Understanding why retirees postpone major financial moves gives you the clarity to secure your nest egg and avoid costly mistakes. You gain a massive advantage when you know which choices your peers put on hold amid fluctuating interest rates and shifting federal policies in 2026. Data reveals that over half of older adults deliberately paused at least one significant monetary transition this year. By examining these delayed choices, you can proactively spot hidden opportunities to stretch your fixed income further. We explore the eight pivotal decisions people avoid today, offering you the actionable foresight necessary to protect your lifestyle, maximize your government benefits, and confidently preserve your long-term wealth.

Current Economic Landscape Shaping Your Retirement

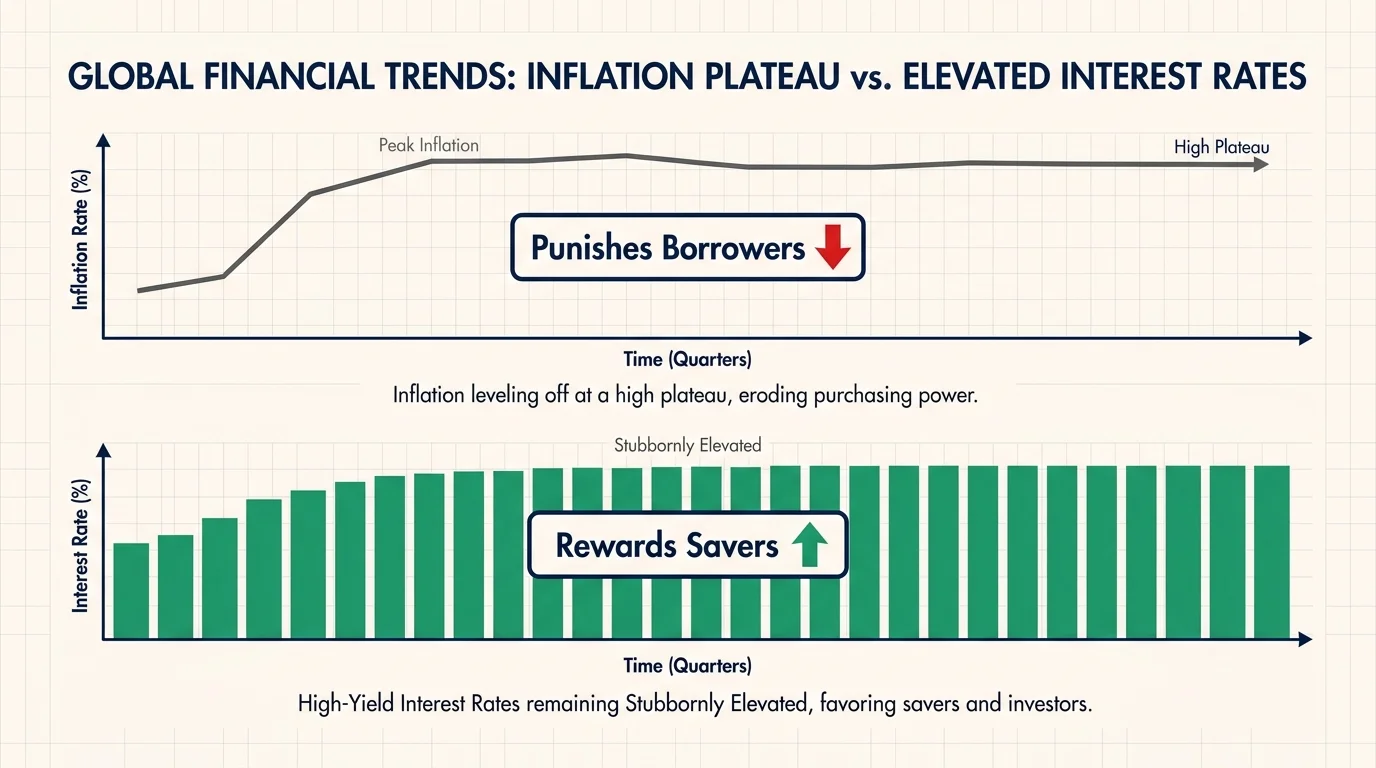

The financial terrain in 2026 demands a highly strategic approach to your savings and fixed income. While the aggressive inflation spikes of the early decade finally leveled out, the cumulative impact of those past price increases permanently elevated your baseline cost of living. Your grocery bills, utility statements, and property taxes consume a noticeably larger percentage of your monthly budget than they did five years ago. Furthermore, federal interest rates remain stubbornly elevated compared to historical averages; this unique environment punishes borrowers but heavily rewards conservative savers holding cash in high-yield vehicles. These conflicting economic signals create a profound sense of psychological paralysis for those approaching their transition out of the workforce. You watch the stock market experience rapid cyclical rotations, making you deeply hesitant to lock in permanent decisions regarding your withdrawal rates or your housing situation. Recognizing how this macroeconomic pressure influences your personal hesitation represents the first critical step toward regaining absolute control over your financial destiny.

Decision 1: Relocating Or Downsizing Your Home

Many pre-retirees originally planned to sell large family homes and purchase smaller, more manageable properties upon leaving the workforce. Today, you likely delay this downsizing transition because of the powerful mortgage rate lock-in effect. Millions of older adults currently hold long-term mortgages with interest rates securely below four percent. The prospect of surrendering that incredibly cheap debt only to take on a new mortgage at current market rates completely ruins the financial logic of downsizing. Even if you desire a smaller footprint to reduce your property maintenance chores, the math simply fails to justify a sudden move. Instead of relocating to a new zip code, you can redirect a portion of your home equity toward modifying your current residence to successfully support aging in place. Adding strategic accessibility features like zero-threshold showers, widening ground-floor doorways, and relocating the primary bedroom to the main level offer immediate lifestyle improvements without requiring a new loan. The AARP provides extensive resources on retrofitting existing homes to safely accommodate varying mobility levels while preserving your valuable real estate investment.

