Understanding how the Internal Revenue Service taxes your retirement income protects your life savings from unnecessary depletion and unexpected penalties. Navigating the modern tax landscape requires a proactive approach to managing your withdrawals, Social Security benefits, and healthcare premiums. Most people assume their tax burden drops the moment they stop receiving a traditional paycheck; unfortunately, this common misconception frequently leads to thousands of dollars in easily avoidable expenses. You might suddenly encounter stealth taxes hidden within Medicare premiums or confusing thresholds that turn your hard-earned benefits into taxable income. Mastering these nine specific tax surprises allows you to keep more of your wealth, preserve your fixed budget, and maintain the financial freedom you spent decades building.

The New Reality of Retirement Taxes

You might expect financial simplicity once you clock out for the final time; reality paints a much more complex picture. Legislative adjustments reshape retirement tax planning almost annually, demanding constant vigilance from anyone relying on fixed income streams. Recent data highlights a critical shift: while cost-of-living adjustments provide temporary relief, shifting tax brackets threaten to push thousands into higher marginal rates. Policy updates dictate exactly how and when you must withdraw your funds, requiring you to carefully balance traditional IRAs, Roth accounts, and taxable brokerage assets. Acknowledging this dynamic landscape empowers you to protect your wealth. Rather than reacting with panic every tax season, you can employ proactive strategies that optimize your withdrawals and preserve your purchasing power against rising living costs.

