Securing a comfortable retirement today requires building multiple streams of reliable cash flow to protect against inflation and outliving your savings. You can achieve lasting financial freedom by integrating passive income and flexible side income into your overarching wealth strategy. Recent labor data reveals a massive surge in older adults extending their earning years on their own terms. Shifting away from total reliance on fixed pensions empowers you to fund travel, cover healthcare, and enjoy daily life without financial stress. Understanding the specific retirement income sources Americans are adopting right now provides a practical roadmap to enhance your security and design a lifestyle that truly reflects your values.

The 2026 Retirement Snapshot: Why Income Streams Are Shifting

The financial landscape for retirees looks entirely different today than it did a decade ago. While inflation rates have cooled, the lingering baseline costs of housing, groceries, and medical care remain elevated. Furthermore, legislative changes—most notably the ongoing rollout of SECURE 2.0 Act provisions—have fundamentally altered how and when you must withdraw from your retirement accounts. This combination of higher living expenses and shifting tax policies has prompted a massive reevaluation of traditional retirement planning. You can no longer rely solely on a standard portfolio withdrawal rate to cover your expenses comfortably.

Tracking by the Bureau of Labor Statistics highlights a clear trend; adults over sixty-five represent the fastest-growing segment of the active workforce. They are not returning to grueling corporate schedules. Instead, they curate a mix of autonomous side income and strategic passive income. Diversifying cash flow protects against economic downturns while providing financial flexibility to support family, pursue passions, and adapt to health shifts. By building an ecosystem of varied revenue streams, you effectively insulate your lifestyle from the unpredictability of traditional markets.

