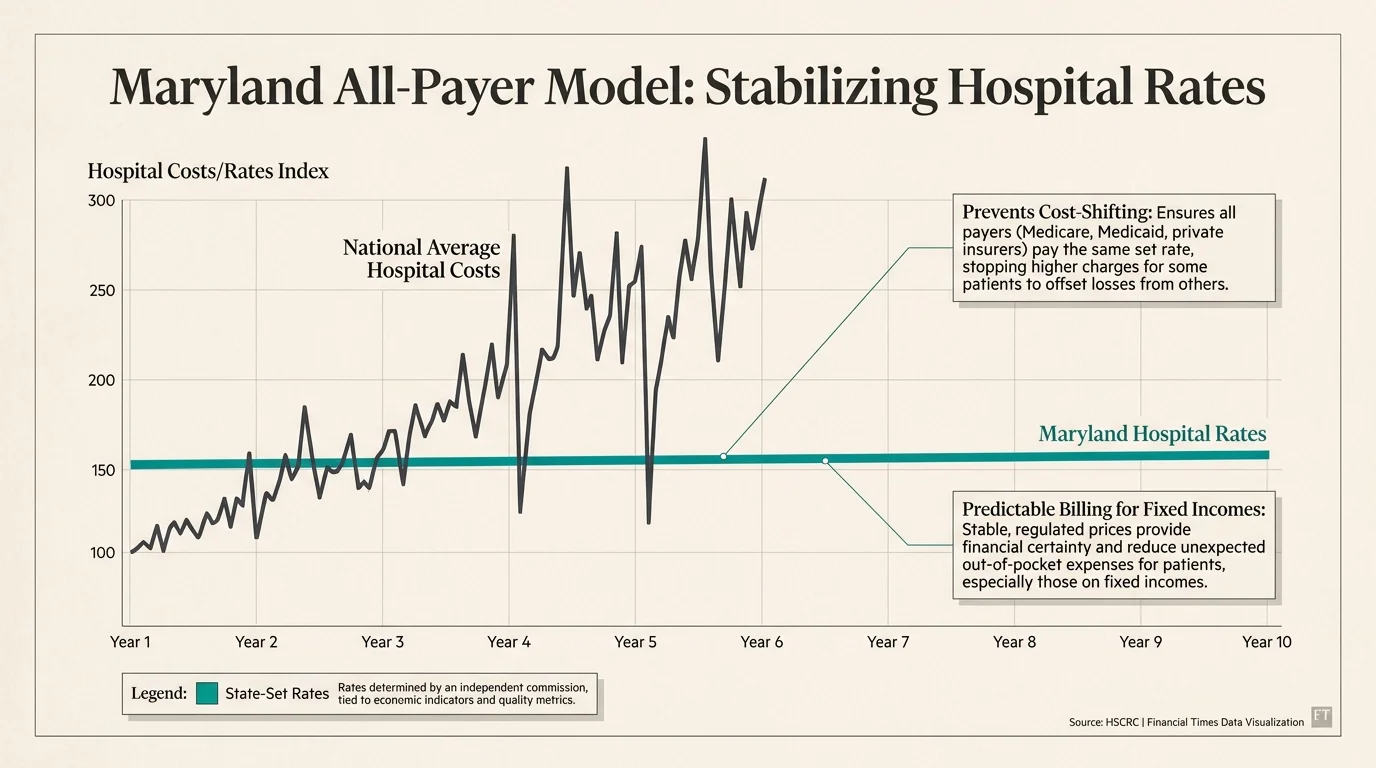

Maryland

Maryland operates a highly unique all-payer model where the state strictly sets hospital rates. This prevents chaotic cost-shifting, dramatically stabilizing healthcare costs for seniors on fixed incomes. You benefit from highly predictable billing and consistent medical inflation rates, allowing you to map out your long-term plan with certainty.

Colorado

Known for an active aging population, Colorado boasts incredibly low obesity and chronic disease rates. This systemic health translates into highly competitive Medicare Advantage and Medigap markets, driving premiums down as insurers vie for healthy policyholders. Retirees relocating here capture significant monthly savings while gaining access to world-class rehabilitative facilities.

