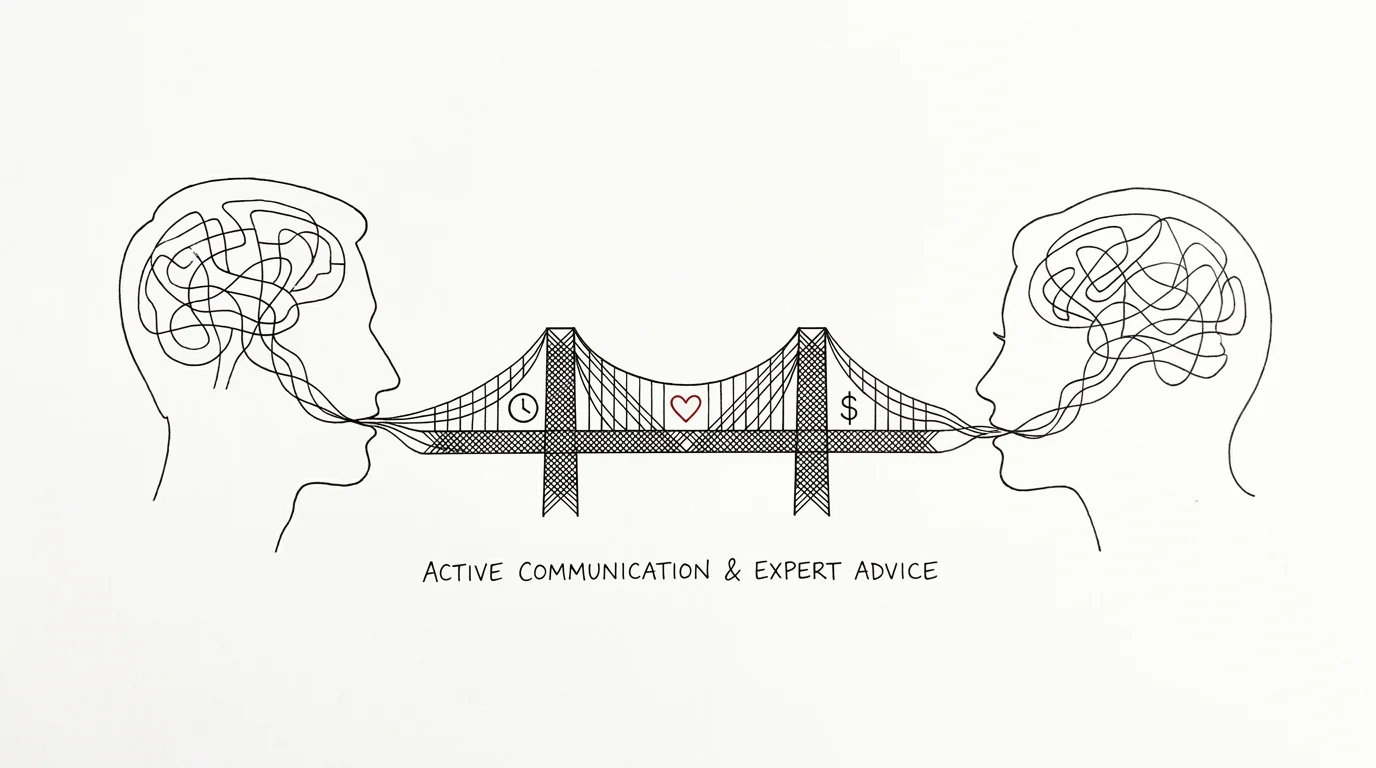

Stepping away from the daily grind and into retirement permanently reshapes the dynamic you share with your spouse, presenting both unexpected financial challenges and profound opportunities for connection. Navigating this transition requires more than just a solid pension plan; it demands active communication to align your evolving schedules, health needs, and individual goals. Recent data reveals that couples who proactively discuss their expectations experience significantly higher satisfaction during their golden years. Whether you are coordinating Medicare enrollment or figuring out how to spend uninterrupted days together, understanding these shifts helps you protect your bond and your budget. Preparing for the realities of constant companionship allows you to build a resilient, fulfilling partnership for the decades ahead.