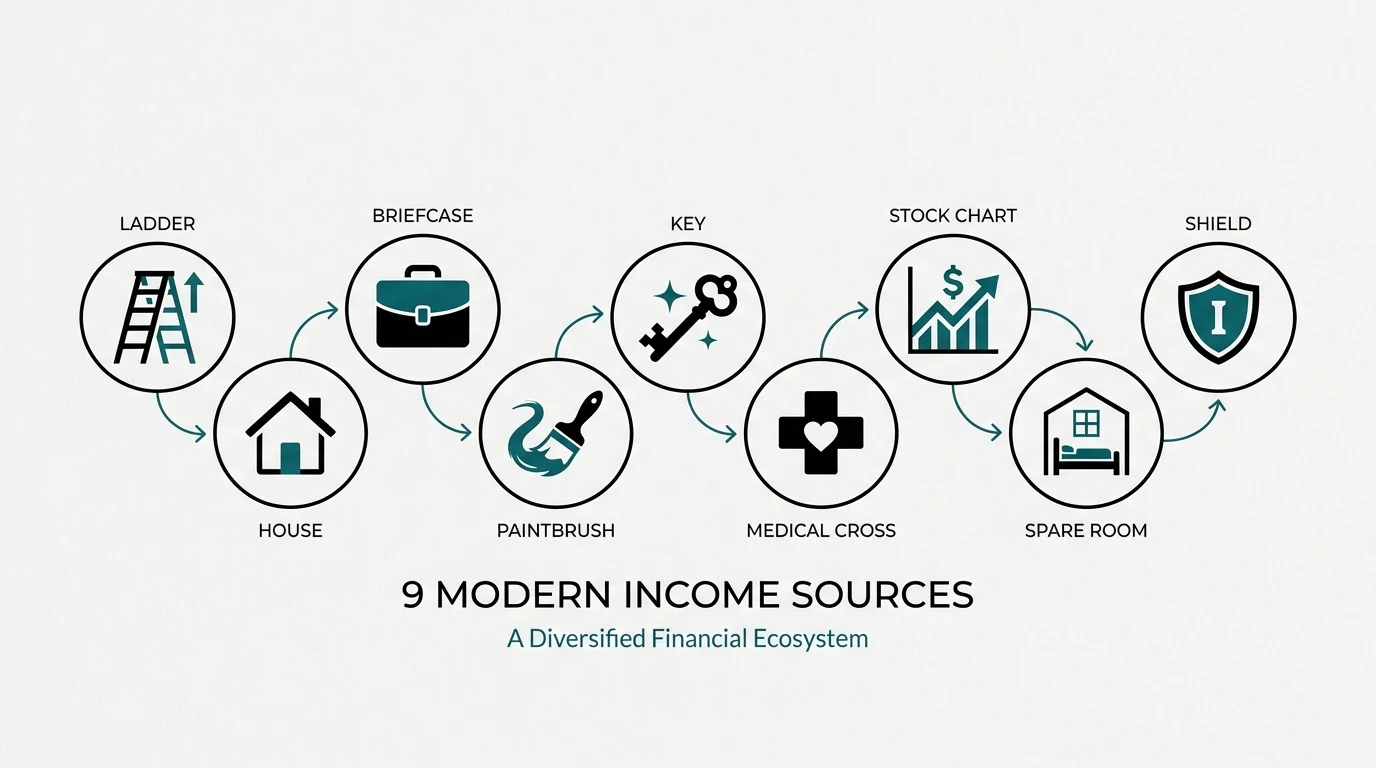

Strategy Pillar 1: Income Planning With 9 Modern Sources

Building a resilient retirement relies on stacking different types of income. Some sources provide guaranteed baseline security, while others offer growth potential to combat inflation. Consider incorporating several of the following nine income streams that retirees are actively adding to their financial plans this year.

