Protecting your nest egg requires you to avoid specific retirement income mistakes that systematically drain savings faster than you might realize. Outliving your money remains the most pressing concern for older adults today; recent data reveals over half of Americans aged 65 and older worry about late-life financial stability. A successful retirement depends on more than the size of your portfolio—it demands a tactical approach to withdrawals, taxation, and healthcare expenses. You must actively manage your resources to build a durable financial foundation that supports your desired lifestyle. Recognizing these common pitfalls early allows you to make precise adjustments, ensuring your hard-earned wealth lasts through every phase of your aging journey.

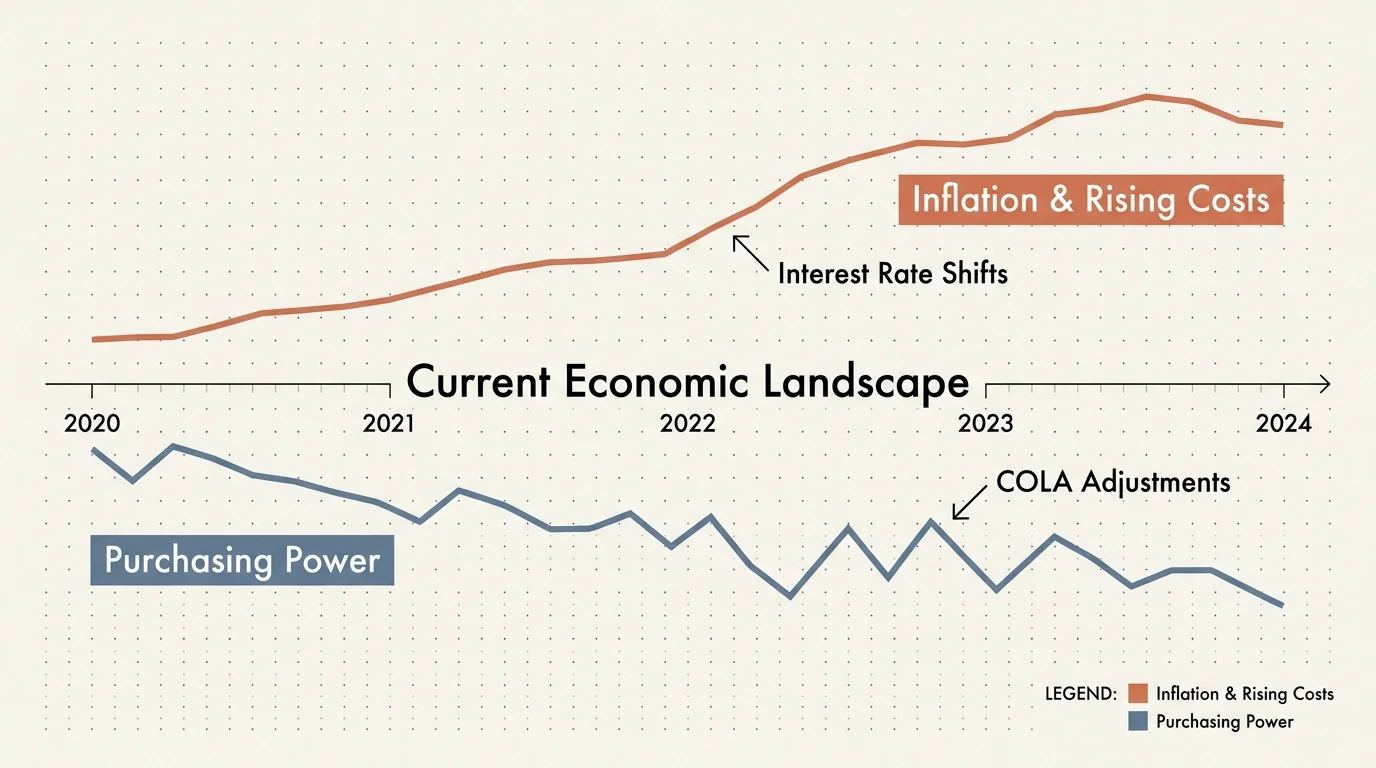

Current Economic Snapshot for Retirees

Recent shifts in policy and market dynamics directly influence how you should manage your retirement income strategy. Inflation shapes household purchasing power, prompting the Social Security Administration to issue an annual cost-of-living adjustment that impacts your monthly budget. Meanwhile, the IRS updates tax brackets and standard deductions, altering how much of your portfolio withdrawal actually stays in your pocket. Current economic conditions require you to remain vigilant; relying on a static financial plan designed a decade ago will leave you vulnerable to rising costs. The broader financial landscape now features fluctuating interest rates, affecting everything from your savings accounts to mortgage rates on a downsized home. You must review your fixed income sources against current inflation metrics to maintain a comfortable standard of living. Taking proactive steps to understand these shifts empowers you to protect your portfolio from unforeseen macroeconomic shocks, providing lasting peace of mind.

