The transition from earning a predictable paycheck to generating your own retirement income represents the most significant financial shift of your life. At the center of this transition sits a permanent, irrevocable decision that dictates the foundation of your financial security for decades. Choosing when to take Social Security involves far more than simply circling a date on the calendar; it requires a comprehensive understanding of actuarial math, tax implications, and your personal longevity expectations. Far too many retirees file for benefits on their sixty-second birthday out of fear—fear that the government will slash benefits, or fear that they will leave money on the table if they experience an early mortality. However, looking closely at the data reveals that this fear-based approach often creates a massive income gap late in life precisely when healthcare costs peak and cognitive decline makes managing complex portfolios more difficult. By shifting your perspective and treating your Social Security benefit as guaranteed longevity insurance rather than a standard investment account you must drain quickly, you can optimize your retirement income timing and protect yourself against the risk of outliving your money.

Aligning Your Income Streams for Maximum Impact

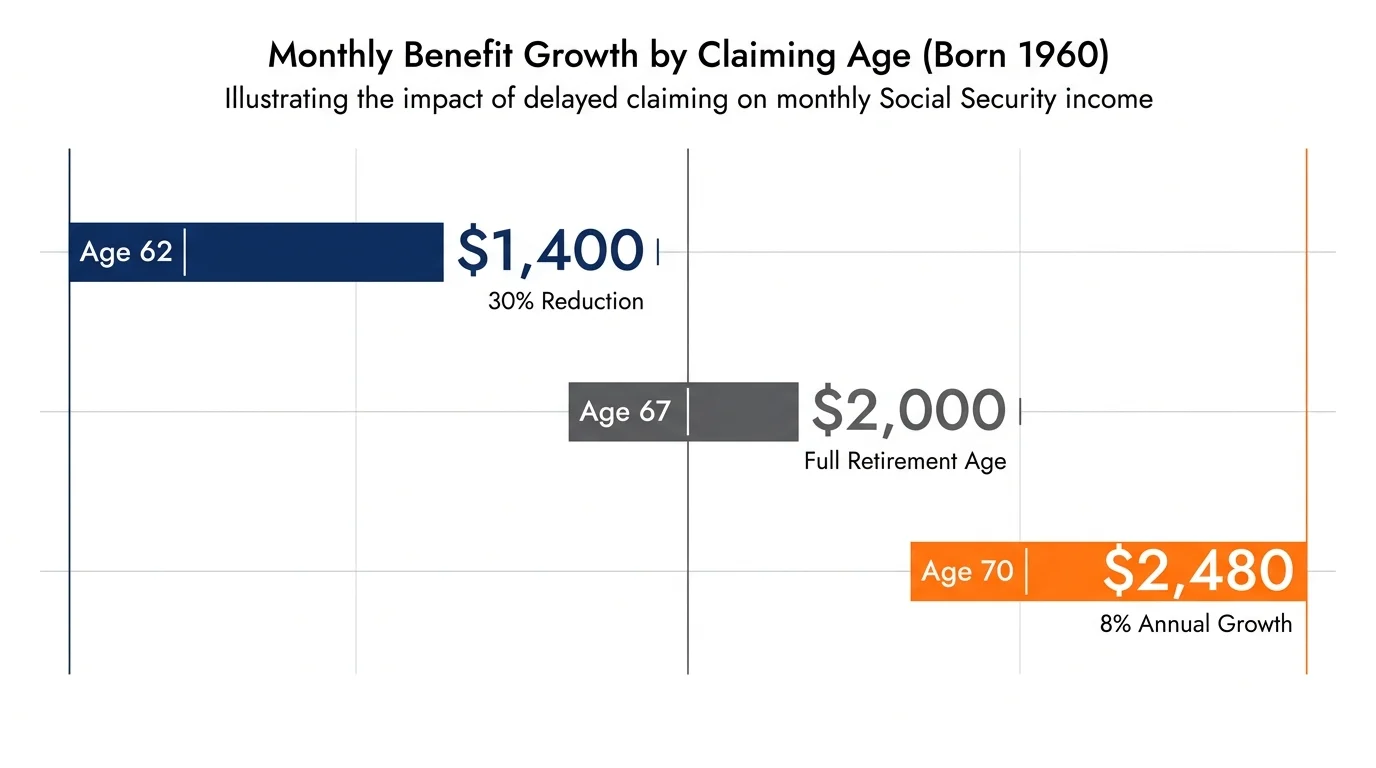

You must evaluate your SSA strategy within the broader context of your entire financial portfolio. Pinpointing the best age SSA beneficiaries should target requires balancing guaranteed government income with portfolio withdrawals, pension distributions, and annuity payments. The mathematical reality of the Social Security system heavily rewards patience. If you were born in 1960 or later, your Full Retirement Age stands at sixty-seven. Claiming at age sixty-two results in a permanent thirty percent reduction in your monthly benefit. Conversely, for every year you delay beyond your Full Retirement Age up to age seventy, your benefit grows by a guaranteed eight percent per year through delayed retirement credits. This means a primary insurance amount of two thousand dollars at age sixty-seven shrinks to fourteen hundred dollars if claimed at sixty-two, but swells to two thousand four hundred and eighty dollars if deferred to age seventy. While these figures illustrate the clear mathematical advantage of waiting, you must consult a licensed financial professional to determine how this baseline interacts with your specific tax brackets and longevity expectations.