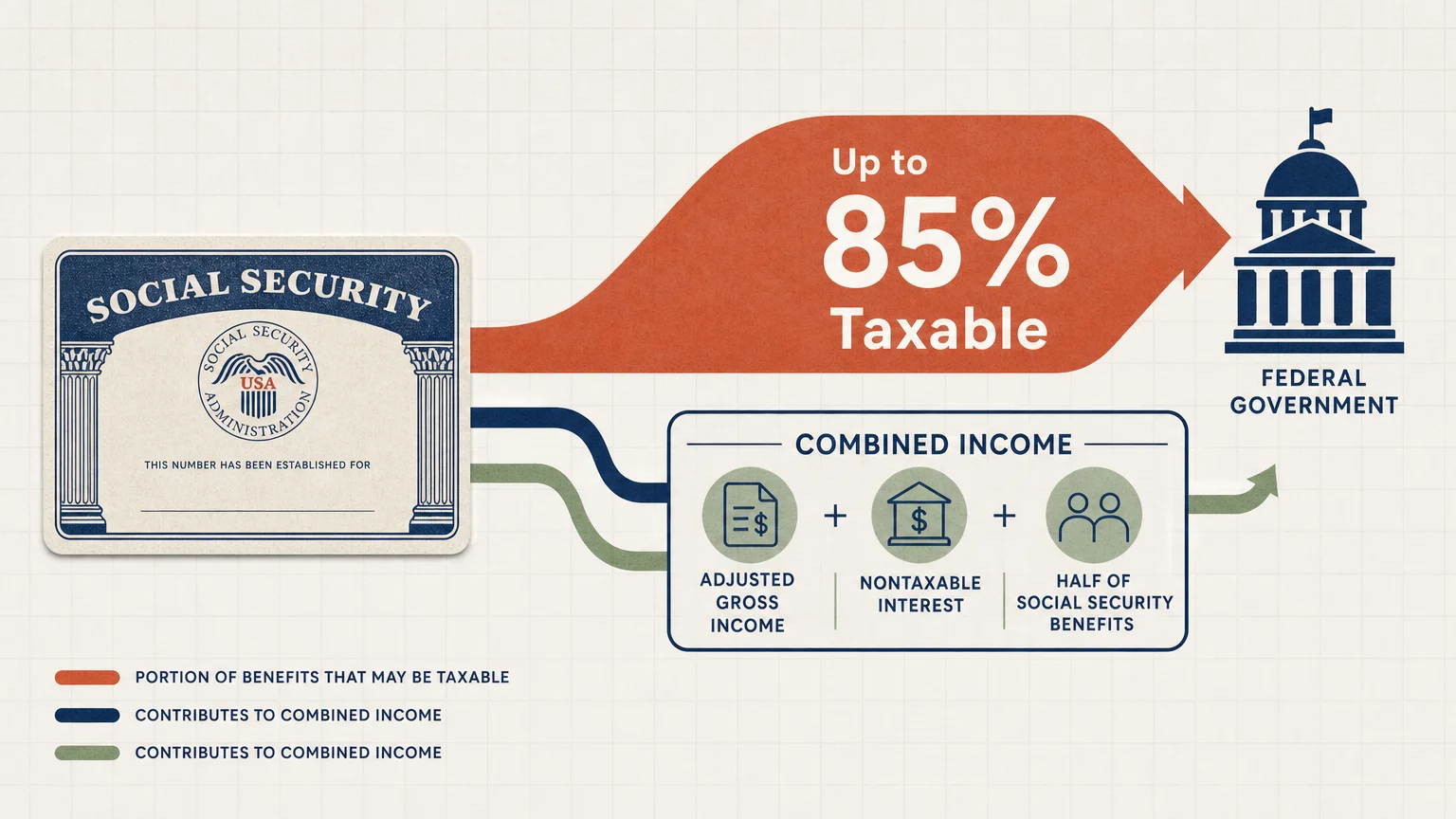

Surprise 1: The Taxation of Social Security Benefits

Countless pre-retirees mistakenly believe their monthly federal benefits are entirely tax-free. Depending on your combined income—which includes your adjusted gross income, nontaxable interest, and half of your Social Security benefits—the federal government can tax up to eighty-five percent of your payments. Because these threshold limits remain unadjusted for inflation since their introduction decades ago, normal wage growth continually drags more retirees into this tax trap. Pulling too much from a traditional 401(k) in a single year inflates your provisional income and unnecessarily subjects your safety net to taxation. Understanding the exact thresholds provided by the Internal Revenue Service ensures you do not hand a massive portion of your benefits back to the government.

