Understanding the hidden rules of Medicare and Social Security can add thousands of dollars to your retirement income and prevent devastating healthcare bills. With over ten thousand Americans turning sixty-five every day, the retirement landscape demands sharp financial vigilance and a proactive approach to your hard-earned benefits. Many retirees unknowingly forfeit a substantial portion of their guaranteed income or face lifetime penalties simply because they miss critical enrollment windows or misunderstand taxation thresholds. You worked decades to secure these lifelines; knowing precisely how to maximize them ensures your fixed budget covers everything from daily expenses to sudden medical needs.

Navigating the Current Policy Landscape

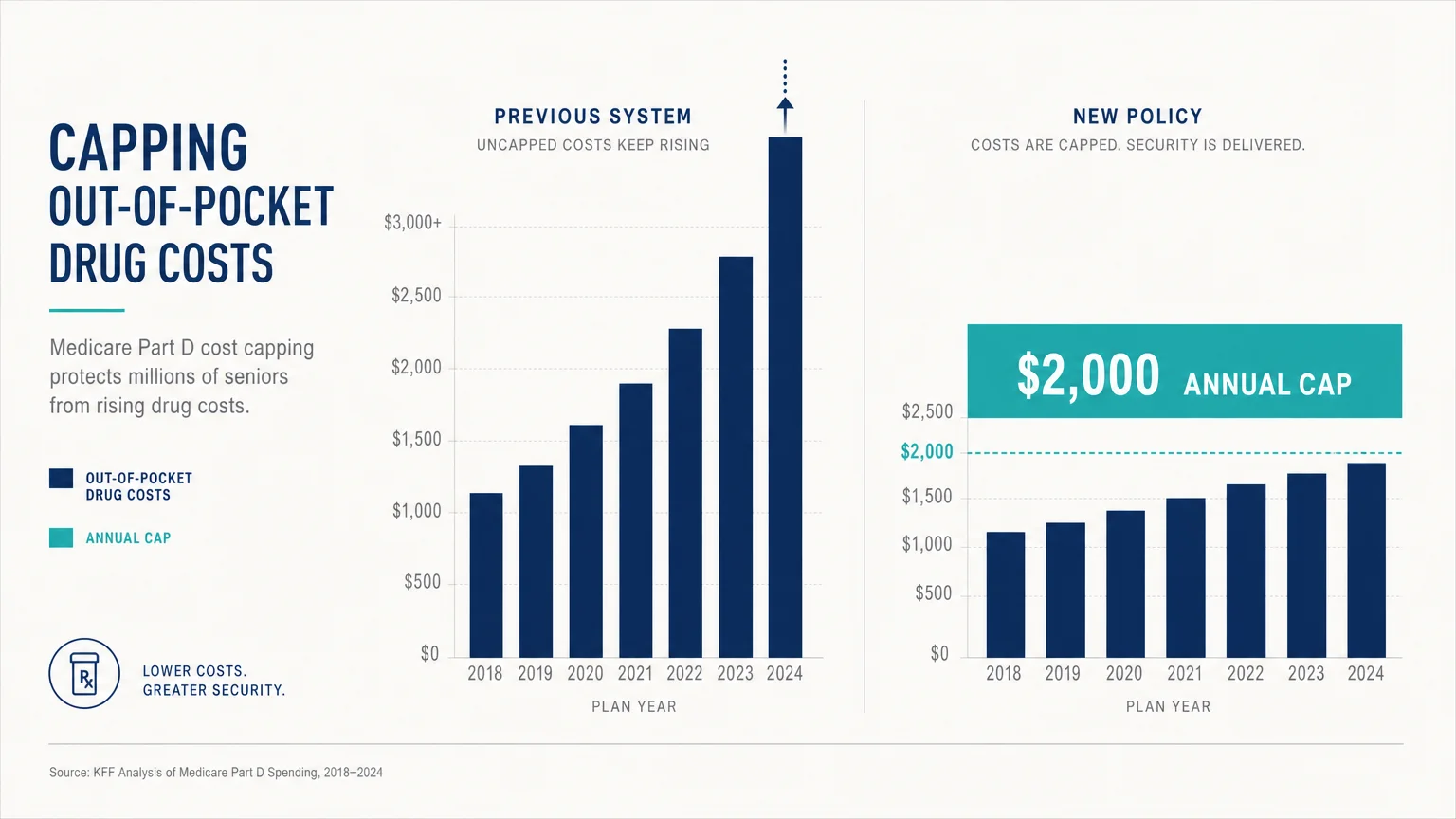

Recent legislative changes have drastically altered the financial framework of retirement in the United States, providing significant relief for older adults on fixed incomes. Chief among these updates is the restructuring of prescription drug costs under Medicare Part D. Thanks to the historic implementation of the Inflation Reduction Act, you now benefit from a strict two thousand dollar annual out-of-pocket cap on prescription medications. This crucial reform eliminates the catastrophic financial burden that previously derailed retirement plans when retirees faced sudden diagnoses requiring expensive specialty drugs. By capping your maximum pharmacy spend across the calendar year, this policy creates predictability for your budget, allowing you to reallocate reserved emergency funds toward travel or wealth preservation.

Beyond healthcare, inflation continues to shape the purchasing power of your Social Security benefits. While annual Cost of Living Adjustments attempt to bridge the gap between fixed incomes and rising consumer prices, the reality often falls short of capturing the true inflation rate for older Americans. Costs for housing, medical care, and specialized transportation frequently outpace the headline inflation metrics tracked by the federal government. Recognizing this disparity empowers you to adjust your personal savings withdrawal rate rather than relying entirely on annual government adjustments to maintain your standard of living.

You must actively monitor these shifting policies to protect your financial independence. A robust retirement plan treats government benefits not as static guarantees, but as dynamic assets requiring ongoing management. Incorporating these modern realities into your financial blueprint prevents unpleasant surprises and equips you with the necessary foresight to weather broader economic uncertainties with total confidence.

