Overlooking just one potential retirement income source can cost you thousands of dollars in compounding interest and tax advantages over your lifetime. Securing your financial independence requires looking beyond traditional pension checks and standard portfolio withdrawals. Recent inflation spikes and shifts in Medicare premiums mean relying solely on conventional strategies leaves your purchasing power vulnerable. You must uncover hidden revenue opportunities embedded within your existing assets, real estate, and tax-advantaged accounts to build a truly resilient retirement. This comprehensive guide details ten overlooked income streams alongside advanced strategies for optimizing Social Security, managing healthcare expenses, and protecting wealth from unexpected market downturns. Activating these financial levers ensures you maintain your lifestyle and protect your legacy.

Optimizing Your Core Income Alignment

Your retirement strategy requires diverse cash flow sources to withstand market volatility and sequence-of-returns risk. While you likely already monitor your primary retirement accounts, integrating specialized income streams into your portfolio strengthens your overall financial foundation.

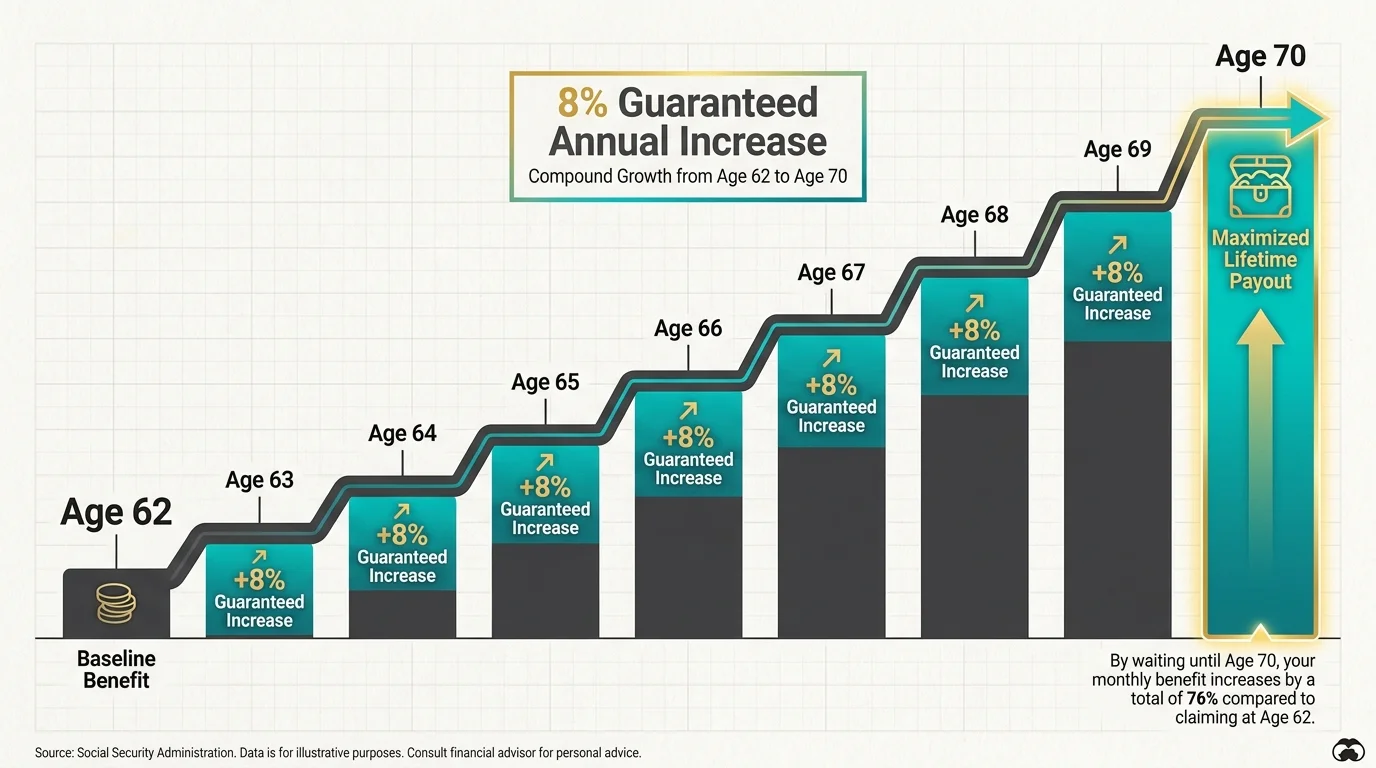

1. Delayed Social Security Credits

Many retirees view delaying benefits simply as a waiting game rather than a powerful investment tool. Claiming your benefits at your full retirement age provides a baseline payout, but choosing to wait yields an eight percent guaranteed annual increase until age seventy. Very few fixed-income investments offer an eight percent risk-free return backed by the federal government. Factoring in life expectancy estimates reveals that delaying often maximizes your lifetime payout. You should evaluate your family health history and immediate cash needs before locking in an early, permanently reduced benefit amount.

2. Health Savings Account Reimbursements

You might currently treat your Health Savings Account as a simple checking account for immediate medical bills. However, treating it as a stealth retirement fund offers massive advantages. Because these accounts feature triple-tax benefits—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified expenses—you can leave the funds invested to compound over decades. By paying current medical expenses out of pocket and saving the receipts, you create a reservoir of tax-free cash you can tap during retirement simply by reimbursing yourself for those past expenses.

