The year 2026 brings an unprecedented wave of financial changes for retirees. The cost of living has shifted, healthcare premiums are rising, and the expiration of the Tax Cuts and Jobs Act means the income tax landscape looks entirely different than it did just a year ago. If you rely on a retirement budget built on outdated assumptions, you risk draining your portfolio prematurely or overpaying the federal government. You need a proactive spending plan that factors in the newly announced 2.8 percent Social Security cost-of-living adjustment, shifting Medicare surcharges, and shrinking standard tax deductions. Creating a retirement budget that actually works in 2026 requires more than simply tracking your grocery bills; it demands a strategic alignment of your income streams, tax liabilities, and risk management protocols.

Aligning Your Income Streams for the Year Ahead

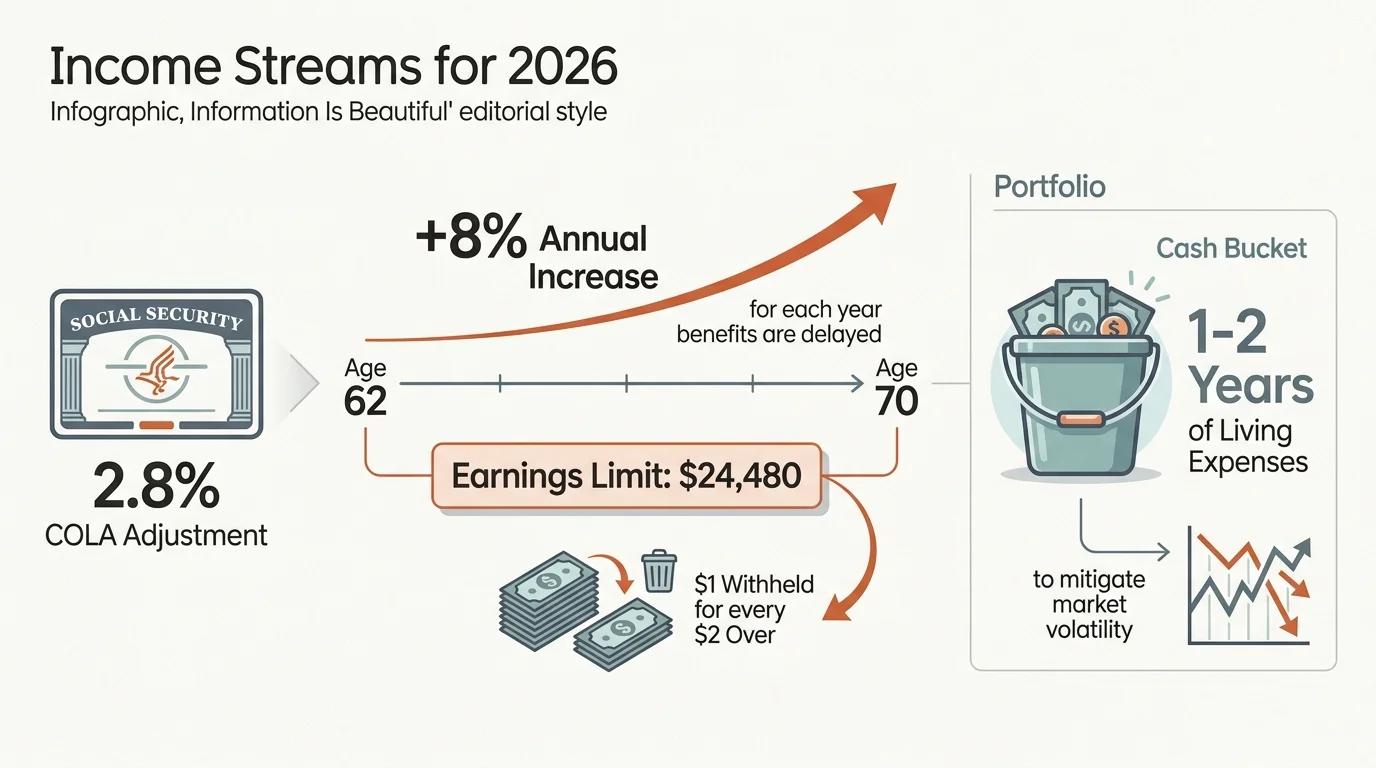

Timing Social Security Decisions

The 2026 cost-of-living adjustment increases Social Security benefits by 2.8 percent, offering a needed buffer against rising household expenses. However, maximizing this income stream depends heavily on your exact age and your ongoing employment status. If you claim benefits before reaching your full retirement age and continue to work part-time, the earnings limit for 2026 restricts you to $24,480 in wage income. The government withholds one dollar in benefits for every two dollars you earn above that specific threshold. You must consult the Social Security Administration to review your earnings record and determine your break-even point before turning on your monthly payments. Waiting until age 70 guarantees an eight percent annual increase in your base benefit amount, but this delay strategy only works if you hold sufficient portfolio assets to bridge the temporary income gap.

Navigating Pension Options and Annuities

If you hold a corporate or government pension, you face the critical decision of taking a lump sum or accepting a lifetime monthly payout. A monthly annuity payment provides a fixed income floor, which shields you from stock market volatility and guarantees a paycheck for life. However, inflation quietly erodes the purchasing power of fixed payments over a twenty-year retirement. Taking a lump sum gives you total control over the principal, allowing you to invest for long-term growth. The mathematical choice depends entirely on the underlying interest rates used to calculate your lump sum and your personal longevity expectations. Always evaluate these irreversible payout elections alongside a licensed fiduciary who can model the long-term impact on your surviving spouse.

Portfolio Withdrawals and the Four Percent Rule Debate