Mistake 1: Claiming Social Security at the Wrong Time

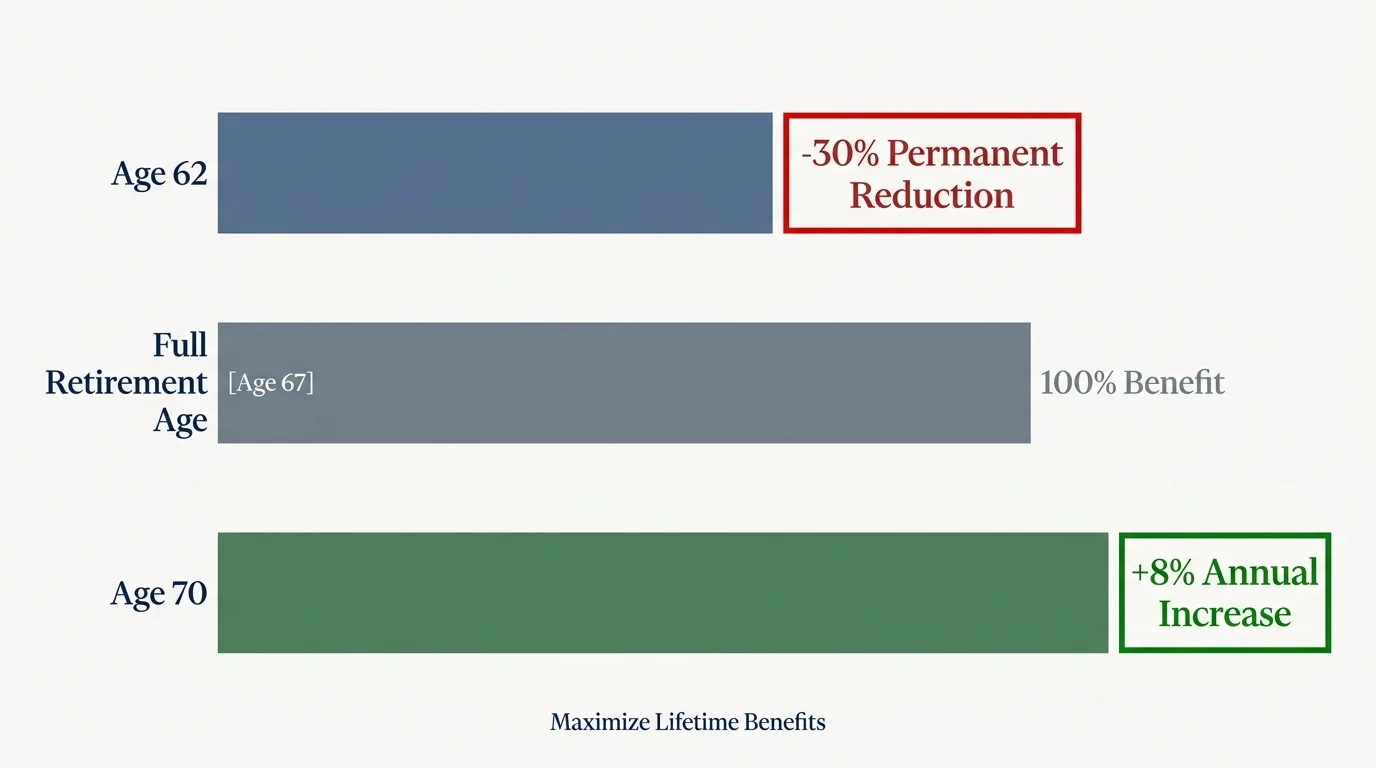

Your Social Security benefits serve as the foundation of your retirement income, yet claiming them at the wrong moment stands as one of the most expensive errors you can make. Taking benefits at age 62 permanently reduces your monthly check by up to 30 percent compared to waiting for your full retirement age. Conversely, delaying your claim until age 70 guarantees an eight percent increase for every year you wait past your full retirement age. Many retirees panic during market downturns and claim early, sacrificing massive lifetime benefits. You must coordinate your claiming strategy with your spouse, considering both individual life expectancies and survivor benefits. Financial planners consistently emphasize that maximizing this guaranteed income stream provides the most effective defense against outliving your savings. Review your earnings record on the official Social Security Administration website to map out your optimal claiming timeline.

