Retirees face a complex financial puzzle today, and understanding the latest shifts in Social Security is the fastest way to secure your hard-earned benefits. The policies governing your monthly checks have changed again, directly impacting your bottom line and future purchasing power. While cost-of-living adjustments try to keep pace with inflation, rising healthcare premiums and stagnant tax thresholds often quietly erode those gains. You need a clear view of exactly what changed this year—and how to adjust your personal financial strategy in response. By mastering the new earnings limits and tracking Medicare deductions, you can protect your income, maintain your lifestyle, and make confident choices about your financial future.

The Current Reality of Retirement Income

The financial landscape for older adults in the United States requires constant vigilance. Unpredictable economic cycles place immense pressure on fixed incomes. While high inflation has subsided, the cumulative effect of rising costs remains a daily reality at the grocery store. You need accurate data to make informed choices about your household budget. Policy adjustments out of Washington dictate exactly how much money lands in your bank account each month; ignorance of these nuances can cost you thousands of dollars annually. Relying on outdated assumptions about Social Security leaves you vulnerable to unexpected tax bills. You must actively manage your income streams to preserve your wealth. Understanding the structural updates to the federal retirement system empowers you to build a resilient safety net.

5 Social Security Changes You Need to Watch

1. The Cost-of-Living Adjustment (COLA) Reality

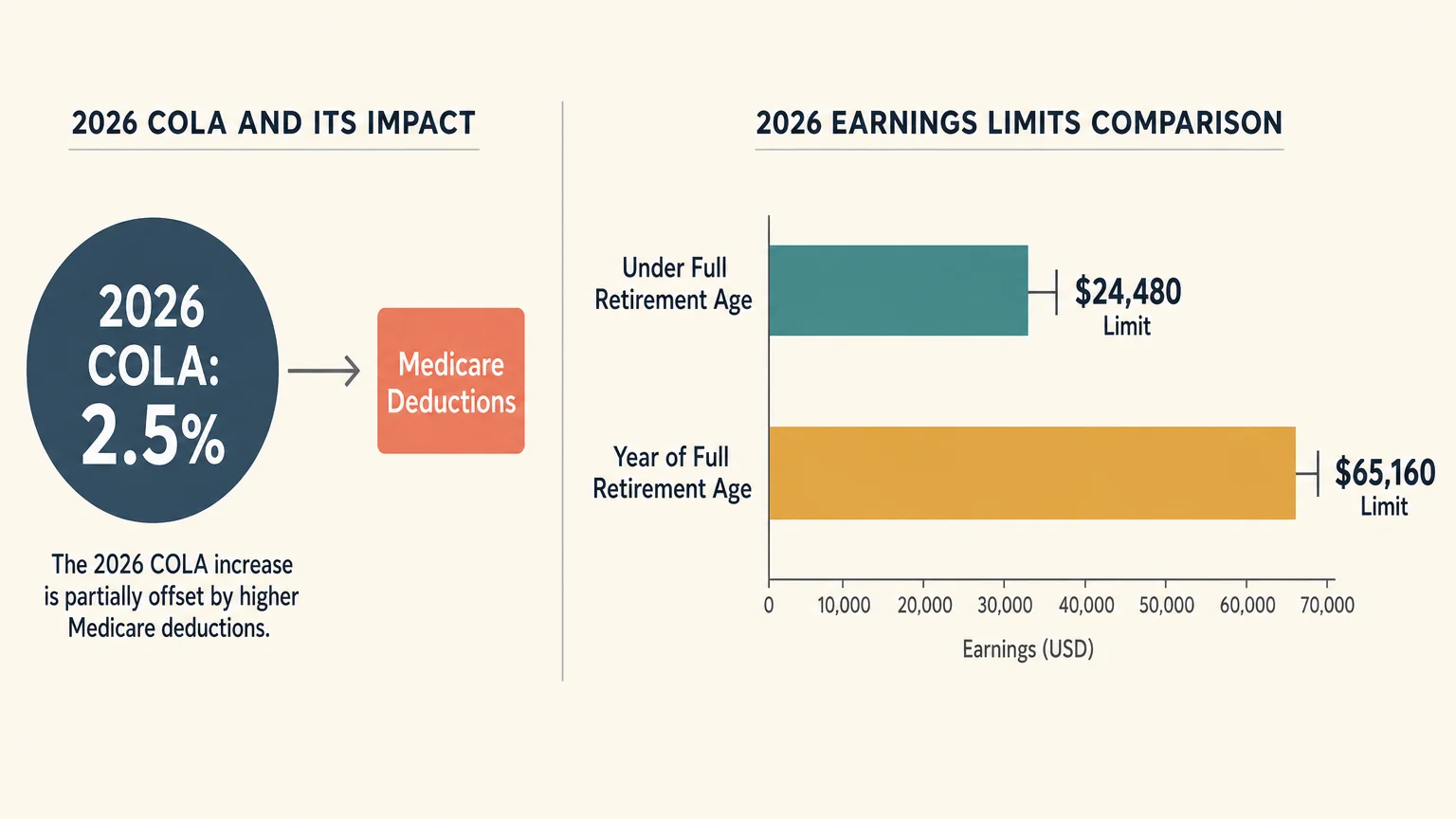

Your Social Security check is adjusted to combat the eroding power of inflation. For 2026, the administration announced a modest 2.5 percent cost-of-living adjustment. While this increase offers a necessary buffer against rising consumer prices, it represents a significant cool-down from historically high adjustments. You must understand that this percentage is applied to your gross benefit amount, not the net cash you actually receive.

