For decades, the financial services industry has sold workers on the idea of a single, magical retirement savings goal. You might have heard that you need exactly one million dollars—or perhaps two million—to safely leave the workforce and enjoy your golden years. This fixation on a static number is dangerously flawed because it completely ignores the dynamic nature of your personal spending, the biting reality of inflation, and the complex web of taxation that awaits you in retirement. The truth is that a comfortable retirement is less about hitting an arbitrary net worth target and more about engineering a reliable, tax-efficient stream of income that can weather varying economic climates. As you shift from the accumulation phase of your working years to the distribution phase of retirement, your entire financial philosophy must adapt.

A significant policy shift is currently forcing future retirees to reevaluate their senior finance planning. Increasing longevity paired with legislative changes—such as the gradual increase of the Social Security full retirement age and the shifting rules surrounding inherited retirement accounts—means you carry more personal responsibility for your financial security than any previous generation. The widening gap between guaranteed fixed income and the actual cost of modern living requires a proactive approach. You cannot simply cross your fingers and hope your portfolio survives; you must actively manage your assets to ensure they outlast you.

Determining how much you need to retire requires you to define your specific lifestyle costs and then build an income bridge to cover them. You must factor in daily living expenses, travel aspirations, potential healthcare shocks, and the hidden costs of aging. By stripping away the generalized advice and focusing on concrete data, you can build a customized US retirement strategy that prioritizes income stability, minimizes tax leakage, and protects your wealth against unforeseen risks. This comprehensive approach transforms a vague hope for the future into a mathematically sound financial reality.

