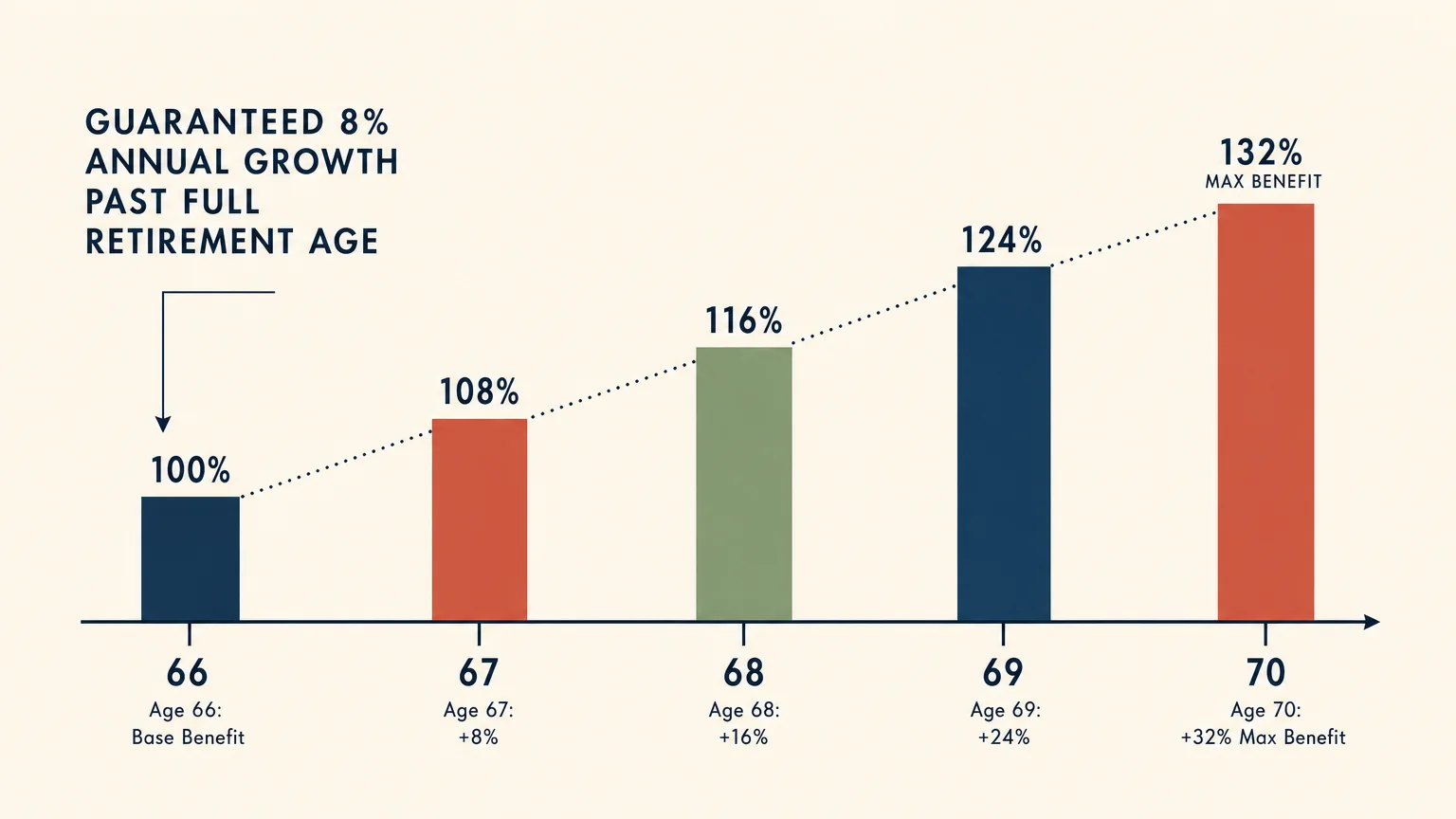

Holding off on your Social Security claim offers a reliable way to secure a higher guaranteed income for life. By waiting past your full retirement age, you lock in an eight percent annual boost to your monthly payout, creating a critical buffer against inflation and rising healthcare costs. More than a quarter of adults aged 65 to 74 remain in the workforce, reflecting a profound shift in how Americans approach their later years. Whether you plan to continue working, tap into investment accounts, or pursue a passion project, a delayed claiming strategy directly impacts your long-term financial resilience. Navigating this decision requires balancing your immediate cash flow needs with the undeniable math of delayed gratification.

