You might think modern retirement looks like an endless vacation, but recent data tells a more dynamic story about how Americans are living their post-career years. Record numbers of older adults are rewriting the rules of aging, transforming everything from workforce demographics to the way healthcare is managed. By unpacking the latest statistics from economists and gerontologists, you gain a massive advantage in planning your own future. This deep dive into the numbers reveals practical strategies for building a resilient income, staying vibrant, and navigating shifting policies. Whether you are counting down the months to your last day on the job or are already enjoying your newfound freedom, these evidence-based insights give you the blueprint needed to thrive.

A Snapshot of the Current Landscape

The year 2026 brings a wave of shifting economic currents that redefine how you approach your golden years. You face a landscape where longevity outpaces historical averages, forcing a fundamental rethink of how long your money actually needs to last. Data from researchers tracking senior demographics points to a critical reality: many Americans remain in a holding pattern regarding their retirement readiness, challenged by persistent inflation and changing workplace dynamics. Yet, this same environment offers unprecedented opportunities to reinvent your trajectory.

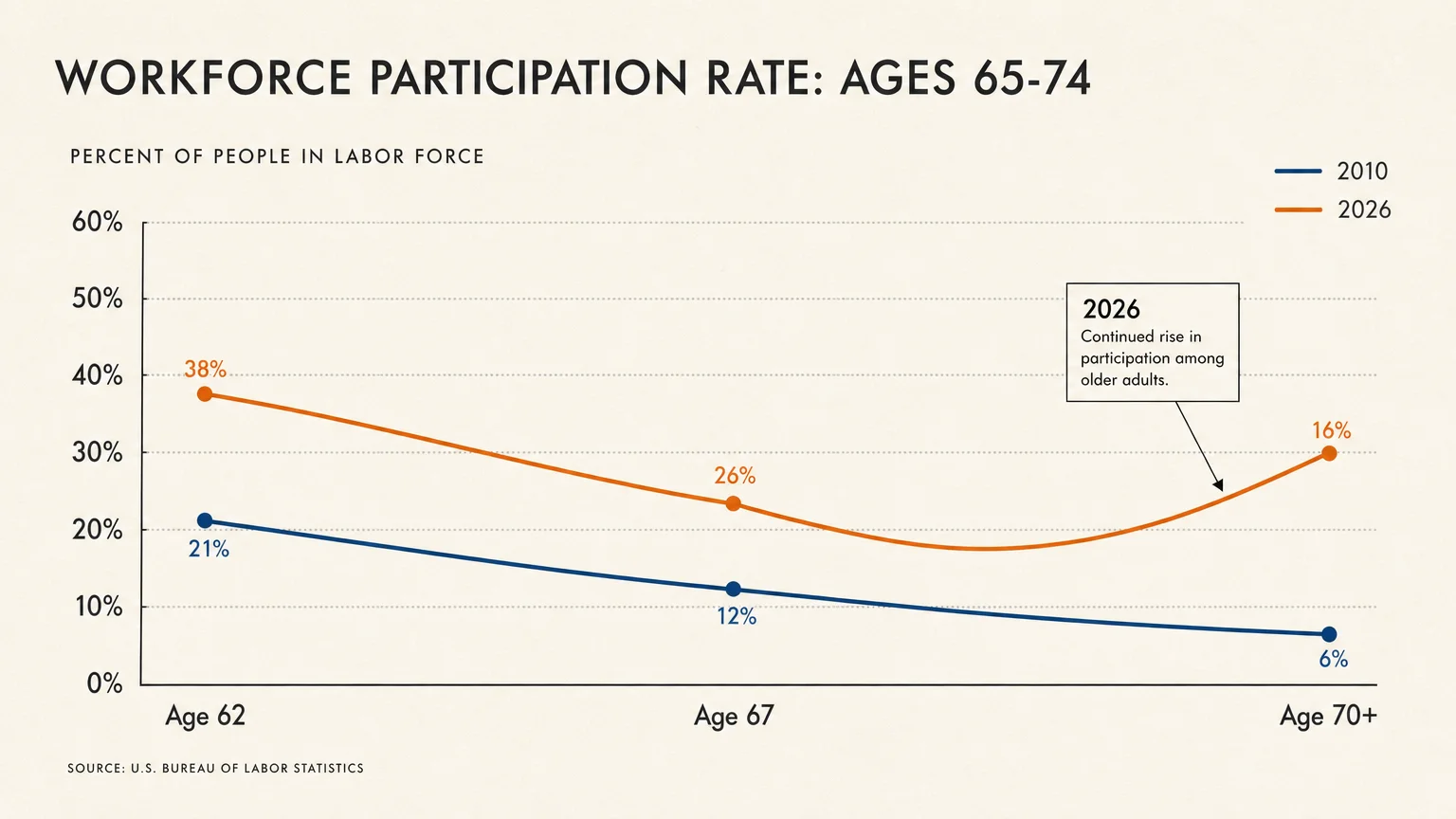

The Bureau of Labor Statistics continues to track a steady surge in older adults remaining in or returning to the workforce. Far from a sign of financial defeat, this trend highlights a resilient demographic taking charge of their monetary and mental well-being. You have more financial tools and flexible employment arrangements at your disposal than ever before to craft a secure future, provided you understand the numbers driving the market today. Knowing the hard data allows you to pivot away from outdated financial models and embrace a highly modern framework for aging.

