Taking legitimate tax deductions keeps more of your hard-earned money in your pocket, but claiming certain breaks can inadvertently trigger an audit. Navigating the tax code during retirement requires precision, especially as recent IRS funding surges have increased scrutiny on complex returns. You need to understand exactly which write-offs draw the attention of federal examiners so you can claim your rightful benefits without fear. From out-of-pocket medical expenses to charitable contributions and small business deductions, knowing the rules protects your retirement income. By organizing your records and applying current tax laws correctly, you can confidently lower your tax bill while keeping your financial life secure and entirely off the federal radar this filing season.

The Current Tax Landscape for Retirees

The transition into retirement fundamentally changes your income profile. Rather than relying on a predictable employer paycheck, you now manage a complex web of withdrawals from deferred accounts, federal benefits, and perhaps part-time income. Recent federal legislation has shifted the rules around required minimum distributions, giving you slightly more time before you must draw down certain retirement accounts. Simultaneously, sweeping budget appropriations have allowed federal tax authorities to modernize their technology and enhance enforcement algorithms, significantly increasing the agency’s ability to scrutinize returns for statistical anomalies.

When you combine complex retirement income streams with enhanced federal oversight, understanding exactly how your IRS tax breaks appear to federal computers becomes crucial. The standard deduction currently sits at historically high levels, and taxpayers aged 65 and older receive an additional standard deduction amount. Because of this high threshold, itemizing your deductions only makes mathematical sense if your total allowable expenses exceed that figure. Those who do choose to itemize often present returns with unusually high deduction claims. This scenario inherently increases your IRS audit risk and invites examiners to demand supporting documentation.