Current Policy and Market Realities

The landscape of retirement continues to shift under the weight of changing demographics and economic pressures. Today, you face an environment where traditional pensions are rare, and the burden of funding a multi-decade retirement rests squarely on your shoulders. Inflation remains a persistent headwind, eating away at the purchasing power of fixed incomes. The federal government provides annual cost-of-living adjustments, but these bumps often lag behind the actual rising costs of housing, groceries, and healthcare. Delaying your benefits acts as a powerful countermeasure to this exact problem. For every year you wait past your full retirement age until age 70, your benefit grows by a guaranteed eight percent. This enhanced payout then becomes the new baseline for all future cost-of-living adjustments, compounding your monthly income significantly over a twenty- or thirty-year retirement. Data from the Bureau of Labor Statistics underscores a broader trend supporting this approach; the labor force participation rate for individuals aged 65 and older has climbed steadily, showing that Americans are staying active longer. This extended earning period provides the cash flow needed to delay claiming benefits and allows you to continue building your nest egg. Understanding how these macroeconomic factors intersect with your budget is the first step in formulating a robust plan.

The Core Strategy Pillars of a Delayed Claim

A successful strategy for maximizing your retirement benefits relies on three foundational pillars: intelligent income planning, intentional lifestyle design, and proactive health management.

Income Planning and Tax Efficiency

Implementing a delayed claiming strategy requires a thoughtful approach to bridging the income gap between the day you stop working full-time and the day you file for your enhanced benefits. You must determine how to cover living expenses during these gap years without derailing long-term financial security. This often involves tapping into your taxable brokerage accounts, traditional IRAs, or 401k plans. While drawing down your portfolio early might seem counterintuitive, you are essentially buying a larger, inflation-adjusted annuity for the rest of your life. By selectively liquidating assets, you gain control over your tax situation. Your federal benefits are taxed based on provisional income, which includes your adjusted gross income, nontaxable interest, and half of your benefit amount. If you rely on IRA withdrawals to bridge the gap, you can strategically manage your tax brackets before fixed income begins. Once you claim your maximum payout at age 70, your required minimum distributions from retirement accounts might be smaller because you spent down those balances. This orchestration of asset decumulation minimizes your lifetime tax burden. Consult a qualified tax professional to model withdrawal sequences, ensuring your bridge strategy aligns with guidelines set by the Internal Revenue Service.

Lifestyle Design for the Wait

Waiting to claim benefits does not mean putting your retirement dreams on hold; rather, it invites you to reimagine those early retirement years. Many older adults embrace phased retirement, transitioning from demanding corporate roles to part-time consulting, freelance work, or passion-driven employment. Earning a modest income during your early sixties easily covers essential expenses, allowing future payouts to grow in the background. Designing a lifestyle that balances work and leisure keeps you connected to your community. You might use this transitional phase to experiment with seasonal living, downsizing to a more manageable home, or relocating to a region with a lower cost of living. Lowering your overhead reduces the income you need to generate, making it easier to delay your claim. Furthermore, the flexibility of partial retirement provides the perfect opportunity to establish new routines. You can dedicate time to volunteering, mentoring younger professionals, or diving into hobbies that demand focus. By actively designing your lifestyle around a delayed claiming strategy, you transform a period of financial waiting into a rewarding chapter of personal growth.

Health, Wellness, and Longevity

Your physical and cognitive health play a massive role in the arithmetic of maximizing your payout. The decision to delay hinges on your life expectancy, making your wellness a literal financial asset. Break-even analysis shows that if you live past your early eighties, waiting until age 70 yields the highest cumulative lifetime payout. Therefore, prioritizing your health is a critical component of your retirement plan. Engaging in regular physical activity, prioritizing a nutrient-dense diet, and attending preventative medical screenings are actionable steps that support your longevity. The very act of working longer or maintaining an active schedule during your gap years provides profound cognitive benefits. Studies consistently show that mental stimulation and social interaction help delay cognitive decline. However, you must be realistic about your physical limitations and the demands of your profession. If your career requires grueling manual labor, extending your working years might cause irreversible wear and tear on your body, nullifying the benefits of a higher monthly check. In such cases, pivoting to a less physically demanding role or utilizing a portfolio bridge strategy becomes essential. Maintaining your vitality ensures you will actually get to enjoy the larger benefit checks you worked hard to secure.