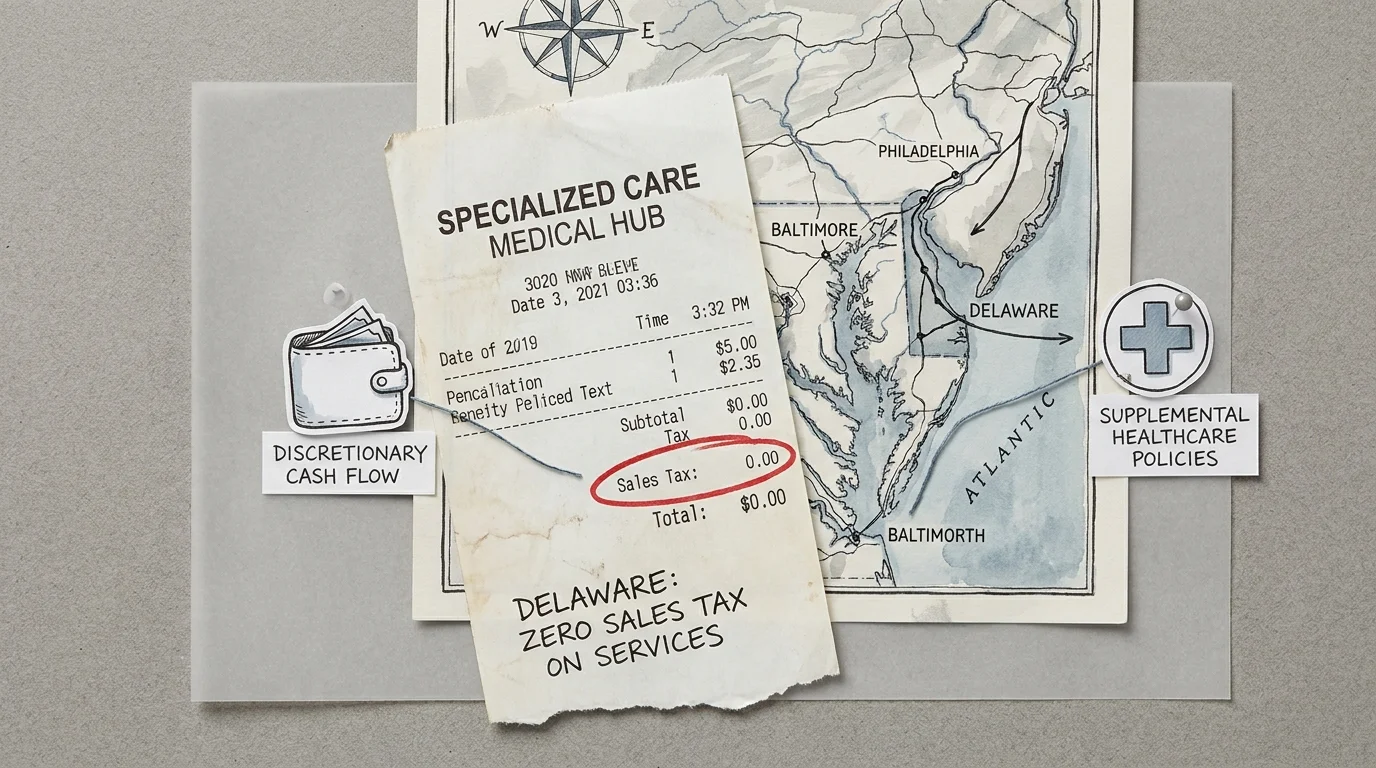

Delaware

Delaware seamlessly combines a complete absence of state sales tax with highly favorable tax treatment for retirement income. Seniors migrating here find these savings free up discretionary cash flow to cover premium supplemental healthcare policies. You effortlessly access elite specialized care in neighboring medical hubs without suffering prohibitive property taxes.

Washington

Washington features no state income tax alongside a remarkably robust regulatory framework overseeing health insurance. Retirees enjoy strong consumer protections against surprise billing and competitive rates for supplemental Medicare plans. The annual income tax savings can easily fund comprehensive long-term care policies or maximize Health Savings Account contributions.

