New legislation is actively reshaping how you fund your post-career years, shifting everything from catch-up contribution limits to Medicare out-of-pocket maximums. You might assume your current withdrawal strategy and health coverage are sufficient, but SECURE 2.0 provisions taking effect in 2026 demand immediate attention. Failing to adapt means you risk leaving thousands of tax-advantaged dollars on the table or absorbing surprise prescription costs. By investigating the latest regulatory updates and market shifts, you can protect your nest egg and preserve your peace of mind. We have outlined exactly how to update your income strategies, refine your healthcare choices, and design a purposeful lifestyle so you can leverage these complex government reforms into concrete financial advantages.

A Snapshot of Policy and Market Updates Right Now

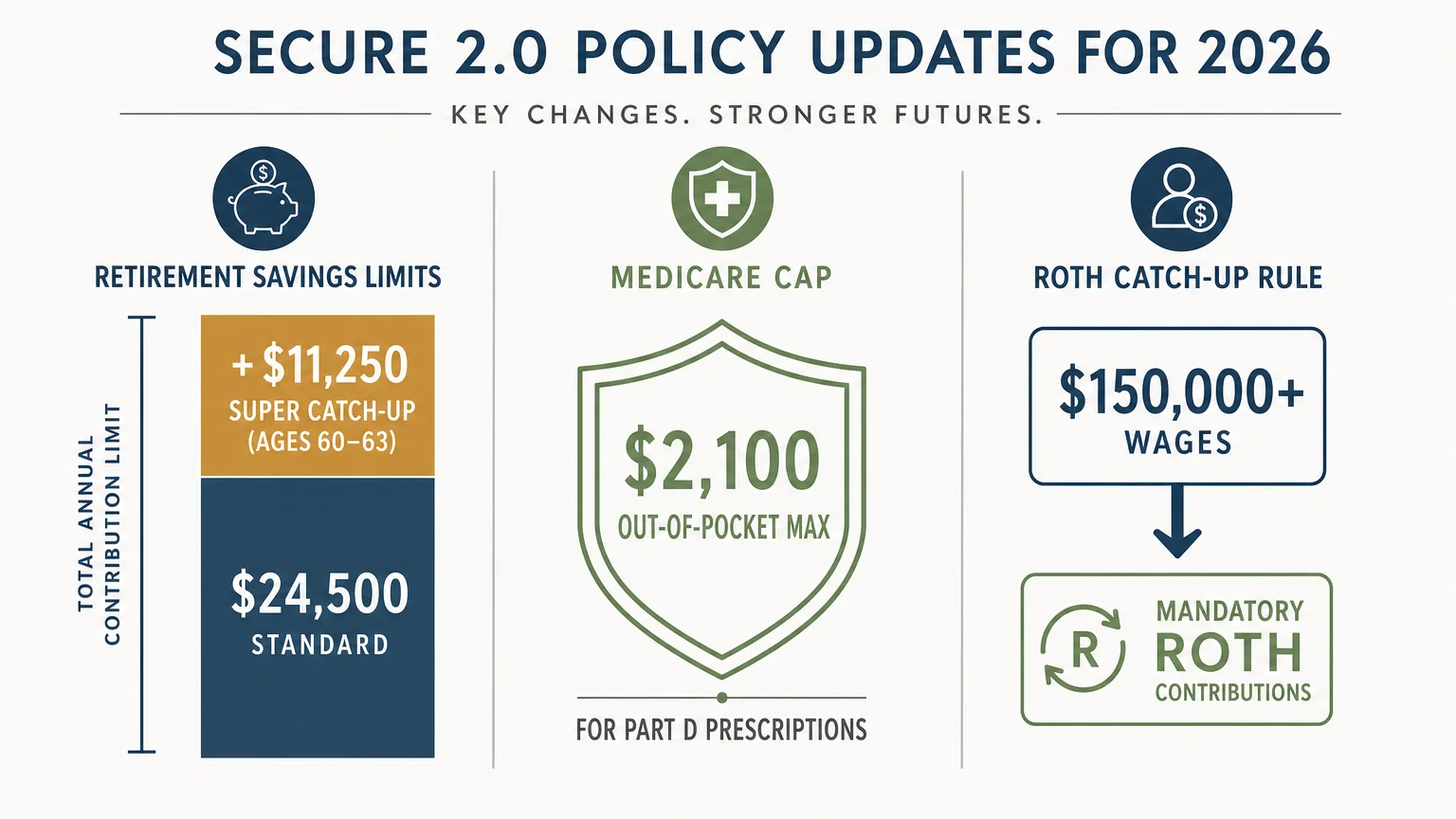

As we navigate 2026, the landscape of post-career finances looks remarkably different than it did just a decade ago. The SECURE 2.0 Act has triggered a cascade of regulatory changes that fundamentally alter how you accumulate and draw down your wealth. Most notably, high earners face a mandatory shift in their savings strategy. If your wages exceeded $150,000 in the previous calendar year with your current employer, you are now required to direct all workplace catch-up contributions into a Roth account. This eliminates the upfront tax deduction many savers historically relied upon to manage their annual tax burdens. Simultaneously, the IRS finalized the standard employee contribution limits for workplace retirement accounts at $24,500. Yet, for individuals traversing the critical ages of sixty to sixty-three, a new super catch-up provision authorizes an additional $11,250 in contributions. This creates an unparalleled opportunity to aggressively stockpile capital during your peak earning years.