Strategic Income Planning Through Social Security

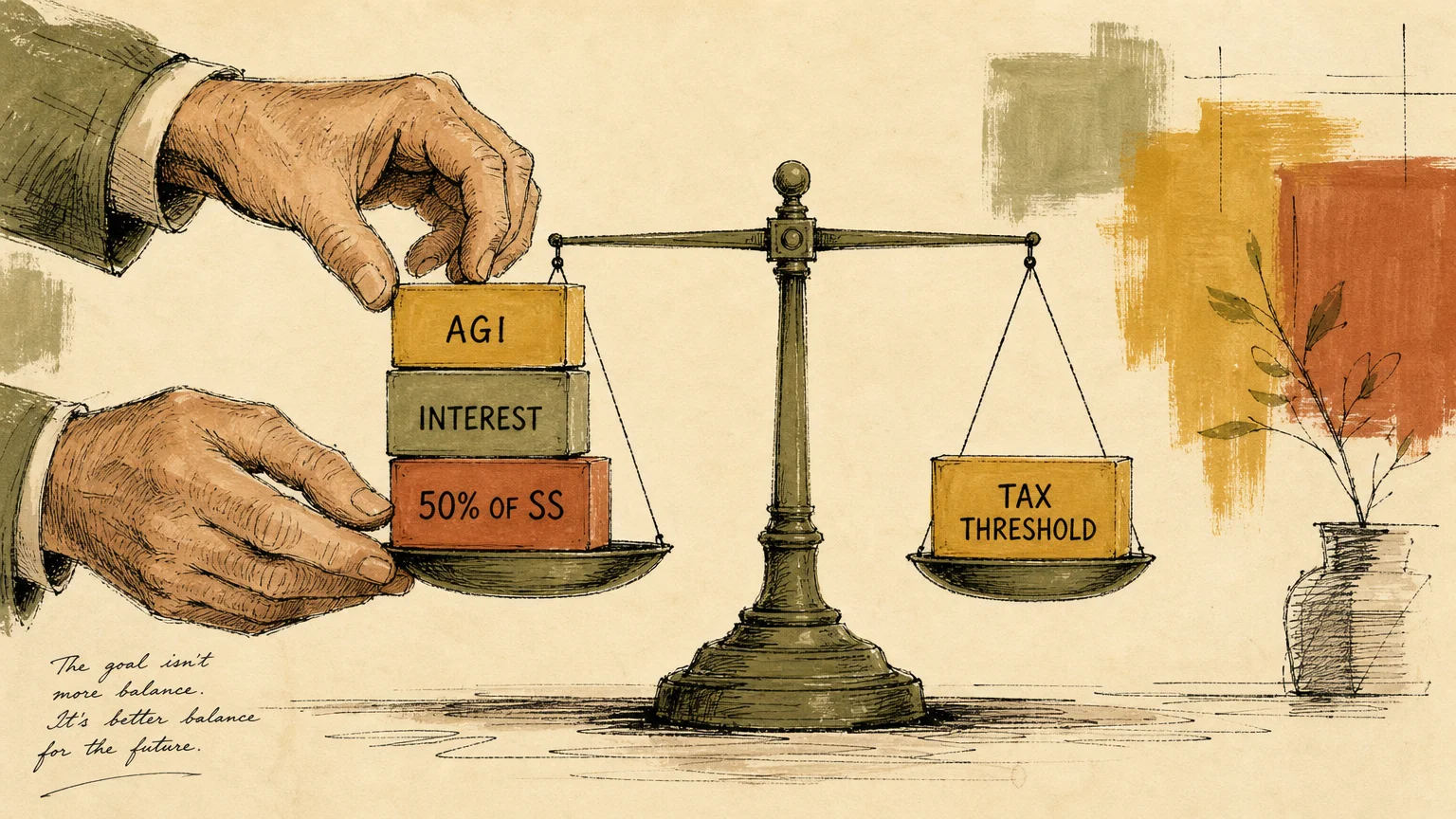

Most retirees view Social Security simply as a monthly check, entirely overlooking the complex tax implications embedded in the system. The Internal Revenue Service utilizes a metric called provisional income to determine how much of your benefit faces federal taxation. Provisional income combines your adjusted gross income, non-taxable interest, and exactly half of your Social Security benefit. If this figure exceeds specific thresholds, up to eighty-five percent of your payments become taxable. You can dramatically reduce this burden by strategically sequencing withdrawals from Roth accounts and traditional IRAs to keep your provisional income below critical trigger points.

Another frequently misunderstood component involves spousal and survivor benefits, which directly impact the long-term financial security of surviving partners. When the higher-earning spouse chooses to claim Social Security early, they permanently lock in a reduced monthly payout for themselves—and simultaneously reduce the maximum survivor benefit their partner will eventually receive. Financial planners consistently emphasize that delaying the higher earner’s claim until age seventy provides the ultimate longevity insurance for a surviving spouse. This strategy holds particular importance for families managing varying health trajectories or multi-generational households where extended family members rely on the stability of the primary retiree’s income.

Furthermore, individuals choosing to work part-time before reaching their Full Retirement Age often fall into the earnings test trap. If you claim benefits early while continuing to work, the Social Security Administration temporarily withholds a portion of your benefits once your employment income surpasses an annual limit. While these withheld funds eventually return to you in the form of a higher monthly payment after you reach Full Retirement Age, the immediate cash flow reduction can severely disrupt your lifestyle design. Understanding exactly how earned income interacts with early claiming strategies prevents accidental budget shortfalls during your crucial transition out of the full-time workforce.