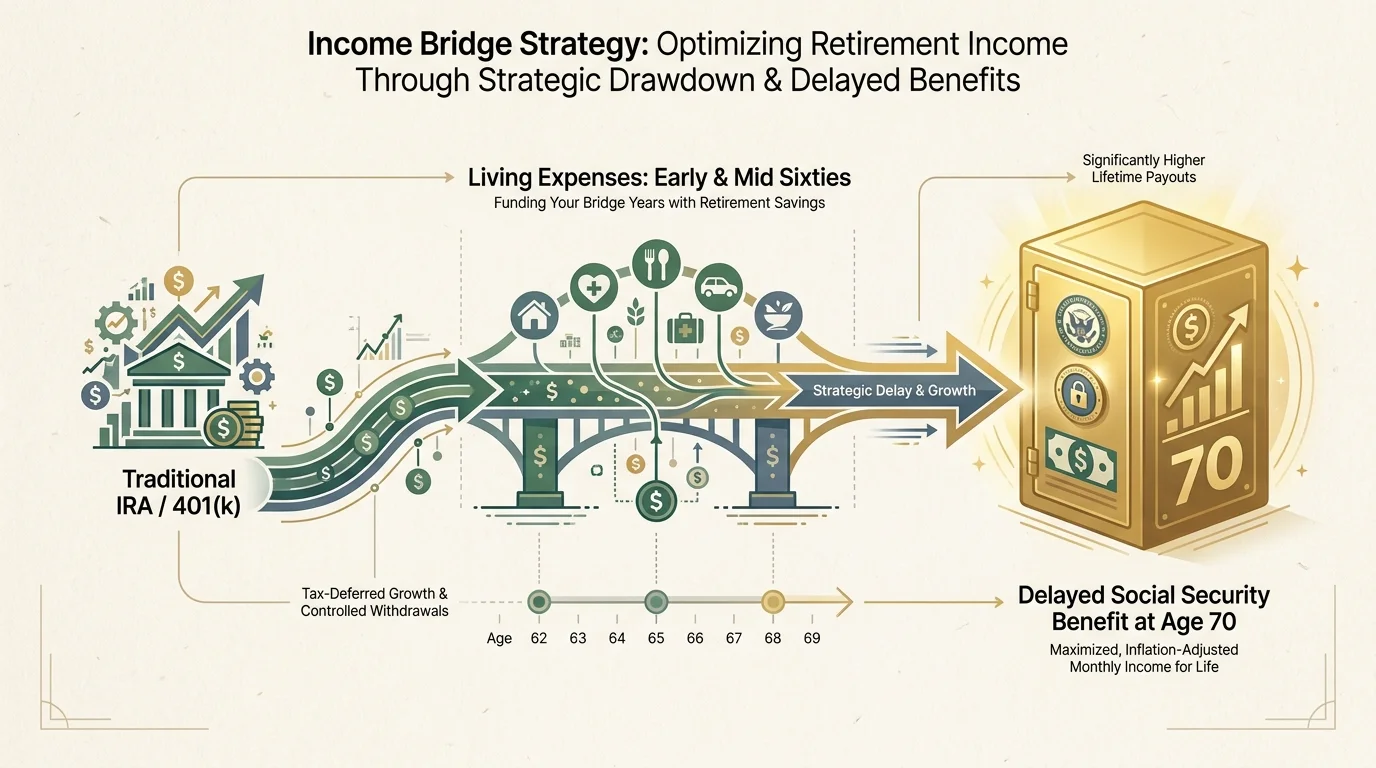

To capture these delayed retirement credits, you might need to employ an income bridge strategy. A bridge strategy involves withdrawing funds from your pre-tax retirement accounts—such as your traditional IRA or workplace 401(k)—during your early and mid-sixties to cover your living expenses while you choose to delay social security benefits. While drawing down your portfolio early might feel counterintuitive, replacing variable market withdrawals later in life with a higher guaranteed, inflation-adjusted government check dramatically reduces your sequence of returns risk. A higher fixed income baseline later in retirement allows you to invest your remaining portfolio more aggressively or simply sleep better at night knowing market crashes will not threaten your ability to buy groceries or pay utility bills.

If you hold a traditional pension or a commercial annuity, you possess additional tools to structure your income timeline. You can coordinate these fixed payments to start immediately upon retirement, reducing the pressure on your investment portfolio while you wait to claim Social Security. Always review the survivorship options on your pensions and annuities. Choosing a single-life payout on a pension might yield a higher monthly check today, but it leaves your surviving spouse highly vulnerable if you pass away first. Balancing your immediate cash flow needs against the long-term security of your household requires running precise projections and understanding how each income stream behaves under various market and mortality scenarios.

Navigating Taxes and Healthcare Costs

Your retirement strategy must account for the silent wealth destroyers: taxes and healthcare expenses. The timing of your Social Security claim profoundly impacts your lifetime tax liability. The Internal Revenue Service taxes up to eighty-five percent of your Social Security benefits based on a formula called provisional income, which includes your adjusted gross income, nontaxable interest, and half of your Social Security benefit. By utilizing the income bridge strategy mentioned earlier, you systematically drain your pre-tax IRA balances during your sixties when your taxable income might be unusually low. Accelerating these withdrawals at a lower marginal tax bracket prevents massive, forced withdrawals later in life.