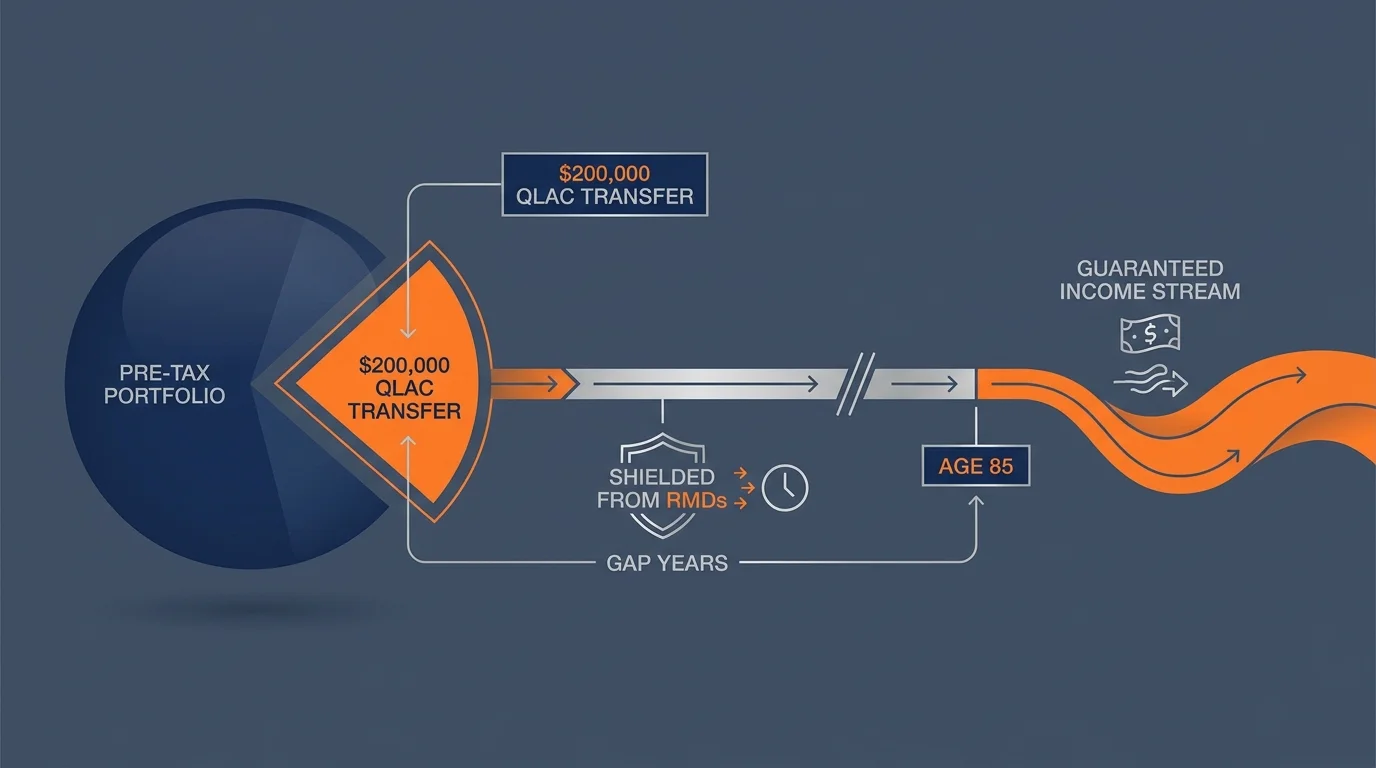

3. Qualified Longevity Annuity Contracts

Securing income for later years requires shielding a portion of your portfolio from mandatory withdrawals. A Qualified Longevity Annuity Contract allows you to transfer up to two hundred thousand dollars from your pre-tax accounts into a deferred annuity. This strategic move removes those funds from your immediate Required Minimum Distribution calculations, lowering your current tax burden. In exchange, the contract guarantees a steady stream of income starting at a later date, typically age eighty-five, ensuring you never outlive your money even if you deplete your primary investment portfolios.