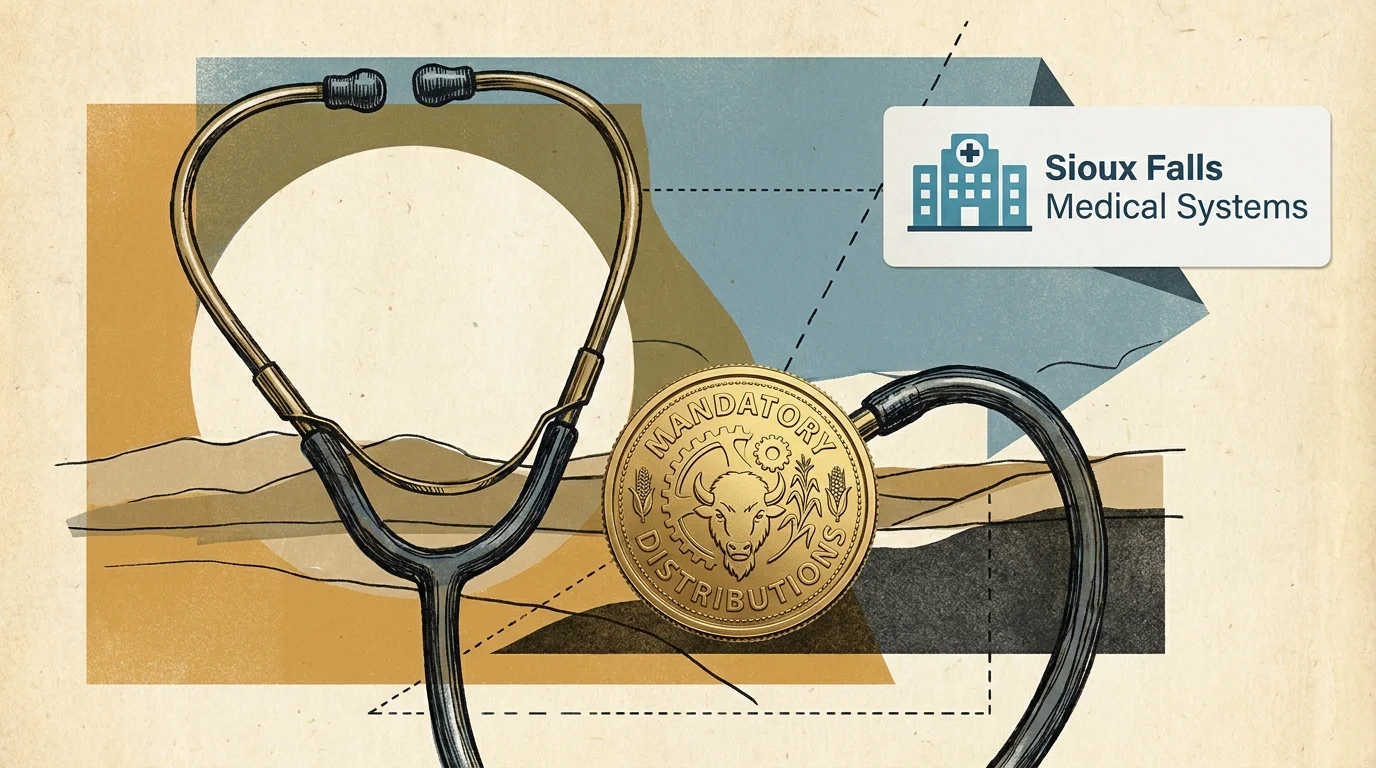

South Dakota

South Dakota offers a wealth-preserving combination of zero state income tax and efficient regional medical systems concentrated around Sioux Falls. The state fosters an economic environment where seniors retain a larger portion of mandatory distributions. You directly leverage these savings to offset localized costs for specialized procedures or prescription drugs.

Nevada

Nevada heavily regulates localized insurance markets to protect seniors while simultaneously offering the financial benefit of zero state income tax. Retirees often leverage the expanding medical infrastructure and competitive Medicare Supplement plans. By establishing residency, you lock in affordable fixed-cost healthcare alongside substantial annual tax savings, reducing mandatory monthly overhead.

South Carolina

South Carolina entirely exempts Social Security benefits from state taxation and offers generous deductions for other traditional retirement income. These targeted advantages allow you to actively redirect portfolio withdrawals toward dedicated health savings. You maximize true purchasing power in a state featuring structurally lower-than-average provider costs and high medical stability.