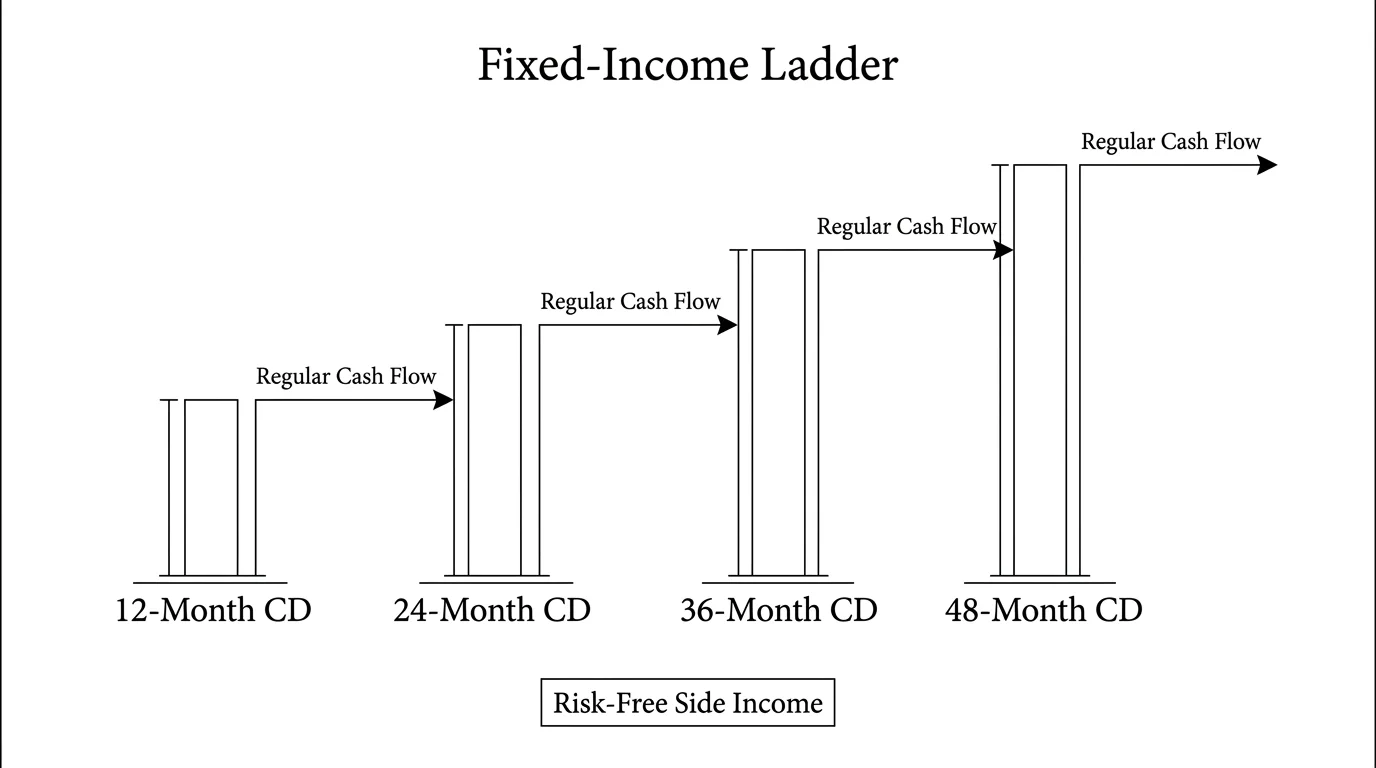

1. High-Yield Cash and Fixed-Income Ladders

With stabilized interest rates, cash equivalents finally generate meaningful returns. Many retirees capitalize on this by building CD ladders or utilizing high-yield savings accounts to secure risk-free side income. By staggering the maturity dates of certificates of deposit or Treasury bills, you ensure a portion of your money becomes available at regular intervals. This strategy allows you to cover immediate living expenses without being forced to sell your long-term equity investments during a market dip. It provides a reliable baseline of passive income while protecting your principal from market volatility.

