Millions of older Americans leave valuable benefits on the table every year because they simply do not realize they qualify for additional monthly income. You can unlock thousands of dollars in hidden government programs, health care subsidies, and senior assistance funds designed to ease the strain of fixed budgets. Recent data from the National Council on Aging reveals that billions in benefits go unclaimed annually, leaving vulnerable retirees struggling to cover basic living expenses. Whether you face rising utility bills, increasing prescription costs, or property tax burdens, discovering these underutilized programs provides vital financial breathing room. Taking the time to evaluate your eligibility could drastically transform your standard of living and secure the comfortable retirement you deserve.

A Snapshot of Today’s Retirement Landscape

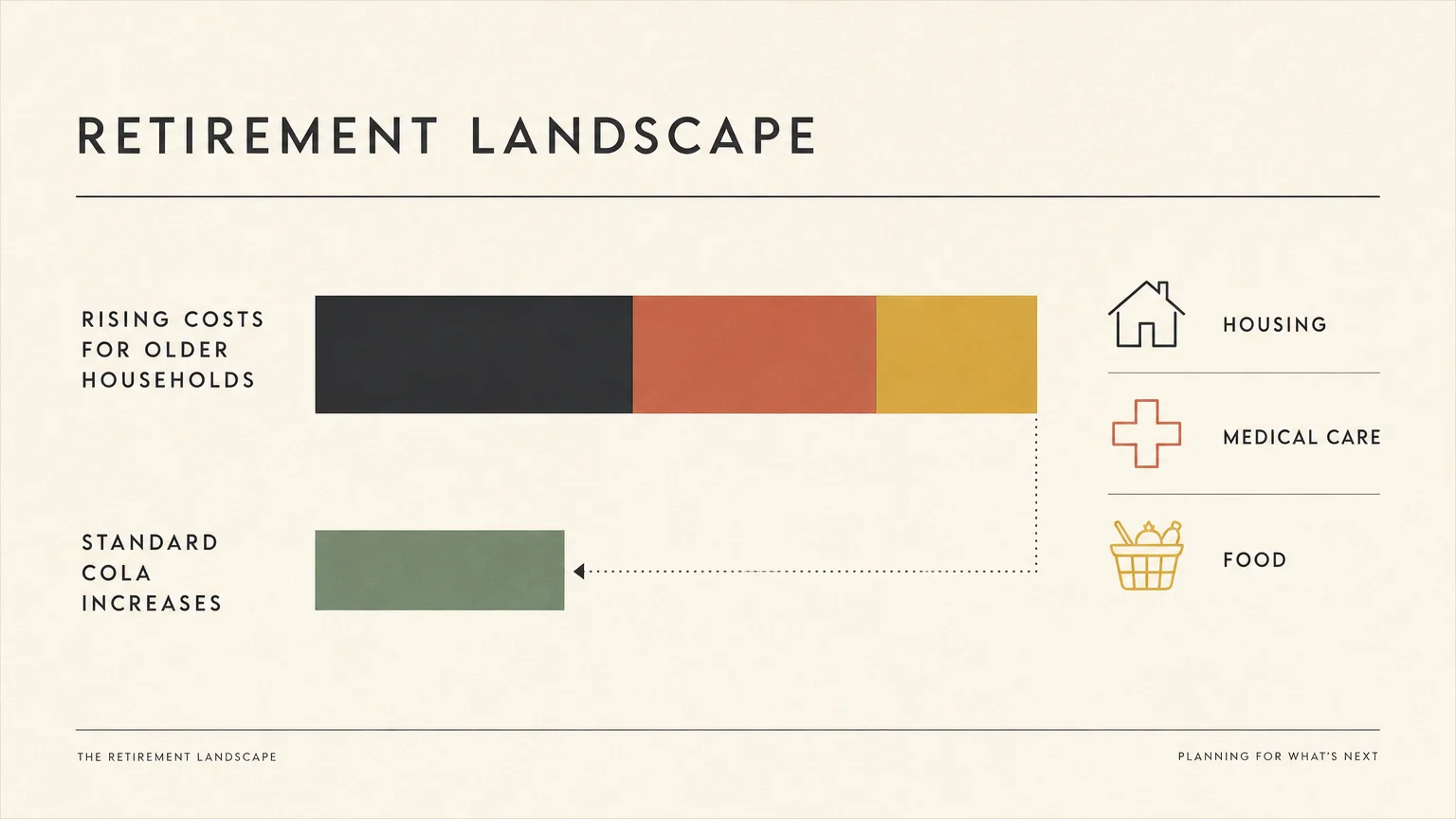

The current economic environment poses complex hurdles for those navigating life after work. With consumer prices fluctuating unpredictably and healthcare expenses continually outpacing standard inflation, maintaining a comfortable standard of living requires immense diligence. Data from the Bureau of Labor Statistics frequently highlights the disproportionate impact of inflation on older households; you spend a significantly larger percentage of your income on medical care, housing, and food compared to younger demographics. While the government provides annual cost-of-living adjustments for social programs, these incremental bumps rarely cover the actual spike in everyday costs.