Red Flag 1: High Out-of-Pocket Medical Expenses

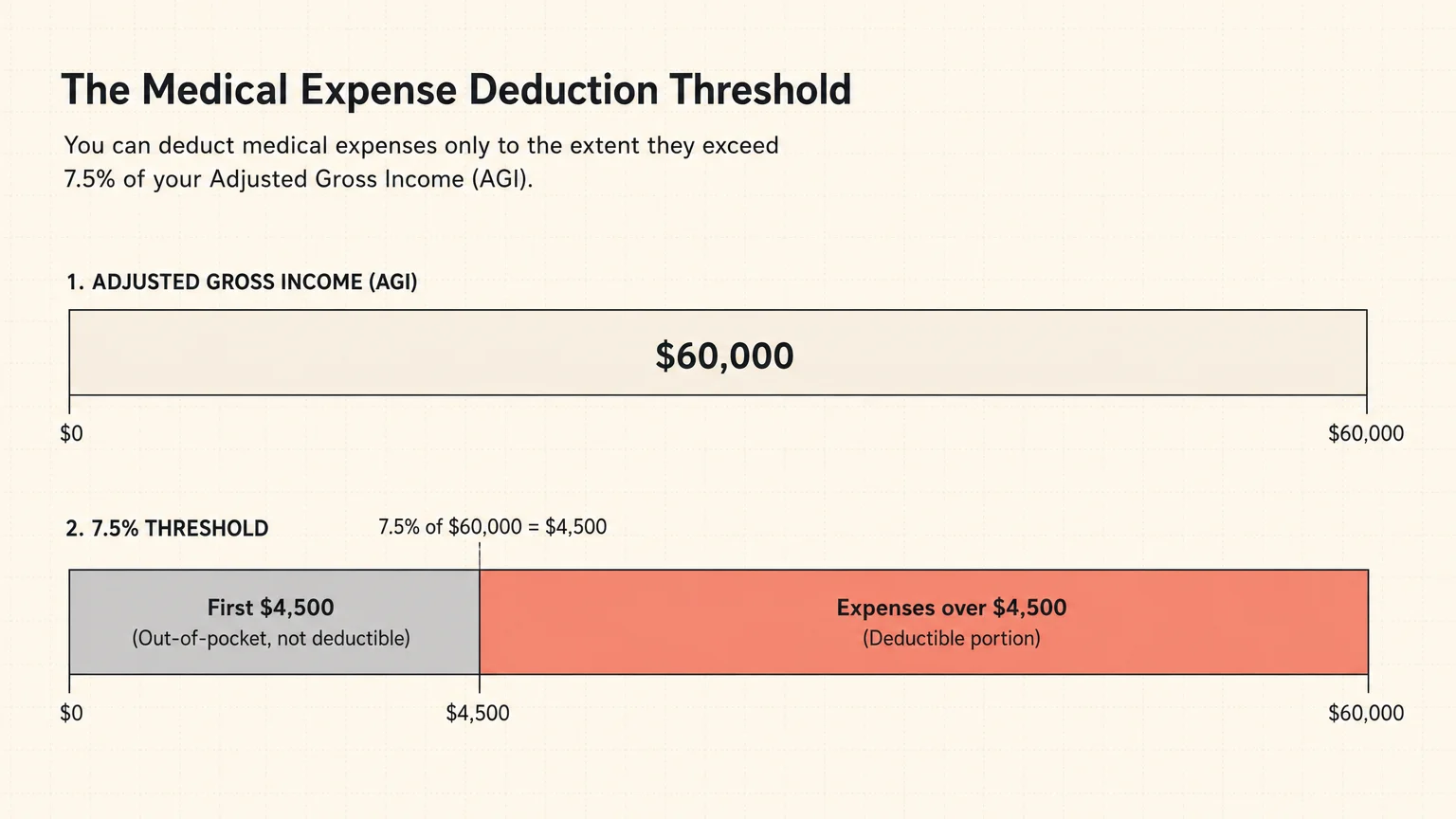

Navigating health and wellness remains a primary focus during your retirement years, and the associated costs can quickly erode a fixed budget. The tax code provides relief by allowing you to deduct qualified medical and dental expenses, but a strict mathematical threshold turns this common deduction into a frequent stumbling block. You can only deduct out-of-pocket medical expenses that exceed 7.5 percent of your adjusted gross income.

For example, if your adjusted gross income totals $60,000, you must absorb the first $4,500 of medical costs yourself; only the expenses rising above that specific figure offer any tax benefit. Misunderstanding this calculation constitutes one of the most common tax return errors among older adults. Taxpayers frequently attempt to deduct their entire medical spend, which immediately triggers an automated review. Furthermore, the definition of a qualified medical expense remains strictly regulated. While you can deduct premiums for long-term care insurance, medically necessary home modifications, and prescription copayments, you cannot write off over-the-counter vitamins, standard gym memberships, or generalized wellness retreats.

To fortify your return, you must maintain pristine physical or digital records of every medical bill, pharmacy receipt, and travel log for medical appointments. The official Medicare portal offers extensive guidance on tracking your healthcare costs and managing your out-of-pocket limits effectively. Organizing your health expenses meticulously ensures your health-related deductions withstand any federal inquiry.

Red Flag 2: Charitable Contributions Without Proper Documentation

Designing a purposeful lifestyle in retirement often involves supporting causes that matter to you. Philanthropy offers deep personal satisfaction, and the federal government rewards your generosity with corresponding tax breaks. However, large charitable contributions consistently attract scrutiny, particularly when those donations involve non-cash assets. Donating an old vehicle, transferring shares of appreciated stock, or giving away valuable artwork can significantly lower your taxable income, but you must follow strict appraisal rules.

If you claim a non-cash deduction exceeding $500, you must file a specific tax form detailing the donation. If the value surpasses $5,000, the law requires a formal, written appraisal from a qualified professional. Attempting to estimate the value of donated household goods without objective evidence frequently raises red flags. For many retirees, a safer alternative exists in the form of Qualified Charitable Distributions.

If you are aged 70 and a half or older, you can transfer funds directly from your individual retirement account to an eligible charity. This strategy counts toward your required minimum distributions but keeps the withdrawn amount entirely out of your adjusted gross income. By lowering your top-line income rather than relying on itemized deductions, you simplify your tax filing. To understand the broader impact of philanthropy on older adults, you can review insights provided by the AARP research and policy divisions, which highlight how structured giving enhances community well-being while optimizing your financial health.

Red Flag 3: Deducting Hobby Expenses as a Small Business Loss

Many retirees choose to monetize their lifelong passions, turning activities like woodworking, freelance consulting, or vintage antiquing into supplemental income streams. This active approach to income planning supports both your mental acuity and your household budget. When you operate a legitimate small business, you can deduct associated expenses such as equipment, travel, and marketing.

The danger arises when your enterprise consistently operates at a loss. The federal government draws a strict line between a profit-seeking business and a personal hobby. If your endeavor fails to generate a profit in at least three out of five consecutive years, examiners will likely reclassify the activity as a hobby. Under current tax laws, you cannot deduct hobby expenses, meaning any previously claimed business losses could be disallowed, resulting in steep penalties and back taxes.

To prove your activity functions as a genuine business, you must treat it like one. This means maintaining a separate bank account, developing a formal business plan, securing the proper local licenses, and keeping rigorous accounting records. Engaging in the gig economy requires intentional financial planning, and keeping your personal and business finances segregated provides your best defense against an audit. The Bureau of Labor Statistics provides detailed data on the rising participation of older Americans in the independent workforce, illustrating just how common these post-career ventures have become. Protect your newfound enterprise from avoidable tax filing mistakes by formalizing your operations.

Red Flag 4: The Home Office Deduction

Alongside the rise of post-career small businesses comes the frequent use of the home office deduction. Claiming a portion of your living space as a business expense offers a valuable tax shield, allowing you to write off a percentage of your utilities, insurance, property taxes, or mortgage interest. However, this specific write-off has historically been a magnet for federal auditors because taxpayers frequently misinterpret the exclusive and regular use requirement.

To legally claim this deduction, the space you use for your business must be dedicated entirely to that purpose. A laptop set up on your dining room table or a desk situated in a guest bedroom that also houses your visiting grandchildren does not qualify. The area must be your principal place of business and used exclusively for work.