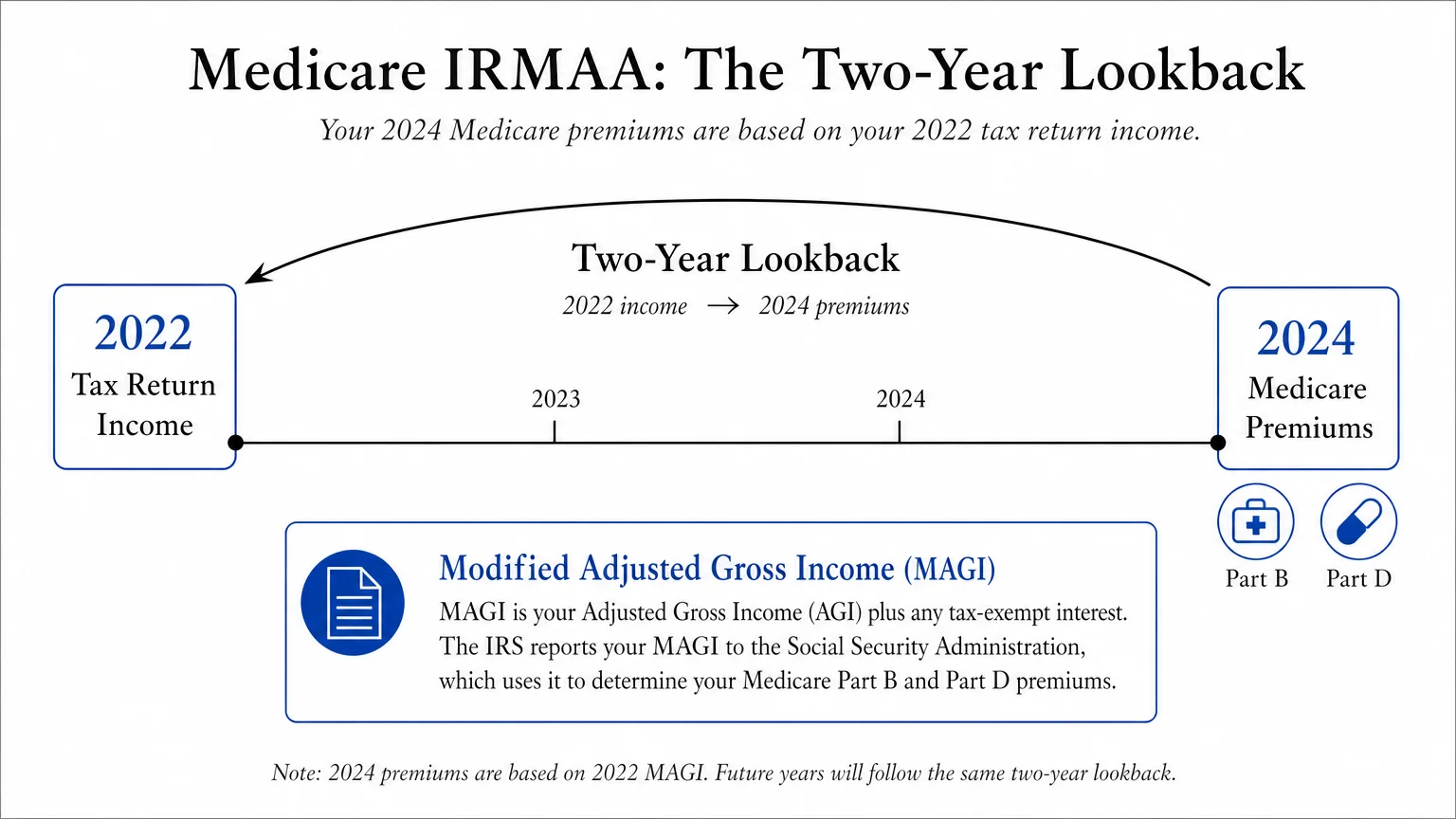

Surprise 2: Medicare IRMAA Surcharges

Healthcare remains one of the largest expenses in your golden years, yet the Income-Related Monthly Adjustment Amount catches many off guard. IRMAA operates as a stealth tax on your Medicare Part B and Part D premiums. If your modified adjusted gross income exceeds specific limits, you face steep surcharges added directly to your monthly healthcare bills. The most frustrating aspect involves the two-year lookback period; the premiums you pay this year depend entirely on the income you reported two years ago. Navigating Medicare.gov guidelines helps you project these thresholds accurately. Careful lifestyle design dictates that you spread out capital gains and large withdrawals over several years to maintain affordable, predictable medical coverage.

Surprise 3: Required Minimum Distribution Traps

The government eventually demands its share of the tax-deferred funds you spent a lifetime accumulating. Current legislation establishes the starting age for Required Minimum Distributions at seventy-three, granting you a specific runway for tax planning. Once you hit that age, you must withdraw a precisely calculated percentage of your traditional retirement accounts every single year. Failing to remove the exact amount triggers a severe penalty that consumes twenty-five percent of the unwithdrawn funds. These forced distributions often push you into higher tax brackets and trigger the aforementioned Medicare surcharges. Mitigating this risk requires a multi-year decumulation strategy, frequently involving strategic Roth conversions during early retirement to reduce the burden of future forced distributions.

Surprise 4: The Widow or Widower Penalty

Losing a spouse brings profound emotional devastation; unfortunately, the tax code compounds this grief with an unexpected financial blow. While your household income generally declines after a partner passes away, your tax status abruptly transitions from Married Filing Jointly to Single. This change slashes your standard deduction in half and significantly compresses your tax brackets. You might earn less total income but suddenly find yourself paying a substantially higher marginal tax rate. This widow penalty forces surviving spouses to drain their portfolios faster just to maintain their baseline standard of living. Comprehensive planning addresses this grim reality by maximizing tax-free growth vehicles and securing robust life insurance policies to create a reliable financial buffer.

Surprise 5: State Tax Inconsistencies on Retirement Income

Where you choose to plant your roots profoundly impacts your financial longevity. Retirees frequently relocate to secure a better climate or live closer to family; however, state tax laws vary wildly and hide expensive surprises. Several states completely exempt pension payouts and Social Security from taxation, while others tax nearly every dollar of your retirement income. Moving to a state with no income tax might seem like a brilliant lifestyle design choice until you encounter exorbitant property taxes designed to compensate for the lost revenue. Evaluating a new home demands a holistic assessment of the total tax burden. You must analyze your unique mix of assets to determine whether relocating actually improves your long-term financial outlook.

Surprise 6: The Ghost Tax of Capital Gains

Transitioning from a steady salary to portfolio withdrawals fundamentally changes how you view investment growth. Selling highly appreciated stocks, mutual funds, or real estate to fund your lifestyle triggers capital gains taxes that can swiftly erode your principal balance. If your overall taxable income crosses certain thresholds, you might also face the Net Investment Income Tax—an additional surcharge layered on top of your standard capital gains rate. Coordinating which assets to sell and when to sell them stands as a crucial component of preserving your wealth. Selling losing investments to offset your gains minimizes your overall liability and prevents you from needlessly paying thousands of dollars more than necessary to fund your retirement lifestyle.