With guaranteed pensions largely gone, you must fund your own longevity through personal savings and investments. This massive shift in retirement funding demands a highly proactive approach to income management and expense reduction. You must intentionally seek out every available resource to stretch your savings as far as possible. Understanding these economic shifts explains why many retirees feel financially squeezed despite decades of careful planning. Acknowledging this economic reality is the absolute first step toward taking control of your financial destiny, pushing past the stigma of asking for help, and seeking out the supplemental monthly payments you might have overlooked during your initial retirement planning phase.

Income Planning: Unlocking Hidden Government Benefits

Finding hidden sources of monthly income often begins with federal and state assistance programs designed specifically for older adults facing financial headwinds. Supplemental Security Income provides a crucial safety net that many mistakenly assume applies solely to individuals with severe lifelong disabilities. In reality, this program provides direct monthly cash payments to adults aged sixty-five and older who meet specific financial criteria. If your savings run low and your Social Security check falls short, this program offers a vital lifeline. You can use these unrestricted funds to pay for rent, secure nutritious groceries, or cover unexpected minor emergencies.

Beyond direct cash payments, nutritional assistance acts as a incredibly powerful income multiplier for older households. While you might not immediately view food assistance as a direct monthly payment, receiving a dedicated allowance for groceries explicitly frees up hundreds of dollars in your primary checking account each month. Unfortunately, millions of perfectly eligible seniors bypass this highly valuable benefit due to outdated societal stigmas or fears of complex application processes. Fortunately, state governments have drastically modernized their systems; you can now complete most applications securely from the comfort of your living room, and specialized agencies routinely provide free translation services to ensure language barriers never prevent you from securing your rightful benefits. When you decisively reduce your out-of-pocket food expenditures, you immediately increase your discretionary monthly income. To explore these opportunities, utilize comprehensive screening tools provided by the National Council on Aging, which quickly match your financial profile with a wide array of available national and local programs.

Health and Wellness: Navigating Medical Assistance

Healthcare costs consistently consume the largest portion of a fixed retirement budget, making medical assistance an essential pillar of your financial strategy. Medicare Savings Programs offer exceptional, measurable value by paying your Part B premiums on your behalf. By covering this mandatory monthly expense—which often exceeds a hundred and seventy dollars—the program effectively injects that exact dollar amount straight back into your primary retirement check. Depending on your specific income level, certain tiers of this savings program also step in to cover costly deductibles, restrictive coinsurance, and frequent copayments, drastically reducing your total out-of-pocket medical liability throughout the year.

Equally important to your financial health is the Extra Help program, a vital initiative administered by the federal government to assist with Medicare Part D prescription drug costs. Managing chronic physical conditions frequently requires multiple, highly expensive medications; paying full retail price can rapidly drain your carefully accumulated resources. Qualifying for this specific subsidy significantly lowers your monthly premiums and caps your pharmacy copays at easily manageable levels. According to reports from the Social Security Administration, securing this benefit alone is worth an estimated five thousand dollars annually for the average enrolled beneficiary. When you actively secure these medical subsidies, you do much more than balance your household budget; you protect your long-term physical health. Gerontological research consistently demonstrates that seniors who can easily afford their prescribed therapeutic regimens experience far fewer emergency room visits, maintain better mobility, and enjoy a substantially higher quality of life.

Lifestyle Design: Reducing Everyday Expenses

Designing a fulfilling retirement requires freeing up capital so you can thrive and pursue your passions. Housing and utility expenses represent substantial fixed costs that limit your ability to enjoy your golden years. The Low Income Home Energy Assistance Program helps you proactively manage the constantly escalating costs of heating and cooling your residence throughout the year. This federally funded initiative sends payments directly to your designated utility providers, significantly lowering your massive monthly bills and protecting you from devastating seasonal price shocks. Detailed information about this vital public service is highly accessible through the official Office of Community Services portal.

