Diversifying your retirement income builds a resilient safety net for the decades ahead, ensuring you never have to rely solely on a single government check. Modern retirees actively combine traditional savings with alternative revenue streams to thrive despite persistent inflation and market volatility. Because the Social Security Administration notes their benefits replace only about forty percent of average pre-retirement earnings, exploring options like dividend portfolios, part-time consulting, and strategic real estate investments helps you bridge the remaining gap. Embracing these multiple income pillars empowers you to fund your ideal lifestyle, protect your hard-earned savings, and enjoy true peace of mind without staring anxiously at the calendar waiting for your next direct deposit.

The Current Landscape of Senior Finances

Recent market dynamics mandate a comprehensive approach to senior finances. While annual cost-of-living adjustments provide some relief against rising prices, these incremental bumps rarely keep pace with the specific expenses retirees actually face daily. Healthcare, specialized housing, and accessible transportation costs consistently outpace general inflation, actively eroding the purchasing power of fixed government benefits issued by the Social Security Administration. Consequently, managing your money today requires looking far beyond traditional pension plans and federal support systems. You must construct a multifaceted financial engine that rapidly adapts to shifting economic winds and unexpected personal expenses.

The modern retirement timeline stretches longer than ever before, routinely spanning two or three full decades. This longevity represents a profound triumph of modern medicine and public health, yet it introduces significant financial complexities that previous generations rarely encountered. To maintain a comfortable standard of living, older adults increasingly choose to remain economically engaged long past traditional retirement ages. Data published by the Bureau of Labor Statistics highlights a clear trend showing older Americans represent the fastest-growing segment of the modern workforce. This reflects a strategic pivot toward flexible, purpose-driven work that substantially supplements investment yields while keeping your mind sharp.

Policy adjustments constantly influence how you must manage your accumulated wealth. Changes to the full retirement age and the complex taxation of benefits demand careful, proactive navigation. When you thoroughly understand the mechanics of the current economic environment, you successfully position yourself to capitalize on emerging opportunities rather than simply reacting to stressful financial pressures. Transitioning from a mindset of passive receipt to active income generation fundamentally alters your entire retirement trajectory, granting you the ultimate autonomy to make lifestyle choices based on desire rather than strict financial limitations.