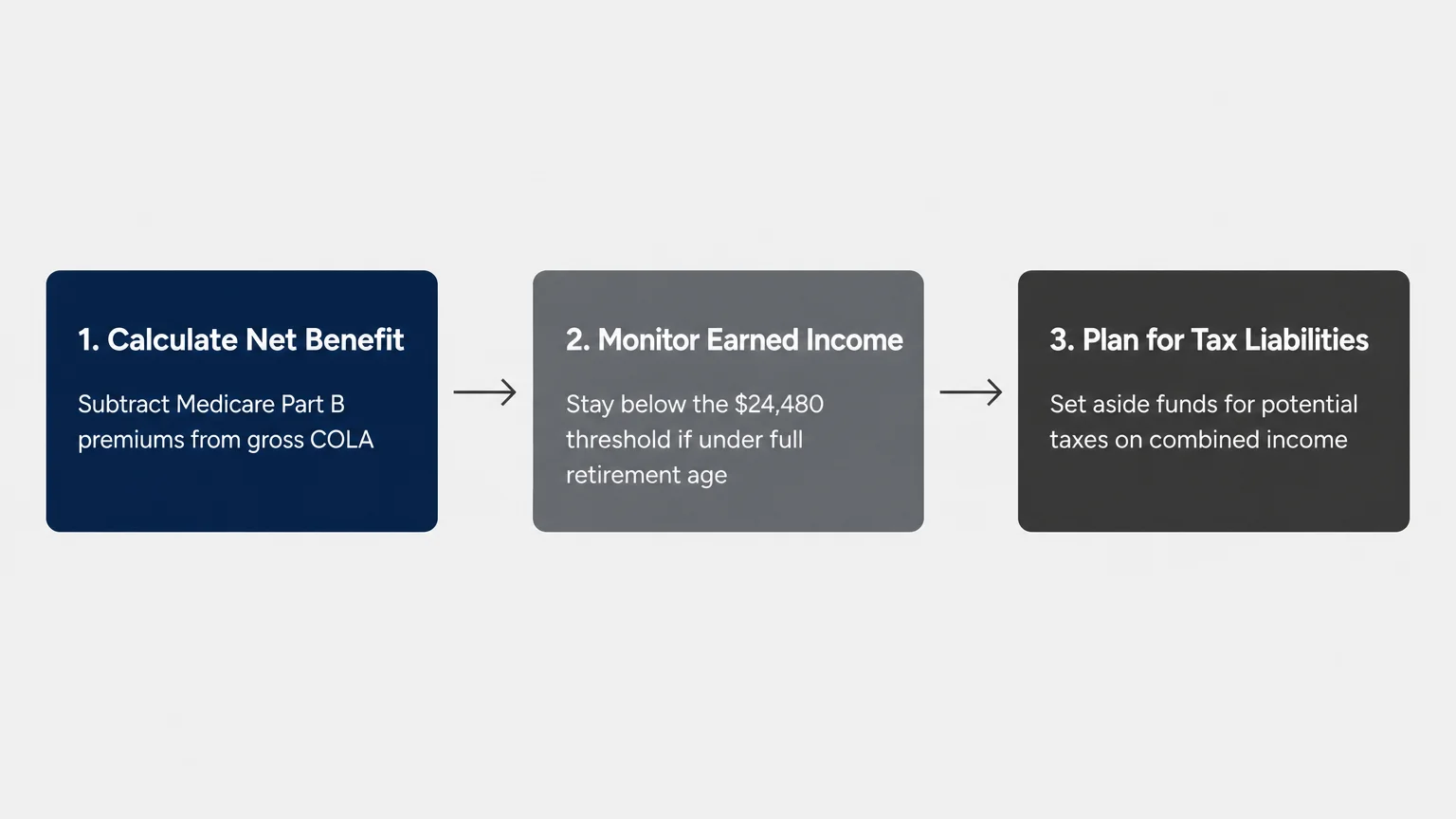

Many retirees make the mistake of mentally spending their COLA increase before it arrives. You should update your household budget based strictly on the net deposit you receive after all deductions. A portion of your raise might vanish before you ever see it, diverted to cover mandatory federal healthcare costs. You should evaluate your spending patterns against your actual net income to avoid falling into debt.

2. Rising Earnings Test Limits for Working Retirees

Working during retirement offers excellent mental stimulation and a secondary income stream. The Social Security Administration encourages this by incrementally raising the earnings test limits. If you claim benefits before reaching your full retirement age in 2026, you can earn up to $24,480 without facing any benefit reductions. Once your earned income exceeds that threshold, the government withholds one dollar for every two dollars you earn.

During the specific calendar year you reach your full retirement age, the earnings limit jumps to $65,160. The withholding ratio also shifts; you lose one dollar for every three dollars earned above the cap. Remember that withheld benefits are not permanently confiscated. Once you reach full retirement age, your monthly payout is recalculated upward to account for those withheld months.

3. The Squeeze of Medicare Part B Premiums

Healthcare costs remain the most unpredictable variable in retirement planning. Most beneficiaries have their Medicare Part B premiums deducted directly from their Social Security checks. When the standard monthly premium for Part B increases, it directly cannibalizes your cost-of-living adjustment. This dynamic creates a frustrating scenario where your gross benefit goes up, but your actual take-home pay remains flat.

The Medicare hold harmless provision does offer protection for many retirees. This rule ensures that your Part B premium increase cannot exceed your COLA, preventing your net check from decreasing. However, this safeguard does not apply to everyone; high-income earners frequently face the full brunt of premium hikes. You need to verify your specific premium tier through the federal Medicare portal.

4. Stagnant Taxation Thresholds Trigger Surprises