In addition to critical utility support, modern telecommunications subsidies ensure you remain seamlessly connected to your family and medical providers without overpaying for basic internet access. State and municipal governments also frequently offer profound property tax relief explicitly designed for older homeowners. Depending on your jurisdiction, you might qualify for a property tax freeze, which securely locks in your home’s assessed value at a fixed rate, or a senior exemption that immediately slashes your annual tax burden. Because these impactful programs are completely administered locally, engaging with your local tax assessor’s office is imperative. By systematically reducing these everyday overhead expenses, you effectively generate a brand new stream of disposable income. You can enthusiastically redirect these newly found savings toward meaningful travel, engaging hobbies, or creating lasting memories with your beloved family.

Expert Voices on Maximizing Retiree Income

Financial professionals and aging specialists strongly advocate for integrating these supplemental benefits into your broader retirement strategy. Certified financial planners frequently observe retirees draining their investment portfolios unnecessarily because they fail to claim rightful assistance. Leading planners strictly advise treating these assistance programs not as a form of charity, but as strategic components of your overall financial architecture. When you intelligently leverage available public subsidies to cover your basic needs, you actively preserve your private nest egg, allowing your core investments significantly more time to grow, compound, and outpace inflation.

Leading gerontologists also continually highlight the profound psychological benefits of securing concrete financial stability through these targeted monthly payments. Constant worry over diminishing bank balances rapidly accelerates cognitive decline and severely exacerbates stress-related physical illnesses. Experts immersed in the field of aging emphasize that claiming your earned benefits effectively restores a profound sense of personal dignity and daily independence. When you decisively remove the terrible anxiety of choosing between life-saving medication and nutritious groceries, your mental bandwidth immediately expands. Retirees who maximize their eligible financial benefits consistently report much higher levels of daily life satisfaction, better sleep patterns, and far greater community engagement. Listening closely to these professional perspectives strongly reinforces the reality that seeking financial assistance is a remarkably smart, strategically sound move for your long-term holistic well-being.