Mistake 2: Ignoring the Tax Torpedo on Withdrawals

Taxes do not disappear when you stop working; they simply change form. Failing to implement a tax-efficient withdrawal strategy quietly devastates your retirement savings. Many retirees pull money exclusively from traditional IRAs and 401(k)s, triggering heavy income tax bills and potentially pushing themselves into higher marginal tax brackets. This influx of taxable income can cause up to 85 percent of your Social Security benefits to become taxable. You mitigate this risk by diversifying your tax exposure. Pulling funds proportionally from taxable brokerage accounts, tax-deferred accounts, and tax-free Roth accounts allows you to control your annual taxable income. Executing strategic Roth conversions during early retirement years defuses future tax bombs, ensuring you retain more of your principal and send less to the Internal Revenue Service.

Mistake 3: Underestimating Healthcare and Medicare Costs

Assuming Medicare covers all your medical expenses represents a critical vulnerability. While Medicare Parts A and B provide essential hospital and medical coverage, they do not pay for everything. You remain responsible for premiums, deductibles, copayments, and services like routine dental care, vision exams, and hearing aids. Fidelity Investments recently estimated that an average retired couple age 65 needs roughly $315,000 to cover healthcare expenses throughout their retirement. To protect your savings, you must build dedicated healthcare reserves. Utilizing Health Savings Accounts during your working years offers a triple-tax advantage for future medical costs. Once enrolled in Medicare, you should rigorously review your Part D prescription drug plan annually during the open enrollment period to ensure your coverage aligns with your specific health needs and medication requirements.

Mistake 4: Failing to Adjust Your Lifestyle Design and Budget

Retirement frees up 40 or more hours of your week, and filling that time often costs money. A common misstep involves carrying a high-spending, working-years lifestyle directly into retirement without analyzing the long-term impact on a fixed portfolio. Travel, dining out, and new hobbies quickly deplete cash reserves during your initial active years. You must intentionally design a lifestyle that aligns with your realistic income constraints. Creating a distinct budget for essential expenses—housing, food, and utilities—and a separate bucket for discretionary spending allows you to adjust quickly when markets decline. Downsizing your primary residence dramatically reduces fixed overhead. Retirees who thrive financially maintain a flexible mindset, finding purpose through low-cost activities, volunteering, and community engagement rather than relying exclusively on expensive leisure pursuits.

Mistake 5: Holding Too Much Cash or Playing It Too Safe

Fear of market volatility drives many well-meaning retirees to liquidate their investments and hold excessive cash. While preserving capital feels safe, inflation acts as an invisible tax that steadily erodes your purchasing power. If your portfolio fails to generate returns that outpace inflation, you effectively lose money every year. A successful strategy requires growth to sustain you over a potential 30-year time horizon. Financial planners advocate maintaining a balanced asset allocation that includes equities for long-term growth and fixed-income investments for stability. You can construct a cash buffer containing one to two years of living expenses to ride out immediate market corrections without selling stocks at a loss. This targeted strategy provides psychological comfort while allowing the remainder of your portfolio to compound and grow over time.

Mistake 6: Neglecting to Plan for Long-Term Care Needs

The physical realities of aging necessitate a pragmatic approach to long-term care planning. A person turning 65 today has almost a 70 percent chance of needing some type of long-term care services in their remaining years. Medicare strictly limits coverage for custodial care, leaving you responsible for assisted living facilities, nursing homes, or in-home health aides. Paying out-of-pocket easily costs upwards of $100,000 annually, swiftly draining savings and potentially impoverishing a surviving spouse. You must evaluate your options long before a health crisis strikes. Traditional long-term care insurance, hybrid life insurance policies, or earmarked real estate assets serve as vital funding mechanisms. Discussing your care preferences with your family and consulting aging resources from organizations like AARP ensures you retain control over your health decisions without sacrificing your financial legacy.