One of the most overlooked threats to your retirement income involves the taxation of your benefits. The federal thresholds that determine whether your Social Security income is taxable have remained completely unchanged since 1984. As annual cost-of-living adjustments naturally push your nominal income higher over time, you are increasingly likely to breach these decades-old caps. A single filer earning a combined income over $25,000, or joint filers surpassing $32,000, will owe federal taxes on up to 50 percent of their benefits.

If your combined income pushes past $34,000 for individuals or $44,000 for couples, up to 85 percent of your Social Security becomes taxable. A simple 2.5 percent COLA can trigger a disproportionately large tax bill. Consulting with a certified tax professional can help you structure your withdrawals to minimize this penalty.

5. The Transition to Age 67 for Full Retirement Benefits

The timeline for claiming your maximum baseline benefit has fundamentally shifted. The gradual phase-in of the new full retirement age is now complete. If you were born in 1960 or later, your full retirement age is firmly set at 67. Claiming your benefits at age 62 remains an option, but doing so now incurs a permanent 30 percent reduction in your monthly payouts compared to waiting.

You must factor this delayed timeline into your long-term income strategy. Waiting until age 70 continues to offer the maximum possible payout, adding an 8 percent delayed retirement credit for every year you hold off past age 67. You should carefully analyze your life expectancy, your family health history, and your available cash reserves before locking in a claiming age.

Strategy Pillars for a Secure Retirement

Income Planning and Financial Optimization

Optimizing your retirement income requires synchronizing your Social Security strategy with your broader investment portfolio. You cannot treat your monthly federal benefit in isolation; it must integrate smoothly with your IRAs and taxable brokerage assets. Strategic drawdown methods extend the longevity of your portfolio. For example, withdrawing funds from taxable accounts before touching tax-advantaged accounts keeps your adjusted gross income lower, reducing the taxation on your benefits. You should establish an account on the official Social Security Administration website to run personalized benefit estimates. Running multiple mathematical scenarios helps you pinpoint the exact claiming age that maximizes your wealth.

