You step up to the grocery checkout counter, watch the final total flash on the screen, and feel a sudden pang of anxiety. Your favorite cuts of meat, your daily prescription medications, and your monthly utility bills all demand a larger share of your wallet than they did just a few years ago. When you cross the threshold into your sixties, the financial rules of the game shift dramatically. You transition from the wealth accumulation phase of your career into the wealth distribution phase of your retirement; this means you rely on a finite pool of assets to sustain your lifestyle. If inflation keeps rising, it acts as a silent thief, steadily eroding the purchasing power of your life savings.

To understand the true threat of persistent inflation, you need to recognize how long your retirement might actually last. A typical modern retirement easily spans twenty to thirty years. According to the Rule of 72—a mathematical principle used to estimate the effect of compound interest—an average annual inflation rate of just three percent will cut the purchasing power of your money in half in exactly twenty-four years. If inflation surges to four or five percent, that timeline accelerates dramatically. A fixed pension that feels generous at age sixty-five might barely cover your property taxes and supplemental health insurance premiums by the time you reach age eighty. Fortunately, you do not have to accept this fate as an inevitability. By proactively aligning your income streams, optimizing your tax strategy, and implementing robust risk management techniques, you can defend your hard-earned wealth against the corrosive effects of a rising cost of living.

Income Alignment: Shielding Your Cash Flow from Rising Prices

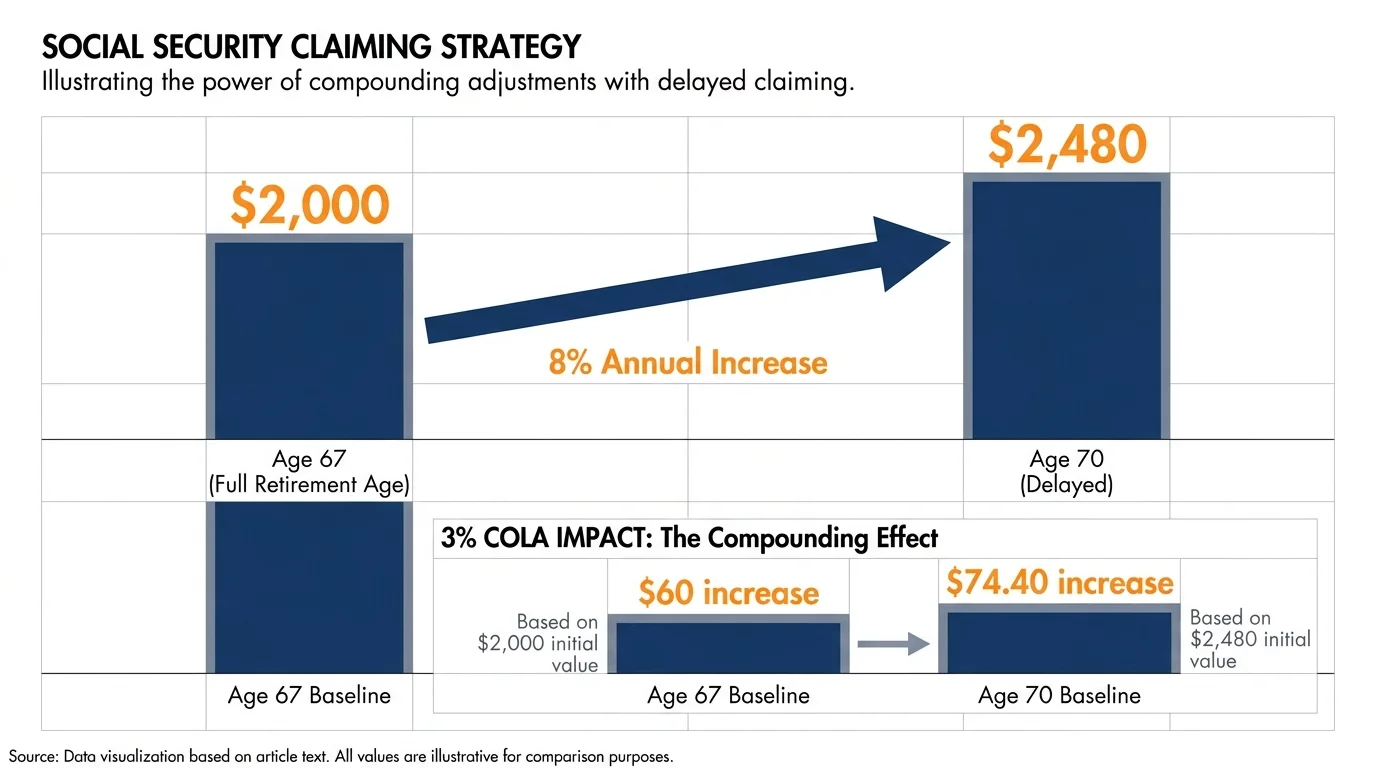

The foundation of an inflation-resistant retirement relies on maximizing the income sources that automatically adjust to economic realities. Social Security remains the most critical inflation-protected asset for the vast majority of retirees. Each year, the Social Security Administration applies a Cost-of-Living Adjustment to your benefits based on the Consumer Price Index for Urban Wage Earners and Clerical Workers. However, because you want to maximize the absolute dollar amount of this annual increase, the timing of your initial claim becomes a vital strategic decision. If you claim benefits early at age sixty-two, you permanently reduce your baseline payout. Conversely, if you wait until age seventy, you earn delayed retirement credits that increase your benefit by eight percent for every year past your full retirement age.