Mistake 7: Supporting Adult Children at the Expense of Your Own Security

Generosity toward your family is a natural impulse, but prioritizing your adult children’s financial needs over your own retirement security threatens your independence. Providing substantial down payments for homes or continually subsidizing an adult child’s living expenses fatally fractures your retirement plan. Unlike your children, who have decades to earn income and recover from financial setbacks, you do not have the luxury of time or a regular paycheck to rebuild a depleted nest egg. You must establish firm financial boundaries to protect your resources. Supporting your family should only occur after you stress-test your portfolio to guarantee your basic needs and emergency funds remain secure. True financial independence means ensuring you never become a financial burden to those same children later in life.

Mistake 8: Falling Victim to High-Yield Scams and Fraud

Seniors represent prime targets for sophisticated financial scams, and falling prey to fraud annihilates your retirement savings overnight. As you seek ways to stretch your income, promises of guaranteed high yields or risk-free crypto investments seem overwhelmingly attractive. Scammers exploit the fear of outliving assets by peddling fraudulent annuities, phony real estate syndications, and complex digital currency schemes. You must cultivate a healthy skepticism toward any unsolicited financial opportunity. Always verify the credentials of financial advisors through federal regulatory resources before handing over your money. Safeguard your personal information, utilize multi-factor authentication on financial accounts, and consult a trusted fiduciary professional before making major shifts in your asset allocation. Protecting your wealth demands active vigilance and a refusal to be rushed into opaque investment decisions.