Income Planning and Financial Resilience

When you build an income strategy for a retirement that might stretch three decades, you need far more than just a rough estimate of your living expenses. Relying solely on market returns exposes you to sequence-of-returns risk, a mathematical trap where a stock market downturn early in your retirement depletes your portfolio faster than it can ever recover. Certified Financial Planner professionals consistently stress the critical importance of creating a reliable paycheck from your investments.

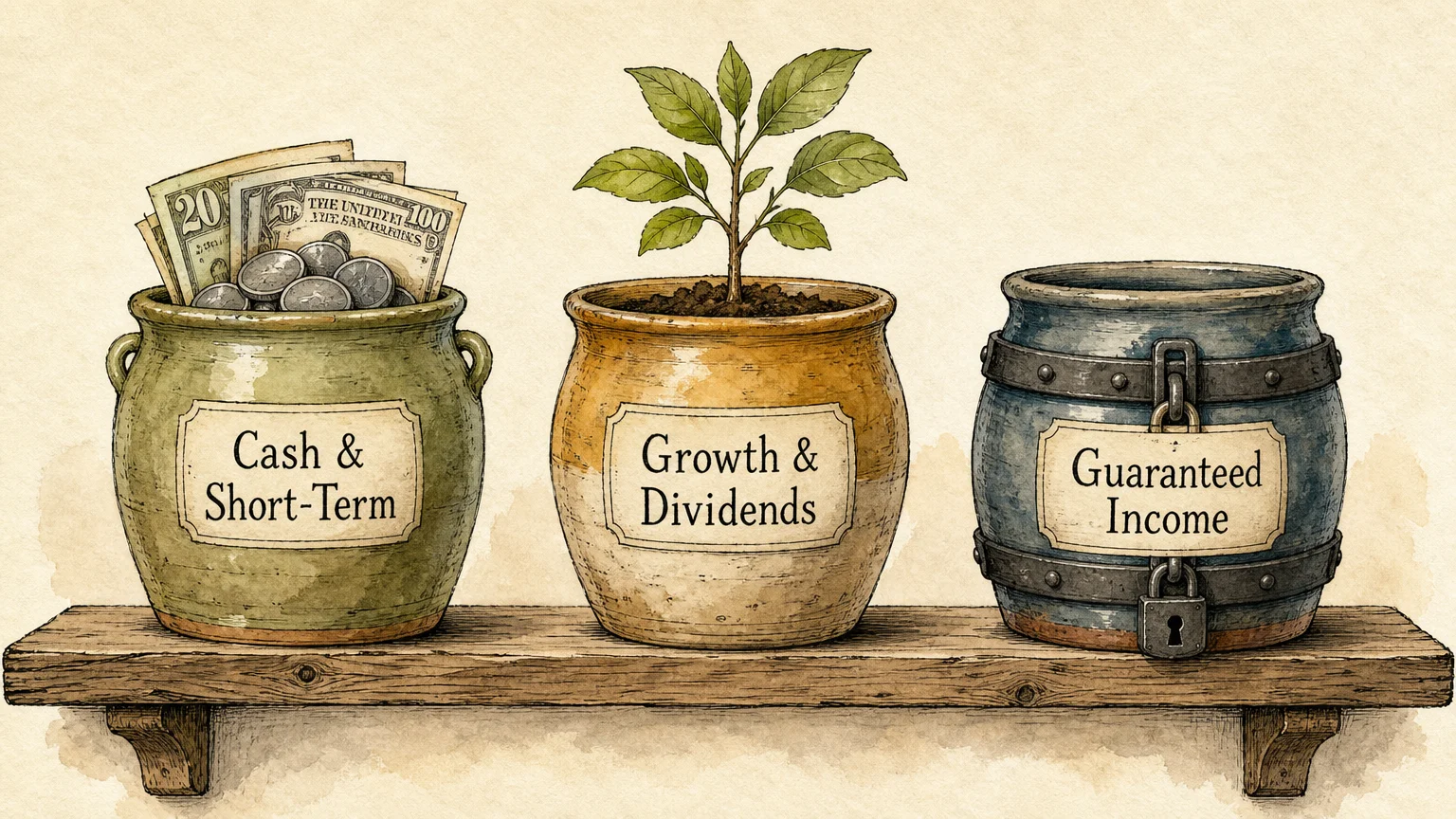

You accomplish this vital task by dividing your assets into distinct time-horizon buckets. One segment holds cash, certificates of deposit, and short-term bonds to cover your immediate needs over the next two to three years; this cash buffer prevents you from selling equity positions at a steep loss when the market inevitably dips. Another bucket focuses on reliable dividend-paying stocks or fixed annuities that act as a personal pension, ensuring a baseline of guaranteed cash flow.