Protecting Your Health and Wealth with Medicare Facts

Securing the right Medicare coverage ranks as one of the most consequential decisions of your later years, yet the intricate rules governing premiums frequently catch retirees off guard. The Income-Related Monthly Adjustment Amount stands as a prime example of a hidden healthcare cost. This federal surcharge increases your Medicare Part B and Part D premiums based on your modified adjusted gross income from two years prior. A single financial event—such as selling a lifelong home or executing a massive Roth conversion—can trigger massive premium spikes down the line. Because the government uses a strict two-year lookback period, anticipating these precise surcharges allows you to time your capital gains and large portfolio withdrawals strategically, protecting your monthly cash flow.

Choosing between Original Medicare paired with a Medigap policy and a Medicare Advantage plan demands careful consideration of your physical mobility and travel aspirations. Medicare Advantage plans heavily restrict you to localized networks of doctors and hospitals, which may severely limit your access to elite specialists if you develop a complex condition. Conversely, Original Medicare combined with a supplemental Medigap policy grants you the freedom to visit any facility nationwide that accepts Medicare. For retirees who split their time between different states or those prioritizing ultimate flexibility in their healthcare choices, the higher upfront premiums of Medigap often deliver superior long-term value and immeasurable peace of mind.

You must also navigate the unforgiving landscape of Medicare enrollment penalties. Missing your Initial Enrollment Period—the seven-month window surrounding your sixty-fifth birthday—results in permanent, compounding financial penalties applied to your monthly premiums for the rest of your life. Delaying enrollment under the false assumption that you do not need coverage immediately guarantees a more expensive future. By reviewing official guidelines provided by the Centers for Medicare & Medicaid Services, you ensure compliance with federal deadlines and shield your retirement savings from unnecessary taxes.