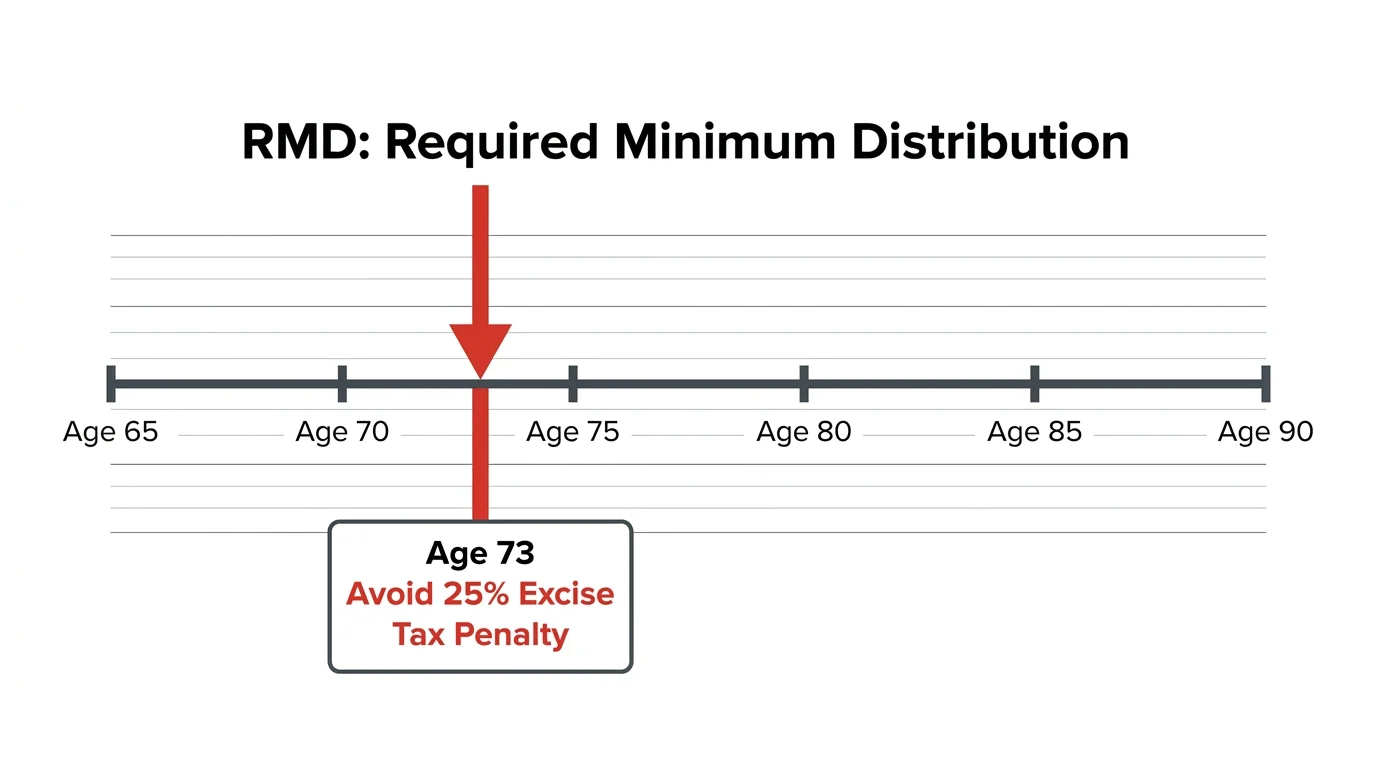

Mistake 9: Overlooking the Impact of Required Minimum Distributions

When you reach your early seventies, the federal government forces you to begin withdrawing money from your traditional tax-deferred accounts. These Required Minimum Distributions mandate taking out a specific percentage of your portfolio annually, regardless of whether you actually need the cash. Failing to plan for these distributions triggers significant unintended consequences. The additional income instantly propels you into a higher tax bracket and subjects you to Medicare premium surcharges. To manage this benefit cliff, you should coordinate with a tax professional well before your required beginning date. Strategies such as Qualified Charitable Distributions allow you to transfer funds directly from your IRA to an eligible charity, satisfying your minimum distribution requirement without adding a single dollar to your adjusted gross income.

Frequently Asked Questions

How much of my retirement savings can I safely withdraw each year?

Financial professionals historically recommended the four percent rule—withdrawing four percent of your portfolio initially and adjusting for inflation. While helpful, current market dynamics and longer life expectancies demand a personalized approach. You should consider a dynamic withdrawal strategy that flexes based on market performance. Pull back on discretionary spending during down markets to preserve principal, while allowing for larger withdrawals during bull markets. Consulting a Certified Financial Planner helps establish a flexible rate tailored specifically to your unique asset mix and lifespan expectations.

Should I pay off my mortgage before I retire?

Entering retirement debt-free significantly reduces your monthly cash flow requirements, providing immense peace of mind while lowering required portfolio withdrawals. However, if you hold a fixed-rate mortgage with an exceptionally low interest rate, your capital might generate higher returns invested in the market than the cost of your debt. You must weigh the psychological comfort of owning your home outright against the mathematical benefits of keeping funds liquid. For many, the emotional relief of eliminating a mortgage payment far outweighs potential fractional investing gains.

How do I protect my retirement income from inflation?

Combating inflation requires a multi-pronged approach to your portfolio design and lifestyle management. You must maintain exposure to growth-oriented assets like equities, which historically outpace inflation over long periods. Additionally, incorporating Treasury Inflation-Protected Securities or certain types of annuities with cost-of-living adjustments helps stabilize your purchasing power. Maximizing your Social Security benefits also provides a vital, guaranteed defense against rising living costs. Adopting a flexible budget allows you to adjust spending patterns when the costs of everyday goods spike, protecting your core savings from rapid depletion.

When is the right time to hire a financial advisor?

You should engage a fiduciary financial advisor when the complexity of your retirement income, tax planning, and estate goals exceeds your comfort level. Transitioning from saving money to safely spending it involves entirely different mathematical strategies and carries much higher stakes. An experienced professional helps you sequence your withdrawals, optimize your tax situation, and avoid emotional investing errors during market volatility. Seek out an advisor who acts as a fiduciary—legally obligated to put your financial interests ahead of their own—to ensure you receive objective, conflict-free guidance.

Take Action Today

Knowledge alone will not protect your retirement savings; you must apply these insights to your specific financial reality. Over the next 48 hours, commit to reviewing just one aspect of your retirement strategy. Log into your financial accounts to check your current cash allocation, pull your latest Social Security statement to evaluate your projected benefits, or schedule a brief meeting with a fiduciary planner to discuss your withdrawal plan. Whether you decide to reassess your budget, consult a professional, or simply educate yourself further on Medicare options, taking ownership of these financial variables reduces your vulnerability to economic turbulence. Making a single, proactive adjustment today builds the momentum needed to secure your financial future. Your hard work brought you to this stage of life, and taking decisive action now ensures your wealth will fully support the vibrant, fulfilling retirement you deserve.