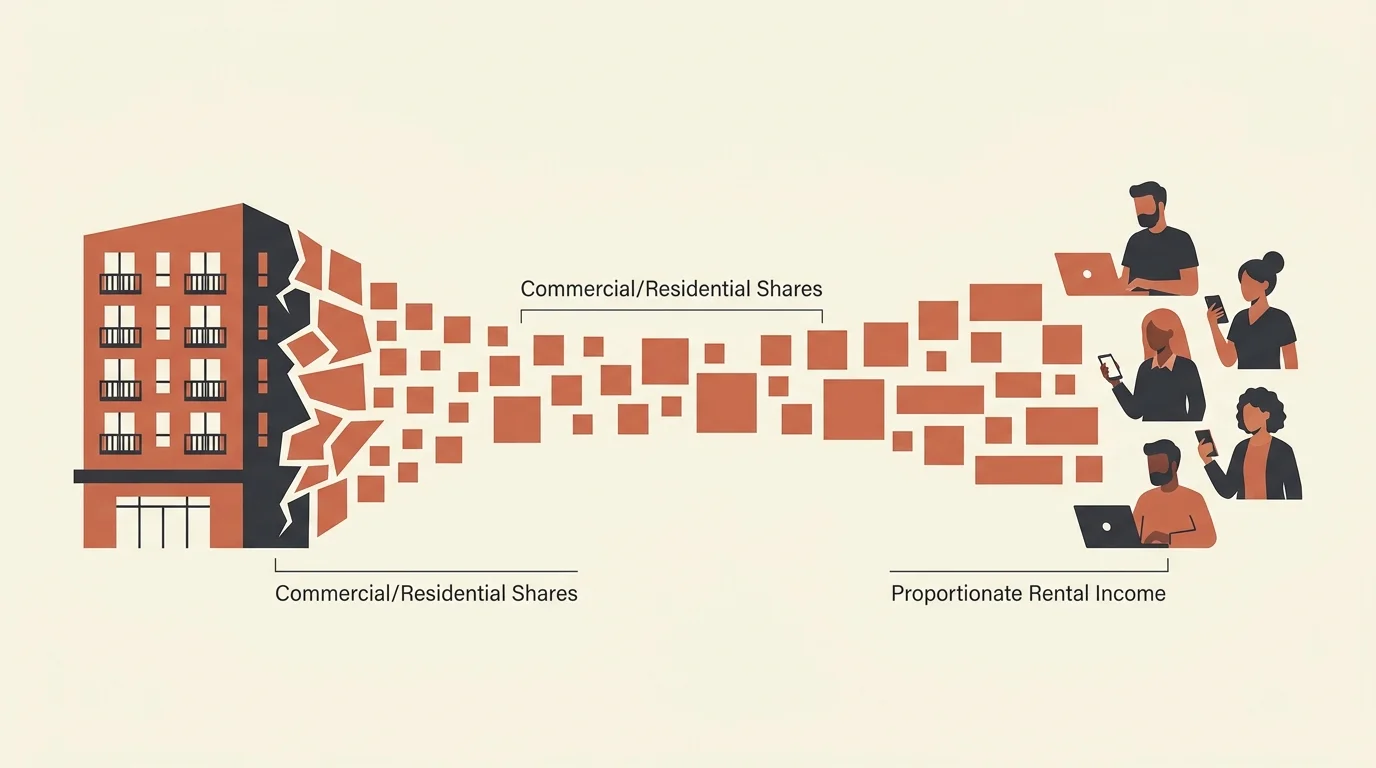

2. Fractional Real Estate Investing

Managing physical rental properties demands intense labor and constant maintenance, which may not align with your physical mobility. Fractional real estate investing solves this by allowing you to buy shares of commercial or residential properties through online platforms or real estate investment trusts. You receive a proportionate share of the rental income and potential appreciation without ever dealing with a broken pipe or a difficult tenant. This approach delivers the inflation-hedging benefits of real estate while maintaining complete passivity, making it an ideal passive income stream for a hands-off portfolio.

3. Part-Time Consulting and Freelance Gigs

Your decades of professional experience carry immense value. Transitioning into part-time consulting lets you monetize your expertise on your own schedule. Whether offering financial guidance, project management, or specialized insights, freelancing provides substantial side income while keeping your mind sharp. This type of work requires minimal physical exertion and accommodates varying levels of mobility through remote work setups. It also provides a vital sense of routine and professional identity, which many older adults struggle to replace after leaving their primary careers.

4. Monetizing Hobbies and Crafting

Retirement offers time to fully immerse yourself in passions previously relegated to the weekends. Turning those hobbies into a profitable venture is easier than ever through digital marketplaces and local community events. Woodworking, gardening, digital art, or baking seamlessly transition into micro-businesses that generate consistent cash. The beauty of this income source lies in its inherent flexibility; you dictate the volume of work based on your energy levels and interest. Monetizing a hobby transforms your leisure time into a financially rewarding endeavor that offsets material costs and funds lifestyle upgrades.