The federal government mandates that you begin taking Required Minimum Distributions from your pre-tax accounts when you reach your early seventies. If you arrive at age seventy-three with millions of dollars sitting in traditional IRAs alongside a maximum Social Security benefit, the resulting forced distributions will push you into a devastatingly high tax bracket. This phenomenon, often referred to as the tax torpedo, causes every additional dollar of IRA withdrawal to trigger taxes on another eighty-five cents of your Social Security benefit, effectively doubling your marginal tax rate on those withdrawals. Proactive tax planning in your sixties neutralizes this threat.

Healthcare costs require equally rigorous planning. Medicare premiums are not static; they fluctuate based on your income from two years prior. If your Required Minimum Distributions or capital gains distributions spike your modified adjusted gross income, you will face the Medicare Income-Related Monthly Adjustment Amount, or IRMAA. This surcharge can easily add thousands of dollars to your annual Medicare premium costs. Smoothing your income through careful withdrawal sequencing helps you avoid tripping these costly IRMAA thresholds.

If you possess a Health Savings Account, you hold one of the most powerful tax-advantaged tools available for retirement healthcare. Health Savings Accounts offer a triple-tax advantage: contributions go in tax-free, growth occurs tax-free, and distributions remain completely tax-free when used for qualified medical expenses. Once you transition to a fixed retirement income, you can deploy these funds to cover Medicare premiums, deductibles, and out-of-pocket medical costs without generating any taxable income that might trigger the tax torpedo or IRMAA surcharges.