Structuring Your Retirement Income Floor

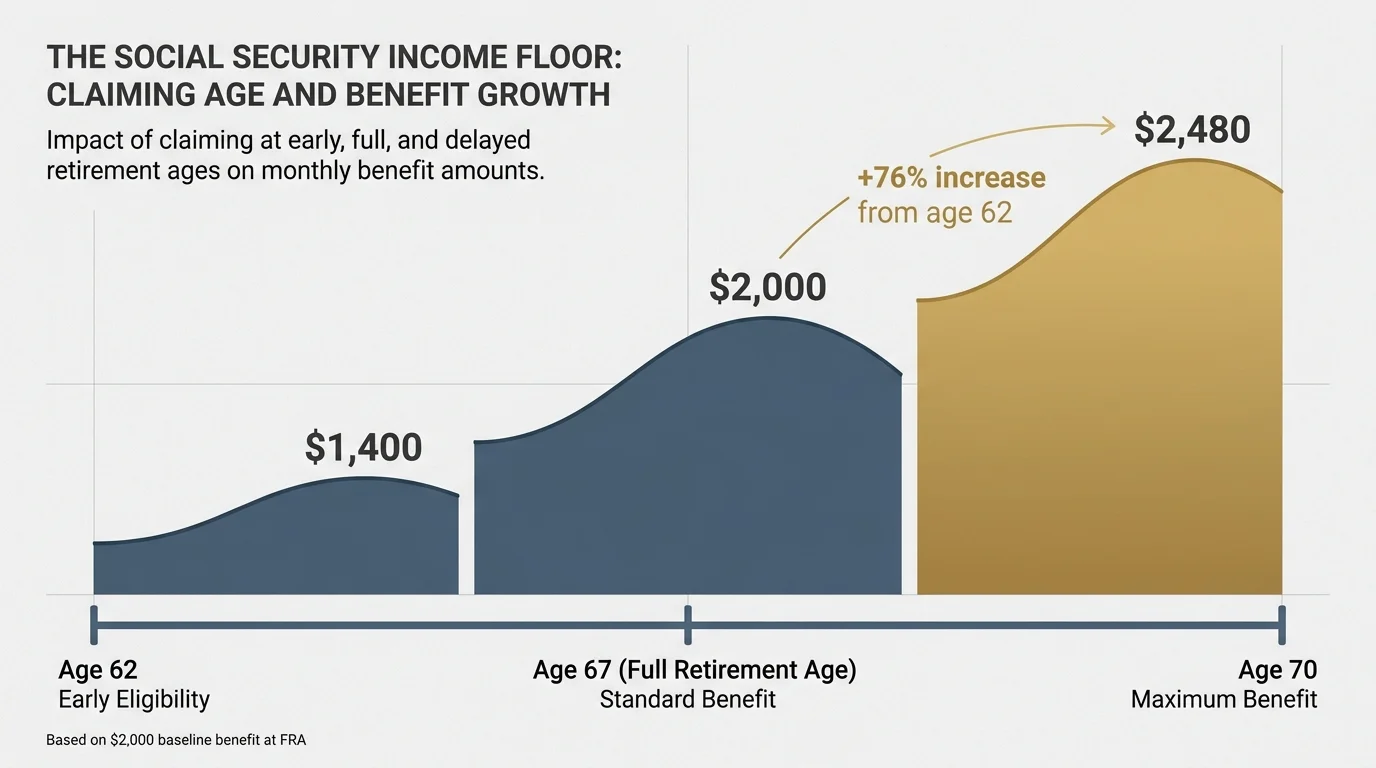

The foundation of any successful retirement strategy is your guaranteed income floor. This floor represents the steady stream of cash you can rely on regardless of what the stock market does on any given day. For the vast majority of Americans, this begins with Social Security. The age at which you choose to claim your benefits is perhaps the most consequential financial decision of your life. While you can claim benefits as early as age sixty-two, doing so permanently reduces your monthly payout. Conversely, delaying your claim until age seventy earns you delayed retirement credits, increasing your base benefit by eight percent for every year you wait past your full retirement age.

Consider a practical math example to illustrate this magnitude. If your full retirement age is sixty-seven and your expected monthly benefit is two thousand dollars, claiming at sixty-two would reduce that check to roughly one thousand four hundred dollars. Waiting until age seventy would boost that exact same benefit to two thousand four hundred and eighty dollars per month. That represents a permanent seventy-six percent increase in your baseline guaranteed income, which also carries a higher cost-of-living adjustment moving forward. You can verify your specific projections by utilizing the Social Security Administration calculators to test different claiming scenarios. Because these decisions are irrevocable after a narrow window, you should discuss your individual life expectancy and spousal benefit strategies with a licensed professional before filing.

Beyond Social Security, pensions and annuities can help solidify your income floor. If you are fortunate enough to possess a traditional defined-benefit pension, you must carefully evaluate the survivorship options. Selecting a single-life payout will yield the highest monthly check, but it leaves your surviving spouse with nothing upon your death; a joint-and-survivor option reduces your initial payout while providing crucial longevity protection for your partner. For those without pensions, commercial annuities can mathematically manufacture an income floor. By trading a lump sum of your portfolio for a guaranteed monthly check, you transfer the longevity risk from your own shoulders to an insurance company. However, annuities are complex contracts embedded with fees and surrender charges, making it imperative to seek objective, fiduciary guidance before locking up your liquidity.

Once your guaranteed income floor is established, your investment portfolio must cover the remaining gap. The historical standard for portfolio withdrawals has long been the four percent rule, which suggests you can safely withdraw four percent of your portfolio in year one and adjust that dollar amount for inflation every subsequent year. Under this model, a five hundred thousand dollar portfolio would generate twenty thousand dollars in your first year of retirement. While this is a helpful baseline, modern financial planning requires a more dynamic approach. Sequence of return risk—the danger of experiencing a major market downturn early in your retirement—can decimate a portfolio if you blindly withdraw a fixed percentage. An adaptable strategy, where you trim your discretionary spending during bear markets and harvest gains during bull markets, offers a much higher probability of sustained success.

