Your monthly benefits are undergoing crucial adjustments this year, fundamentally altering how you structure your household budget and retirement timeline. With inflation stabilizing, the Social Security Administration instituted distinct policy shifts regarding your cost-of-living adjustment and the retirement earnings test limit. Navigating these shifts requires a proactive approach so you capture every dollar you deserve rather than leaving money on the table. Whether you already collect your checks or plan to claim them soon, mastering the nuances of this update empowers you to secure your financial foundation. Examining the direct impacts on your income, taxes, and healthcare premiums helps you weather economic fluctuations and enjoy the lifestyle you spent decades building.

Decoding the Policy and Market Updates Influencing Retirees

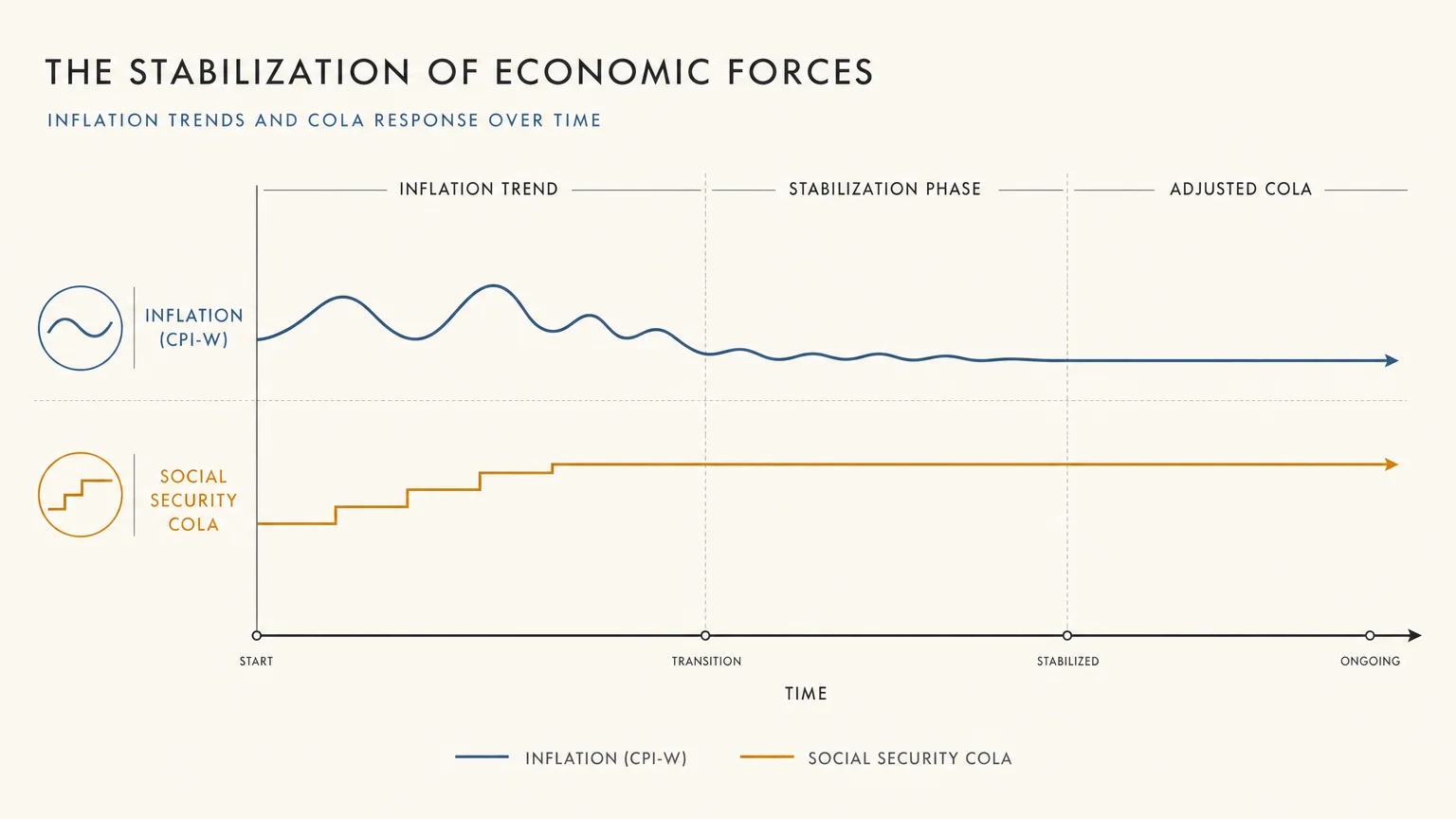

The landscape of federal retirement benefits constantly evolves, but the adjustments implemented this year carry unique significance for your daily financial reality. With the Bureau of Labor Statistics confirming a stabilization in consumer prices, the subsequent cost-of-living adjustment reflects a normalized economic environment. This moderation means you must maximize the efficiency of your existing income streams rather than relying on substantial bumps to offset rising household costs. Furthermore, the Social Security Administration updated the retirement earnings test exempt amounts; this structural shift allows individuals claiming benefits before reaching full retirement age to earn a higher wage without triggering a withholding of their checks. Understanding the interplay between these adjustments ensures you maintain a robust safety net during volatile economic cycles. View these policy updates not merely as administrative changes, but as essential variables in your comprehensive financial blueprint.

