As you cross the threshold into retirement, the financial game changes entirely. You transition from accumulating assets over several decades to distributing those assets in a sustainable, strategic manner. The current economic landscape—marked by fluctuating inflation rates, shifting tax policies, and unpredictable market volatility—exposes a critical retirement income gap for many seniors. You must adapt your financial strategy to protect your purchasing power while navigating incredibly complex government rules. Making investment mistakes retirees typically fall for can jeopardize the nest egg you worked so hard to build. Senior investing errors often stem from a lack of proactive planning rather than poor stock picking. You need a comprehensive strategy to avoid bad investments and ensure long-term financial safety well into your later years.

Creating a bulletproof retirement income plan requires you to coordinate your Social Security benefits, pension payouts, portfolio withdrawals, and healthcare spending. A misstep in one area creates a ripple effect that can trigger higher taxes and deplete your principal balance faster than anticipated. By identifying and avoiding the most common pitfalls, you can protect your wealth and enjoy the peace of mind you deserve.

Income Alignment and Withdrawal Pitfalls

1. Fumbling Your Social Security Timing

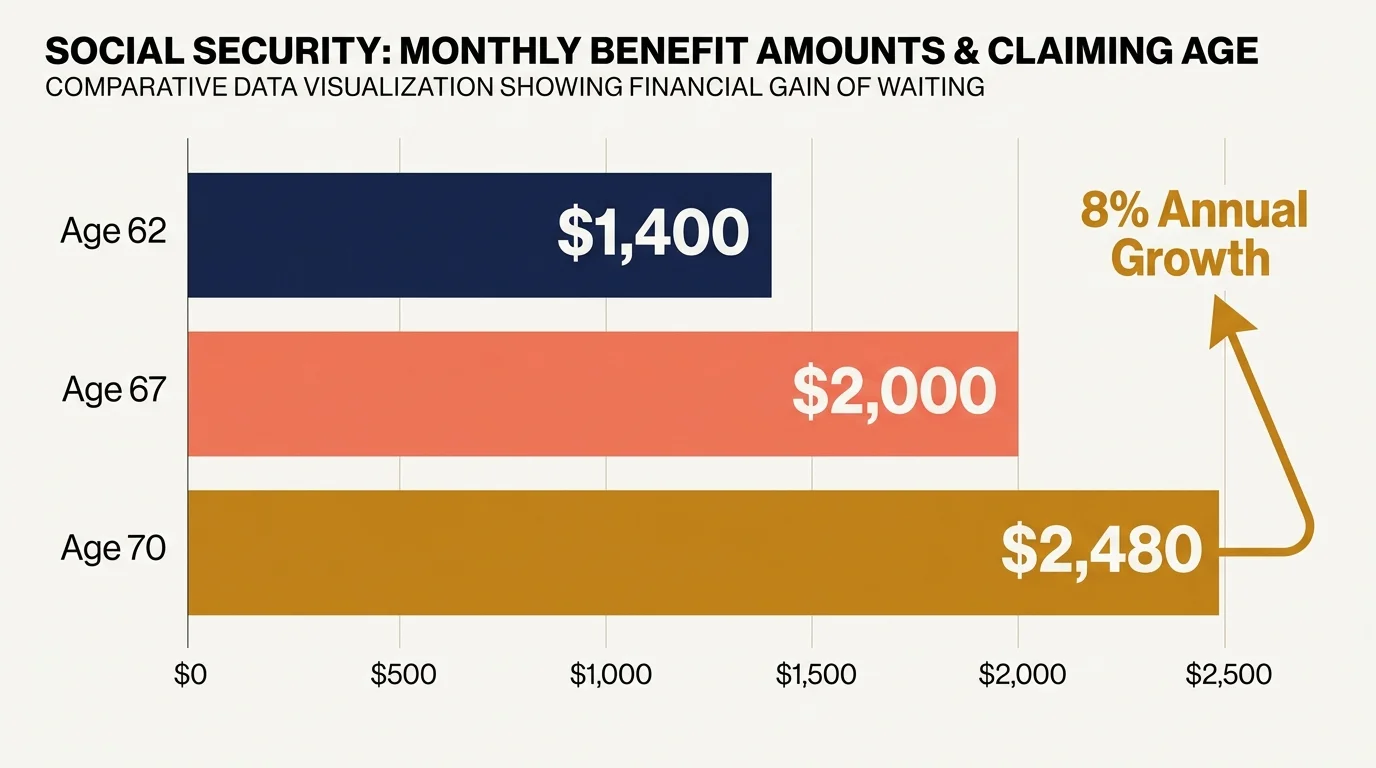

You might feel tempted to claim your Social Security benefits as soon as you turn 62; however, doing so locks in a permanently reduced monthly payout. Many retirees claim early out of fear that the system will run out of money, ultimately sacrificing hundreds of thousands of dollars over a typical