The Current Landscape Shaping Retired Couples

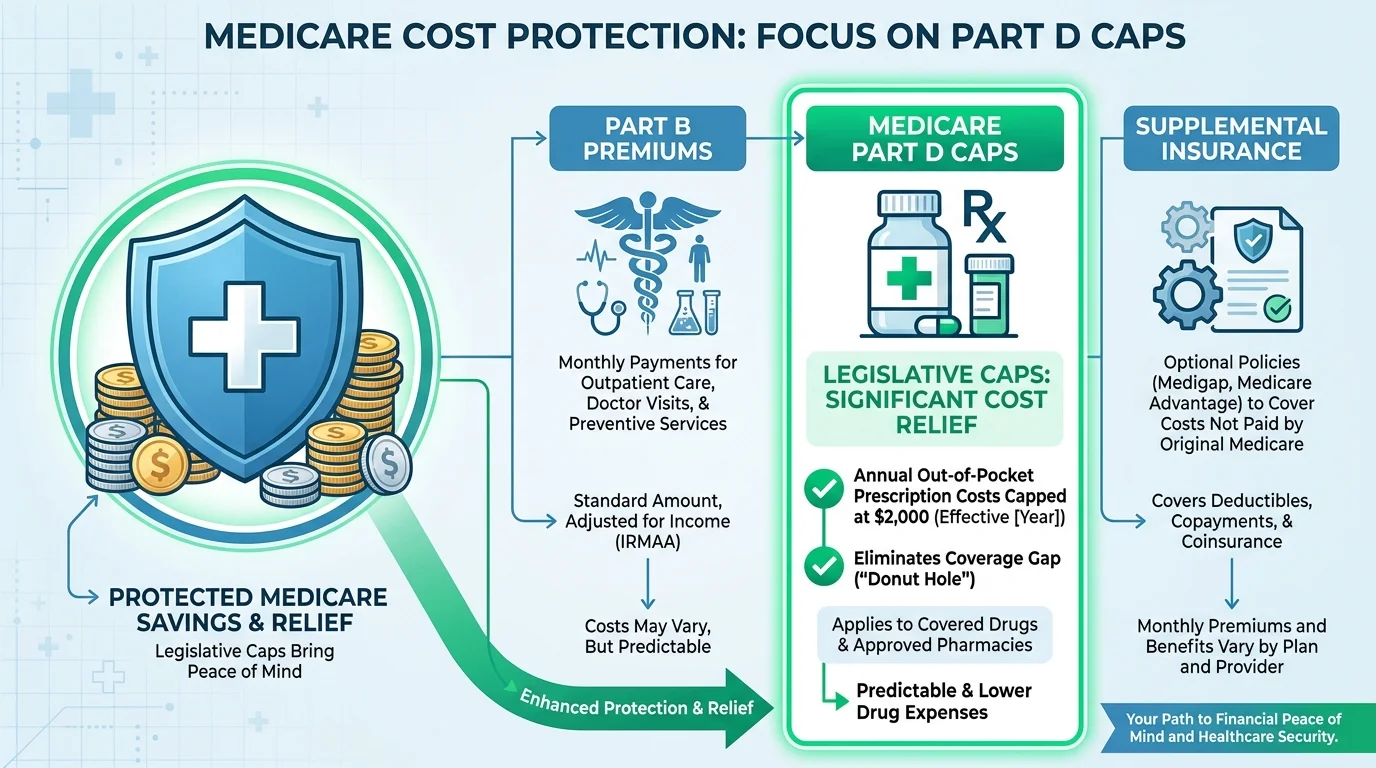

Modern retirement looks drastically different than it did a generation ago. Longer life expectancies mean you might spend thirty years in this phase, requiring your portfolio and your marriage to endure decades of economic shifts. Recent inflation has heavily pressured fixed incomes, forcing couples to ruthlessly rethink their purchasing power and daily spending habits. Simultaneously, healthcare policies continuously evolve, directly impacting your bottom line. For instance, recent legislative caps on Medicare Part D out-of-pocket costs bring much-needed relief to pharmaceutical budgets, yet navigating the broader Medicare landscape remains remarkably complex. You must adapt to these macroeconomic forces together. When you view market volatility, tax policy updates, and inflation through a unified lens, you transform external financial stressors into opportunities for teamwork. Tackling these challenges head-on strengthens your bond and creates a formidable defense against unpredictable economic tides.