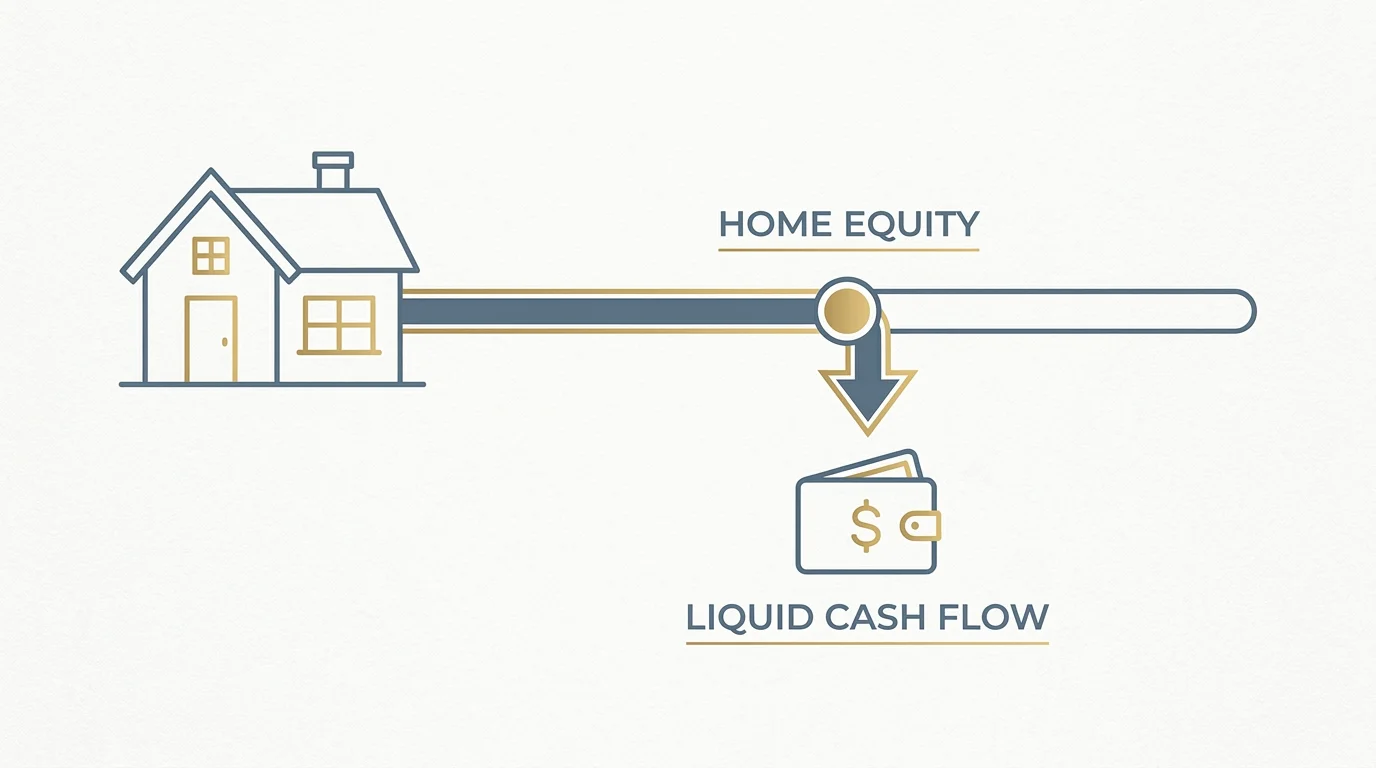

5. Reverse Mortgages and Home Equity

For many Americans, their primary residence represents their largest single asset. A reverse mortgage allows homeowners aged sixty-two and older to convert home equity into tax-free cash flow without selling the property or taking on monthly payments. While requiring careful consideration of upfront fees and inheritance implications, it serves as a powerful tool for those on fixed budgets. Tapping into home equity provides a lump sum for immediate medical needs, a line of credit for emergencies, or monthly disbursements that supplement your standard retirement income.

6. Health Savings Account (HSA) Distributions

If you contributed to a Health Savings Account, you possess a highly tax-efficient income vehicle. Once you reach age sixty-five, you can withdraw funds for non-medical expenses without facing the standard twenty percent penalty, though you will pay ordinary income tax on those distributions. However, if you use the funds for qualified medical expenses, the withdrawals remain entirely tax-free. Strategically utilizing your HSA to cover premiums, copays, or dental work effectively frees up your other retirement income for discretionary spending, maximizing your overall financial freedom.