Consider a mathematical example. If your primary insurance amount at your full retirement age of sixty-seven is $2,000 per month, delaying your claim until age seventy boosts your baseline benefit to $2,480 per month. When a hypothetical three percent cost-of-living adjustment is applied, that increase equals $74.40 on the higher benefit, compared to just $60 on the full retirement age benefit. Over a twenty-year period, compounding those larger annual adjustments provides a massive shield against rising prices. Because individual situations vary wildly, you should always consult a licensed financial professional to evaluate your breakeven age and coordinate your claiming strategy with your spouse. You can explore the exact impact of your birth year and claiming age through the official Social Security Administration retirement planner.

Balancing Fixed Pensions and Portfolio Withdrawals

While Social Security adjusts for inflation, most corporate and municipal pensions do not. A fixed monthly pension payout of $1,500 will remain exactly $1,500 for the rest of your life. To bridge the gap between your fixed income and your rising expenses, you must turn to your investment portfolio. Historically, many retirees relied on the classic four percent rule, withdrawing a flat four percent of their initial portfolio balance and adjusting that dollar amount upward for inflation each year. In an environment defined by high inflation and unpredictable market returns, a rigid withdrawal rule poses significant dangers. You face a severe sequence of returns risk if you blindly withdraw large, inflation-adjusted amounts from your portfolio during a market downturn; doing so permanently destroys the capital you need to generate future growth.

Instead of locking yourself into a static withdrawal rate, you should adopt a dynamic withdrawal strategy. This involves reducing your discretionary spending during years when the stock market declines, thereby allowing your portfolio to recover. Furthermore, you must maintain a balanced asset allocation. Keeping your entire nest egg in cash or low-yield certificates of deposit might feel safe in the short term, but it guarantees a negative real return when inflation outpaces your interest rate. Maintaining an appropriate allocation to equities and dividend-paying stocks provides the historical growth necessary to outpace inflation over a multi-decade horizon. You can review fundamental guidance on building a diversified portfolio through the asset allocation strategies provided by the Securities and Exchange Commission.

Tax and Healthcare Strategy: Keeping More of What You Earn

When the cost of everyday goods goes up, you naturally need to withdraw more money from your retirement accounts to maintain your standard of living. If the bulk of your savings resides in tax-deferred accounts like traditional IRAs or 401(k)s, pulling out extra cash triggers a cascade of tax consequences. Every dollar you withdraw from a traditional IRA is taxed as ordinary income. If inflation forces you to increase your distributions, you might unintentionally push yourself into a higher marginal tax bracket, meaning the federal government takes a larger slice of your remaining wealth.

The situation complicates further when you reach your seventies and face Required Minimum Distributions. The federal government mandates that you must begin withdrawing a specific percentage of your tax-deferred accounts starting at age seventy-three, or age seventy-five depending on your birth year. If decades of inflation have driven up the nominal value of your investments, your mandatory withdrawals will be substantial. A highly effective strategy for mitigating this risk involves executing strategic Roth IRA conversions during your sixties. By converting portions of your traditional IRA to a Roth IRA during the gap years between your retirement and your required distribution age, you voluntarily pay taxes at your current, potentially lower tax rate. Once the money enters the Roth account, all future growth and withdrawals are entirely tax-free, insulating you from future tax hikes and forced distributions. To ensure compliance with federal codes, review the official required minimum distribution rules published by the Internal Revenue Service.

Managing Medicare IRMAA and Healthcare Costs

Rising inflation directly impacts your healthcare costs, and poor tax planning exacerbates the pain. Medicare Part B and Part D premiums are tied to your modified adjusted gross income from two years prior. If your portfolio withdrawals or mandatory distributions push your income above certain thresholds, you will be hit with the Income-Related Monthly Adjustment Amount, commonly known as IRMAA. This surcharge acts as a hidden tax on successful retirees.

The IRMAA surcharge operates on a strict cliff system. If your modified adjusted gross income exceeds a designated tier by even one single dollar, you are forced to pay the higher premium rate for the entire calendar year. Managing your taxable income through Roth distributions, utilizing Health Savings Accounts if you are eligible, and managing capital gains can help you stay below these punitive thresholds. Health Savings Accounts are particularly valuable because they offer a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are completely tax-free. Shielding your healthcare dollars from taxation provides a powerful buffer against medical inflation. You can track current surcharge thresholds by reviewing the official Medicare premium costs guide.