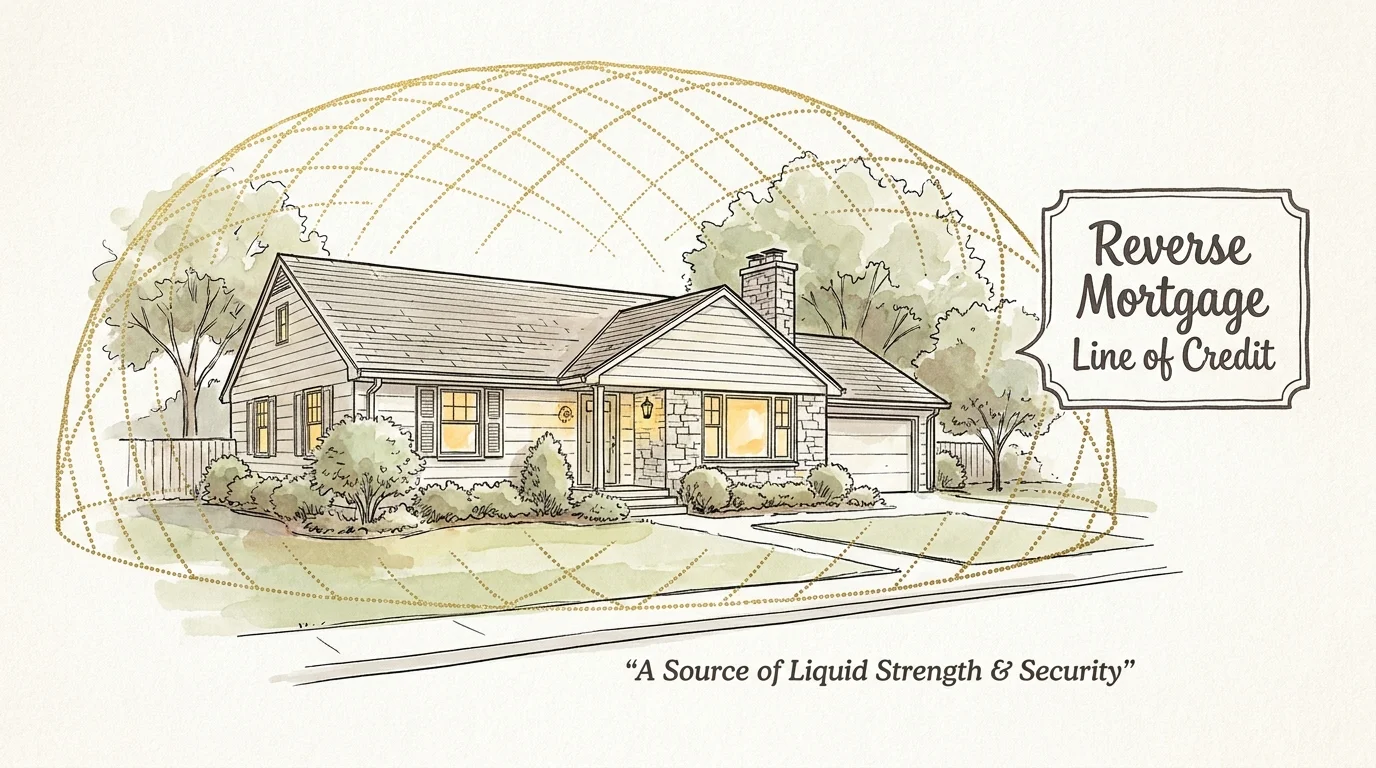

4. Home Equity Conversion Mortgages

Your primary residence likely represents a significant portion of your net worth, yet it generates zero liquid income. A Home Equity Conversion Mortgage operates as a government-insured reverse mortgage line of credit that grows over time. Rather than taking an immediate lump sum, you establish this credit line early in retirement. When a bear market hits, you draw from your home equity instead of selling depressed stocks at a loss. Utilizing specialized mortgage strategies and consulting a licensed professional ensures you apply this tool safely without compromising your living situation.