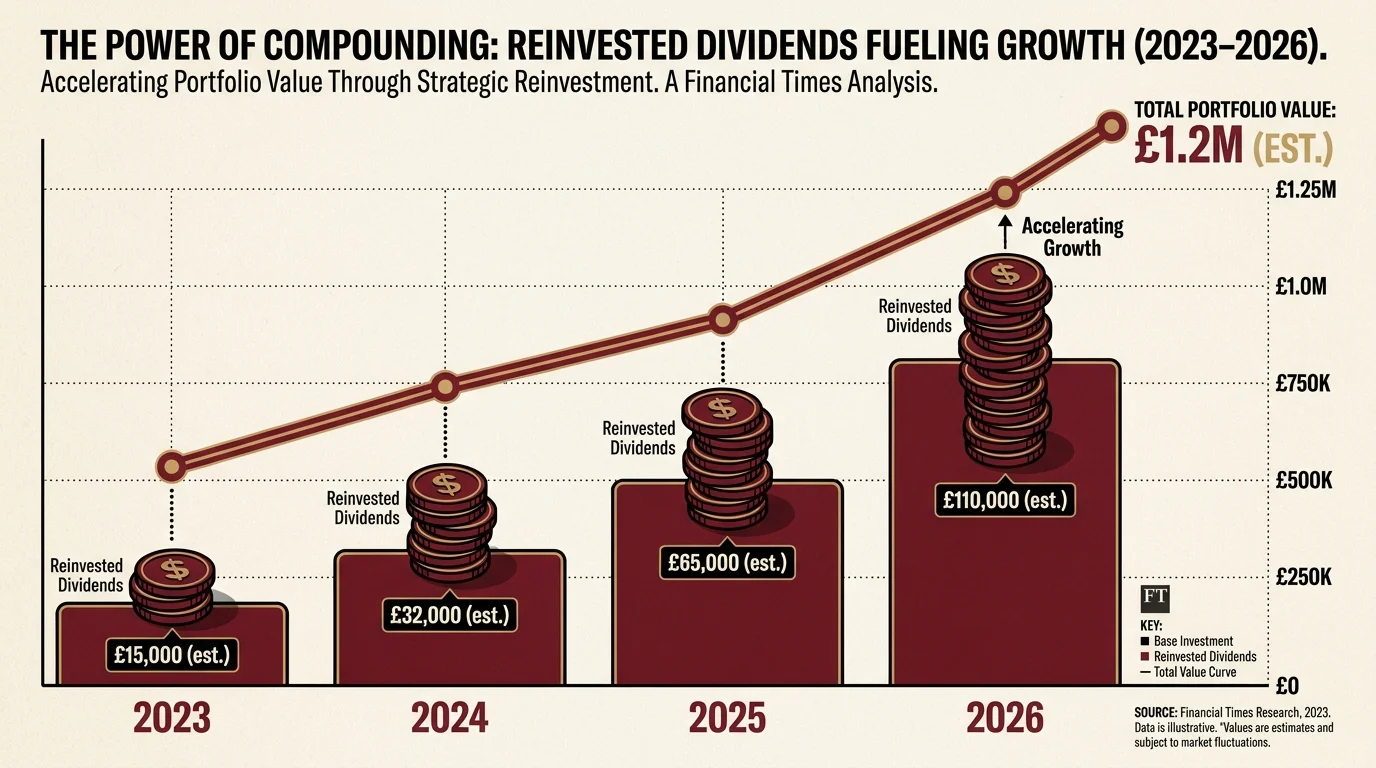

7. Dividend Growth Portfolios

Investing in companies with a history of increasing dividend payouts provides a growing stream of passive income that outpaces inflation. Rather than relying solely on price appreciation, dividend growth investing focuses on the cash distributed to shareholders each quarter. As these companies raise their dividends year after year, your personal yield on your original investment continually increases. This strategy requires patience and careful selection of high-quality equities, but it ultimately creates a robust income engine that sustains your purchasing power throughout a long retirement.

8. Renting Out Spare Rooms or Driveways

The sharing economy offers retirees innovative ways to monetize existing assets. If you kept your family home, you likely have unused space. Renting out a spare bedroom to travel nurses, leasing your driveway for RV parking, or offering up your basement for storage generates significant monthly side income. This strategy leverages the property you already own and maintain, turning dormant space into a reliable cash generator. It provides a practical solution for stretching a fixed budget without requiring new investments or complex financial maneuvering.