Decision 2: Claiming Social Security Benefits

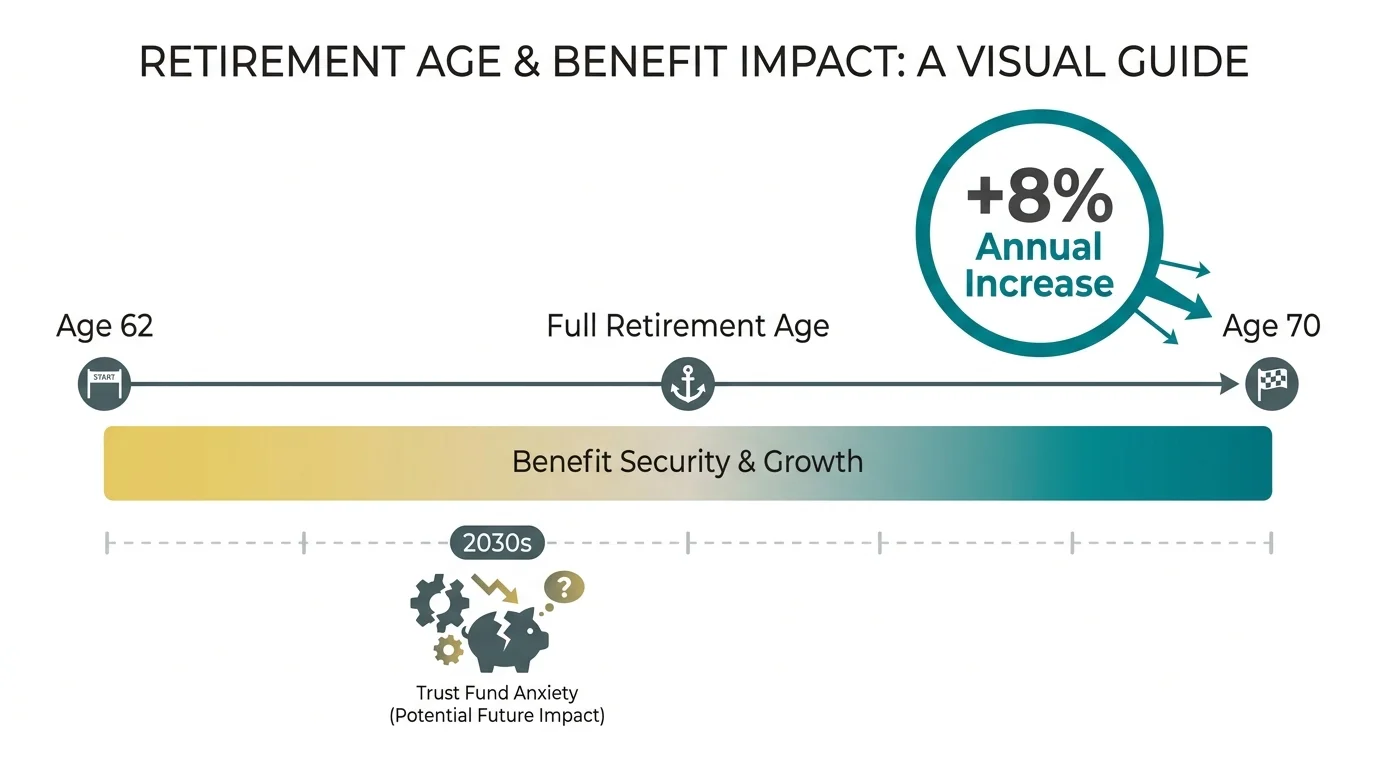

Deciding exactly when to initiate your monthly government benefits ranks among the most stressful choices you face. You secure a permanent, guaranteed eight percent annual increase to your payments by waiting from your full retirement age until age seventy. However, persistent and alarming headlines regarding the projected depletion of the Social Security trust fund by the mid-2030s cause immense anxiety for fixed-income households. You likely delay making a firm claiming plan because you constantly second-guess the system’s long-term legislative longevity. Certified Financial Planner professionals routinely emphasize that Congress possesses multiple powerful legislative levers to shore up the program before any broad benefit cuts occur. Rather than acting impulsively based on political fear, you must base your timeline strictly on your personal health metrics, your spousal survivor benefits, and your available liquid assets. You can instantly review your most accurate, up-to-date benefit estimates and stress-test various claiming ages directly through the secure Social Security Administration portal.

Decision 3: Adjusting Portfolio Withdrawal Rates

You likely spent your career hearing financial pundits preach the absolute safety of the rigid four percent rule for portfolio withdrawals. Today, unpredictable market volatility and sustained underlying inflation make that static guideline feel incredibly precarious. You delay officially formalizing your drawdown strategy because you harbor a deep-seated fear of depleting your investment capital prematurely. Rather than guessing your safe withdrawal amount each January, you should actively transition toward a dynamic withdrawal framework. A dynamic approach allows you to withdraw slightly more discretionary cash during robust market years and strategically tighten your belt when equities experience a sharp cyclical dip. Data published by the Bureau of Labor Statistics reveals that retiree household spending typically peaks in the early, active retirement years before gradually declining as travel slows down. Planning for these highly variable spending phases ensures you do not hoard your cash unnecessarily when you could be fully enjoying the freedom of your early retirement years.