On the healthcare front, beneficiaries are experiencing profound cost restructuring that dramatically limits financial exposure. The Medicare Part D out-of-pocket maximum is definitively capped at $2,100 for the year. This legislative ceiling protects those dependent on expensive specialty medications from devastating pharmacy bills, permanently eliminating the catastrophic coverage gaps of the past. Meanwhile, standard Part B deductibles have marginally increased alongside a moderate cost-of-living adjustment from the Social Security Administration. These parallel shifts in tax law, savings caps, and healthcare limits demand that you rigorously recalibrate your monthly cash flow models. Updating your assumptions based on these specific, modern metrics prevents you from making outdated financial decisions that could otherwise derail your long-term security.

Three Strategy Pillars for a Resilient Retirement

Income Planning and Tax Optimization

Navigating the modern tax landscape requires viewing your portfolio not as a single bucket of money, but as distinct tax environments. Because the new Roth mandate forces higher-income individuals to pay taxes upfront on catch-up contributions, you must be increasingly strategic about your overall asset location. Financial experts strongly recommend holding assets with explosive growth potential—such as domestic equities and aggressive index funds—inside your Roth accounts where future gains remain completely shielded from the IRS. Conversely, you should place slower-growing, income-generating assets like corporate bonds and dividend-paying stocks inside your traditional, pre-tax accounts. Furthermore, because required minimum distributions now begin at age seventy-three, you possess a larger runway to execute deliberate Roth conversions during your early sixties. Converting strategic portions of your traditional IRA into a Roth IRA when your earned income temporarily drops can drastically reduce the massive, forced taxable withdrawals you would otherwise face later in life.

Health and Wellness Expense Management

Medical expenses remain one of the most volatile variables in your post-career budget, but new regulations offer enhanced predictability and control. With the Part D out-of-pocket ceiling firmly set at $2,100, you can finally model your maximum annual pharmacy liability with absolute confidence. However, establishing this budget assumes you actively manage your coverage. Insurance carriers continually adjust their medication formularies; a highly effective generic drug covered fully in one year might be suddenly moved to a more expensive pricing tier the next. You must verify your specific prescriptions against official Medicare coverage parameters every single autumn during Open Enrollment. Beyond prescriptions, long-term care financing has received a vital legislative boost. You are now permitted to withdraw up to $2,500 annually from qualified retirement accounts without incurring the standard ten percent early withdrawal penalty, provided those funds are used exclusively to pay for certified long-term care insurance premiums. This empowers you to secure adequate personal care coverage without prematurely depleting your liquid savings.

Lifestyle Design and Purposeful Aging

True wealth encompasses the vitality, purpose, and accessibility you experience daily. Stepping away from the workforce does not require a complete cessation of professional activity; in fact, the concept of phased retirement allows you to dial back your hours while maintaining a crucial sense of identity. Under newly implemented rules, part-time employees who log just five hundred hours a year for two consecutive years are now fully eligible to participate in employer-sponsored retirement plans. You can transition smoothly into consulting, teaching, or administrative roles, supplementing your income while still receiving valuable employer matching funds. When evaluating your living arrangements, focus heavily on accessibility and community infrastructure. Modify your primary residence early by installing grab bars, widening doorways, and eliminating trip hazards so you can safely age in place regardless of unexpected mobility changes. Connecting your physical living space to nearby public transit and robust healthcare networks ensures you never feel isolated or physically trapped as your lifestyle naturally evolves.

Expert Perspectives on Navigating the Transition

Achieving absolute stability during this era of complex reform requires blending precise financial mechanics with behavioral science. Certified Financial Planner professionals consistently emphasize that recent legislation demands a proactive rather than reactive stance on your future tax liabilities. Advisors argue that absorbing a tax hit today through Roth vehicles builds an invaluable reservoir of tax-free liquidity for your eighties and nineties. When you inevitably face an unpredicted medical emergency late in life, pulling fifty thousand dollars from a Roth account will not push you into a higher tax bracket or inadvertently trigger Medicare premium surcharges. Financial planners repeatedly highlight that taxes represent the single largest expense in retirement, making strategic tax deferral and mitigation absolutely paramount.

Gerontologists view these structural financial changes through the lens of cognitive preservation and emotional well-being. Researchers analyzing aging patterns note that individuals who maintain structured societal roles—whether through part-time employment, vigorous volunteer commitments, or structured physical routines—exhibit dramatically lower rates of cognitive decline. Leveraging part-time work to maximize the new employer retirement plan eligibility rules not only bolsters your financial defenses but directly contributes to your neurological health. Real-world accounts reveal that dedicating a few focused hours each November to audit healthcare plans prevents the chronic financial anxiety that frequently plagues older adults. Engaging with Bureau of Labor Statistics data on older workers confirms that staying partially employed is rapidly becoming the statistical norm, blending profound financial pragmatism with proven longevity benefits.