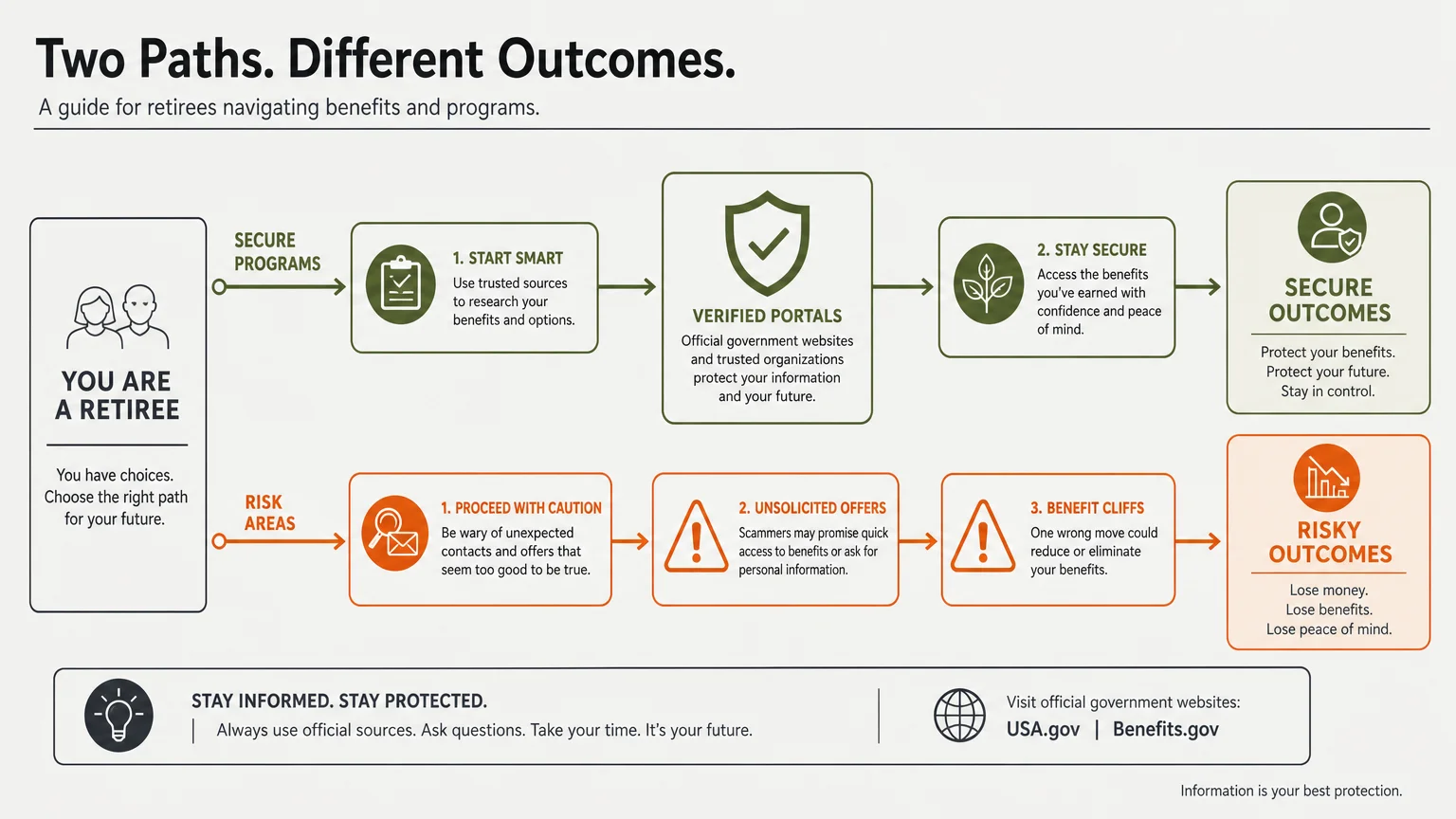

Safeguards: Beware of Scams and Benefit Cliffs

While exploring these monthly payments benefits your budget, you must navigate this terrain with caution and awareness of potential pitfalls. The most significant danger comes from predators seeking to exploit your search for financial relief. Sophisticated scammers routinely masquerade as official government representatives, offering completely fake monthly benefits in direct exchange for your highly sensitive Social Security number, banking details, or an illegal upfront processing fee. You must always remember that legitimate federal agencies will never call you out of the blue to aggressively demand personal information, nor will they threaten you with sudden legal action. If you ever receive a highly suspicious inquiry, hang up your phone immediately and contact the specific agency directly using securely verified phone numbers.

Another critical, yet frequently overlooked, risk involves navigating the dreaded benefit cliff. Many highly valuable assistance programs feature incredibly strict income and asset thresholds. A remarkably slight increase in your documented income—perhaps stemming from a required minimum distribution or a small part-time job—could inadvertently and abruptly disqualify you from thousands of dollars in vital medical or housing subsidies. You must carefully monitor your adjusted gross income and actively consult with a certified tax professional before making any significant financial moves. Deeply understanding these rigid thresholds prevents deeply unexpected disruptions to your carefully planned monthly budget. By remaining constantly vigilant, you can safely maximize your household benefits while vigorously protecting your identity and your assets.

Frequently Asked Questions

Does claiming these monthly payments affect my Social Security retirement benefits?

No; securing assistance through programs like Extra Help or energy subsidies does not reduce your Social Security retirement payments. These specialized programs exist specifically to supplement your primary, fixed income, not to replace or diminish it in any way. You can confidently apply for these various benefits knowing your core retirement funds remain entirely intact and completely unaffected.

How do I know if my household income exceeds the limits for senior assistance?

Income limits vary significantly depending on the program, your state of residence, and your household size. Many robust programs carefully assess your modified adjusted gross income, while others strictly factor in your total liquid assets, including savings accounts and investment portfolios. The most effective way to accurately determine your standing is to use a secure online benefits calculator or schedule an in-person appointment with your local Area Agency on Aging.

Can I complete the applications for these government benefits entirely online?

Yes, the vast majority of federal and state assistance programs now feature highly secure, encrypted online portals that drastically streamline the application process. You can easily upload necessary verification documents, track your application status in real-time, and securely receive official correspondence digitally. However, if you strongly prefer face-to-face assistance or encounter technical difficulties, local community centers and state health departments consistently offer robust in-person support.

Are these supplemental monthly payments considered taxable income by the IRS?

Generally speaking, means-tested assistance programs explicitly designed to help older adults with basic living expenses do not count as taxable income on your annual returns. Benefits like nutritional assistance, energy bill credits, and crucial Medicare premium subsidies are legally exempt from standard federal income tax. However, because national tax laws are highly complex, discussing your specific financial situation with a certified tax advisor actively ensures you remain fully legally compliant.

Take Action For Your Financial Future

You possess the power to reshape your financial landscape and ease the burdens of living on a fixed income. Do not let another stressful month pass by leaving your valuable resources completely untouched. In the next forty-eight hours, commit to making one decisive change; gather your most recent tax return, find a quiet space, and utilize a secure online screening tool to check your eligibility for just one program discussed today. Taking merely fifteen minutes of your time to courageously explore your financial options could easily yield hundreds of dollars in profound monthly savings, granting you the lasting peace of mind and the ultimate financial freedom you truly deserve.