Decision 4: Transitioning Medicare Coverage Options

Choosing between traditional Medicare paired with a supplemental Medigap policy and an all-in-one Medicare Advantage plan feels incredibly overwhelming. You delay evaluating your health coverage options each fall because the sheer volume of glossy marketing materials and complex coverage grids creates severe decision paralysis. Consequently, many older adults simply allow their existing healthcare plans to auto-renew blindly, frequently missing out on potentially thousands of dollars in premium savings. Your personal medical needs evolve rapidly; a budget-friendly plan that served you perfectly at age sixty-five might leave you completely exposed to devastating out-of-pocket costs following a new diagnosis at age seventy-two. You must take aggressive control of your predictable healthcare expenses by meticulously reviewing your regular prescription drug usage and your anticipated specialist visits annually. You can directly compare strict out-of-pocket maximums and local provider networks using the official Medicare online plan finder to guarantee your medical coverage perfectly aligns with your current physical condition and your fixed budget.

Decision 5: Securing Long-Term Care Coverage

Absolutely no one enjoys contemplating a future scenario where they might require daily physical assistance with basic living activities like bathing or dressing. You delay investigating long-term care coverage because traditional standalone insurance premium costs skyrocketed drastically over the last decade, and the strict medical underwriting process feels highly intrusive. Ignoring this statistical risk entirely leaves your carefully constructed retirement savings highly vulnerable to a sudden, catastrophic health event. Gerontologists routinely warn that relying solely on your adult children for unpaid caregiving severely strains family relationships and heavily impacts your heirs’ own financial trajectory. Rather than purchasing an expensive traditional policy that you might never use, you can proactively explore hybrid life insurance products featuring robust long-term care riders. These modern financial instruments provide a dedicated, tax-free pool of money for assisted living facilities or in-home health aides if you require support, while still offering a substantial death benefit payout to your beneficiaries if you ultimately remain healthy.

Decision 6: Finalizing Estate Plans And Beneficiary Designations

Comprehensive estate planning rarely serves as an enjoyable topic of conversation during family gatherings. You delay updating your final wills, living trusts, and durable power of attorney documents because the required legal jargon feels frustratingly dense and the underlying subject matter feels deeply morbid. However, 2026 marks a profoundly critical turning point for generational wealth transfer in the United States. The formal expiration of key tax provisions within the Tax Cuts and Jobs Act means federal estate tax exemption thresholds drop by roughly half this year. Failing to formally update your legal documents right now exposes your heirs to completely avoidable, massive tax liabilities. Furthermore, outdated beneficiary designations on your individual retirement accounts legally trump whatever instructions you carefully outlined in your last will and testament. You should dedicate a quiet afternoon this week to reviewing your formally designated beneficiaries across all bank and brokerage accounts. Consult a qualified estate attorney to verify your documents fully comply with the latest Internal Revenue Service regulations and accurately reflect your current legacy wishes.

Decision 7: Gifting Assets To Adult Children

You deeply want to help your adult children successfully navigate an increasingly expensive national housing market or comfortably fund your young grandchildren’s college education accounts. Yet, you delay transferring any substantial financial gifts because you constantly worry about running out of money during your own later years. This completely understandable hesitation perfectly illustrates the emotional tension between your strong desire to leave a meaningful legacy and your biological need for fundamental self-preservation. Certified financial planners strongly suggest running a comprehensive stress test on your retirement portfolio before you write a large check to your family members. You must definitively ensure your core lifestyle expenses and your maximum potential medical liabilities remain fully funded up to age ninety-five. Once you mathematically verify your own baseline financial security, you can confidently utilize the current annual gift tax exclusions to transfer your wealth efficiently. Gifting your assets strategically allows you to witness the profound, positive impact of your generosity while you are still alive to enjoy the moment.

Decision 8: Committing To A Phased Retirement Schedule

The traditional cultural concept of executing a hard, sudden stop to your decades-long career on a random Friday afternoon no longer dominates the modern workforce. You delay giving your formal notice to your employer because you legitimately fear the sudden loss of your professional identity and the abrupt disappearance of your daily intellectual structure. Instead of facing a drastic psychological transition, many seasoned professionals now successfully negotiate customized phased retirement arrangements. You can gradually reduce your weekly hours over a manageable two-year period, retaining a proportional percentage of your salary while simultaneously maintaining crucial social connections with your longtime colleagues. This gradual, intentional glide path into full retirement effectively protects your mental health and prevents you from immediately tapping into your fragile investment portfolios during volatile market conditions. You should proactively approach your human resources department to discuss flexible consulting roles or structured part-time schedules that empower you to step back gracefully without walking away entirely.