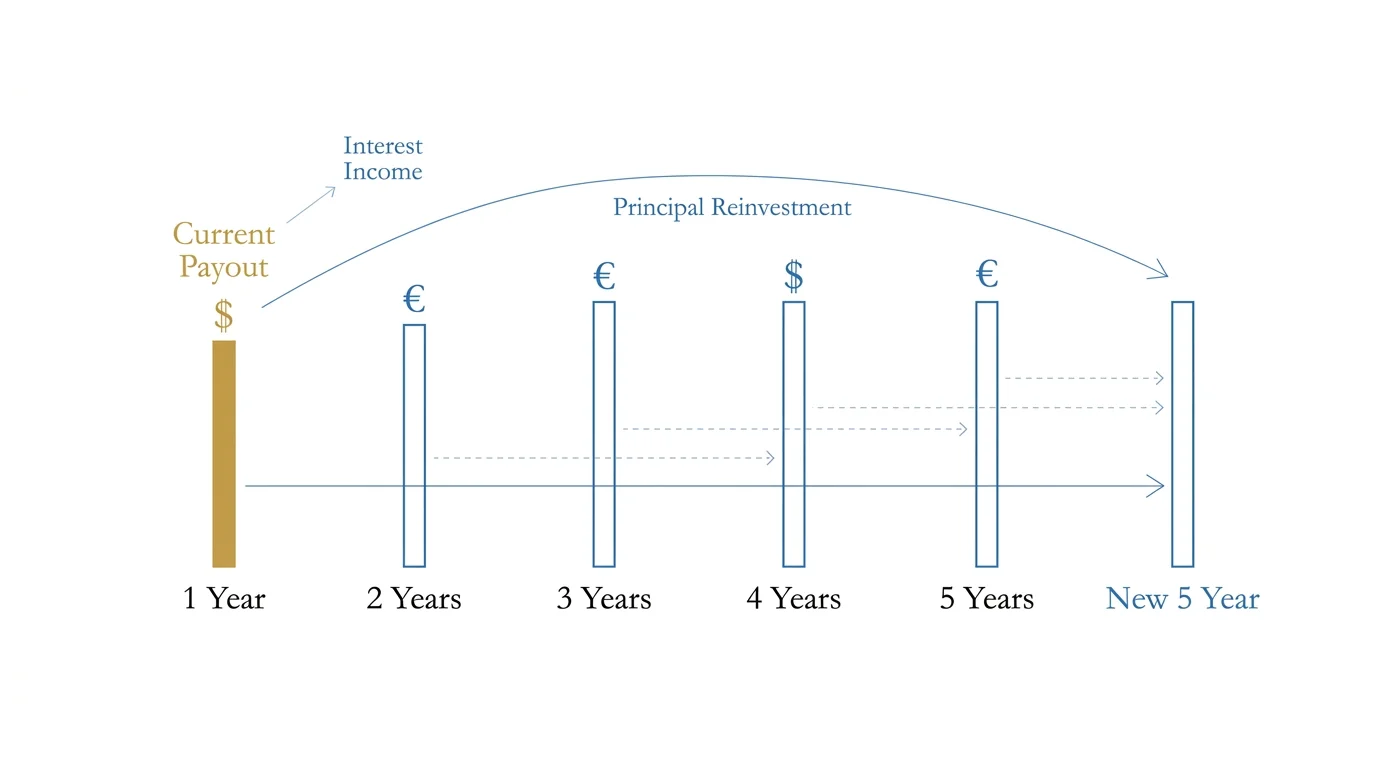

5. Fixed-Income Bond Ladders

Relying strictly on bond mutual funds exposes your principal to interest rate fluctuations. Building an individual fixed-income bond ladder eliminates this risk. By purchasing a series of Treasury or high-quality municipal bonds programmed to mature sequentially, you guarantee exactly when your principal returns. As each bond matures, it provides reliable cash flow to cover your living expenses; if you do not need the cash immediately, you simply reinvest the principal at the back end of the ladder to capture higher yields.

6. Cash Value Life Insurance Loans

Permanent life insurance policies often hold substantial accumulated cash value that remains completely insulated from equity market volatility. Rather than surrendering the policy, you can take tax-free policy loans against the cash value to supplement your income during years when your stock portfolio declines. Because you borrow against the death benefit rather than withdrawing the funds directly, you trigger no taxable event. You must monitor the loan balance alongside your licensed insurance professional to avoid allowing the policy to lapse, which could result in a severe tax penalty.

