Maximizing your pension income requires looking closely at how geography dictates your purchasing power, tax burden, and quality of life. The modern retiree leans heavily on fixed income sources, making your chosen home state a crucial financial decision rather than just a climate preference. Relocating to states that exempt pension payouts from taxation or boast significantly lower living costs can inject tens of thousands of dollars into your retirement budget over a single decade. We analyze the latest economic data to show you exactly how different regions treat your hard-earned benefits, giving you the practical tools necessary to confidently evaluate your ideal destination and protect your long-term financial security.

The Current Landscape of Pension Income and Retirement Finances

Managing retirement finances today requires far more precision than it did a generation ago. While inflation has cooled from its recent historic peaks, the baseline cost of everyday goods, real estate, and healthcare remains substantially elevated. You can no longer rely on simple geographic assumptions—moving south or west does not automatically guarantee a more affordable lifestyle. Instead, state legislatures actively rewrite their tax codes to compete for retiring demographics, recognizing that older adults bring steady, reliable economic activity to local businesses. Recent legislative shifts offer you broader flexibility for how you manage distributions, but state-level taxation ultimately dictates the daily purchasing power of those funds.

Navigating this complex geographic map means understanding the fierce economic competition between regions. Some states systematically eliminate taxes on retirement distributions to reverse population declines and attract wealth, while others heavily tax both public and private pensions to fund extensive local infrastructure projects. Consequently, your monthly retiree budget fluctuates wildly depending on whether your mailing address sits in a high-tax northeastern corridor or a tax-friendly midwestern or southern enclave. Taking a proactive, research-driven approach to understanding these ongoing legislative trends ensures you maintain total control over your hard-earned wealth rather than surrendering it to avoidable local tax burdens.