Generating your own paycheck from an investment portfolio requires abandoning rigid withdrawal frameworks. The traditional four percent rule assumes you adjust your withdrawal amount for inflation every single year, regardless of underlying market performance. In the economic environment of 2026, dynamic withdrawal strategies protect your principal far better. When the stock market experiences a severe downturn, you should skip your inflation adjustment or temporarily reduce your withdrawal rate to avoid locking in permanent losses. You achieve this flexibility by maintaining a cash reserve holding one to two years of living expenses. This cash bucket gives your equity investments time to recover without forcing you to sell shares at a massive discount. Check the official investor education materials provided by the Securities and Exchange Commission to understand how sequence of returns risk can devastate an otherwise healthy portfolio.

Mastering Tax Changes and Healthcare Strategy

The TCJA Sunset and Tax-Efficient Withdrawals

The expiration of the Tax Cuts and Jobs Act at the end of 2025 drastically alters the mathematics of retirement withdrawals. In 2026, the top federal income tax bracket reverts from 37 percent to 39.6 percent, and the lower brackets compress, pushing more of your middle-class income into higher marginal tax rates. Furthermore, the standard deduction shrinks by roughly half, meaning you will pay taxes on a significantly larger portion of your retirement income. You must sequence your account withdrawals strategically to mitigate this tax spike. Drawing exclusively from a pre-tax traditional IRA can trigger a massive tax bill. Blending your withdrawals across taxable brokerage accounts, tax-deferred IRAs, and tax-free Roth accounts allows you to control your adjusted gross income and keep your overall tax liability manageable.

Mandatory Withdrawals and SECURE 2.0

The federal government eventually demands its share of your tax-deferred retirement accounts. Under the rules implemented by the SECURE 2.0 Act, the required minimum distribution age remains at 73 for the 2026 tax year. If you turn 73 this year, you must take your first mandatory withdrawal by April 1 of the following year. Missing this deadline triggers a harsh 25 percent penalty on the exact amount you failed to withdraw. You can reduce this penalty to 10 percent if you correct the mistake quickly, but proactive planning eliminates the risk entirely. Check the official guidelines published by the Internal Revenue Service to calculate your required distribution amount based on your life expectancy factor and your December 31 account balance from the prior year. Additionally, be aware of new SECURE 2.0 catch-up contribution rules in 2026; if you earned over $145,000 in the prior year and want to make catch-up contributions to your workplace plan, the law forces you to direct those funds into an after-tax Roth account.