Strategy Pillar One: Income Planning and Benefit Optimization

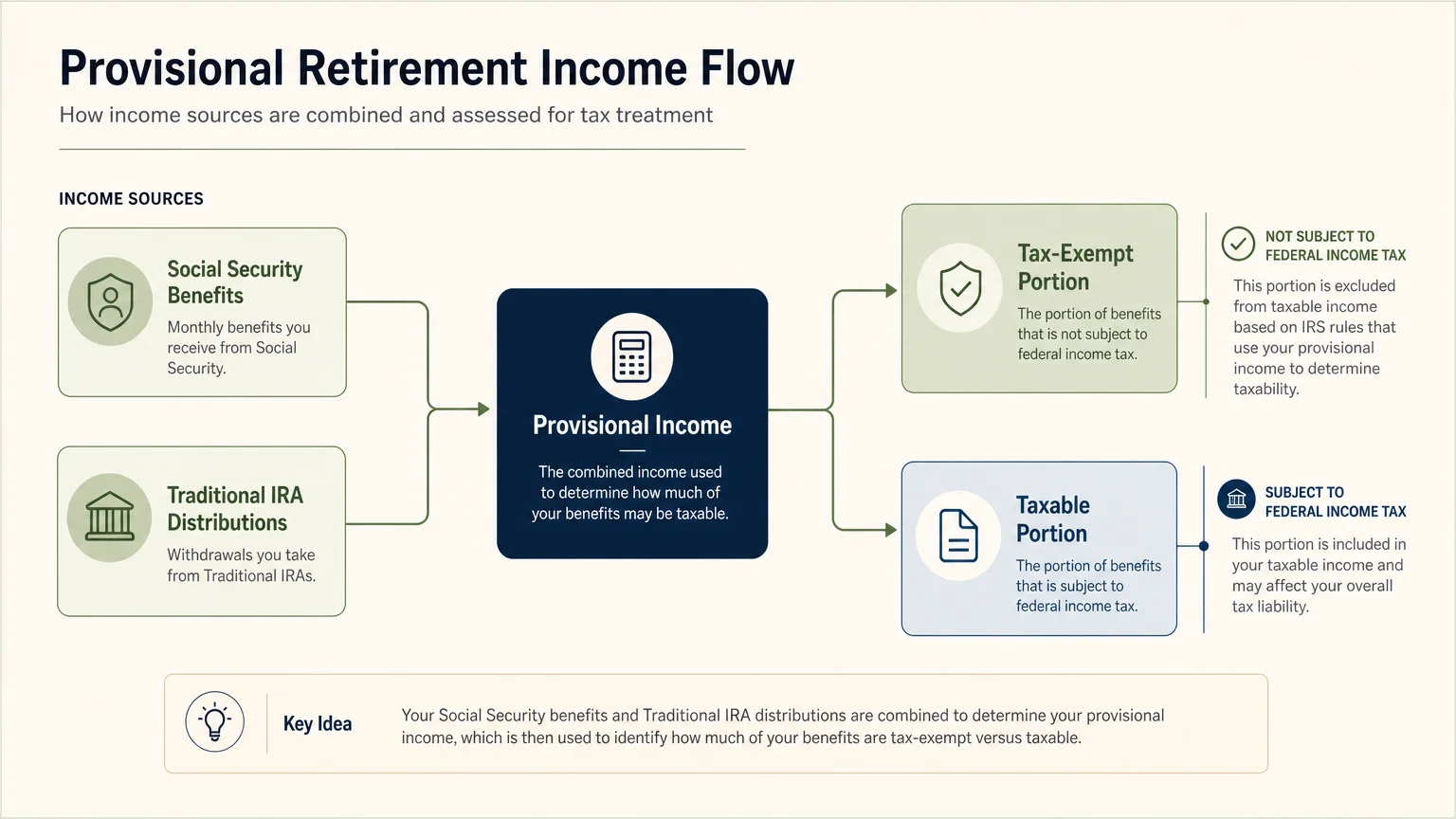

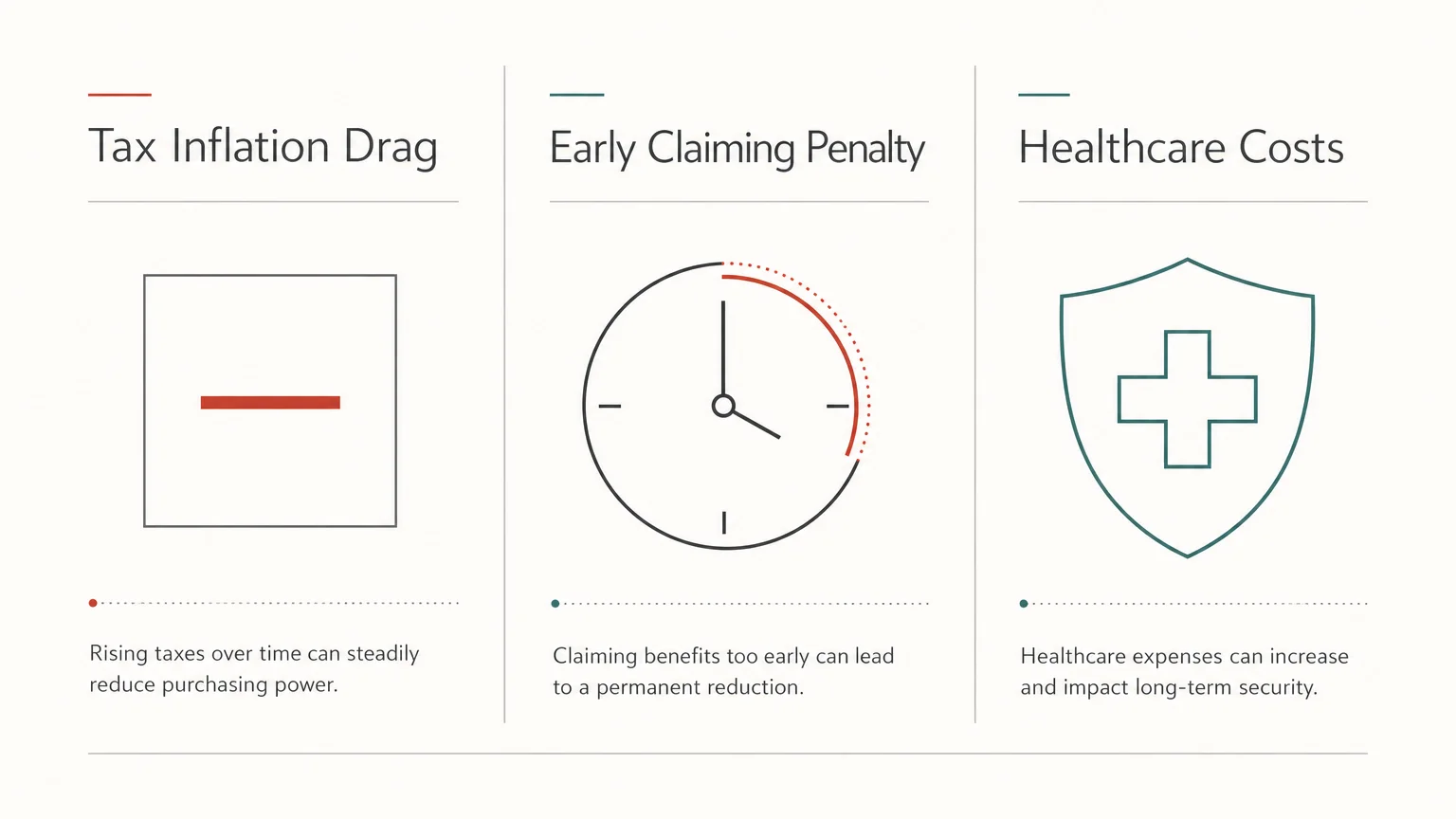

Developing a resilient income strategy requires you to analyze your net usable cash flow rather than just the gross amount of your monthly benefit. Many retirees operate under the persistent misconception that their federal benefits remain immune to taxation. However, depending on your combined income, a significant portion of your Social Security payments may become subject to federal income tax. The Internal Revenue Service establishes specific provisional income thresholds dictating this taxation. Because these thresholds remain unadjusted for inflation, more retirees face unexpected tax liabilities each year as their nominal income naturally grows. You must rigorously assess your withdrawals from traditional retirement accounts, as taking large taxable distributions could push your combined income over these rigid thresholds. Strategically timing distributions or utilizing targeted Roth conversions earlier in your retirement journey can mitigate this tax burden and preserve your purchasing power. Furthermore, if you choose to remain in the workforce while receiving early benefits, carefully monitoring your gross wages ensures you stay below the newly adjusted earnings limit, avoiding the temporary withholding of your hard-earned funds.

Strategy Pillar Two: Lifestyle Design Across Diverse Backgrounds

Translating your optimized income into a fulfilling routine represents the core of successful lifestyle design on a fixed budget. Social Security updates directly influence your capacity to engage in activities that bring you joy, lasting purpose, and community connection. Because mobility levels, familial obligations, and cultural