Income Alignment and Structuring Your Withdrawals

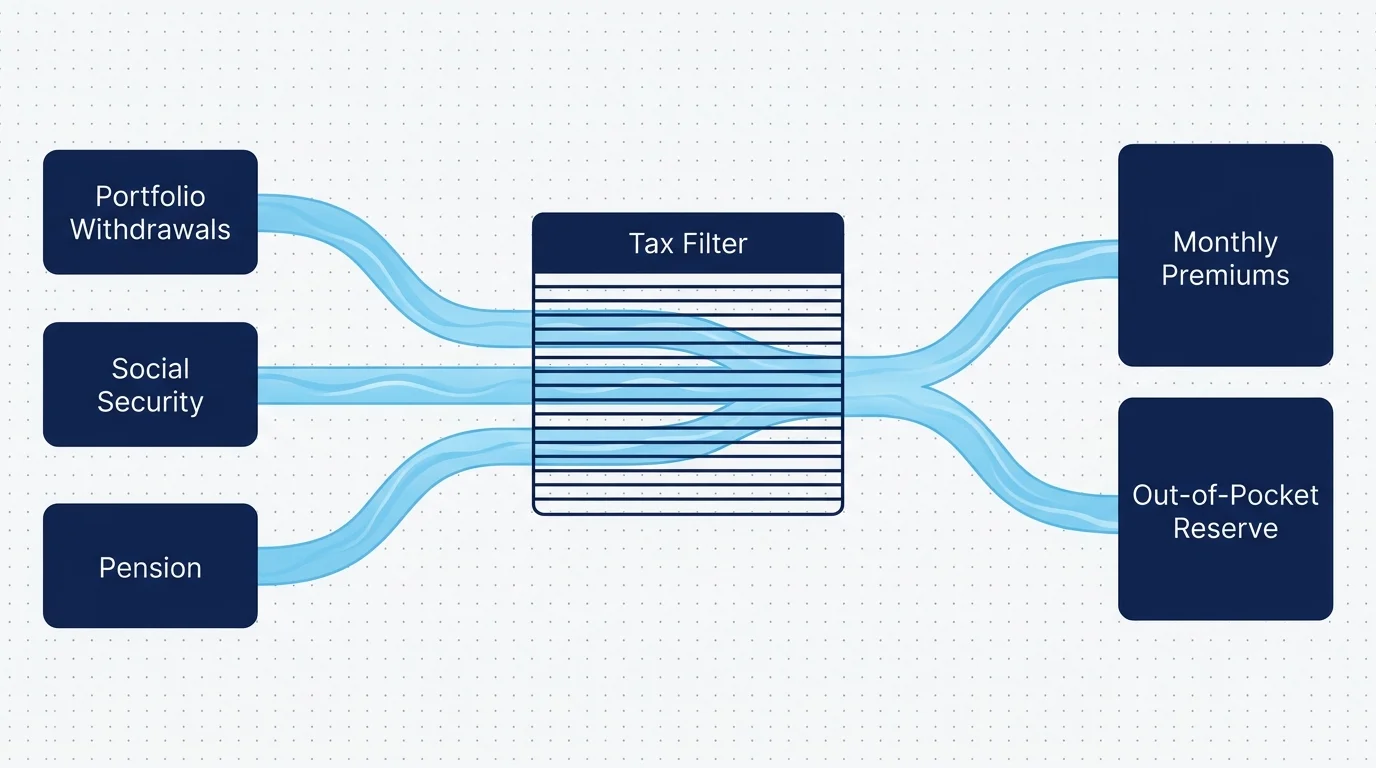

Structuring your income effectively requires significantly more than simply taking distributions from your accounts when you need cash. Your strategy must carefully sequence Social Security, pension payouts, and portfolio withdrawals to protect your principal against market volatility. Delaying Social Security until age seventy remains one of the most mathematically sound decisions you can make, as your baseline benefit increases by an exceptional eight percent annually from your full retirement age. You can utilize benefit calculators provided by the Social Security Administration to determine your optimal claiming strategy. This guaranteed income stream permanently offsets escalating clinical costs.

Pensions and fixed annuities add another powerful layer of certainty to your monthly cash flow. If you hold a traditional pension, selecting the optimal payout option requires meticulously analyzing your personal life expectancy alongside your spouse’s projected healthcare needs. Fiduciary professionals consistently recommend establishing an absolute income floor that securely covers your essential living expenses, strictly including baseline medical costs. You should view these guaranteed income sources as the unshakable bedrock of your financial stability.

Once your essential expenses are covered, you must approach your investment portfolio to generate reliable supplemental cash flow. Relying on an outdated rule of thumb for withdrawals can severely expose your nest egg to sequence of returns risk, especially if a market downturn coincides with a major medical event. Implementing a dynamic withdrawal strategy allows you to intelligently adjust distributions based on real-time portfolio performance. By taking less during down years, you give your equities essential time to recover.