Designing a Purposeful Retirement Lifestyle

Optimizing your government benefits does far more than inflate your bank account; it serves as the foundation for a vibrant, purposeful chapter of life. When you eliminate the chronic anxiety associated with unpredictable medical bills and insufficient monthly income, you unlock the mental bandwidth necessary to pursue meaningful engagements. Gerontologists emphasize that financial security directly correlates with positive health outcomes by lowering stress and allowing older adults to invest in preventative wellness. Whether you dedicate your days to mentoring young professionals or volunteering, profound financial stability fuels your physical and emotional vitality.

Your living environment also plays a tremendous role in this holistic lifestyle design. Aging in place requires financial capital for home modifications—such as installing walk-in showers, widening doorways, lowering kitchen countertops, or building accessible ramps for varying mobility needs. The extra capital preserved through smart Medicare choices and tax-efficient Social Security strategies directly funds these vital renovations. This alignment between your wealth and your living space empowers you to remain deeply rooted in your preferred community. Ultimately, mastering your finances transforms retirement from a period of passive withdrawal into an era of active, joyful community participation and profound personal reinvention.

Expert Insights on Scams and Safeguards

As you navigate these complex benefit systems, you must remain intensely vigilant against the sophisticated criminal networks targeting American retirees. Fraudsters continuously evolve their tactics to separate you from your guaranteed income, frequently masquerading as federal agents. A prevalent scam involves unexpected phone calls from individuals claiming your Social Security number faces immediate suspension due to criminal activity. These imposters demand urgent payment via gift cards or wire transfers to resolve the fictitious issue. You must remember that authentic government agencies never initiate contact through threatening phone calls or demand immediate digital payments; all official communication arrives via secure, physical mail.

Healthcare fraud presents an equally devastating risk to your financial safeguards. Criminals routinely offer fake genetic testing kits or back braces, asking for your Medicare number to bill the government for services you never requested or needed. This medical identity theft compromises your medical records and complicates your ability to receive legitimate care. Consumer protection advocates from AARP strongly recommend reviewing your quarterly summary notices with a critical eye. Report any unfamiliar charges immediately to protect the integrity of your coverage. Furthermore, consulting a Certified Financial Planner acts as a powerful safeguard; these fiduciaries help you spot anomalies in your financial plans and build robust defense mechanisms against predatory schemes.

Frequently Asked Questions About Retirement Benefits

Can I change my Social Security claiming strategy after I apply?

Yes; the federal government provides a one-time opportunity to reverse your claiming decision within twelve months of your initial application. If you secure part-time employment or simply realize you claimed too early, you can file a formal withdrawal of application. You must repay every dollar you and your family received up to that point. Once you execute this repayment, your benefit record resets, allowing your future monthly payments to grow until you choose to reapply.

Does Original Medicare cover dental, vision, or long-term care?

Original Medicare excludes routine dental procedures, vision exams, hearing aids, and non-medical custodial care. Many retirees mistakenly believe the government funds nursing home stays, leading to catastrophic out-of-pocket expenses later in life. To cover these critical services, you must purchase a comprehensive Medicare Advantage plan that includes ancillary benefits, secure standalone dental and vision policies, or explore separate long-term care insurance solutions while you remain in good health.

How does working part-time affect my Social Security check?

If you claim Social Security benefits before reaching your Full Retirement Age and choose to remain in the workforce, your payments face a strict earnings test. The federal government temporarily withholds a portion of your benefits once your employment income surpasses an annual limit. While the government eventually recalculates your monthly benefit to restore these withheld funds over your remaining lifetime, the immediate loss of cash flow often shocks retirees relying on that income. Carefully calculating your projected part-time earnings prevents accidental budget shortfalls.

How does inflation actually impact my future benefits?

The government adjusts your benefits annually based on data from the Consumer Price Index for Urban Wage Earners and Clerical Workers, provided by the Bureau of Labor Statistics. While this adjustment prevents severe erosion of your purchasing power, it frequently lags behind the localized inflation rates of healthcare and housing. Consequently, you must maintain supplemental investment accounts to outpace real-world price increases effectively and guarantee your long-term prosperity.

Your Next Steps for a Secure Future

Mastering the complexities of your retirement benefits demands consistent attention, but the financial rewards justify every ounce of your effort. You hold the power to dictate how these federal programs serve your ultimate life goals. Instead of waiting for the government to dictate your income and healthcare access, take immediate action to secure your safety net. Within the next forty-eight hours, log in to your official federal portals to verify your earnings history, review your current healthcare coverage limits, and ensure your beneficiary designations reflect your current wishes. By implementing just one proactive change today, you build a resilient, impenetrable foundation that supports a truly thriving and joyous retirement.