Navigating Taxes and Healthcare Costs

It is a common misconception that your tax burden vanishes once you stop working; in reality, tax planning becomes significantly more complicated in retirement. During your career, your tax rate was dictated by your salary. In retirement, your tax bracket is dictated by which accounts you choose to pull money from. A thoughtless withdrawal strategy can easily push you into a higher marginal tax bracket and trigger unnecessary taxes on your Social Security benefits. To combat this, you must categorize your assets into three distinct tax buckets: taxable brokerage accounts, tax-deferred accounts like traditional IRAs and 401(k)s, and tax-free accounts like Roth IRAs.

A highly effective, tax-efficient strategy involves drawing down your taxable accounts first, allowing your tax-deferred and tax-free accounts to enjoy longer periods of compound growth. However, this strategy is interrupted by legislative mandates known as Required Minimum Distributions. Current tax law dictates that once you reach age seventy-three—or seventy-five, depending on your birth year—you are legally forced to withdraw a specific percentage from your tax-deferred accounts annually, whether you need the money or not. Failure to take these distributions results in steep penalties. You can review the exact tables and timelines via the IRS guidelines on Required Minimum Distributions. By utilizing Roth conversions during your early retirement years—when your income is typically lower—you can systematically drain your pre-tax accounts, thereby reducing the size of your future forced distributions and controlling your lifelong tax liability.

Healthcare expenses represent another massive, often unpredictable drain on retirement savings. Medicare is a lifeline for seniors, but it is absolutely not free. Your monthly premiums for Medicare Part B and Part D are directly tied to your modified adjusted gross income through a surcharge known as the Income-Related Monthly Adjustment Amount. The federal government looks at your tax return from two years prior to determine your current premium; a sudden spike in income—perhaps from selling a piece of real estate, executing a large Roth conversion, or taking a massive required minimum distribution—can catapult you into a higher premium bracket. To understand the specific thresholds that could trigger these surcharges, you should familiarize yourself with the Medicare official cost guidelines.

Health Savings Accounts offer a unique, stealthy advantage for managing these inevitable medical costs. If you funded a Health Savings Account during your working years, that money grows completely tax-free and can be withdrawn tax-free to cover qualified medical expenses, including Medicare premiums, out-of-pocket deductibles, and co-pays. Unlike flexible spending accounts, this money rolls over year after year. Deploying these funds strategically allows you to cover healthcare shocks without inflating your taxable income, thereby shielding you from unexpected premium surcharges and preserving the longevity of your core investment portfolio.

Protecting Your Wealth and Legacy

Accumulating a healthy retirement nest egg is only half the battle; defending that wealth from external threats is equally critical. The most glaring threat to senior finance is the exorbitant cost of long-term care. Medicare does not cover custodial care, such as assistance with bathing, dressing, or eating, nor does it cover extended stays in assisted living facilities. With the national average for a private room in a nursing home hovering around nine thousand dollars per month, an extended healthcare crisis can bankrupt a healthy portfolio in a matter of years. You must confront this risk head-on by exploring long-term care insurance, hybrid life insurance policies, or purposefully earmarking a substantial portion of your portfolio as a self-funded healthcare reserve.

Beyond medical costs, seniors are disproportionately targeted by financial fraud and sophisticated scams. Protecting your wealth requires a high degree of vigilance and a healthy dose of skepticism. You should freeze your credit across the major bureaus, monitor your financial statements diligently for unauthorized charges, and establish trusted contacts with your financial institutions. When evaluating financial products or seeking advice, always verify the credentials and disciplinary history of the professionals you interact with using tools like FINRA BrokerCheck. Ensuring your advisors are legally bound to act as fiduciaries prevents you from being sold expensive, commissioned products that benefit the broker rather than your retirement plan.