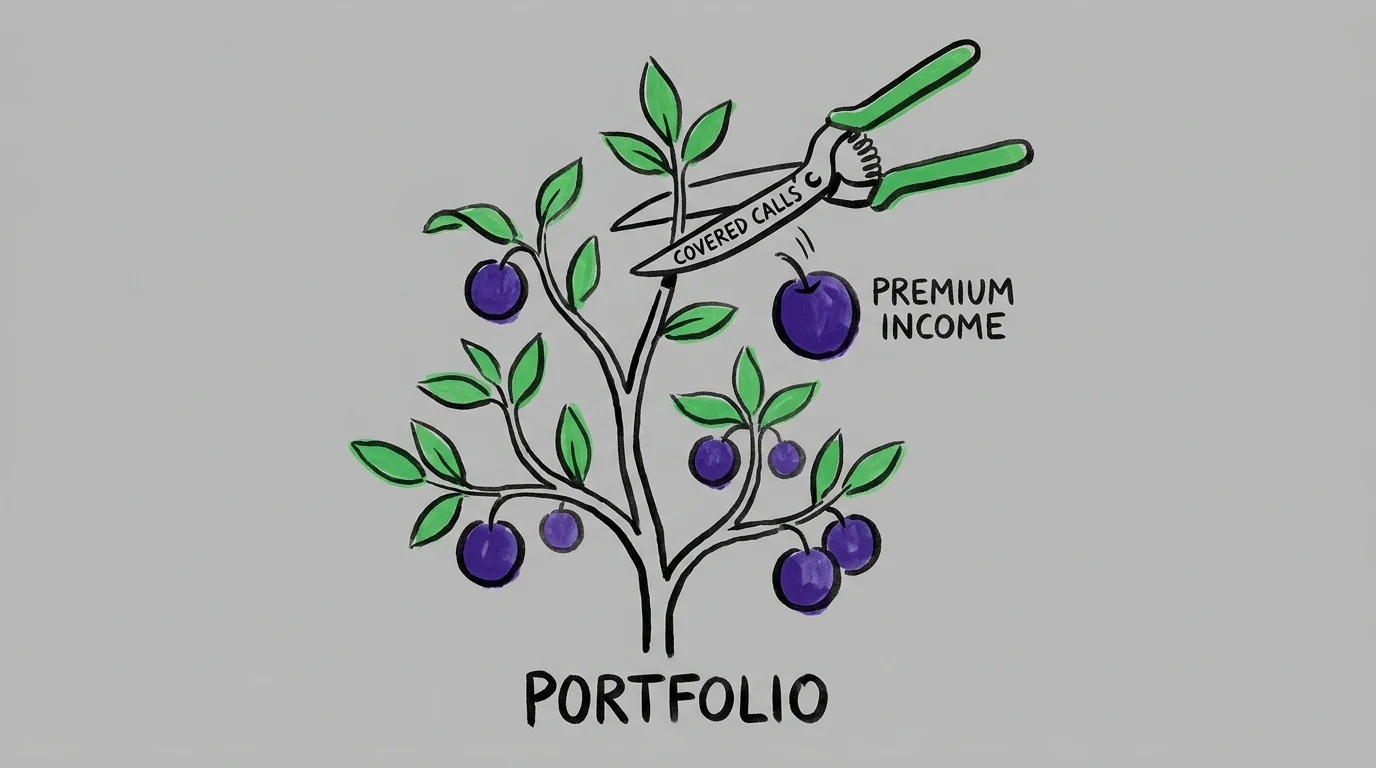

7. Covered Call Options on Existing Portfolios

If you hold a large volume of blue-chip stocks, you can generate immediate premium income by writing covered call options. This strategy involves selling another investor the right to purchase your shares at a specific, higher price within a set timeframe. In exchange for capping your potential upside on those shares, you collect an upfront cash premium. If the stock price remains stable, the option expires worthless, you keep your shares, and you retain the cash. This conservative options strategy turns stagnant equity positions into active income generators.

8. Brokered Certificates of Deposit

Standard retail bank deposits rarely outpace inflation. Moving your cash reserves into brokered certificates of deposit allows you to access significantly higher institutional yields. Available through standard brokerage platforms, these instruments trade on the secondary market and provide extensive flexibility in duration matching. You can build a high-yield cash ladder while maintaining standard federal insurance protections up to two hundred fifty thousand dollars per issuing institution. Reviewing comprehensive investor protection data helps you safely navigate the secondary market and avoid callable bond risks.

9. Real Estate Investment Trusts

Direct real estate investment requires significant capital and demanding landlord responsibilities. Real Estate Investment Trusts offer an accessible alternative by allowing you to purchase shares in commercial real estate portfolios directly through your standard brokerage account. Federal law mandates that these trusts distribute at least ninety percent of their taxable income to shareholders as dividends. This structure creates a robust, passive income stream that often features higher yields than traditional equity dividends, providing valuable portfolio diversification without property management burdens.

10. Qualified Charitable Distributions

While not a direct payout, preventing wealth from leaving your accounts acts as a powerful equivalent to generating new income. Once you reach age seventy and one-half, you can transfer up to one hundred five thousand dollars annually directly from your Individual Retirement Account to an eligible charity. This Qualified Charitable Distribution satisfies your mandatory withdrawal requirements without adding a single dollar to your Adjusted Gross Income. Reviewing the official distribution guidelines demonstrates how this strategy reduces your tax bracket and preserves the rest of your portfolio.