twenty-year retirement. The math heavily favors patience for those in good health. If your primary insurance amount at your full retirement age of 67 is $2,000 per month, claiming at 62 slashes your benefit to just $1,400. Conversely, waiting until age 70 allows your benefit to grow by 8 percent annually through delayed retirement credits, bringing your monthly check to a robust $2,480. This guaranteed, inflation-adjusted income stream forms the bedrock of your retirement security.

You must evaluate your break-even point to determine the optimal claiming age. This calculation compares the total cumulative benefits of claiming early versus delaying. Generally, if you live past your early eighties, waiting until age 70 maximizes your lifetime payout. You should always review the official Social Security Administration guidelines to understand how your specific birth year impacts your full retirement age. Because these decisions are largely irrevocable after the first twelve months, always consult a licensed financial professional for individualized advice before locking in your claiming strategy.

2. Ignoring the Tax Impact of Your Withdrawal Strategy

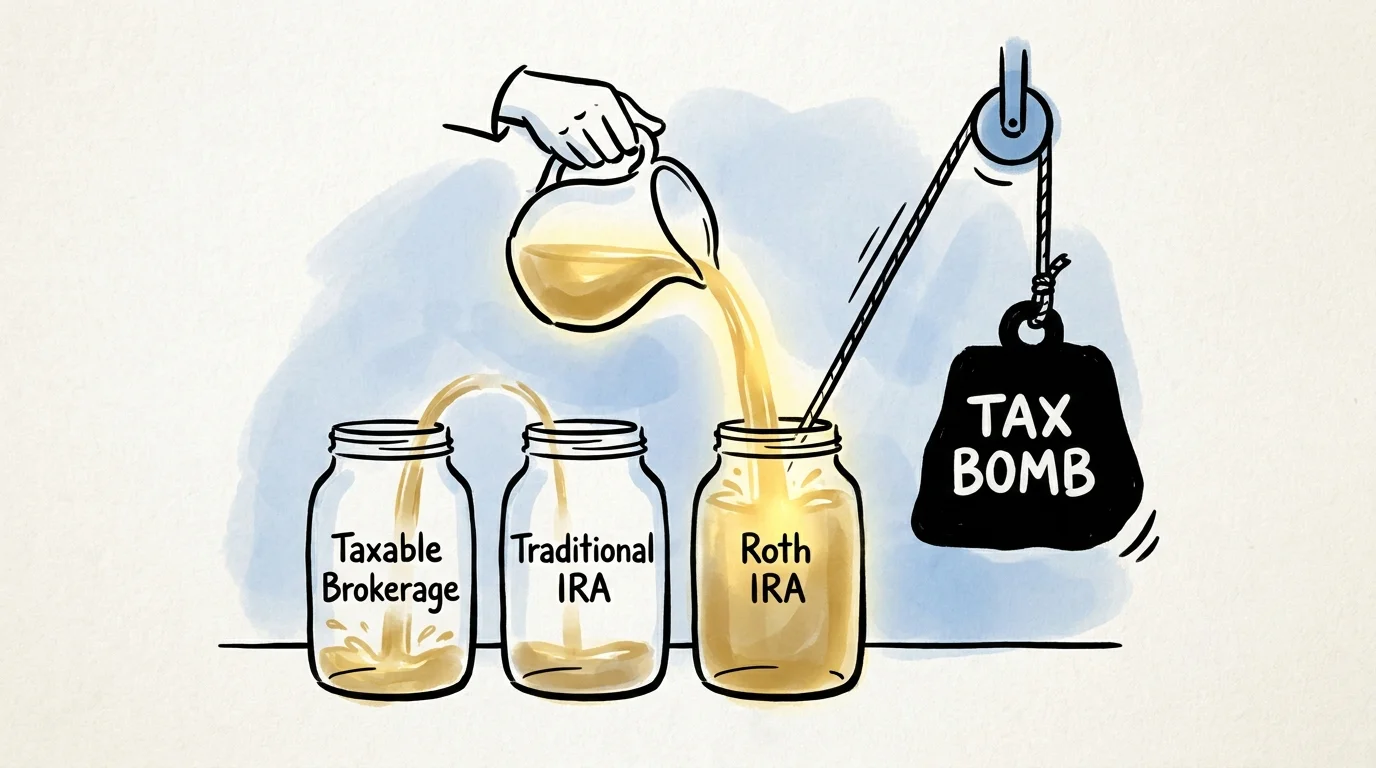

Retirees often withdraw funds randomly from various accounts without considering the severe tax consequences. When you reach age 73, the government mandates that you begin taking withdrawals from your traditional IRAs and 401(k)s. These forced distributions are taxed as ordinary income and can unexpectedly push you into a significantly higher marginal tax bracket. If you rely solely on tax-deferred accounts for your early retirement years, you are setting yourself up for a massive tax bomb later in life.