Insights from Financial and Aging Professionals

Experts across wealth management and gerontology universally emphasize the power of patience when navigating the retirement system. Certified Financial Planners frequently highlight the fact that an eight percent annual return—guaranteed by the federal government and devoid of stock market volatility—is virtually impossible to replicate through traditional investments. They advise clients to view delayed claiming as longevity insurance, protecting against the threat of outliving one’s savings. From a psychological perspective, experts in aging research argue that the structure required to delay benefits yields tremendous secondary benefits. Gerontologists point out that individuals who maintain a connection to the workforce report higher levels of life satisfaction and a stronger sense of purpose. When you delay your claim, you are making a profound bet on your own future, altering how you view your health and daily habits. Moreover, experts at organizations like AARP remind retirees that the decision extends beyond the individual earner. For married couples, maximizing the higher earner’s benefit by waiting until age 70 guarantees that the surviving spouse will inherit the largest possible monthly check. This survivor benefit strategy remains a highly effective way to protect a widowed partner from financial hardship.

Navigating Risks and Building Safeguards

While delaying your claim offers immense upside, the strategy is not without distinct risks that require vigilant attention. The most obvious hazard is the unpredictable nature of human health. If you receive a terminal diagnosis or experience a severe decline in physical capabilities, adhering stubbornly to a delayed claiming strategy makes little sense. You must remain flexible, continuously reevaluating your health status and your family’s history of longevity to ensure the math still works in your favor. Another critical pitfall involves the complex intersection of healthcare and retirement planning. Even if you delay your primary income stream, you must proactively manage your transition to federal healthcare at age 65. Failing to enroll during your initial eligibility window can result in lifelong premium penalties, a costly mistake undermining the extra income gained from delaying. You can find detailed guidance on enrollment timelines directly through the official Medicare portal. Additionally, the period leading up to retirement makes you a target for sophisticated financial scams. Fraudsters frequently impersonate government officials, attempting to steal personal information under the guise of optimizing your benefits. Always verify communications independently utilizing resources from the Social Security Administration.

Frequently Asked Questions

Do I have to delay my healthcare enrollment if I delay my retirement claim?

You absolutely do not need to delay your healthcare enrollment, and doing so can be an expensive error. Eligibility for federal healthcare coverage begins at age 65, independent of when you start receiving your monthly retirement income. If you are not receiving benefits when you turn 65, you must proactively sign up for your healthcare coverage; it will not be done automatically. Missing your initial enrollment period can trigger late enrollment penalties that permanently increase your monthly premiums.

What happens to spousal benefits if I decide to delay my own claim?

The rules governing spousal benefits operate differently than those for individual retirement benefits. While your own retirement benefit grows by a guaranteed percentage for every year you wait past your full retirement age, spousal benefits do not earn these delayed retirement credits. The maximum spousal benefit is capped at fifty percent of the primary earner’s full retirement age benefit. If you are claiming strictly on your partner’s work record, there is no financial advantage to waiting past your own full retirement age.

How does working during my delay period affect my taxes?

Continuing to work while you wait to claim your benefits provides excellent cash flow, but you are generating earned income subject to federal and state taxation. Because you have not yet claimed your benefits, you do not have to worry about the earnings test withholding any of your monthly checks. You should work closely with a tax professional to understand how your wages interact with any withdrawals you make from traditional retirement accounts. Proper tax planning ensures your bridge strategy does not push you into an unnecessarily high tax bracket.

Can I change my mind if I delay my benefits but suddenly need the money?

Yes, the system provides a safety valve if your circumstances change unexpectedly. If you reach your full retirement age, decide to delay, and then experience a sudden financial hardship, you can apply for retroactive benefits. The government allows you to claim up to six months of retroactive payments, provided those months do not precede your full retirement age. Taking a retroactive lump sum resets your monthly benefit amount to what it would have been six months prior, reducing your permanent payout in exchange for immediate cash.

Moving Forward with Confidence

Creating a successful retirement requires you to blend the mathematics of financial planning with the personal vision you hold for your future. Holding out for a larger monthly check provides an unparalleled layer of security against inflation and longevity risks, ensuring you have the resources to thrive in your later decades. Yet, this approach demands careful preparation, an assessment of your health, and a solid bridge plan to cover your expenses today. Your financial journey is uniquely your own, and the right claiming strategy will seamlessly align with your specific household needs. Do not let uncertainty paralyze your decision-making process. Over the next forty-eight hours, take one concrete step toward clarity. Log into your government portal, download your earnings statement, and review your projected benefit amounts at various claiming ages. Armed with your actual numbers, you can sketch out a timeline that confidently supports the retirement lifestyle you have spent a lifetime building.