Income Planning Beyond the Monthly Benefit

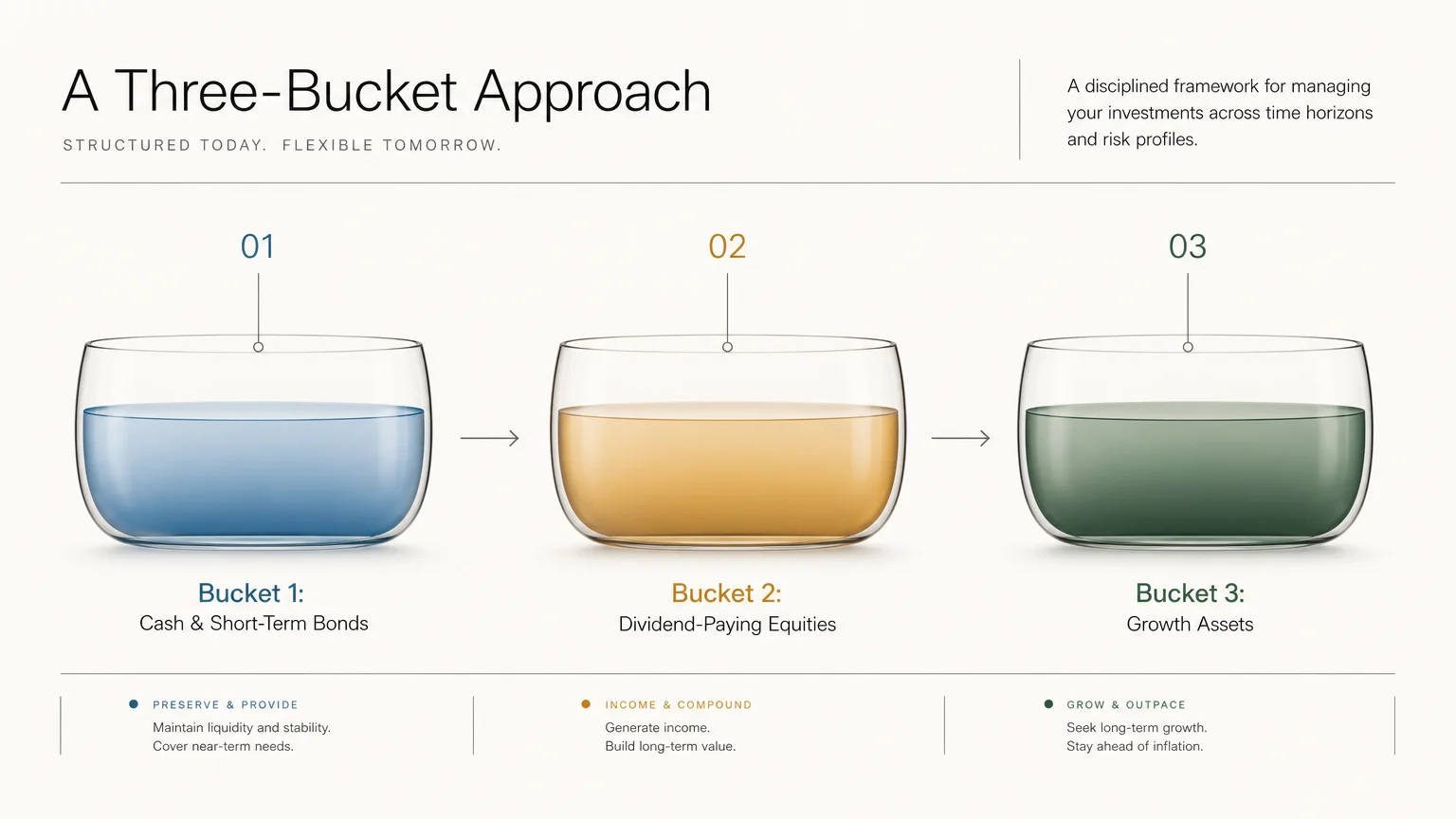

Building a robust financial portfolio requires integrating diverse asset classes that generate consistent, reliable cash flow regardless of market conditions. Certified Financial Planner professionals routinely emphasize the absolute importance of creating dedicated income buckets. This specialized strategy involves segregating your assets based on exactly when you plan to spend them, which powerfully protects your immediate living expenses from sudden stock market downturns. You can allocate cash equivalents and short-term bonds to cover the first few years of your retirement, while confidently allowing the remainder of your portfolio to remain invested in higher-yielding, growth-oriented assets.

Dividend-paying equities offer a highly compelling avenue for sustainable revenue generation. Companies boasting a long history of continually increasing their payouts—often referred to within the industry as dividend aristocrats—provide a fantastic dual benefit of regular cash deposits and long-term capital appreciation. When you deliberately invest in broadly diversified dividend index funds, you actively participate in overall market growth while securing a reliable stream of money that frequently outpaces historic inflation rates. Real estate investment trusts present another highly viable option for individuals seeking direct exposure to lucrative property markets without shouldering the heavy physical demands of hands-on property management. These unique trusts legally distribute the vast majority of their taxable income directly to shareholders, creating an incredibly attractive yield for fixed-budget households.

Fixed-income vehicles remain a fundamental cornerstone of conservative, stress-free wealth management. Constructing a comprehensive bond ladder guarantees a highly predictable return of both principal and interest at staggered, carefully timed intervals. This deliberate approach powerfully mitigates interest rate risk; if national rates rise, you simply reinvest your maturing assets at the newer, higher prevailing yields. Furthermore, fixed annuities can permanently transfer severe longevity risk completely off your shoulders and onto a regulated insurance company. By purchasing a single premium immediate annuity, you instantly secure a guaranteed, unchangeable monthly payment for life, effectively creating a personalized, bulletproof pension that perfectly complements your baseline federal benefits.

Lifestyle Design That Pays Dividends

Retirement planning clearly extends far beyond sterile spreadsheets and fluctuating investment accounts; it requires highly intentional lifestyle design that transforms your lifelong passions into tangible, spendable financial resources. The expanding gig economy currently provides unprecedented, unparalleled flexibility for older adults seeking to monetize their deeply accumulated industry expertise. If you spent decades mastering a highly specific corporate sector, part-time consulting allows you to command premium hourly rates while strictly dictating your own working hours. You selectively choose only the specific projects that intellectually stimulate you, completely avoiding the toxic office politics and exhausting daily commutes that defined your earlier career.