Understanding the strict mechanics of your retirement accounts also requires a close look at tax implications. The Internal Revenue Service dictates exactly when and how much you must withdraw from your traditional, tax-deferred retirement accounts through Required Minimum Distributions. If you miscalculate these mandatory distributions, you face steep financial penalties that bite directly into your fixed budget.

You must also account for the silent reality that inflation quietly erodes your purchasing power. A fixed pension payment that feels incredibly generous today will buy significantly less in ten or fifteen years. Concrete data shows that retirees who diversify their income streams—combining Social Security benefits, modest part-time consulting, and a balanced investment portfolio—report much higher confidence in their overall financial security. You maintain control of your destiny by reviewing your withdrawal rates annually and adjusting your discretionary spending to match actual market performance rather than relying on a static, unchanging percentage.

Lifestyle Design and the Unretirement Movement

The concept of a full-stop, traditional retirement continues to fade into obscurity as the unretirement movement gains incredible momentum. Recent figures reveal that nearly one in four retirees engages in part-time or full-time work after officially leaving their primary careers. This profound shift transcends sheer financial necessity.

While many single retirees and women cite income generation as a primary motivator for returning to work, gerontologists note that a significant portion of older adults return to the workplace to maintain vital social connections and sharp cognitive function. You do not have to view work as a heavy burden in your later years. Instead, you can leverage your decades of institutional expertise to secure consulting roles, mentorship positions, or flexible gig work that fundamentally respects your need for autonomy and leisure.

This evolving stage of life also invites you to deeply rethink your physical environment and daily habits. You might find that the sprawling family home no longer serves your daily needs, especially when varying mobility requires a much more accessible floor plan. Downsizing or relocating to a community that aligns with your cultural background and social preferences plays a massive role in your overall psychological happiness.

Researchers studying senior demographics consistently find that prolonged isolation poses a severe health risk comparable to a sedentary lifestyle. By intentionally designing a daily routine that forces you to interact with neighbors, industry colleagues, or fellow volunteers, you build a robust social safety net. Practical lifestyle design means you actively evaluate your neighborhood for walkability, access to essential services, and rich opportunities for meaningful civic engagement. You can start today by skill-mapping your current professional talents and exploring how those translate into low-stress, high-reward advisory roles. Whether you mentor young professionals or manage local community projects, staying actively engaged delays cognitive decline and redefines your fundamental sense of purpose.

Health, Wellness, and the Cost of Longevity

Your physical well-being dictates your financial trajectory far more than any sudden stock market fluctuation. Healthcare remains one of the largest, most unpredictable expenses you will face as you navigate aging. According to tools like the AARP health care cost calculator, a couple retiring today must realistically earmark hundreds of thousands of dollars just to cover medical premiums and out-of-pocket expenses throughout their later years. You cannot safely rely on a generic national average; you must meticulously tailor your financial projections to your personal health history, pre-existing conditions, and family longevity trends.

Navigating the frustrating complexities of modern healthcare coverage requires serious, ongoing diligence. Medicare provides a foundational safety net, but it leaves significant coverage gaps that can devastate a carefully planned fixed budget. You must thoroughly understand the strict structural differences between managed Medicare Advantage plans and traditional Medicare paired with a supplemental Medigap policy. Your ultimate choice directly determines your out-of-pocket maximums, your network of available specialists, and your ability to seek specialized treatment while traveling across state lines.

Furthermore, you need to acknowledge the stark reality of long-term care expenses. Many pre-retirees falsely assume that government benefits will automatically pay for a nursing home stay or a dedicated in-home health aide. In truth, federal health programs primarily cover acute medical care and highly limited rehabilitative stays. You must actively explore long-term care insurance, asset-based hybrid policies, or aggressively dedicated savings to ensure you can afford the care you need without compromising your family’s financial stability. Concrete examples of this proactive planning involve fully funding a Health Savings Account during your final working years, allowing that capital to compound tax-free specifically to address future medical bills.