Tax and Healthcare Strategy

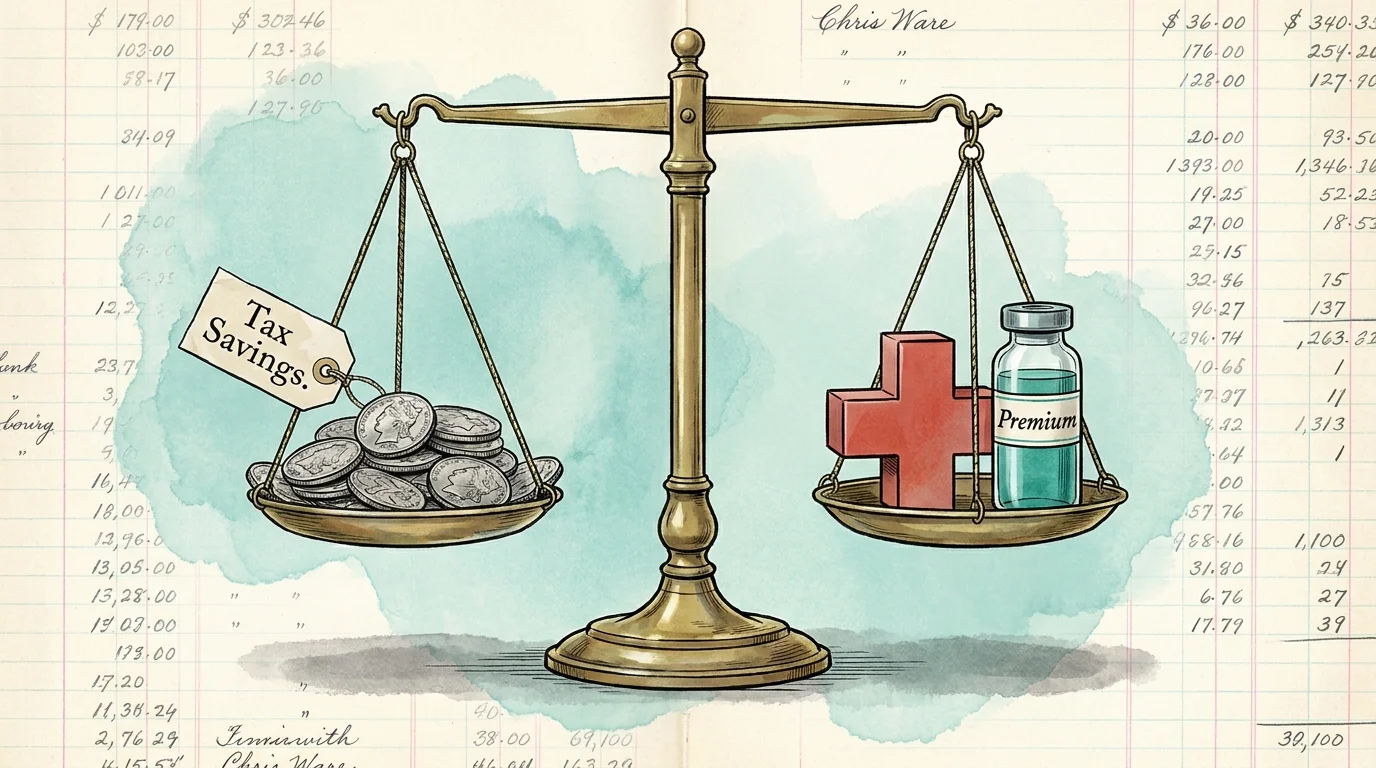

Your overall healthcare costs and baseline tax liabilities are intrinsically linked, meaning a tactical misstep in one area inevitably inflates the other. Required Minimum Distributions from your traditional tax-deferred retirement accounts begin at age seventy-three, legally forcing you to recognize taxable income regardless of your actual cash needs. These mandatory distributions can easily push you into a significantly higher tax bracket and inadvertently trigger Medicare Income-Related Monthly Adjustment Amounts. You can review the specific income brackets and surcharges on the official Medicare website to better anticipate these added expenses.

To systematically mitigate this cascading financial effect, you should rigorously evaluate strategic Roth conversions early in your retirement. By deliberately converting pre-tax assets to Roth accounts before reaching mandatory distribution age, you voluntarily pay taxes at your current known rate. Future withdrawals from these designated Roth accounts remain entirely tax-free and do not factor into the modified adjusted gross income calculations that determine future Medicare premiums. This proactive maneuver firmly stands as a premier strategy for insulating accumulated wealth from stealth healthcare taxes.