Medicare IRMAA and Healthcare Costs

Your healthcare budget requires precise income management because Medicare premiums directly correlate with your tax returns from two years prior. The standard Medicare Part B premium for 2026 stands at $202.90 per month. However, if your modified adjusted gross income from 2024 exceeds $109,000 as a single filer or $218,000 as a married couple filing jointly, you will face an Income-Related Monthly Adjustment Amount. This surcharge cliff is unforgiving; a single dollar over the threshold pushes you into the first tier, adding hundreds of dollars to your annual healthcare costs. The highest brackets can push your monthly Part B premium up to $689.90. To fund out-of-pocket medical expenses efficiently, maximize your Health Savings Account if you remain on an eligible high-deductible health plan before enrolling in Medicare. The 2026 contribution limit reaches $4,400 for individuals and $8,750 for families, plus a $1,000 catch-up contribution if you are 55 or older.

Protecting Your Wealth and Securing Your Legacy

Funding Long-Term Care Needs

A realistic retirement budget must account for the high probability of needing extended custodial care. The Medicare program covers acute hospital stays and limited skilled nursing rehabilitation, but it completely ignores the cost of daily custodial assistance in an assisted living facility or at home. Relying solely on your investment portfolio to fund a sudden hundred-thousand-dollar annual care bill can devastate a surviving spouse. You should explore hybrid life insurance policies featuring long-term care riders or purchase dedicated traditional care policies. These financial instruments provide a leveraged pool of tax-free money specifically earmarked for health events, protecting your core retirement assets from rapid depletion.

Fraud Prevention and Shielding Assets

Protecting your nest egg from sophisticated financial scams remains a mandatory component of modern retirement planning. Cybercriminals and fraudulent investment promoters specifically target seniors controlling large retirement balances. You must routinely monitor your credit reports and freeze your credit files at the major bureaus to prevent identity theft. When evaluating new investment opportunities, verify the credentials of the financial advisor through the Financial Industry Regulatory Authority database. Never wire funds to unverified offshore accounts, and always maintain distinct, strong passwords for your primary financial institutions. Your budget survives only if your underlying principal remains secure from bad actors.