Surprise 7: Phased Retirement and the Earnings Test

Modern retirees frequently redefine their golden years by working part-time, launching consulting businesses, or turning hobbies into profitable ventures. The Bureau of Labor Statistics tracks continuous growth in older workforce participation. Earning money while collecting early Social Security benefits triggers the earnings test, a mechanism that temporarily withholds a portion of your monthly checks if your wages exceed an annual limit. Navigating these rules via the Social Security Administration prevents you from inadvertently forfeiting your cash flow. While you eventually receive those withheld funds back as an adjusted payout after reaching full retirement age, the immediate disruption can destabilize your monthly budget and unnecessarily complicate your annual tax filings.

Surprise 8: Scams Targeting Tax-Advantaged Accounts

The complexity of the U.S. tax code creates a fertile breeding ground for malicious actors looking to exploit confusion. Cybercriminals constantly develop sophisticated methods to steal your identity, file fraudulent returns, or siphon funds from your IRAs. A common tactic involves criminals posing as federal agents demanding immediate payment for fictitious back taxes, leveraging the threat of arrest to panic their victims. Scammers specifically target older adults holding substantial assets in tax-advantaged accounts. Protecting yourself requires unwavering skepticism; legitimate government agencies never demand payment via gift cards or wire transfers. Utilizing resources from the AARP Fraud Watch Network helps you stay informed and adds vital layers of defense to your hard-earned retirement savings.