Strategic Pillars for Maximizing Your Retirement Finances

Income Planning and Tax Optimization

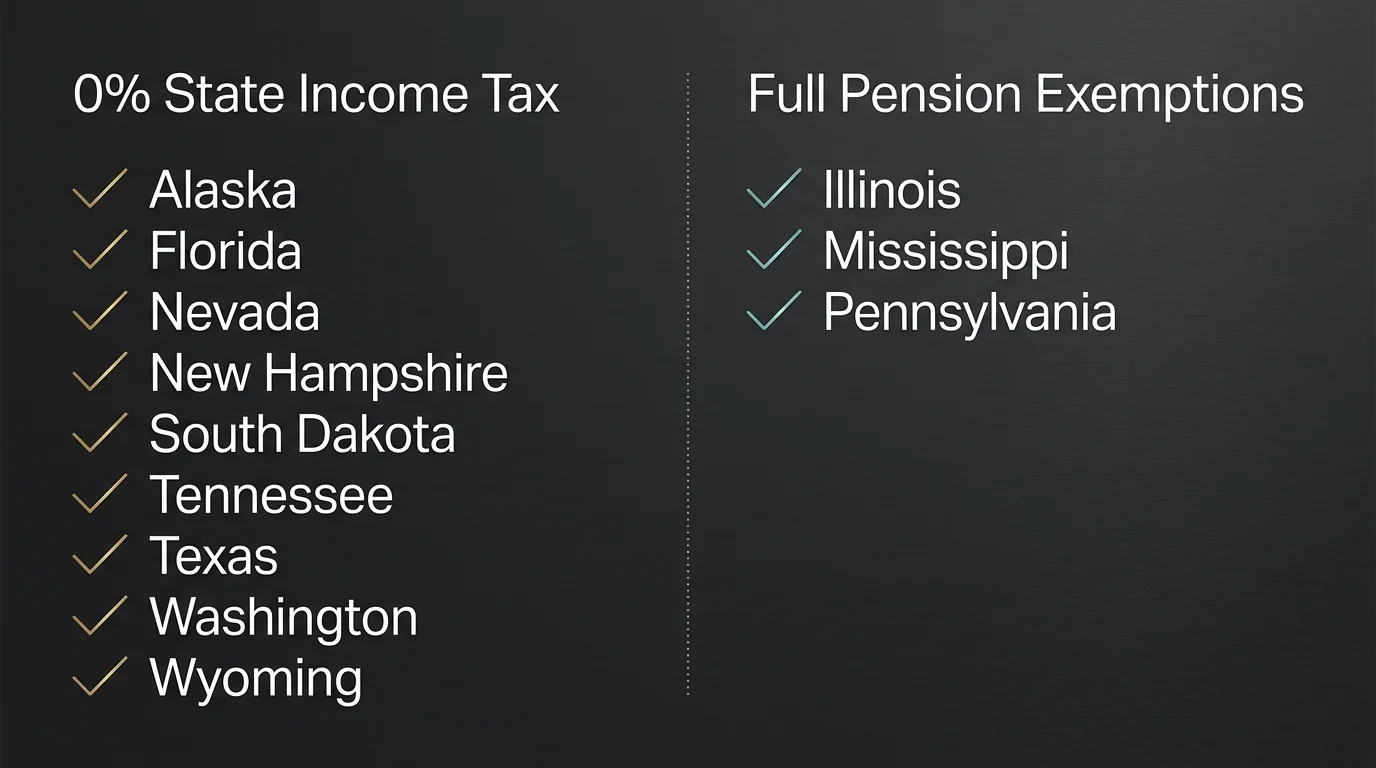

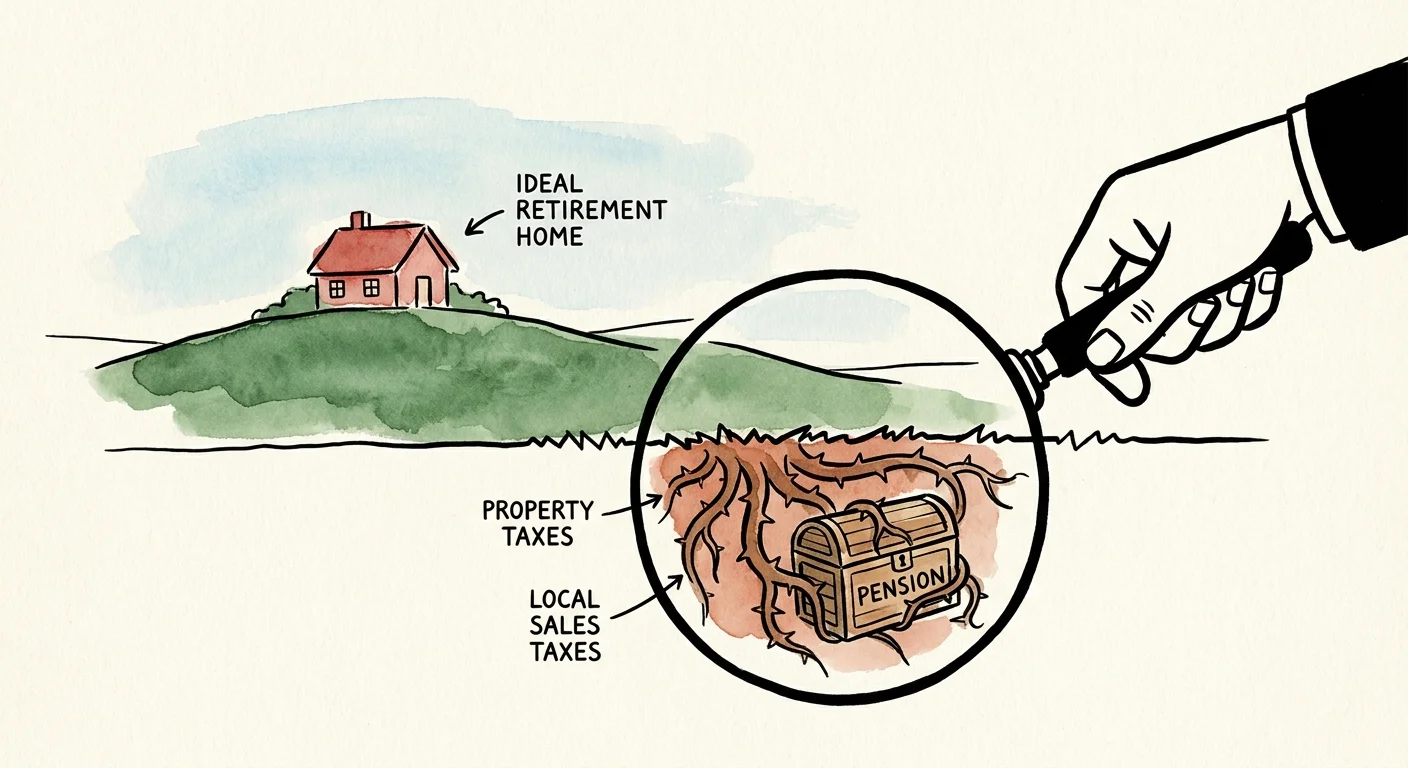

Securing your financial independence begins with rigorous income planning and a clear-eyed assessment of state tax liabilities. Currently, nine states levy absolutely no state income tax—Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Relocating to one of these jurisdictions instantly shields your regular pension income, investment dividends, and standard account withdrawals from state-level taxation. However, focusing solely on the lack of an income tax ignores the broader fiscal reality of municipal funding. You must carefully evaluate the total tax burden, which incorporates local property taxes, municipal sales taxes, and state estate levies.

Several regions offer compelling alternatives by maintaining a general income tax while completely exempting specific retirement revenues. States such as Illinois, Mississippi, and Pennsylvania do not tax pension income or distributions from qualified retirement plans. This targeted approach often provides a highly balanced environment, combining the benefits of robust public services funded by the broader workforce with a specialized protective shield around your personal retirement finances. Conversely, states with aggressively high baseline taxes sometimes offer age-based standard deductions that mitigate the financial blow for middle-income households, proving that headline tax rates rarely tell the entire story.

Before putting a down payment on a new home, you need to understand the critical distinction between public and private pensions. Many states treat federal, state, or municipal government pensions with extreme leniency, offering generous exemptions specifically designed to keep retired civil servants, educators, and military personnel within their borders. Private corporate pensions frequently receive substantially less favorable treatment, meaning a retired municipal worker and a retired corporate executive living on the exact same street might face entirely different tax obligations. You can explore detailed state-by-state tax policies through the Internal Revenue Service to verify exactly how local governments will treat your distinct income streams.

Lifestyle Design and Relocation Realities

Protecting your pension requires evaluating everyday living expenses just as closely as you examine tax brackets. The cost of living varies dramatically from county to county, deeply influencing how far your monthly checks stretch. Housing represents the largest single expense for most older adults. While states like Florida and Texas offer incredible tax advantages, they have simultaneously experienced massive surges in housing costs and homeowners insurance premiums over the past five years. You might save thousands on income taxes only to spend those exact savings on rapidly escalating property insurance.