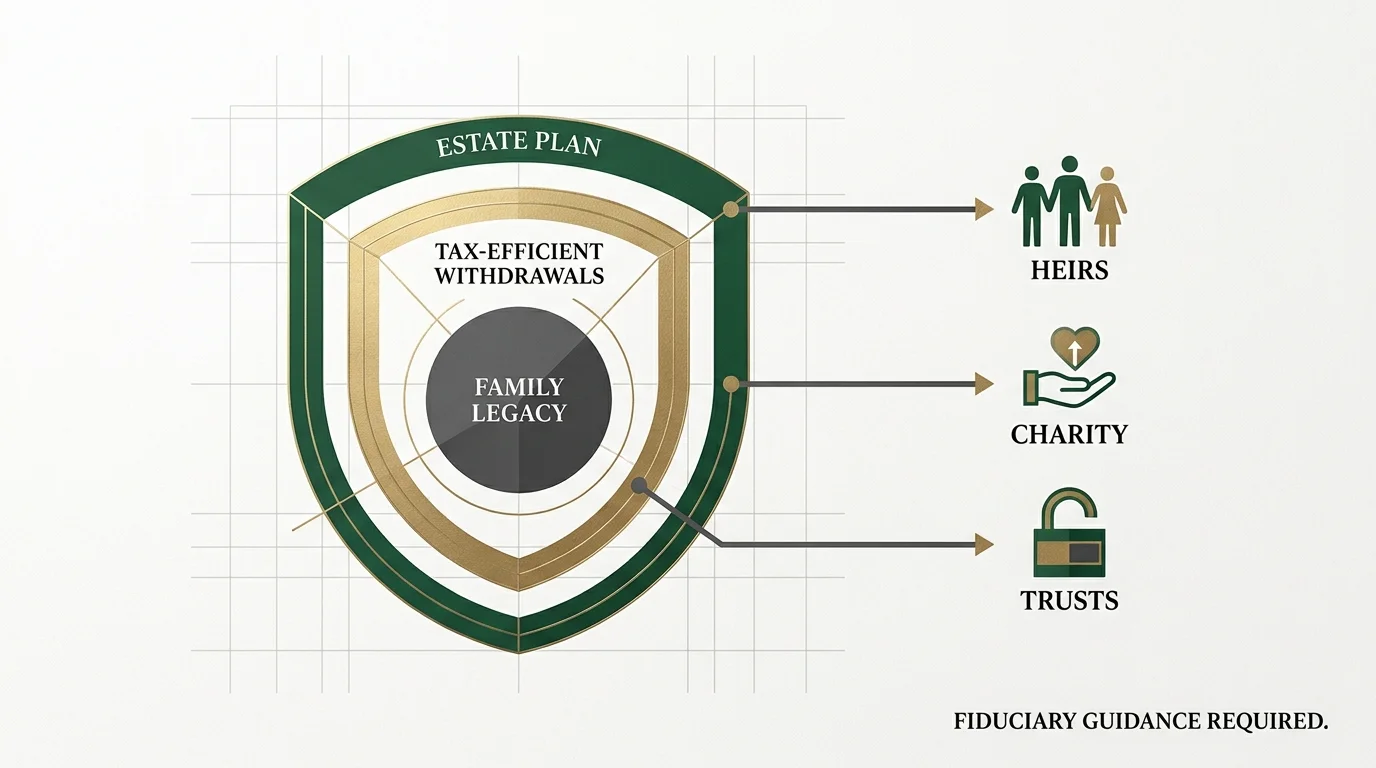

Estate Basics Before the Exemption Drops

The shifting tax code in 2026 carries massive implications for the financial legacy you leave behind. With the sunsetting of recent tax laws, the lifetime estate and gift tax exemption drops by approximately fifty percent, landing near $7.25 million for individuals and $14.5 million for married couples. If your home equity, retirement accounts, and life insurance death benefits push your total net worth above these thresholds, your heirs could face a 40 percent federal estate tax. You must review your beneficiary designations across all accounts immediately; these direct designations legally override your written will. Schedule a comprehensive review with a qualified estate attorney to draft a revocable living trust, update your durable power of attorney, and shield your legacy from unnecessary taxation and probate delays.

Frequently Asked Questions

Does part-time work affect my Social Security benefits?

Yes, but only if you claim benefits before reaching your full retirement age. In 2026, the government imposes an earnings limit of $24,480. If your wages exceed this exact amount, your benefits face a temporary reduction. The Social Security Administration holds back one dollar for every two dollars you earn above the limit. Once you reach your full retirement age, you can earn an unlimited amount of money without any penalty applied to your monthly check.

How do I hedge my retirement budget against inflation now?

You must maintain a diversified portfolio that includes growth-oriented equities, as stocks historically outpace inflation over long horizons. Additionally, consider allocating a portion of your fixed-income portfolio to Treasury Inflation-Protected Securities or Series I Savings Bonds. Adjusting your discretionary spending downward during years of unusually high inflation also preserves your vital purchasing power.

Are financial advisor fees worth the cost during retirement?

A fiduciary financial advisor charges a transparent fee to manage your investments, optimize your tax strategy, and prevent emotional decision-making during severe market downturns. The value of an advisor far exceeds their fee if they successfully navigate complex tax transitions, prevent you from triggering a massive Medicare surcharge, or construct a dynamic withdrawal sequence that extends the overall lifespan of your portfolio.

How should a surviving spouse adjust their budget after a death?

The death of a spouse drastically alters household cash flow. The surviving spouse typically loses the smaller of the two Social Security checks and may experience a permanent reduction in pension income. Furthermore, the survivor now files taxes under the single tax brackets, which compress much faster and trigger significantly higher marginal rates. You must immediately revise your spending plan and consult a tax professional to navigate this difficult financial transition.

Take Control of Your Financial Future

Creating a robust retirement budget for 2026 goes far beyond cutting back on dining out or skipping vacations. It requires a complete understanding of how the newly compressed tax brackets, increased Medicare premiums, and shifting withdrawal rules interact with your personal savings. Your financial security depends entirely on continuous monitoring and proactive adjustments. Take the time this month to gather your bank statements, investment prospectuses, and tax documents. Run the numbers on your anticipated healthcare expenses and project your mandatory distributions based on current IRS life expectancy tables. Most importantly, do not attempt to navigate the complexities of the 2026 tax code alone. Schedule a consultation with a licensed fiduciary planner and a certified public accountant to stress-test your strategy. Your retirement years should represent a time of peace and fulfillment; a mathematically sound budget provides the exact foundation you need to enjoy that freedom.

4 Responses

CHPQbNbaSLEJYYvU

OCcHiKTYhxCuEFvWggqDh

VxvfJfMkNPiMuuOa

MIbpzsWlVscIselOPev