Finally, your retirement strategy is incomplete without a robust estate plan. Estate planning is not solely for the ultra-wealthy; it is a fundamental act of care for the people you leave behind. At a minimum, your protective framework should include a finalized will, a durable power of attorney for financial matters, and an advance healthcare directive. You must also routinely audit the beneficiary designations on your retirement accounts, life insurance policies, and bank accounts. Beneficiary designations supersede the instructions in your will, meaning an outdated form could accidentally send your life savings to an ex-spouse rather than your current family. Engaging an estate planning attorney ensures your assets bypass the costly, public probate process and transfer smoothly to your chosen heirs.

Frequently Asked Questions

How does part-time work affect my Social Security benefits?

Working a part-time job in retirement can provide immense psychological benefits and valuable supplemental income, but it requires careful navigation of the Social Security earnings test. If you claim your benefits before reaching your full retirement age and continue to earn wages, the government will temporarily withhold one dollar in benefits for every two dollars you earn above a specific annual limit. It is critical to understand that this withheld money is not permanently confiscated. Once you reach your full retirement age, the Social Security Administration will recalculate your monthly benefit upward to account for the months your payments were reduced. However, if you wait until your full retirement age to claim, the earnings test disappears entirely, allowing you to earn an unlimited salary while collecting your full benefit.

What are the best ways to hedge against inflation in retirement?

Inflation silently destroys your purchasing power, making a static pile of cash highly dangerous over a two-decade retirement. To protect your lifestyle, your portfolio must generate returns that outpace the rising cost of goods. Dividend-paying equities are a historically reliable inflation hedge; fundamentally strong companies tend to increase their prices as costs rise, subsequently passing those increased profits back to shareholders through growing dividends. Additionally, you should consider Treasury Inflation-Protected Securities, which are government bonds whose principal value automatically adjusts upward based on changes in the Consumer Price Index. Maintaining a diversified mix of growth-oriented stocks and inflation-adjusted bonds ensures your income continues to stretch just as far in year twenty as it did in year one.

How do I know if I am paying too much in financial advisor fees?

Understanding exactly how your financial advisor is compensated is essential to preserving your wealth. Advisors typically operate under one of three models: commission-based, fee-based, or fee-only. Commission-based brokers earn money by selling you specific financial products, creating an inherent conflict of interest. A fee-only fiduciary advisor charges a transparent percentage of the assets they manage, an hourly rate, or a flat retainer fee, and they are legally obligated to place your financial interests ahead of their own. A standard benchmark for assets under management is roughly one percent per year. If your total investment expenses—including the advisor’s fee and the internal expense ratios of your mutual funds—exceed one and a half percent, you are likely sacrificing too much of your compounding growth. You can educate yourself on standard fee structures through Investor.gov resources.

How do we prepare for the financial impact when one spouse passes away?

The death of a spouse is emotionally devastating, and it frequently triggers a harsh financial reality known as the widow’s penalty. When one partner dies, the surviving spouse is allowed to step into the larger of the two Social Security checks, but the smaller check vanishes permanently. This results in an immediate reduction in total household income. Simultaneously, the surviving spouse must now file their taxes as a single taxpayer rather than married filing jointly. Because the income brackets for single filers are significantly compressed, the surviving spouse often ends up paying a higher effective tax rate despite having less overall income. Comprehensive senior finance planning anticipates this transition by strategically funding tax-free Roth accounts and securing adequate life insurance while both partners are still healthy.

Your Next Steps to Secure Your Future

You cannot put your retirement income planning on autopilot. Achieving a comfortable, stress-free retirement requires ongoing adjustments as tax laws evolve, markets fluctuate, and your personal goals shift. Take control of your financial trajectory today by gathering your most recent investment statements, logging into your Social Security portal to verify your projected benefits, and auditing your current withdrawal rate against your actual living expenses. It is never too late to optimize your strategy. Take the initiative to schedule a comprehensive check-in with a fee-only fiduciary advisor and a qualified tax professional to ensure your wealth is structured efficiently, protected from unnecessary taxation, and primed to support the retirement lifestyle you have worked so hard to build.

2 Responses

XQItgPQRHoLgnSaKCV

FJUKQzplBHAvCxNABP