Strategy Pillars: 10 Ways Retirement Changes Your Relationship

1. You must reinvent your daily routines

When you both worked, your days followed a rigid structure dictated by commutes, meetings, and office hours. Retirement suddenly drops forty to fifty unstructured hours into your weekly lap. Without the anchor of a traditional job, you and your spouse must consciously design how you spend your time. Many couples find themselves stepping on each other’s toes simply because they are unused to sharing the exact same space all day. You have to actively negotiate wake-up times, meal schedules, and leisure activities. According to data from the American Time Use Survey, retirees spend significantly more time on household activities and leisure. How you divide that time determines your marital harmony. Establishing intentional, structured routines prevents aimlessness and ensures you both feel productive.

2. Your household division of labor shifts dramatically

For decades, you likely operated under an established agreement regarding who handles the cooking, cleaning, yard work, and bill paying. When you retire, those old agreements quickly become obsolete. If you retire before your spouse, you might suddenly feel pressured to take on all domestic duties. Alternatively, if you both retire simultaneously, the spouse who previously managed the household might feel micromanaged by a partner who suddenly wants to reorganize the kitchen or optimize the grocery runs. You need to sit down and actively redistribute household chores based on your new energy levels and physical mobility. Treating the division of labor as an ongoing conversation helps prevent bitter resentment from taking root in your marriage.