backgrounds vary widely among retirees, a uniform approach to retirement living simply does not work. You might prioritize funding multi-generational family gatherings, or perhaps you prefer allocating resources toward accessible home modifications allowing you to age safely in place. By accurately forecasting your updated benefit amount after taxes, you can confidently designate funds for these deeply personal priorities. Engaging with local community centers, participating in subsidized lifelong learning programs, or exploring affordable domestic travel allows you to maintain a vibrant lifestyle without overextending your financial limits. You hold the ultimate power to dictate how your benefits support your unique definition of a life well-lived; meticulous budgeting transforms your monthly check into a passport for continued personal growth and exploration.

Strategy Pillar Three: Health, Wellness, and Medicare Integration

The intricate relationship between your benefits and ongoing healthcare expenses demands rigorous attention, particularly concerning the seamless integration of mandatory Medicare premiums. For the vast majority of beneficiaries, Medicare Part B premiums are deducted directly from Social Security payments before the funds ever reach their personal bank accounts. When the Centers for Medicare and Medicaid Services announce standard premium adjustments, these cost increases can significantly dilute the financial impact of your annual cost-of-living adjustment. You must factor these automatic deductions into your household cash flow projections to prevent unexpected budget shortfalls. Additionally, understanding the statutory hold harmless provision provides vital context; this protective rule prevents your Part B premium from increasing more than your cost-of-living