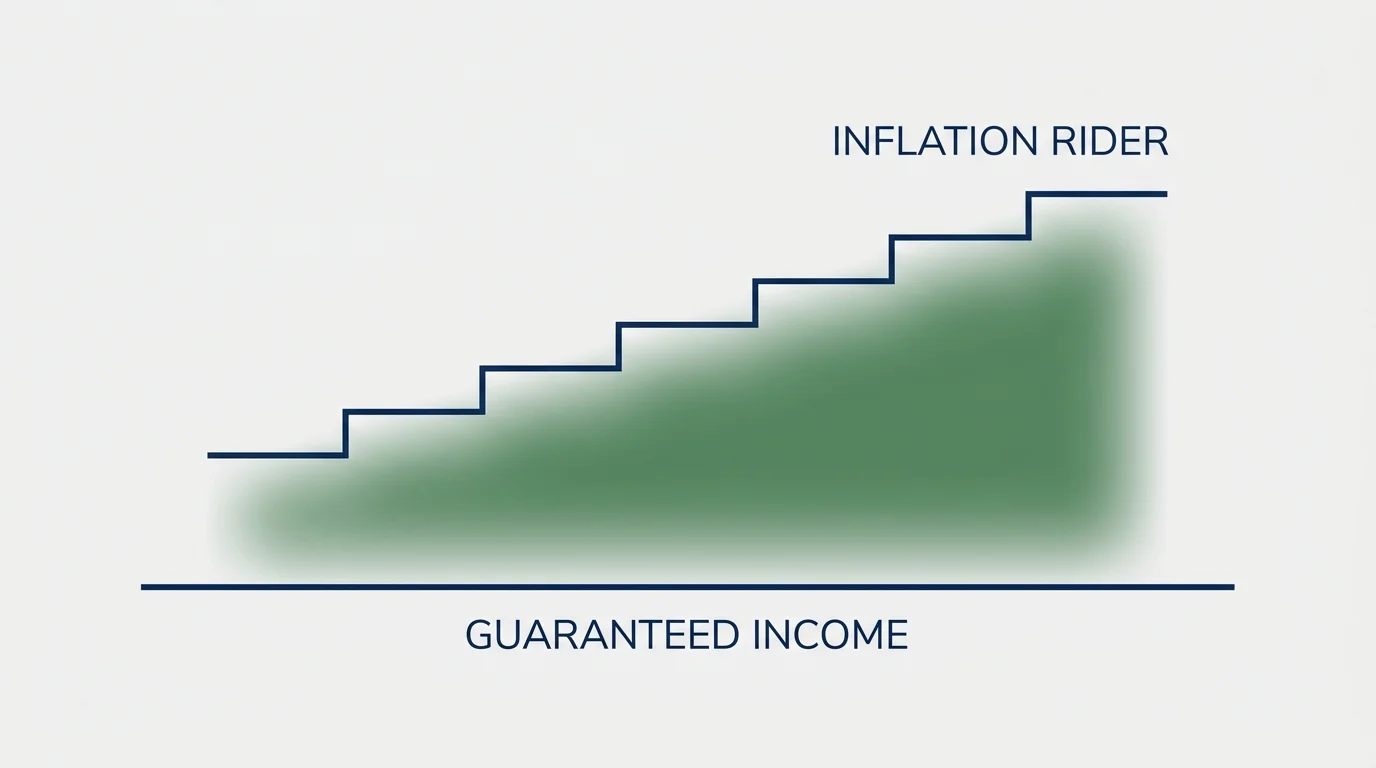

9. Annuities with Inflation Riders

Annuities offer a contractual guarantee of income for life, acting as a private pension that protects against outliving your assets. Modern products frequently include optional inflation riders, which automatically increase your monthly payout to keep pace with the rising cost of living. While they require relinquishing a portion of your liquid capital, the psychological comfort of receiving a guaranteed monthly check is invaluable. Incorporating a well-researched annuity into your financial plan establishes a solid floor of secure retirement income, empowering you to invest the remainder of your portfolio more aggressively.

Strategy Pillar 2: Lifestyle Design on a Flexible Budget

Creating a sustainable retirement requires aligning income streams with lifestyle choices. Retirees navigating financial freedom prioritize spending flexibility. By categorizing expenses into essential needs and discretionary wants, you dynamically adjust your lifestyle based on market performance and side income fluctuations. Embracing a flexible budget lets you travel extensively during high-income months and scale back when you prefer a slower pace. Recognizing diverse cultural backgrounds and varying mobility levels within your community also inspires new ways to live richly on less. Multi-generational housing arrangements and localized social groups provide deep fulfillment without demanding high financial output, proving that a rewarding retirement lifestyle does not require a massive bank account.