Critical Risks and Safeguards to Watch

As you integrate these evolving government benefits into your master financial plan, you must remain hyper-vigilant against hidden financial penalties and aggressive predatory schemes. The most pervasive invisible threat is the Medicare Income-Related Monthly Adjustment Amount, commonly known as IRMAA. This surcharge acts as a stealth tax on your Part B and Part D premiums, triggered strictly by your modified adjusted gross income. If you withdraw a substantial lump sum from a traditional pre-tax account to purchase a recreational vehicle or fund a major home renovation, that single distribution could artificially inflate your taxable income. Breaching a specific IRMAA threshold by even a single dollar subjects you to significantly higher Medicare premiums for an entire calendar year. You can mitigate this painful benefit cliff by sourcing large capital expenditures from your Roth accounts or spreading traditional distributions strategically across multiple tax years.

Concurrently, the rollout of new federal adjustments spawns a fresh wave of highly sophisticated criminal activity. Fraudsters are intimately aware of the SECURE 2.0 provisions and the Medicare out-of-pocket caps. Criminals frequently contact older Americans posing as federal representatives, aggressively claiming they must issue you a modernized 2026 healthcare card to maintain your coverage. They rely heavily on fear and urgency to extract your sensitive banking information. Criminals utilize advanced spoofing technology to make caller identification screens display official government acronyms. The government will never call you unprompted to request personal identification numbers or demand immediate payments. Safeguard your identity by establishing secure digital profiles with the Social Security Administration annual adjustments portal to monitor your actual communications. Always freeze your credit files with the major reporting bureaus, and if you receive a suspicious inquiry, hang up immediately.

Frequently Asked Questions About Recent Reforms

Do I have to make Roth catch-up contributions if my salary is below the threshold?

If your wages from a single employer fell below the $150,000 threshold in the preceding calendar year, you retain full flexibility over your catch-up contributions. You can choose to direct those funds into a traditional pre-tax bucket, effectively reducing your current taxable income, or you can opt for Roth contributions. The mandatory Roth requirement strictly targets high earners based on their prior year FICA wages. Checking your specific guidance provided by the Internal Revenue Service ensures you stay compliant with the protocols your human resources department must enforce.

Will the new Medicare out-of-pocket maximum cover my medical office visits?

It is vital to distinguish clearly between your pharmacy benefits and your broader medical insurance. The $2,100 out-of-pocket ceiling applies exclusively to Medicare Part D, which strictly covers the prescription drugs you pick up at a retail pharmacy or order via a mail delivery service. This cap does not apply to Medicare Part B services, which encompass standard doctor visits, outpatient surgeries, and physician-administered medications like certain chemotherapy infusions. You must still account for standard Part B deductibles and coinsurance when budgeting for clinical treatments.

Can I withdraw from my retirement account to pay for long-term care insurance?

Yes, recent legislative adjustments created a highly specific safe harbor for long-term care planning. You can withdraw up to $2,500 annually from a qualified retirement plan to pay for certified long-term care premiums without facing the ten percent early withdrawal penalty normally applied to individuals under age fifty-nine and a half. While you still owe standard federal and state income taxes on a pre-tax distribution, eliminating the punitive early fee makes funding these protective policies significantly easier for early retirees.

How does the new super catch-up provision work for people in their early sixties?

The super catch-up rule is an age-targeted mechanism designed to accelerate wealth accumulation right before traditional retirement age. If you are aged sixty, sixty-one, sixty-two, or sixty-three in 2026, you can contribute an additional $11,250 on top of your standard workplace retirement limit. Once you turn sixty-four, the limit automatically reverts to the standard catch-up amount for those aged fifty and older. This brief four-year window offers a spectacular opportunity to rapidly expand your nest egg when your earning power is likely peaking.

Take Action Today

Reading about legislative updates provides essential foundational knowledge, but true financial security requires immediate, decisive implementation. You hold the absolute power to shape your economic reality by leveraging these complex reforms rather than simply letting them happen to you. Your financial trajectory will not improve through passive observation; it requires engaging directly with your benefit portals and tax professionals to systematically realign your strategies. Open your computer, log into your employer benefits dashboard or the federal Medicare portal, and verify your contribution designations and health coverages. Reviewing your AARP policy tracking resources alongside your personal financial statements will clarify exactly where you stand today. Make a commitment to execute one tangible adjustment in the next forty-eight hours—whether that means increasing your deferral rate to hit the super catch-up limit, scheduling a meeting with a fiduciary planner to discuss proactive Roth conversions, or independently verifying the specific pricing tier status of your medications. Taking direct control today guarantees you can step into your post-career years with enduring confidence and unshakeable financial clarity.