Accessibility and physical comfort play incredibly crucial roles in how you structure and maintain your secondary income streams. If varying mobility or sudden chronic health conditions unexpectedly keep you physically close to home, the modern digital marketplace offers truly abundant, low-stress opportunities. Remote business consulting, specialized virtual tutoring, and freelance technical writing require little more than a highly reliable internet connection and a comfortable ergonomic chair. You can brilliantly leverage your deep knowledge of historical events, advanced business management, or the creative arts to actively guide younger professionals or university students. This completely remote approach fiercely protects your vital physical energy reserves while significantly supplementing your monthly household budget.

Strategic housing decisions also reliably unlock surprisingly substantial wealth generation potential. Many insightful retirees eventually discover that their primary, long-held residence represents their single largest untapped financial asset. Intentionally downsizing to a smaller, significantly more accessible home not only drastically reduces expensive utility bills and frustrating maintenance costs, but it also rapidly frees up massive amounts of dormant home equity for immediate market reinvestment. Alternatively, if you strongly prefer to remain deeply rooted in your current community, you might intelligently consider house hacking by legally renting out a finished basement or a comfortable spare bedroom. Reputable platforms catering specifically to traveling medical nurses or visiting university academics allow you to generate substantial, highly consistent rental income with relatively low personal risk, brilliantly turning empty physical space into a highly reliable financial asset.

Health and Wellness as Wealth Preservation

Traditional financial advisors rarely discuss resting cardiovascular health or advanced mobility training, yet physical well-being firmly stands as one of the absolutely most effective wealth preservation strategies currently available to you. Chronic debilitating illness and unexpected, catastrophic medical emergencies possess the terrifying destructive power to completely decimate even the most meticulously crafted financial blueprints. Dedicated gerontologists and specialized aging researchers consistently demonstrate that actively investing your time and financial resources into preventative health measures dramatically reduces your total lifetime medical expenditures. When you strictly prioritize daily physical movement, highly nutrient-dense nutrition, and regular preventative medical screenings, you fiercely and actively defend your hard-earned nest egg.

Navigating the dense complexities of federal healthcare funding absolutely requires proactive, continuous education. The primary federal health insurance program currently offers numerous vital preventative services at absolutely no additional out-of-pocket cost, provided you thoroughly understand exactly how to properly access them. The official Medicare portal explicitly details an incredibly extensive list of fully covered diagnostic screenings, annual wellness visits, and specialized chronic disease management programs specifically designed to catch minor health issues long before they require massively expensive surgical interventions. By aggressively maximizing these available benefits, you entirely avoid the devastating, portfolio-draining costs directly associated with severe medical crises. Keeping your physical body exceptionally strong translates immediately and directly into keeping your personal bank accounts highly robust.

Furthermore, managing your specialized healthcare savings tools effectively and strategically provides a remarkably hidden source of immense financial flexibility. If you smartly funded a dedicated Health Savings Account during your active working years, those specific funds continuously grow completely tax-free and can be subsequently withdrawn totally tax-free for any legally qualified medical expenses throughout your retirement. Unlike restrictive flexible spending accounts that expire annually, these powerful health savings balances roll over indefinitely year after year. Deliberately using this specifically dedicated pool of money for necessary monthly prescriptions, expensive vision care, and major restorative dental procedures aggressively prevents you from prematurely draining your primary, wealth-generating investment portfolios, allowing your core financial assets significantly more time to powerfully compound and exponentially grow.

Protecting Your Assets from Invisible Threats

Securing lucrative alternative income streams naturally introduces entirely new complex variables that absolutely require highly vigilant risk management. One major, frequently overlooked hazard directly involves accidentally triggering totally unintended tax consequences and sudden, painful benefit reductions. Earning substantially high alternative income can rapidly increase your modified adjusted gross income, potentially subjecting a significantly larger portion of your fixed federal retirement benefits to heavy taxation. Additionally, unknowingly crossing highly specific income thresholds immediately initiates the dreaded Income-Related Monthly Adjustment Amount, commonly known throughout the financial industry as the Medicare surcharge. This punitive calculation drastically and unexpectedly increases your Medicare Part B and Part D monthly premiums, effectively and brutally neutralizing the hard-won financial gains you recently made through your various side ventures. You absolutely must work closely and regularly with a certified tax professional to strategically optimize your annual withdrawal strategies and effectively manage your total taxable income efficiently under current Internal Revenue Service guidelines.