Identifying Risks and Establishing Safeguards

Every robust retirement plan includes a comprehensive, fiercely defensive strategy. You must remain vigilant against the increasingly sophisticated scams targeting seniors and their vulnerable nest eggs. Cybercriminals and coordinated phone scammers frequently impersonate government officials, attempting to steal your identity or siphon your hard-earned savings.

A classic example involves a hostile caller claiming to represent the Social Security Administration, aggressively demanding immediate payment to resolve a fabricated, urgent issue with your account. You protect yourself simply by hanging up and contacting the agency directly through their official, verified channels. The government will never demand payment via wire transfer, prepaid gift cards, or cryptocurrency.

Another significant, hidden risk involves the dreaded benefit cliff. If you decide to work while simultaneously receiving Social Security benefits before reaching your full retirement age, you face the federal earnings test. The government will temporarily withhold a substantial portion of your benefits if your earned income exceeds a specific annual threshold. While you eventually recoup these withheld funds through higher recalculated payments later in life, the sudden, unexpected reduction in immediate cash flow can deeply shock your monthly budget.

You must calculate your projected earnings carefully before accepting a new job offer or expanding your lucrative consulting business. Taking the time to map out these complex financial intersections prevents you from accidentally triggering higher tax brackets or absorbing increased Medicare premiums, commonly referred to as the Income-Related Monthly Adjustment Amount. Paying close attention to these subtle income thresholds actively safeguards your wealth from unnecessary, preventable taxation.

Frequently Asked Questions

How much does the average American actually have saved for retirement?

While financial institutions routinely publish average retirement account balances, these numbers vary wildly by age, geographic location, and income level. Recent industry data shows average portfolio balances hovering around the middle six figures for those nearing traditional retirement age. However, average numbers often skew unnaturally high due to ultra-wealthy outliers at the top of the spectrum. You should consider the profound difference between median and average savings. While the average might be inflated, the median balance provides a much more realistic benchmark for the typical American household. Ultimately, focusing strictly on your personal replacement ratio—the exact percentage of your pre-retirement income you need to maintain your specific standard of living—yields far more actionable insights than obsessing over generalized comparative benchmarks.

Will working part-time affect my Social Security benefits?

Working part-time only impacts your current Social Security payouts if you claim benefits before reaching your designated full retirement age. If you fall into this specific category and earn more than the annual limit set by the government, a portion of your benefits will be systematically withheld. Once you reach your full retirement age, however, you can earn as much as you want without facing any reduction in your monthly check. If you delay claiming until age seventy, you actually earn delayed retirement credits, permanently increasing your baseline benefit. Navigating this system requires you to intelligently weigh your immediate need for cash against the long-term mathematical advantage of locking in a higher monthly payout for the rest of your life.

What is the most overlooked expense in retirement?

Long-term care and out-of-pocket medical costs consistently catch new retirees completely off guard. Many individuals budget meticulously for housing, international travel, and daily food expenses, but they drastically underestimate the compounding cost of prescription drugs, comprehensive dental care, and hearing aids—essential services frequently excluded from basic medical coverage. You must also proactively plan for the financial impact of structural home modifications. As varying mobility becomes a factor, you may need to widen doorways, install secure grab bars, or convert a main-floor room into a primary bedroom. Budgeting for these environmental adaptations early prevents you from resorting to high-interest credit cards or rapidly depleting your emergency cash reserves when an acute physical need suddenly arises.

How can I protect my savings from inflation?

You combat the silent thief of inflation by maintaining a intelligently diversified portfolio that includes growth-oriented investments, even long after you stop working full-time. Shifting your entire nest egg into cash or ultra-conservative bonds practically guarantees that your purchasing power will decline severely over a twenty-year horizon. You might also explore Treasury Inflation-Protected Securities or Series I Savings Bonds, which automatically adjust their baseline value based on current inflation rates, providing a highly reliable hedge against rising consumer prices. Real estate also serves as a traditional, proven hedge against inflation, whether you own your primary residence outright or invest in diversified real estate investment trusts. Maintaining a balanced approach ensures that at least one sector of your portfolio will respond positively to rising consumer costs, thereby preserving your hard-earned standard of living.

Take Action for Your Future

Knowledge only transforms your retirement trajectory when you deliberately attach it to decisive, measurable action. You possess the practical tools, the verifiable data, and the proven strategies to construct a deeply fulfilling and financially secure future. Choose one specific area of your master plan that currently feels vulnerable and commit to addressing it immediately. Take the next forty-eight hours to log into your online government benefits portal to meticulously verify your earnings history, or sit down with a calculator to determine your exact projected monthly healthcare premiums. A single proactive step today drastically reduces your financial anxiety tomorrow. You worked incredibly hard for your money and your hard-won freedom; now is the time to actively ensure they both last for the rest of your vibrant, purposeful life.