You also need to factor transportation and utility costs into your lifestyle design. Relocating to a rural, tax-friendly state often necessitates driving long distances for basic groceries, social engagements, and medical appointments. The money saved on state taxes can quickly evaporate at the gas pump or through the hidden costs of isolation. Choosing a location with accessible public transit, walkable neighborhood infrastructure, and diverse cultural amenities often proves more cost-effective—and emotionally fulfilling—than isolating yourself in a remote area solely to avoid taxes. True financial optimization requires balancing your spreadsheet with your desired quality of life.

Health, Wellness, and Long-Term Care Costs

No discussion about retirement states is complete without a deep dive into healthcare accessibility and pricing. Medical expenses represent the most unpredictable variable in your long-term financial plan. While standard coverage remains consistent nationwide, the out-of-pocket costs for supplemental insurance, specialized care, and long-term assisted living facilities differ vastly across state lines. States with incredibly low costs of living sometimes suffer from severe shortages of geriatric specialists and primary care physicians, forcing residents to travel out of state for critical treatments.

You must actively research the local healthcare infrastructure before committing to a move. Investigate the density of top-tier hospital systems and the availability of in-home care professionals in your target zip code. Additionally, state regulations dictate the pricing structures for supplemental insurance policies that cover the gaps left by traditional coverage. By reviewing the federal Medicare guidelines alongside local state health department data, you can build an accurate projection of your future medical expenses and ensure your chosen destination supports your long-term physical well-being just as well as your wallet.

Perspectives from Retirement and Aging Experts

Certified Financial Planners consistently warn against making major geographic moves based exclusively on tax avoidance. Financial advisors frequently highlight a phenomenon known as the “sunshine tax”—the hidden premium you pay for living in highly desirable, warm-weather retirement havens. These professionals urge clients to run comprehensive cash-flow simulations that account for property taxes, sales taxes, and regional inflation before packing their bags. They emphasize that while keeping more of your pension income is a worthy goal, the mathematical reality of cross-country relocation often requires five to seven years just to break even on the physical moving and real estate transaction costs.