3. Financial power dynamics require realignment

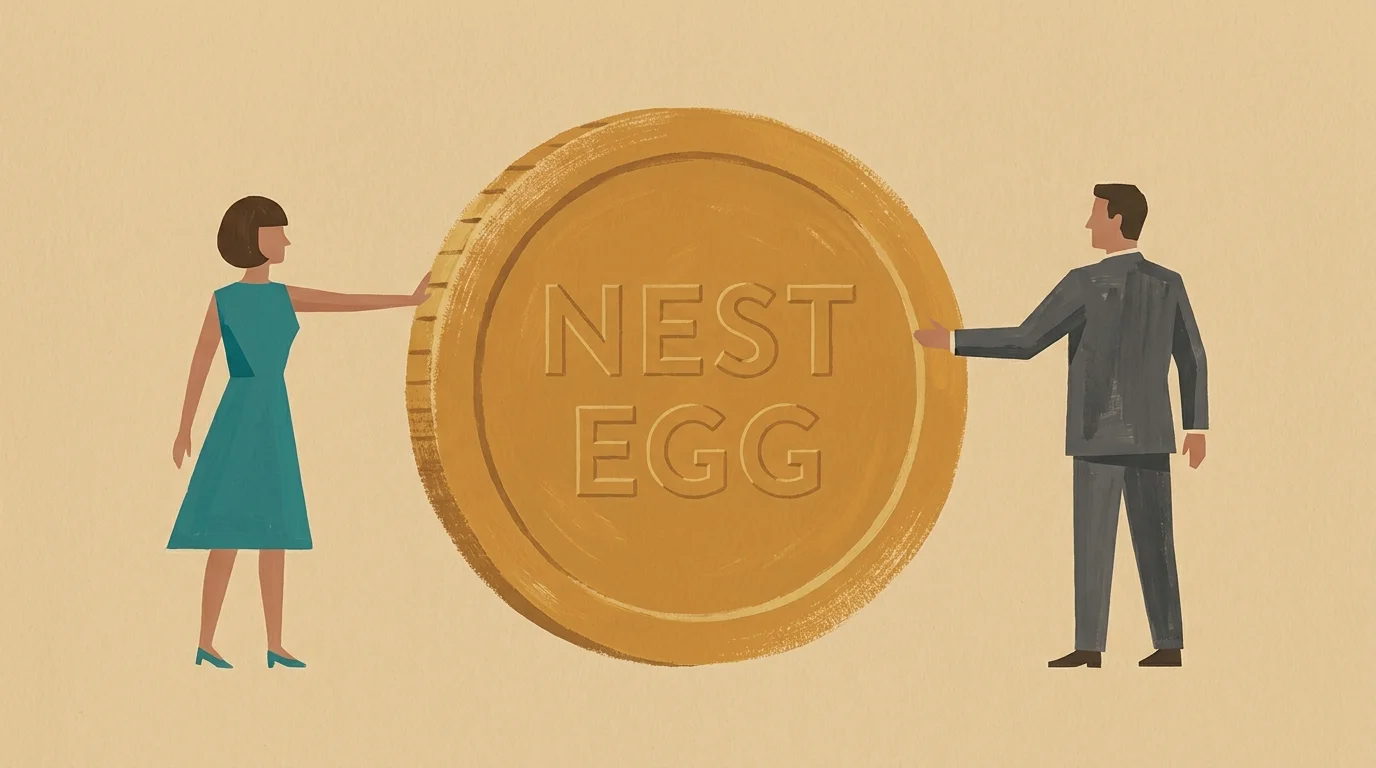

Transitioning from accumulating wealth to spending down your nest egg forces a major psychological shift that often disrupts marital power dynamics. The spouse who previously acted as the primary breadwinner might experience a loss of identity or control, while the partner who managed the day-to-day budget might feel intense anxiety about drawing money from investment accounts. You must shift your shared mindset from earning a paycheck to generating a synthetic paycheck from your portfolio. This requires complete transparency and joint decision-making. Equalizing your financial voice ensures both partners feel secure and respected, regardless of whose name happens to sit on the larger retirement account.

4. You face complex Social Security claiming decisions together

Deciding when to file for Social Security is not an individual choice; it is a joint strategic move that heavily impacts both of your lives. The age at which the higher-earning spouse claims benefits directly determines the survivor benefit available to the remaining spouse later in life. Claiming too early permanently reduces the monthly income the surviving partner will rely on when facing single-person household expenses. Utilizing resources from the Social Security Administration allows you to model different claiming scenarios. By thoughtfully coordinating your filing dates, you maximize your lifetime household income and provide a crucial financial safety net for your partner.

5. Healthcare costs become a shared financial focus

Medical expenses easily represent one of the largest line items in your retirement budget, and navigating this landscape requires intense teamwork. When you transition to Medicare, you face confusing enrollment windows, supplement choices, and fluctuating prescription drug costs. A single mistake by one spouse can drain your shared savings rapidly. Furthermore, you must monitor your combined income carefully to avoid triggering surcharges—such as the Income-Related Monthly Adjustment Amount—that inflate your Medicare premiums based on your joint tax returns. Treating healthcare planning as a joint financial priority protects your wealth and ensures you both secure the medical coverage necessary to enjoy a high quality of life.

6. Your need for personal space intensifies

Constant companionship sounds incredibly romantic in theory, but in practice, spending all day together often leads to unnecessary friction. You both require physical and emotional space to decompress, pursue individual interests, and maintain your sense of self. Many retirees experience “hovering spouse syndrome,” where one partner constantly shadows the other out of sheer boredom. You need to establish designated personal zones within your home where you can read, craft, or simply enjoy solitude without interruption. Encouraging each other to maintain solo hobbies and independent friendships creates a much healthier dynamic. Allowing yourselves time apart ensures that the time you do spend together remains engaging and meaningful.

7. Caregiving responsibilities begin to alter your dynamic

As you progress deeper into retirement, the odds increase that one of you will encounter health setbacks requiring the other to step into a caregiving role. This transition fundamentally shifts your relationship from a partnership of equals to a dynamic of caregiver and care recipient. The physical demands of lifting, managing medications, and driving to appointments can utterly exhaust the healthier spouse. You must proactively discuss your long-term care preferences before a medical crisis occurs. Exploring family caregiving resources together allows you to identify support systems like in-home aides or community respite programs. Planning for these inevitable health changes protects the caregiver’s wellbeing and preserves the dignity of your marriage.

8. You must merge conflicting spending and saving habits

Retirement heavily amplifies any existing financial personality clashes between you and your spouse. If you are a natural saver, watching your account balances fluctuate with the stock market might compel you to hoard cash and restrict activities. Conversely, if your spouse is a spender eager to check off bucket-list trips, they might view your frugality as an unnecessary barrier to enjoying their hard-earned freedom. Operating on a fixed budget demands that you find a middle ground. Creating a guilt-free personal allowance for each person helps quickly diffuse tension. Regular budget reviews allow you to adjust your spending based on actual market performance rather than fear, ensuring you compromise without sacrificing security.

9. Your social circles shrink and merge

Leaving the workforce severs your daily connection to colleagues and professional acquaintances, dramatically shrinking your independent social networks. Consequently, many retired couples turn completely inward, relying entirely on each other for conversation, entertainment, and emotional support. This intense mutual dependence places an unfair burden on your marriage. You simply cannot expect your spouse to fulfill every social role in your life. You need to actively build new, overlapping social circles by joining community groups, volunteering, or taking local classes. Fostering a robust network of friends outside of your marriage introduces fresh ideas into your household and prevents the deep isolation that often accompanies the later stages of retirement.