Designing a Purposeful Lifestyle

Retirement represents a profound psychological transition. A purposeful lifestyle directly influences your financial stability and overall satisfaction. Many older adults find that part-time employment provides necessary mental engagement while easing the strain on their savings. Volunteering your time with local community organizations delivers deep meaning without requiring large financial outputs. You must intentionally design your daily routine to balance inexpensive hobbies with occasional luxury expenditures. Living on a largely fixed income requires mastering the art of prioritization. By actively choosing where to allocate your discretionary funds, you can maintain a fulfilling lifestyle regardless of market volatility.

Prioritizing Health and Wellness

Your physical health is inextricably linked to your financial resilience. Chronic medical conditions rapidly deplete your retirement savings through out-of-pocket costs and prescription co-pays. Prioritizing preventative care is the most effective financial strategy you can deploy. You should fully utilize the free preventative screenings and annual wellness visits covered by your Medicare plan. Engaging in daily physical activity preserves your mobility and reduces your reliance on expensive medical interventions. Eating a nutrient-dense diet and maintaining strong social connections have been scientifically proven to extend healthy longevity. Investing time into your well-being today protects your assets tomorrow.

Expert Perspectives on Navigating Policy Shifts

Gaining insight from seasoned professionals helps you filter out the noise. Certified Financial Planners consistently emphasize the danger of emotional decision-making when claiming federal benefits. Financial experts frequently observe that retirees panic during periods of high inflation, choosing to claim their benefits early to secure immediate cash flow. This reactionary move permanently locks in a reduced payout. Experts recommend building a reliable cash buffer in a high-yield savings account to ride out economic turbulence without claiming benefits prematurely.

Gerontologists highlight the critical intersection of policy and quality of life. Research indicates that older adults who maintain part-time employment experience lower rates of cognitive decline. The rising earnings test limits provide a valuable opportunity for you to stay engaged in the workforce without instantly sacrificing your benefits. Experts strongly advocate for a phased retirement approach, allowing you to adjust to a new daily rhythm.

Recognizing Risks and Safeguarding Your Benefits

The modern retirement landscape is unfortunately littered with financial hazards. Scam artists constantly exploit announcements about cost-of-living adjustments to steal sensitive personal information. You must remember that federal agencies will never call you out of the blue demanding payment via wire transfers. If you receive a suspicious call regarding your benefits, hang up immediately and contact the fraud prevention resources available through organizations like AARP.

Beyond outright fraud, watch out for dangerous benefit cliffs. A benefit cliff occurs when a minor increase in your income disqualifies you from essential assistance programs. If your cost-of-living adjustment pushes your monthly income slightly above the threshold for utility relief, you could lose vital support. You should actively monitor your gross income to ensure a slight bump in your federal check does not trigger a massive loss of secondary benefits.

Frequently Asked Questions

Can I work full-time and still collect my Social Security benefits?

Yes, but timing dictates how much you keep. If you have reached your full retirement age, you can earn an unlimited amount without reductions. If you have not, your benefits face temporary reductions if your income exceeds the annual limit. Track your wages carefully if working before age 67.

Will my benefits automatically increase when I reach my full retirement age?

Your base benefit does not suddenly jump on your birthday. However, if you had benefits withheld in previous years because you earned above the limit, the administration automatically recalculates your payment. This increases your ongoing check to account for withheld months without requiring you to file any special paperwork.

How do I know if I owe federal taxes on my Social Security income?

You must determine your combined income, which includes your adjusted gross income, nontaxable interest, and half of your yearly benefits. If this exceeds $25,000 for single filers or $32,000 for married couples, a portion becomes taxable. Use the worksheets on the official Internal Revenue Service website to run your numbers.

What happens if Medicare premiums increase more than my cost-of-living adjustment?

For most retirees, the hold harmless provision ensures your standard Part B premium cannot increase by more than your cost-of-living adjustment, guaranteeing your net deposit will not decrease. However, high-income beneficiaries paying income-related surcharges do not receive this exact protection and may experience a reduction in their net checks.

Your Next Steps

Information only holds value when paired with immediate action. The regulatory environment surrounding your retirement income requires proactive management. You have the power to optimize your cash flow and protect your financial independence. Take a moment to log into your official federal account and download your most recent statement. Verify your reported earnings history and review your projected payouts at different claiming ages. Taking this single, simple action over the next 48 hours will illuminate your financial reality and help you map out a confident path forward.