Protection and Legacy: Defending Your Wealth from Erosion and Fraud

Protecting your savings requires defending against localized inflation spikes, specifically the skyrocketing cost of long-term care. General inflation might hover around three or four percent, but the cost of nursing home care, assisted living facilities, and in-home nursing aids historically increases at a much steeper rate. A multi-year stay in a specialized memory care facility can completely decimate a carefully constructed investment portfolio, leaving a surviving spouse impoverished. You must address this risk proactively by evaluating traditional long-term care insurance, exploring hybrid life insurance policies that offer long-term care riders, or intentionally earmarking a portion of your portfolio for self-funding medical emergencies.

High inflation also breeds an environment ripe for financial exploitation. When seniors watch their purchasing power dwindle, they often experience a sense of financial desperation, making them prime targets for sophisticated scammers. Fraudsters frequently pitch unregulated, high-yield investments, promising guaranteed returns that perfectly outpace inflation. If an investment opportunity promises absolute safety alongside double-digit returns, it is almost certainly a scam. You must remain vigilant, freeze your credit reports to prevent identity theft, and independently vet any financial professional offering advice. Always utilize tools like FINRA BrokerCheck to verify an advisor’s credentials and disciplinary history before handing over a single dollar of your savings.

Finally, do not let inflation disrupt your legacy planning. Because inflation pushes up the nominal value of real estate and investment portfolios, you might find that your estate eventually crosses state-level estate tax exemption thresholds, even if you remain comfortably below the federal estate tax limits. You should regularly review your estate plan with a qualified attorney to ensure your wills, trusts, and powers of attorney reflect current financial realities. Moreover, review the beneficiary designations on all your retirement accounts and life insurance policies; these designations bypass your will entirely, and failing to update them can result in your assets going to an ex-spouse or a deceased relative.

Frequently Asked Questions

Should I work part-time to offset inflation?

Working part-time during your sixties or early seventies is one of the most effective strategies for combatting inflation. Even a modest part-time income allows you to reduce the amount of money you withdraw from your investment portfolio. By leaving your investments untouched during periods of market volatility and high inflation, you significantly mitigate your sequence of returns risk. Furthermore, generating earned income allows you to delay claiming Social Security, which guarantees a larger, inflation-adjusted monthly benefit later in life. Just be aware of the Social Security earnings test if you claim benefits before reaching your full retirement age, as earning too much can temporarily withhold a portion of your monthly check.

What are the best inflation hedges for my portfolio?

Protecting a portfolio requires a multifaceted approach. Treasury Inflation-Protected Securities, commonly known as TIPS, are government bonds whose principal value adjusts upward with the Consumer Price Index, ensuring your investment keeps pace with inflation. Series I savings bonds operate on a similar principle, offering a composite interest rate that includes a fixed rate and an inflation rate. However, for long-term growth, a globally diversified portfolio of equities remains your strongest defense. Companies that produce essential goods and services can typically pass higher costs on to consumers by raising their prices, allowing their stock valuations and dividends to grow over time. Real estate, whether owned directly or through Real Estate Investment Trusts, also serves as a robust hedge because property values and rental incomes generally rise alongside broad economic inflation.

How do advisor fees impact my returns during high inflation?

When inflation is eating away at your purchasing power, every fraction of a percent matters. If you pay a financial advisor a traditional asset under management fee of one or two percent annually, that fee represents a massive drag on your net returns. If your portfolio grows by five percent, but inflation is four percent, your real return is only one percent; if your advisor then takes a one percent fee, your actual wealth has not grown at all. You should scrutinize your fee structures aggressively. Consider transitioning to a fee-only fiduciary advisor who charges a flat annual retainer or an hourly rate for comprehensive financial planning, rather than surrendering a percentage of your total assets year after year.

How should I plan for a surviving spouse in an inflationary environment?

The death of a spouse often triggers a silent financial crisis known as the single tax penalty. When one spouse passes away, the surviving spouse loses the smaller of the two Social Security checks coming into the household. However, the survivor’s household expenses—such as property taxes, utilities, and home maintenance—rarely drop by half. To make matters worse, the surviving spouse must now file taxes as a single individual. The tax brackets for single filers are much narrower than those for married couples filing jointly, meaning the survivor will hit higher tax brackets at much lower income levels. To protect a surviving spouse from future inflation, you must secure adequate life insurance, maximize the primary earner’s Social Security benefit through delayed claiming, and proactively execute Roth conversions while you are still married and benefiting from wider tax brackets.

Empowering Close

Rising inflation undeniably shifts the landscape of your retirement, but it does not have to compromise your financial security. You possess the tools to fight back against the rising cost of living by carefully timing your guaranteed income streams, optimizing your tax footprint, and maintaining a diversified, growth-oriented portfolio. Take control of your financial narrative today. Gather your most recent investment statements, review your current portfolio withdrawal rates, and map out your estimated tax liabilities for the upcoming year. Schedule a comprehensive check-in with a fee-only fiduciary planner or a qualified tax professional to stress-test your strategy against persistent inflation. By acting decisively now, you secure the peace of mind necessary to truly enjoy the retirement you have spent a lifetime building.