Protecting Your Wealth and Securing Your Legacy

Maximizing your income and minimizing your taxes mean nothing if you fail to protect your wealth from catastrophic risks and predatory threats. Long-term care costs represent the most significant variable expense in retirement. The majority of retirees will require some form of assisted living or in-home care during their final years, and standard Medicare does not cover custodial care. You must decide whether to self-fund this risk using your investment portfolio or transfer the risk to an insurance company through a traditional long-term care policy or a hybrid life insurance product. A robust, delayed Social Security benefit serves as an excellent defense against long-term care costs, providing a high baseline of monthly cash flow to help pay for home health aides or facility fees.

Protecting your wealth also demands extreme vigilance against financial exploitation. Scammers increasingly target retirees with sophisticated phishing schemes, identity theft, and fraudulent investment pitches. Establishing your personal profile on the Social Security Administration portal early prevents identity thieves from filing a fraudulent claim on your earnings record. Always verify the credentials of financial professionals through regulatory databases and maintain a healthy skepticism toward any investment promising high returns with zero risk; government resources dedicated to protecting your investments from fraud outline exactly how to spot and avoid these catastrophic schemes.

Securing your legacy requires updating your estate plan to reflect your current reality. A foundational estate plan includes a last will and testament, a durable power of attorney for finances, and an advance healthcare directive. You must routinely audit the beneficiary designations on your retirement accounts, life insurance policies, and brokerage accounts. Transfer-on-death and payable-on-death designations supersede the instructions written in your will. If you finalized your divorce a decade ago but forgot to update the beneficiary form on your primary IRA, your ex-spouse will inherit those assets regardless of what your current will dictates. Aligning your legal documents with your actual intentions ensures a smooth transfer of wealth to your heirs.

Frequently Asked Questions on SSA Strategy and Retirement Income

Can I claim Social Security while working part-time?

You can claim benefits while continuing to work, but doing so before you reach your Full Retirement Age exposes you to the earnings test. If you earn more than the annual limit established by the Social Security Administration, the government will withhold one dollar in benefits for every two dollars you earn above that threshold. Once you reach your Full Retirement Age, the earnings test disappears entirely, allowing you to earn an unlimited amount of income without facing any benefit withholding. The withheld funds are not permanently lost; the administration recalculates your benefit at your Full Retirement Age to account for the months you did not receive a check, but the temporary reduction can disrupt your cash flow significantly.

How does Social Security act as an inflation hedge?

Social Security represents the ultimate inflation hedge in your retirement portfolio because it includes an annual Cost of Living Adjustment tied to the Consumer Price Index. Unlike fixed pension payments or standard bond yields that lose purchasing power as prices rise, your Social Security benefit mechanically adjusts to keep pace with economic inflation. By delaying your claim to age seventy, you apply these percentage-based cost of living increases to a much larger base number, compounding your protection against inflation over the decades.

How do I evaluate the fees charged by financial professionals?

Understanding exactly how your advisor earns money protects your portfolio from excessive drag. You should prioritize working with a fee-only fiduciary who legally commits to placing your financial interests ahead of their own profit margins. Advisors typically charge a percentage of assets under management—often around one percent annually—or they charge a flat hourly fee for comprehensive financial planning. You can utilize directories focused on finding a fiduciary financial planner to identify professionals who provide transparent fee structures. Avoid advisors who earn hidden commissions by selling complex, proprietary mutual funds.

How does my claiming strategy affect my surviving spouse?

Your claiming timeline directly determines the financial security of your surviving partner. When one spouse passes away, the surviving spouse inherits the larger of the two Social Security checks received by the household, while the smaller check disappears entirely. If you served as the primary breadwinner and you claim your benefit early at age sixty-two, you permanently lock in a reduced survivor benefit for your spouse. By delaying your claim to age seventy, you guarantee that your surviving partner will receive the maximum possible monthly income for the rest of their life.

Take Control of Your Retirement Strategy Today

Securing a comfortable, anxiety-free retirement demands decisive action and continuous oversight. You possess the power to shape your financial future by moving beyond guesswork and anchoring your decisions in hard data. You must build a comprehensive timeline that illustrates exactly how your portfolio withdrawals, tax liabilities, and Social Security benefits interact over the decades. Schedule a deep-dive check-in with a trusted, fee-only fiduciary to stress-test your assumptions against historical market data and evolving tax legislation. Taking the time to optimize your strategy today ensures that your wealth serves your life, rather than the other way around.