Navigating Risks And Protecting Your Nest Egg

Delaying complex financial decisions occasionally serves as a highly prudent strategy when global markets experience severe, unpredictable turbulence. However, chronic procrastination introduces significant structural vulnerabilities into your long-term wealth preservation plan. Opportunistic fraudsters specifically target older adults who appear uncertain or disconnected from their daily financial management. When you fail to consolidate your scattered legacy retirement accounts or neglect to monitor your consumer credit actively, you leave the back door wide open for devastating identity theft and highly sophisticated phishing scams. Furthermore, ignoring the intricate, strict rules surrounding required minimum distributions from your tax-advantaged accounts automatically triggers massive, unforgiving federal tax penalties. You must actively build a proactive defense system around your savings. Set recurring calendar reminders for critical age-based enrollment milestones, review your primary bank statements weekly for anomalous charges, and never hesitate to freeze your credit files at the major bureaus if you suspect any suspicious activity. Taking decisive, preventative action firmly insulates your hard-earned wealth from emerging external threats.

Frequently Asked Questions

How does sustained inflation affect my decision to delay Social Security?

Sustained inflation dramatically increases your baseline daily living expenses, making the guaranteed cost of living adjustments provided by Social Security incredibly valuable. When you delay claiming your benefits until age seventy, you not only increase your base payout by eight percent annually, but you also ensure that future inflation adjustments compound on a significantly larger foundational number. If you possess enough liquid savings to bridge the income gap without selling depressed equities, delaying your claim serves as one of the most effective inflation hedges available to modern retirees.

Should I downsize my primary home if my current mortgage rate is extremely low?

You must weigh the ongoing physical maintenance costs and the associated property taxes of your current home against the harsh reality of acquiring a new mortgage at current market rates. If your existing mortgage sits below four percent, purchasing a smaller property often results in a higher monthly payment. However, if you can sell your large home, capture substantial tax-free equity, and purchase your new, smaller property entirely in cash, downsizing remains a highly viable strategy to reduce your overall lifestyle expenses.

What is the most common financial mistake new retirees make in 2026?

The most common error involves maintaining an overly conservative investment portfolio out of sheer panic. Many new retirees hastily shift all their assets into cash or low-yield bonds the moment they stop working. Because modern retirements frequently last three decades, completely abandoning growth-oriented equities ensures your purchasing power will inevitably succumb to long-term inflation. You must maintain a balanced, diversified allocation that actively generates both immediate income and necessary long-term capital appreciation.

Are hybrid long-term care policies worth the investment for a fixed budget?

Hybrid policies offer immense peace of mind because they eliminate the strict use-it-or-lose-it risk associated with traditional long-term care insurance. While the upfront premiums or required lump-sum funding can seem intimidating on a strictly fixed income, these vehicles protect your broader portfolio from total liquidation in the event of a severe health crisis. If you lack the substantial excess capital required to self-insure against a multi-year stay in an assisted living facility, a hybrid policy represents a highly strategic defensive investment for your estate.

Your Next Step

Achieving total confidence in your retirement requires you to stop procrastinating and start executing. You do not need to tackle all eight of these complex transitions simultaneously to dramatically improve your financial security. Momentum builds rapidly through small, deliberate actions. Over the next forty-eight hours, choose exactly one delayed decision from this list and take the first concrete step toward resolving it. Whether you log into the government portal to verify your benefit estimates, schedule a brief consultation with a certified fiduciary planner, or finally review your primary account beneficiaries, your proactive effort immediately reduces your underlying anxiety. Taking charge of your financial trajectory today empowers you to fully enjoy the rich, rewarding lifestyle you spent decades diligently building.