Navigating Tax Efficiency and Healthcare Strategies

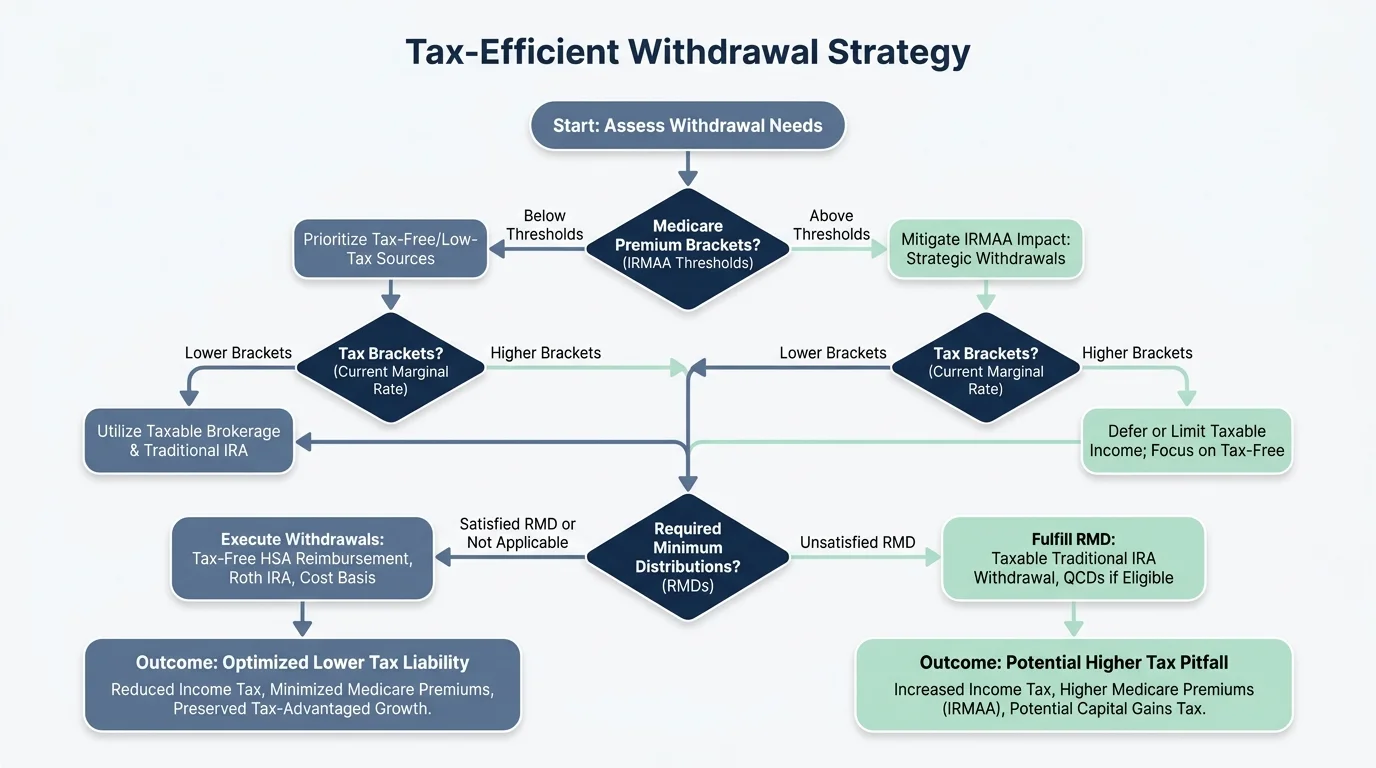

Your gross income matters far less than your net income after taxes and healthcare premiums. Proactive tax planning requires balancing withdrawals across pre-tax, post-tax, and tax-free accounts to maintain an optimized Adjusted Gross Income. Understanding the interplay between your capital gains, pension distributions, and Social Security taxation is critical to keeping your money out of federal coffers. Whenever you draw exclusively from traditional retirement accounts, you risk pushing yourself into higher marginal tax brackets. Strategic withdrawals from Roth accounts or cash reserves during high-expense years keep your taxable income stable and preserve your wealth over the long term.

Healthcare costs represent the most significant variable expense in your retirement budget. Medicare premiums are not static; they fluctuate based directly on your tax returns from two years prior. If your taxable income crosses specific thresholds, you face an Income-Related Monthly Adjustment Amount surcharge. This surcharge can quickly double your Medicare Part B and Part D premiums. Consulting the standard Medicare cost brackets helps you project your future liabilities. Executing strategic Roth conversions early in retirement or utilizing the previously mentioned charitable distribution strategies helps you avoid these costly, invisible tax cliffs.