You can mitigate this risk by implementing a tax-efficient withdrawal sequence. A common strategy involves pulling income from taxable brokerage accounts first, allowing your tax-deferred and tax-free Roth accounts more time to compound. Alternatively, you might consider executing strategic Roth conversions during the low-income years between your retirement date and the onset of your required minimum distributions. By converting traditional IRA funds to a Roth IRA, you pay taxes at your current, lower rate and secure tax-free growth for the rest of your life. Always review the Internal Revenue Service distribution rules to ensure you do not miss deadlines, as the penalty for failing to take a mandated distribution is steep.

Tax Strategy and Healthcare Cost Management

3. Triggering Unnecessary Medicare Premium Surcharges

The Income-Related Monthly Adjustment Amount, commonly known as IRMAA, acts as a hidden tax on successful retirees. When your modified adjusted gross income crosses specific thresholds, your Medicare Part B and Part D premiums skyrocket. The government uses your tax return from two years prior to determine your premium tier; therefore, your income at age 63 directly dictates your Medicare costs at age 65. Retirees who fail to plan for this two-year lookback period often receive a nasty surprise in the mail.

Capital gains from a major portfolio rebalance, a large real estate sale, or a massive traditional IRA withdrawal can easily push your income over the IRMAA limits. You must project your income carefully and manage your capital gains to stay just below these threshold brackets. If you recently experienced a life-changing event—such as retiring and losing your primary salary—you can file Form SSA-44 to request a reduction in your income-related adjustment. Understanding Medicare premium guidelines prevents you from accidentally surrendering thousands of dollars to unnecessary surcharges.

4. Underestimating Out-of-Pocket Healthcare and Long-Term Care Costs

Assuming Medicare will cover all your medical expenses represents a catastrophic financial error. Medicare provides excellent coverage for hospital stays and doctor visits, but it explicitly does not pay for custodial care. If you suffer a cognitive decline or a physical ailment that requires a stay in an assisted living facility or full-time nursing home, you must pay those bills out of pocket. In many parts of the country, specialized memory care or private nursing facilities cost well over $100,000 per year.

You must build a dedicated healthcare buffer into your investment strategy. If you retire before age 65 and use a high-deductible health plan, fully funding a Health Savings Account offers a triple-tax advantage: your contributions are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses remain tax-free. For long-term care needs, consider exploring hybrid insurance policies that combine a death benefit with long-term care riders. This approach ensures that if you never need the care, your heirs still receive a financial benefit, eliminating the “use it or lose it” risk associated with traditional policies.

Risk Management and Portfolio Protection

5. Failing to Balance Portfolio Risk Against Inflation

Many retirees panic during market downturns and move their entire portfolio into cash or highly conservative bonds. While this eliminates stock market volatility, it exposes you to an equally destructive force: inflation. Over a twenty-year retirement, even a modest 3 percent annual inflation rate will decimate your purchasing power. An item that costs $50,000 today will cost nearly $90,000 in twenty years. If your investments are locked in low-yield certificates of deposit that fail to outpace inflation, you are mathematically guaranteed to lose buying power over time.

Conversely, taking on too much risk exposes you to sequence of returns risk. If the stock market drops 20 percent during your first year of retirement and you simultaneously withdraw 5 percent for living expenses, your portfolio takes a devastating 25 percent hit from which it may never recover. You must strike a delicate balance by utilizing a bucket strategy. Keep one to two years of living expenses in liquid cash, allocate the next five years to stable fixed-income instruments, and invest the remainder in diversified equities for long-term growth. Rely on unbiased Securities and Exchange Commission asset allocation resources to help structure a resilient portfolio.

6. Falling Victim to High Fees and Predatory Sales Pitches

Every dollar paid in excessive investment fees is a dollar permanently removed from your retirement income stream. Wall Street often pushes complex, high-commission products—such as certain variable annuities or non-traded real estate investment trusts—that prioritize the advisor’s boat payment over your financial security. A seemingly harmless 2 percent annual fee can devour hundreds of thousands of dollars in potential growth over a multi-decade retirement.