adjustment, ensuring your net check does not decrease from one year to the next. However, this protection does not cover everyone—such as new enrollees or higher-income earners—so you must verify how these healthcare mandates interact with your specific financial profile. Prioritizing routine preventive health measures directly safeguards your federal benefits from being entirely consumed by escalating medical costs.

Expert Perspectives on Navigating Your Financial Future

Financial professionals and aging advocates consistently emphasize that adapting to these federal benefit updates requires both tactical precision and psychological resilience. Certified Financial Planner practitioners frequently observe that retirees who proactively model various income scenarios experience significantly less daily anxiety regarding market volatility and sudden policy shifts. By utilizing sophisticated financial forecasting tools, you can visualize exactly how updated earnings limits impact your portfolio over a twenty-year horizon. Gerontologists also highlight the undeniable connection between financial security and long-term cognitive health. When you remove the chronic stress associated with budget uncertainty, you free up vital mental bandwidth to focus on meaningful personal relationships and stimulating intellectual pursuits. Experts strongly advise against making reactive financial decisions based on sensationalized news headlines. Instead, consult credentialed fiduciary advisors who base their recommendations on peer-reviewed financial principles and legislative texts. Gathering actionable insights from professionals who specialize in comprehensive retirement planning empowers you to implement customized strategies that protect your legacy and enhance your daily quality of life.