10. You redefine your legacy and end-of-life goals

Retirement provides the immense time and perspective necessary to confront uncomfortable conversations about your legacy. You and your spouse must align your visions for the future, which includes deciding how to distribute your accumulated assets and what charitable causes you wish to support. More importantly, you must openly discuss end-of-life care preferences, establish medical advance directives, and ensure your account beneficiaries are fully updated. Facing your mortality together requires deep vulnerability and immense trust. By formalizing your estate plans side-by-side, you remove dangerous ambiguity and ensure your final wishes reflect a unified front, ultimately providing profound peace of mind for both you and your loved ones.

Expert Voices on Navigating the Transition

Certified Financial Planners® and gerontologists consistently emphasize that successful retirement requires treating your marriage as an active, evolving partnership rather than an autopilot arrangement. Financial professionals advise that couples who schedule regular money meetings experience far less anxiety during severe market downturns; they heavily recommend complete transparency regarding account balances and withdrawal strategies. Similarly, aging researchers and psychologists note that maintaining independent identities dramatically reduces the friction associated with sudden, constant companionship. The consensus across both financial and relational fields is entirely clear: relying on outdated assumptions rather than explicit communication fractures relationships. You must treat this life stage as a completely new chapter that requires ongoing negotiation, abundant grace, and a willingness to compromise on everything from minor budget adjustments to major lifestyle overhauls.

Critical Risks and Safeguards for Your Nest Egg

Protecting your joint assets requires intense vigilance against emerging threats. Scammers aggressively target older adults, often attempting to drain joint accounts through sophisticated phishing, tech support frauds, or imposter schemes. You must establish an unbreakable rule that neither spouse authorizes significant financial transfers without consulting the other first. Additionally, you face severe structural risks like unexpected tax liabilities. Failing to accurately plan for Required Minimum Distributions can unexpectedly push you into a much higher tax bracket, increasing your Medicare premiums and drastically reducing your net income. Finally, the absence of a long-term care strategy remains the absolute greatest threat to a surviving spouse’s financial security. Purchasing insurance, earmarking specific investments, or exploring hybrid policies ensures that one partner’s sudden medical crisis does not bankrupt the other.

Frequently Asked Questions

How do we handle different retirement dates?

When one spouse retires before the other, jealousy and resentment easily surface. The working spouse might resent the retiree’s newfound leisure time, while the retiree might feel terribly lonely or burdened by expectations to manage the entire household single-handedly. You must set incredibly clear boundaries regarding chores and weekend activities to ensure both partners feel their time and efforts are respected.

What should we do if our travel goals clash?

Differences in travel aspirations usually stem from varying energy levels, physical mobility, or lingering financial anxieties. If you dream of expensive international excursions while your partner strongly prefers quiet local road trips, you must compromise through alternating destinations. You can also enthusiastically embrace solo travel or trips with friends, allowing you to fulfill your wanderlust without forcing an unwilling partner out of their comfort zone.

Does retirement typically increase the divorce rate?

Gray divorce—the phenomenon of couples splitting after age fifty—has surged significantly in recent decades. The sudden removal of busy career distractions often exposes deep, previously unaddressed fractures in a marriage. Proactive, honest communication and, when necessary, seeking professional relationship counseling provide the vital tools required to rebuild intimacy and successfully navigate the complex emotional terrain of this transition.

How can we maintain individual identities?

Preserving your unique individuality demands highly intentional effort. You must dedicate time and resources to hobbies, distinct friendships, and volunteer work that do completely not involve your spouse. Maintaining separate spheres of influence prevents emotional enmeshment, massively boosts your self-esteem, and ultimately gives you far more interesting things to discuss when you reconvene at the dinner table.

Take Action Today

Do not wait for friction to dictate your transition. Within the next forty-eight hours, sit down with your spouse and schedule a formal “state of our retirement” meeting. Brew a pot of coffee, put away your phones, and identify one specific area—whether it is your daily routine, your spending boundaries, or your social goals—that urgently needs realignment. Taking this single proactive step sets a commanding tone of teamwork and ensures you build a shared future filled with purpose and mutual respect.