If you are still working or have not yet formally enrolled in Medicare, fully funding a Health Savings Account offers unparalleled financial leverage. These specialized accounts represent the only triple-tax-advantaged vehicle in the federal tax code; your initial contributions are tax-deductible, your invested funds grow tax-free, and your withdrawals remain entirely tax-free when utilized for qualified medical expenses. You can learn more about contribution limits directly through official Internal Revenue Service publications. Letting your investments compound uninterrupted creates a dedicated tax-free war chest.

Protection and Legacy Planning

Protecting your wealth from catastrophic health events and malicious bad actors represents a fundamental component of any resilient retirement strategy. Long-term care costs continue to soar at alarming rates, and traditional Medicare explicitly does not cover custodial care or extended nursing home stays. Relying solely on your primary investment portfolio to self-fund these massive potential liabilities is a high-risk financial gamble. You should actively explore hybrid life insurance policies or linked-benefit annuities that provide dedicated long-term care multipliers, guaranteeing a tax-free death benefit if you remain healthy.

Elder financial exploitation maliciously drains billions of dollars from dedicated retirement accounts every single year. Global fraudsters target older adults possessing significant liquid assets, utilizing sophisticated technological tactics to bypass traditional banking security measures. You must establish extremely strict personal safeguards, such as permanently enabling multi-factor authentication on all financial accounts. Reviewing resources provided by the Securities and Exchange Commission can equip you with the essential knowledge needed to rapidly identify and thwart emerging investment scams before they compromise your savings.

A comprehensive, legally sound estate plan acts as the ultimate protective barrier for your accumulated wealth and personal healthcare directives. You urgently need more than just a standard will; durable powers of attorney for both complex healthcare and financial decisions legally allow someone you implicitly trust to make choices if you become incapacitated. Without these specific directives in place, your family may face expensive court guardianship proceedings. Additionally, you must systematically review your primary and contingent beneficiary designations across all retirement accounts.

Frequently Asked Questions

How does working part-time during retirement impact my healthcare and income?

Earning wages while actively collecting Social Security before reaching your full retirement age subjects you directly to the federal earnings test, which temporarily withholds a specific portion of your benefits. From a strategic healthcare perspective, engaging in part-time work can be incredibly beneficial if it successfully provides access to employer-sponsored health insurance. This coverage allows you to safely delay your initial Medicare enrollment and continue funding a Health Savings Account. However, unexpected part-time earnings can easily push you into higher tax brackets and trigger permanent Medicare surcharges.

What are the most reliable methods for hedging against medical inflation?

General medical inflation historically outpaces the standard consumer price index, demanding highly targeted growth within your retirement portfolio. Maintaining a robust, properly diversified allocation to global equities remains one of the absolute best defenses against long-term purchasing power erosion. Additionally, integrating Treasury Inflation-Protected Securities and healthcare-specific exchange-traded funds can provide reliable growth tied to broader economic price increases. You should consistently balance your immediate need for short-term capital preservation with the mathematical necessity of long-term capital appreciation.

How do I navigate the different fee structures charged by financial advisors?

Thoroughly understanding exactly how your chosen advisor is compensated remains deeply critical to preserving your long-term returns. Fiduciary, fee-only financial advisors charge a highly transparent rate and are legally obligated to place your financial interests firmly above their own. Conversely, commission-based brokers may secretly earn hidden payouts for actively selling you specific insurance products, introducing severe structural conflicts of interest. You should always demand a written fee disclosure and verify credentials through the Financial Industry Regulatory Authority before entrusting them with your strategy.

What financial steps must a surviving spouse take immediately following a loss?

The sudden death of a spouse drastically alters the surviving partner’s entire financial landscape, requiring immediate and highly strategic adjustments. The newly consolidated household will permanently lose the smaller of the two monthly Social Security checks, directly reducing guaranteed monthly baseline income. Furthermore, the surviving spouse will be forced to file future taxes as a single filer, frequently resulting in higher taxes on the exact same gross income. A proactive survival plan involves adjusting withdrawal strategies, reassessing tax withholdings, and rapidly updating estate documents to reflect reality.

Your Next Steps

Navigating the complex intersection of rising healthcare costs, unpredictable taxation, and sustainable retirement income requires sustained attention and proactive adjustments. Relocating to a significantly more favorable tax state is simply one critical piece of a much larger puzzle designed to fiercely protect your purchasing power. You hold the ultimate power to reshape your long-term financial trajectory by strategically optimizing your withdrawal sequencing and ruthlessly leveraging tax-advantaged accounts. Take the necessary time this week to thoroughly review your investment statements, evaluate your medical coverage, and accurately calculate your projected tax liabilities.