Recognizing Risks and Safeguarding Your Retirement

As federal policies update and the broader economic environment shifts, malicious actors inevitably attempt to exploit the resulting confusion, making it absolutely imperative that you recognize and neutralize potential risks. Social Security-related scams proliferate rapidly during periods of transition. Fraudsters frequently pose as official government agents, utilizing highly threatening language to demand immediate payment or sensitive personal information under the false guise of updating your account. Legitimate government agencies will never demand wire transfers, cryptocurrency, or retail gift cards to resolve an alleged benefit issue; organizations like the AARP Fraud Watch Network track these evolving schemes to help you stay vigilant. Beyond outright criminal fraud, you must also guard against the subtle hazard of the benefit cliff. This troubling phenomenon occurs when a slight increase in your retirement income abruptly disqualifies you from essential assistance programs, such as subsidized senior housing or nutritional support. Carefully calculating how a modest adjustment impacts your eligibility for these income-based programs ensures you do not inadvertently lose access to highly valuable supportive services.

Frequently Asked Questions About Your Benefits

How does the new earnings limit affect my part-time job?

If you claim your federal benefits before reaching your designated full retirement age, the government places a strict cap on the amount of income you can earn from an employer without incurring a penalty. When your earned income exceeds this annual threshold, the administration temporarily withholds a portion of your monthly checks. You must track your gross wages closely to ensure your part-time employment enhances your overall financial standing. Once you reach full retirement age, this earnings restriction disappears entirely, allowing you to work as much as you desire without any reduction to your payments, effectively granting you the freedom to maximize both your career earnings and your hard-earned federal benefits simultaneously.

Will my Medicare Part B premium increase wipe out my annual adjustment?

Many retirees worry that rising healthcare costs will consume their entire cost-of-living adjustment, leaving them with no actual increase in disposable income. While the hold harmless provision protects most beneficiaries from seeing their net checks decrease strictly due to Part B premium hikes, it does not guarantee a larger bank deposit. If the premium increase absorbs the exact dollar amount of your annual adjustment, your net payment remains flat. You must review your annual notice carefully to understand exactly how premium changes impact your specific bottom line, allowing you to adjust your discretionary spending accordingly before the new year begins.

Are my monthly checks taxable under the current federal rules?

Yes, a substantial portion of your monthly benefits may become subject to federal income tax depending on your overall financial picture. The Internal Revenue Service utilizes a specific formula based on your combined income—which includes your adjusted gross income, nontaxable interest, and half of your Social Security benefits—to determine your exact tax liability. Because Congress has not adjusted these base income thresholds for inflation, more retirees cross the taxable line each year. Collaborate with a qualified tax professional to structure withdrawals from other retirement accounts strategically, minimizing this often-overlooked federal tax burden so that you retain control over a larger percentage of your overall retirement wealth.

How do I verify that my earnings history is accurately recorded?

Your ultimate benefit amount directly reflects the lifetime earnings history meticulously recorded by the government, making data accuracy essential to your financial wellbeing. You can review your personal earnings record by creating and accessing your secure online account through the official federal portal. Regularly verifying this data ensures you receive full credit for every dollar paid into the system throughout your career. If you spot a discrepancy, gather your old tax returns or original W-2 forms and submit a correction request promptly, as resolving administrative errors guarantees you receive your maximum earned monthly payment for the remainder of your retirement years.

Take Your Next Step Forward

Securing your financial independence requires you to transition from passively receiving information to actively managing your available resources. The adjustments to your federal benefits present a clear opportunity to optimize your income strategy, minimize tax liabilities, and fiercely protect your healthcare access. You possess the innate capability to align these vital updates with your personal long-term goals, ensuring your fixed income fully supports a dynamic lifestyle. Within the next forty-eight hours, log into your secure online federal portal to verify your earnings history and review your latest benefit statement. This single, decisive action establishes the foundation for a confident, well-funded retirement journey.