If you meet this rigorous standard, you can choose between calculating your actual expenses based on the square footage of the office relative to your entire home, or utilizing the simplified method. The simplified method provides a standard dollar amount per square foot up to a maximum limit, greatly reducing the required math. Measuring your space accurately and taking photographs of your dedicated office setup can save you immense frustration later. Providing precise, factual data demonstrates to any potential auditor that you understand and respect the boundaries of the tax code.

Expert Voices: Perspectives on Audit Prevention

Financial professionals and gerontologists note that the transition into fixed-income living requires a fundamental shift in how you manage administrative tasks. Certified Financial Planner professionals emphasize that proactive tax planning prevents costly reactive measures. Rather than scrambling to find receipts in April, experts recommend digitizing your records throughout the entire year. Taking photographs of receipts and logging mileage immediately after a business or medical trip ensures your data remains accurate and accessible.

Furthermore, researchers studying cognitive changes and financial decision-making in older adults highlight that simplifying your financial life reduces the risk of costly errors. Consolidating scattered investment accounts and setting up automated tax withholding on your pension and Social Security benefits can dramatically reduce the complexity of your annual return. When your financial picture remains clear and organized, you reduce the likelihood of making arithmetic errors or omitting critical income documents. Working alongside a trusted fiduciary or a certified public accountant provides an essential layer of security, ensuring an objective expert reviews your strategy before you submit your final documents to the government.

Safeguards: Avoiding Scams and Benefit Cliffs

As you navigate complex deductions, you must also protect yourself from external threats and hidden financial traps. Tax-related identity theft and ghost preparer scams aggressively target older adults. A fraudulent preparer might promise unusually large refunds, base their fee on a percentage of your return, and ultimately refuse to sign the tax document, leaving you entirely liable for their fabricated deductions. Always verify your preparer’s credentials through official federal databases and remember that legitimate authorities will never initiate contact demanding immediate payment via text message, wire transfer, or gift card.

Beyond outright fraud, you must also monitor how your tax strategies impact other retirement benefits. Claiming certain deductions or realizing large capital gains can inadvertently push your adjusted gross income over specific thresholds, triggering a benefit cliff. The most prominent example is the Medicare Income-Related Monthly Adjustment Amount, commonly known as IRMAA. A sudden spike in your reported income can lead to significant surcharges on your Part B and Part D premiums two years down the line. You can explore the mechanics of how your earnings impact your benefits through the Social Security Administration resources, which offer comprehensive guides on managing your income thresholds. Careful income planning ensures that a minor tax victory today does not result in a massive healthcare expense tomorrow.

Frequently Asked Questions

How long should I keep my tax records and supporting documents after retiring?

You should retain all tax returns and supporting documentation for at least three years from the date you filed your original return, or two years from the date you paid the tax, whichever is later. However, if you omit more than 25 percent of your gross income, the government can audit you for up to six years. For documents related to property purchases, business assets, or home improvements, you must keep the records for as long as you own the asset plus the standard three-year window, as these figures determine your taxable gain when you eventually sell.

Can I deduct my monthly Medicare premiums as a qualified medical expense?

Yes, you can include your Medicare Part B and Part D premiums, as well as premiums for supplemental Medigap policies, in your calculation for medical deductions. However, these premiums must be combined with your other out-of-pocket medical costs, and the grand total must still exceed the 7.5 percent adjusted gross income threshold before you see any tax benefit. If your premiums are automatically deducted from your Social Security checks, you must still track these amounts for your itemized deductions.

What exactly triggers an automatic review of my tax return?

Automated computer systems scan every submitted tax return, comparing your numbers against statistical norms for your specific income bracket. If your charitable deductions, business losses, or medical expenses fall wildly outside the average range for your peers, the system flags your return for human review. Additionally, simple mismatches—such as failing to report income from a 1099 form that the government already has on file—will generate an immediate automated notice requiring you to explain the discrepancy.

How do I correctly report the volunteer miles I drive for a registered charity?

When you drive your personal vehicle in service of a qualified charitable organization, you can deduct a set rate per mile driven. To claim this deduction legally, you must maintain a contemporaneous logbook. This means you must record the date, the number of miles driven, the specific charitable purpose of the trip, and the destination at the exact time the driving occurs. Trying to estimate your mileage at the end of the year violates the documentation rules and will likely be disallowed upon review.

Your Next Step

Taking control of your tax strategy empowers you to protect your wealth and enjoy your retirement with total peace of mind. Over the next 48 hours, establish a dedicated and secure physical folder or an encrypted digital drive labeled with the current tax year. Place your most recent medical receipts, charitable donation acknowledgments, and any side-business invoices directly into this new hub. By organizing your records today, you eliminate the stress of tax season, ensure you capture every legitimate deduction, and build an airtight defense that keeps your finances safe, secure, and ready for whatever the future holds.