Understanding the critical legal difference between actively earned income from a consulting gig and purely passive income generated from a real estate trust powerfully empowers you to structure your personal finances highly defensively. Another incredibly pervasive and dangerous threat to your ongoing financial security actively comes from highly sophisticated, technologically advanced fraud schemes specifically targeting older, wealthier adults. As you intelligently diversify your financial assets across various new digital platforms and modern investment vehicles, you unfortunately become a highly attractive potential target for viciously malicious actors.

Heartless scammers frequently and aggressively use the enticing, fake promise of guaranteed, unbelievably high-yield alternative investments to ruthlessly separate unsuspecting retirees from their carefully accumulated capital. You must always rigorously verify the official credentials of any new financial advisor or digital investment platform before ever transferring your funds. The AARP Fraud Watch Network serves as an absolutely invaluable, highly protective resource for accurately tracking current financial scams and actively learning exactly how to identify deeply predatory behavior. By strictly maintaining a highly healthy skepticism toward any unsolicited, high-pressure investment opportunities and by regularly and meticulously monitoring your personal credit reports, you successfully construct an entirely impenetrable defensive fortress securely around your precious retirement resources.

Frequently Asked Questions

How much of my income should come from sources other than Social Security?

Experienced financial planners generally recommend that standard government benefits should logically replace only about forty percent of your total pre-retirement income. To successfully maintain your current, comfortable standard of living, the remaining sixty percent must predictably come directly from alternative financial sources. You should strategically aim to comprehensively build a highly diversified overall portfolio where your personal cash savings, robust investment yields, and flexible part-time earnings comfortably and reliably cover all your essential daily living expenses and fun discretionary spending.

Can earning extra money reduce my Social Security benefits?

Claiming your federal benefits before officially reaching your designated full retirement age while simultaneously earning substantial job income can definitely temporarily reduce your specific monthly payouts. The government strictly withholds a designated portion of your benefits if your actively earned income explicitly exceeds a specific, annually adjusted limit. However, once you finally reach your exact full retirement age, this restrictive earnings test absolutely no longer applies, and you can freely earn an entirely unlimited amount of money without facing any benefit reductions. Notably, purely passive revenue generated from investments, pensions, or rental properties strictly does not count toward this earnings limit.

Are dividend stocks a safe replacement for fixed-income investments?

While robust dividend stocks offer truly excellent, proven potential for significantly growing your passive income right alongside rising inflation, they inherently carry substantially higher market volatility than traditional, conservative fixed-income investments like treasury bonds or certificates of deposit. Stock prices constantly fluctuate based on unpredictable global market conditions, and even highly stable companies can suddenly cut their dividend payments during severe, prolonged economic downturns. You should strategically view dividend equities as a highly powerful, aggressive complement to your defensive fixed-income strategy rather than a total, complete replacement. Maintaining a highly balanced, thoughtful mix of securely guaranteed bonds and growth-oriented, dividend-paying equities successfully ensures you consistently enjoy both unshakeable financial stability and long-term, inflation-beating purchasing power.

What is the most reliable way to generate passive income in retirement?

True reliability in generating passive income fundamentally stems from incredibly broad, strategic asset diversification rather than desperately seeking a single, mythical perfect investment. Carefully constructing a robust portfolio that simultaneously includes low-cost, broadly diversified dividend index funds, highly staggered, predictable bond ladders, and potentially a secure fixed annuity creates a highly dependable, unshakeable revenue stream. Real estate investment trusts also reliably provide highly consistent, lucrative payouts without ever requiring the exhausting physical labor of traditional property management. By smartly combining these fundamentally different asset classes, you mathematically ensure that if one specific sector unexpectedly experiences a temporary, painful decline, your other carefully selected investments continue to relentlessly generate the vital cash you desperately need to fully support your daily, vibrant life.

Take Action Today

Achieving true, lasting financial independence during your golden years absolutely requires immediate, highly decisive action rather than passive, fearful observation. You fully hold the immense power to entirely redesign your personal financial architecture and securely fund the vibrant lifestyle you genuinely deserve. Review your current, detailed financial statements within the next forty-eight hours to identify exactly how much of your monthly cash flow heavily depends on fixed government programs. Once you clearly establish this baseline, confidently select one highly specific alternative income strategy—whether thoroughly researching a high-yield dividend fund or exploring a remote consulting opportunity—and dedicate one uninterrupted hour to mapping out your very first step. By actively taking firm control of your financial narrative today, you successfully build an absolutely unshakeable, resilient foundation for a vibrant, totally secure, and deeply fulfilling future.