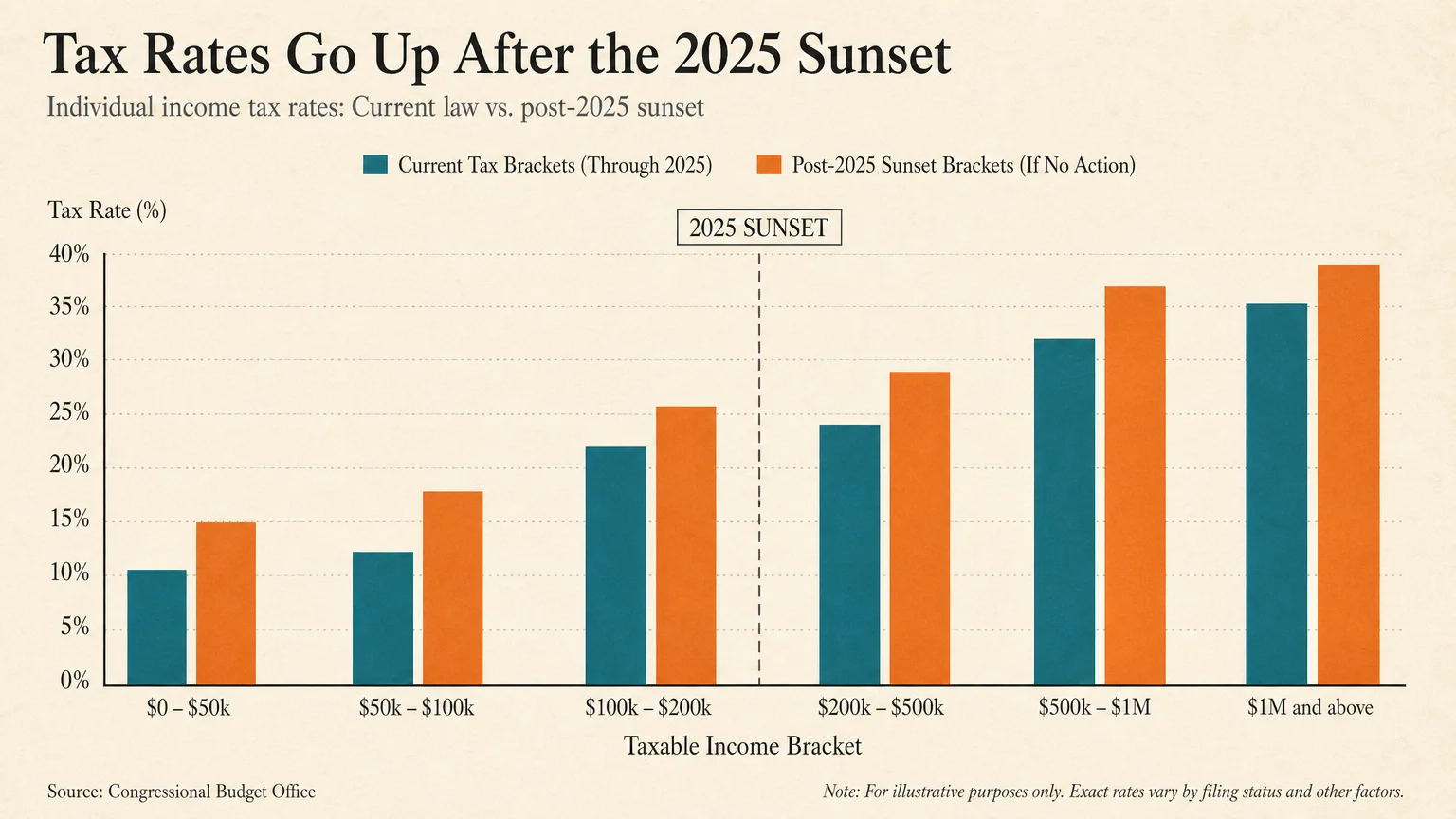

Surprise 9: The Aftermath of the Tax Cuts and Jobs Act Sunset

Legislation rarely remains permanent, and a massive tax shift recently became reality for anyone planning a multi-decade retirement. With the expiration of several Tax Cuts and Jobs Act provisions at the end of 2025, marginal tax brackets reverted to higher historical levels, and the standard deduction decreased for many households. Retirees who previously enjoyed minimal tax friction now face steeper tax hikes on their standard distributions and pension income. Recognizing this new legislative reality demands immediate strategic adjustments. Many financial professionals encourage thoroughly reviewing your withdrawal sequences and aggressively utilizing tax-efficient accounts to protect your future income from these newly reinstated, higher taxation levels.

Expert Voices on Building a Tax-Efficient Future

Mastering your financial destiny requires integrating diverse perspectives from those who study aging and wealth management. Certified Financial Planners consistently emphasize that tax diversification is just as crucial as asset diversification. Holding a strategic mix of taxable, tax-deferred, and tax-free accounts gives you the ultimate control over your annual taxable income, allowing you to manipulate your withdrawals efficiently. Gerontologists add a crucial human element to these mechanics, noting that financial anxiety severely impacts cognitive longevity. Stressing over an unexpected tax bill elevates cortisol levels and detracts from your joyful experiences. Retirees who build a resilient, tax-efficient framework consistently report higher levels of life satisfaction, replacing fear of the unknown with actionable confidence.

Frequently Asked Questions About Retirement Tax Planning

Do I still need to file a tax return if my only income is Social Security?

If your sole source of income consists of Social Security benefits, you generally do not need to file a federal return; however, you must closely monitor any supplemental income you earn. The moment your combined income surpasses the base threshold set by the government, a portion of your benefits becomes taxable, mandating that you file a return. Filing remains highly recommended even with minimal income to secure potential refundable credits and protect your identity from fraudsters attempting to file a fake return in your name.

How can I avoid paying taxes on my retirement income?

Achieving a completely tax-free retirement requires utilizing accounts funded with after-tax dollars. Roth IRAs and Roth 401(k)s stand as the premier vehicles for tax-free growth; qualified withdrawals from these accounts do not add a single cent to your taxable income. Additionally, utilizing Health Savings Accounts to cover qualified medical expenses provides a secondary stream of tax-free money. For your traditional accounts, careful planning allows you to withdraw just enough to stay within the standard deduction, effectively minimizing your federal tax liability for those specific dollars.

What happens if I miss my Required Minimum Distribution?

Failing to take your mandatory withdrawal triggers an incredibly steep penalty levied by the federal government. Recent legislation set this penalty at twenty-five percent of the unwithdrawn amount, with a further reduction to ten percent if you correct the mistake quickly. If you discover a missed distribution, you must withdraw the funds immediately and file a specific tax form to report the error. You can frequently attach a letter explaining that the shortfall occurred due to reasonable error—such as a medical emergency—and request a penalty waiver.

Can I deduct my Medicare premiums on my tax return?

You can deduct your Medicare premiums, but strict criteria dictate whether you actually receive a financial benefit. The IRS categorizes Part B, Part D, and supplemental insurance premiums as deductible medical expenses. To utilize this deduction, you must itemize your deductions rather than taking the standard deduction, and your total qualified medical expenses must exceed seven and a half percent of your adjusted gross income. Because the standard deduction for seniors is quite high, most retirees find that itemizing does not make mathematical sense without catastrophic medical emergencies.

Your Next Step Toward Tax Confidence

Empowering yourself to navigate the retirement tax maze begins with a single, decisive action. Over the next forty-eight hours, pull up your most recent tax return and locate your adjusted gross income to determine exactly how close you are to triggering the next Medicare surcharge bracket or Social Security taxation threshold. Armed with this concrete data, you can schedule a conversation with a trusted tax professional to map out a strategic withdrawal plan for the upcoming year. Taking proactive control of your financial narrative eliminates the anxiety of unexpected expenses and ensures your savings remain right where they belong.