Gerontologists and aging specialists offer a distinct, equally critical perspective focused on community integration. Aging researchers advocate strongly for prioritizing social networks and family proximity over marginal financial gains. Relocating to a perfectly optimized tax haven means little if you suffer from profound social isolation and lack a support system during a medical emergency. Experts from leading advocacy organizations for older adults continually stress that community engagement, a sense of deep personal purpose, and accessible social infrastructure dramatically improve both longevity and cognitive health. Ultimately, the best state for your retirement is one that harmonizes your financial realities with your human need for connection.

Uncovering Hidden Risks and Regional Safeguards

Aggressively chasing the lowest possible cost of living can expose you to unforeseen financial dangers. One of the most common pitfalls involves sudden property tax reassessments. Many states attract new residents with low initial property taxes, only to aggressively reassess home values upon purchase, resulting in a shocking tax bill during your second year of residency. You must also remain hyper-vigilant regarding regional insurance crises. Coastal and wildfire-prone states are currently experiencing unprecedented volatility in home insurance markets, with major carriers completely abandoning certain zip codes and leaving retirees stranded with exorbitant, state-mandated fallback policies.

Furthermore, moving across state lines makes you a prime target for relocation scams and predatory service providers. Criminals specifically target older adults who are transitioning to new states and lacking established relationships with local contractors, financial institutions, and medical providers. Always verify the licensing and background of any professionals you hire in a new city. You can track accurate regional expenditure data and identify cost anomalies by utilizing resources from the Bureau of Labor Statistics, allowing you to establish a realistic baseline for local pricing and actively protect yourself against predatory inflation.

Frequently Asked Questions About Retirement States

Do all states tax private pension income the same way as public pensions?

No, the tax treatment between public and private pensions varies significantly across the country. Many states offer full or partial exemptions specifically for government pensions—such as those earned by teachers, police officers, and federal workers—while applying standard income tax rates to private corporate pensions. You must verify the exact tax code of your prospective state to understand how they classify your specific payout. Never assume that a generic “pension exemption” applies equally to all retirement income sources.

How do property taxes and insurance premiums offset zero income tax benefits?

States require revenue to operate schools, maintain roads, and fund emergency services. When a state lacks an income tax, it almost always compensates by levying higher property taxes, implementing steeper sales taxes, or imposing various municipal fees. Additionally, popular zero-income-tax states frequently experience volatile real estate markets, leading to exorbitant homeowners insurance premiums. You must calculate the total combined burden of property taxes, sales taxes, and insurance to determine if moving actually improves your bottom line.

Will moving to a state with a lower cost of living affect my federal benefits?

Relocating to a cheaper state does not alter the gross amount of your federal Social Security benefits. The federal government calculates your baseline payout based entirely on your lifetime earnings record and your age at claiming. However, states have their own rules regarding the taxation of those federal benefits. You can review exactly how your benefits are calculated and managed regardless of your location by consulting the Social Security Administration. While your gross federal check remains identical, your net take-home pay will shift based on your new state’s tax laws.

What should I consider about healthcare access when evaluating new retirement states?

Beyond standard medical costs, you must investigate the physical accessibility of specialized care. Cheaper, rural states often suffer from severe shortages of geriatric specialists, neurologists, and specialized physical therapists. You should research the proximity of highly rated hospital networks, the availability of comprehensive in-home nursing services, and the local availability of public transportation for medical appointments. Securing affordable housing loses its appeal entirely if you must travel three hours each way to consult with your cardiologist.

Your Next Steps for a Secure Retirement

Finding the perfect state to maximize your pension income requires looking past the glossy brochures to understand the hard data driving local economies. You have the power to protect your financial legacy by actively balancing state tax codes against property costs, healthcare accessibility, and your fundamental need for a supportive community. Your ideal retirement destination exists at the intersection of mathematical reality and lifestyle preference.

Take direct action today to solidify your financial future. Over the next forty-eight hours, pull your most recent state tax return and calculate exactly how much of your current tax bill stems directly from your pension or retirement distributions. Compare that single figure against the average property tax rate of your top two dream destinations. This simple, concrete exercise will immediately clarify whether crossing state lines will truly transform your retiree budget or merely shift your expenses from one column to another.