Strategy Pillar 3: Health, Wellness, and Managing Medical Costs

Physical health directly impacts financial stability in retirement. Medical expenses remain a significant threat to fixed budgets, making proactive wellness strategies a critical component of your financial plan. Investing time in preventative care and physical activity drastically reduces the likelihood of encountering catastrophic medical bills. When evaluating your retirement income, you must factor in the evolving costs associated with aging. Navigating the complexities of Medicare requires careful attention to coverage gaps and premium adjustments. Generating additional side income covers specialized treatments, wellness programs, and out-of-pocket costs that traditional insurance misses. By prioritizing your well-being, you protect your wealth and ensure you maintain the stamina required to enjoy the fruits of your labor.

Expert Voices: What Gerontologists and Financial Planners Say

Industry professionals agree the modern retirement paradigm demands a holistic approach. Financial planners emphasize that relying strictly on traditional bond yields and Social Security leaves you vulnerable to purchasing power erosion. They advocate for a diversified strategy balancing guaranteed cash flow with growth-oriented assets. Meanwhile, gerontologists highlight the profound mental health benefits of maintaining side income. They note that part-time work or monetized hobbies provide crucial social engagement and a renewed sense of purpose, which are key indicators of longevity and cognitive health. The consensus is clear; staying active economically and socially dramatically improves your retirement experience and insulates you against the isolation that often accompanies aging.

Risks and Safeguards: Protecting Your Financial Freedom

While adding new income streams enhances your security, it also introduces specific risks that require careful navigation. Earning too much side income triggers a benefit cliff, where increased revenue suddenly subjects your Social Security benefits to higher taxation or increases your Medicare Part B and Part D premiums through Income-Related Monthly Adjustment Amounts. You must also remain vigilant against the rising tide of financial scams targeting older adults. Fraudsters frequently disguise themselves as lucrative investment opportunities or high-paying remote work platforms. Always verify the legitimacy of any platform before transferring funds. Engaging with advocacy groups like the AARP provides excellent guidance on identifying current fraud tactics and implementing robust safeguards to protect your hard-earned wealth.

Frequently Asked Questions About Retirement Income

How does earning side income affect my Social Security benefits?

If you claim Social Security before reaching your full retirement age, earning side income above a certain annual threshold temporarily reduces your benefit payouts. The Social Security Administration withholds a portion of your benefits depending on how much you earn over the limit. However, once you reach your full retirement age, you can earn an unlimited amount of side income without facing any reduction in your monthly checks.

Are passive income streams truly passive for older adults?

The term passive income suggests a complete lack of effort, but nearly all streams require initial setup and ongoing monitoring. Building a dividend portfolio requires diligent research, and fractional real estate demands regular review of platform performance. While they do not require daily physical labor, maintaining these streams requires ongoing financial literacy and periodic portfolio rebalancing to ensure they remain aligned with your long-term goals.

Can I use Medicare to offset my health and wellness expenses?

Medicare covers a wide range of essential medical services, hospital stays, and prescription drugs, but it does not cover everything. Routine dental care, vision exams, hearing aids, and alternative wellness programs generally fall outside standard coverage. Understanding these limitations is crucial for your income planning, as you need to allocate specific funds from your passive income or side gigs to cover out-of-pocket health expenses.

What is the benefit cliff, and how do I avoid it?

A benefit cliff occurs when a small increase in your income disqualifies you from substantial government subsidies or triggers significant tax increases. For retirees, this commonly manifests as increased Medicare premiums or crossing the threshold where more of your Social Security becomes taxable. You avoid this by working closely with a tax professional to carefully manage your withdrawals using guidelines established by the Internal Revenue Service.

Your Next Steps

Achieving financial freedom and securing a vibrant retirement is entirely within your grasp. You do not need to implement every strategy at once to see a meaningful difference. Review your current cash flow and identify one specific area to generate additional support. Open a high-yield savings account or outline a plan to monetize a skill you possess. Take one actionable step in the next forty-eight hours to build a new income stream. Your future self will appreciate the foundation you lay today.