Protecting Your Wealth and Solidifying Your Legacy

Generating diverse income streams means nothing if a single catastrophic event wipes out your accumulated assets. Ensuring your surviving spouse and children are not burdened by complex legal battles or severe medical debt should be your primary motivation. Traditional long-term care insurance often features exorbitant premiums, but modern hybrid life insurance policies offer highly practical alternatives. These hybrid products allow you to accelerate the death benefit to cover facility care or in-home nursing expenses; if you never need the care, your heirs still receive the tax-free death benefit. This ensures your dedicated capital is never wasted.

Beyond physical health, you must actively protect your financial assets from sophisticated external threats. Elder financial fraud strips billions of dollars from seniors annually through complex phishing schemes, identity theft, and fraudulent investment pitches. You should freeze your credit across all three major bureaus and implement multi-factor authentication on every financial account. Establishing a trusted contact on your brokerage accounts empowers your financial institution to pause suspicious outgoing transfers and contact a designated family member if they suspect cognitive decline or coercion.

Solidifying your legacy also requires meticulous estate planning. Your will does not dictate where your retirement accounts and life insurance proceeds go; beneficiary designations override all other legal documents. Failing to update these forms after a divorce, death, or birth can result in your assets flowing to an unintended individual or becoming trapped in a lengthy probate process. You must conduct an annual review of every account to verify that primary and contingent beneficiaries accurately reflect your current wishes.

Frequently Asked Questions About Senior Finances

How does part-time work impact my benefits?

Earning an active income while claiming early Social Security triggers the retirement earnings test. If you earn above a specific annual limit before reaching your full retirement age, the government temporarily withholds a portion of your benefits. These withheld funds are not permanently lost; your benefit undergoes a positive recalculation upon reaching full retirement age to account for the withheld months. Once you reach full retirement age, you can earn an unlimited amount of active income without experiencing any reductions to your monthly benefit checks.

What are the most effective inflation hedges for retirees?

Combating the erosion of your purchasing power requires holding assets that historically rise alongside consumer prices. Treasury Inflation-Protected Securities adjust their principal value based on the Consumer Price Index, guaranteeing your real rate of return never falls below zero. Additionally, incorporating a diversified basket of dividend-growth stocks provides an organic income stream that outpaces inflation. Tangible assets, including real estate investment trusts and structured commodities, also offer robust defense against depreciating currency.

How can I evaluate financial advisor fees?

Transparency dictates the difference between a valuable partnership and a toxic drain on your portfolio. You should exclusively hire advisors who operate under a strict fiduciary standard, meaning they are legally bound to act in your best financial interest. Understand whether the advisor charges a flat annual retainer, an hourly consultation rate, or a percentage of your assets under management. You must demand an itemized breakdown of all underlying fund fees, administrative costs, and trading commissions to ensure you retain maximum yield.

What are the essentials of surviving spouse planning?

The death of a partner initiates a massive financial shock often referred to as the widow’s penalty. The surviving spouse typically loses the smaller of the two Social Security checks coming into the household. Simultaneously, the survivor transitions from the favorable joint-filing tax brackets into the highly compressed single-filer tax brackets, frequently resulting in a higher tax burden despite a drop in total income. Comprehensive planning requires securing adequate life insurance, maximizing pension survivorship options, and structuring tax-free liquidity to bridge the inevitable income gap.

Take Command of Your Financial Future

Mastering your retirement requires moving beyond passive observation and actively managing your diverse resources. By implementing strategic bond ladders, maximizing your healthcare savings accounts, and ruthlessly protecting your portfolio from tax inefficiencies, you build an unshakeable financial fortress. You possess the tools necessary to optimize your core income, secure your healthcare funding, and leave a lasting, impactful legacy. Review your most recent financial statements today, verify your beneficiary designations, and schedule a comprehensive strategy session with a licensed fiduciary to align these powerful income streams with your specific lifestyle goals.