You must rigorously audit your investment expenses. Ask your advisor for a transparent breakdown of their management fees, fund expense ratios, and any hidden trading costs. Furthermore, you must verify the credentials of anyone offering you financial advice. Always use a free financial professional background check to ensure your advisor has a clean disciplinary record. Demand to work strictly with fiduciaries—professionals legally bound to place your financial interests above their own profit motives. If an investment opportunity sounds too good to be true, it is almost certainly a scam designed to separate you from your life savings.

7. Neglecting Beneficiary Designations and Estate Basics

An outdated beneficiary form operates as a ticking time bomb for your heirs. A beneficiary designation on a 401(k), IRA, or life insurance policy is a legally binding contractual agreement that completely supersedes the instructions written in your last will and testament. If you finalize a flawless estate plan with your attorney but forget to remove an ex-spouse from an old employer-sponsored retirement account, your ex-spouse will legally inherit those funds regardless of your current wishes.

You must implement a routine schedule to review and update your designations after any major life event, including marriages, divorces, births, and deaths. Additionally, you should establish Transfer on Death or Payable on Death designations for your standard bank accounts and taxable brokerage accounts. This simple administrative step allows your assets to bypass the expensive and time-consuming probate process, ensuring your surviving spouse or children gain immediate access to funds to cover funeral expenses and ongoing living costs.

Frequently Asked Questions

Will part-time work reduce my Social Security benefits?

Working part-time during retirement offers a fantastic way to stay socially engaged and supplement your income, but it can temporarily impact your Social Security checks if you claim early. If you collect benefits before reaching your full retirement age, the government applies an earnings test. For every two dollars you earn above a specific annual limit, the Social Security Administration withholds one dollar of your benefits. Once you reach your full retirement age, this earnings limit disappears entirely, and you can earn an unlimited amount of money without facing any benefit reductions. Furthermore, the government recalculates your benefit at your full retirement age to slowly credit back the amounts they previously withheld.

What investments offer the best protection against inflation?

To combat the silent wealth-destroyer that is inflation, you must own assets that naturally appreciate in value or provide rising income streams over time. High-quality, dividend-paying stocks serve as an excellent primary defense; companies that consistently raise their dividends provide an increasing cash flow that helps offset rising grocery and energy costs. Treasury Inflation-Protected Securities also play a vital role in a conservative portfolio, as their principal value adjusts upward in tandem with the Consumer Price Index. Finally, maintaining exposure to real estate—either through physical property or broadly diversified Real Estate Investment Trusts—provides a traditional hedge, as property values and rental incomes generally rise alongside broader economic inflation.

How can I determine if my financial advisor fees are too high?

You evaluate your advisor’s compensation by comparing their value proposition against industry benchmarks. The traditional assets under management model typically charges around 1 percent annually for portfolios up to one million dollars, with the percentage decreasing as your wealth grows. If you are paying 1.5 percent or more without receiving comprehensive financial planning, tax strategy, and estate coordination, you are drastically overpaying. You should also scrutinize the underlying expense ratios of the mutual funds and exchange-traded funds inside your portfolio; these should ideally average below 0.50 percent. Consider exploring advisors who charge a flat annual retainer or an hourly rate if you simply need a portfolio check-up without ongoing management.

How should a surviving spouse handle inherited investments?

The death of a spouse represents a profound emotional trauma, and rushing into massive financial changes during a period of grief often leads to irreversible mistakes. Your immediate focus should be securing short-term cash flow and gathering all necessary documentation, including multiple copies of the death certificate. From an investment standpoint, a surviving spouse generally has the unique right to roll an inherited IRA directly into their own name, treating the funds as if they originally belonged to them. Additionally, taxable brokerage accounts receive a step-up in basis upon death, wiping out previous capital gains taxes on appreciated stock. You should pause, gather your trusted financial and tax advisors, and map out a revised income plan before liquidating any major assets.

Securing Your Financial Legacy

Taking control of your retirement income plan requires continuous monitoring and proactive adjustments. The financial landscape shifts daily, and a strategy that worked perfectly five years ago may expose you to unnecessary risks today. You must review your monthly bank and brokerage statements meticulously to identify hidden fees, ensure your asset allocation aligns with your risk tolerance, and confirm your beneficiary designations reflect your current wishes. Do not wait for a market crash or an unexpected medical bill to test the resilience of your portfolio. Take action today by organizing your financial documents, mapping out your tax liabilities, and scheduling a comprehensive portfolio review with a licensed fiduciary to guarantee your golden years remain truly golden.