Finding the perfect place to spend your golden years means balancing your fixed budget with access to quality healthcare and a thriving community. If you want to relocate to conservative-leaning regions, the best red states to retire in 2026 offer aggressive tax breaks on pensions and lower overall living costs to stretch your savings further. Recent economic shifts push retirees to prioritize states combining robust eldercare infrastructure with zero state income taxes. Evaluating popular destinations requires examining local property tax assessments and rising property insurance rates. You can secure a comfortable, purpose-driven lifestyle by matching your specific financial realities and mobility needs with the right state’s unique legislative environment and cultural landscape.

The 2026 Retirement Landscape and Policy Shifts

Retirees face a unique economic environment today. While the aggressive inflation spikes of previous years have largely cooled, the residual elevated cost of living requires you to maximize every dollar of your fixed income. Consequently, migration trends reveal a strong preference for states offering favorable tax environments and lower regulatory burdens. Many conservative-leaning states proactively court older demographics by implementing legislation designed to protect retirement assets from state-level taxation. You must look beyond the simple promise of low taxes; evaluating the overall cost of living requires a comprehensive understanding of how local municipalities fund their public services, infrastructure, and emergency response networks.

State legislatures continually adjust their tax codes to attract affluent and stable senior populations. You will notice increased competition among these states to offer the most compelling financial packages—ranging from property tax freezes for older homeowners to complete exemptions on public and private pension income. Navigating this landscape demands strategic foresight. Moving across state lines triggers a complex web of financial transitions, meaning you must weigh potential tax savings against the reality of current mortgage rates, housing inventory shortages, and shifting healthcare networks.

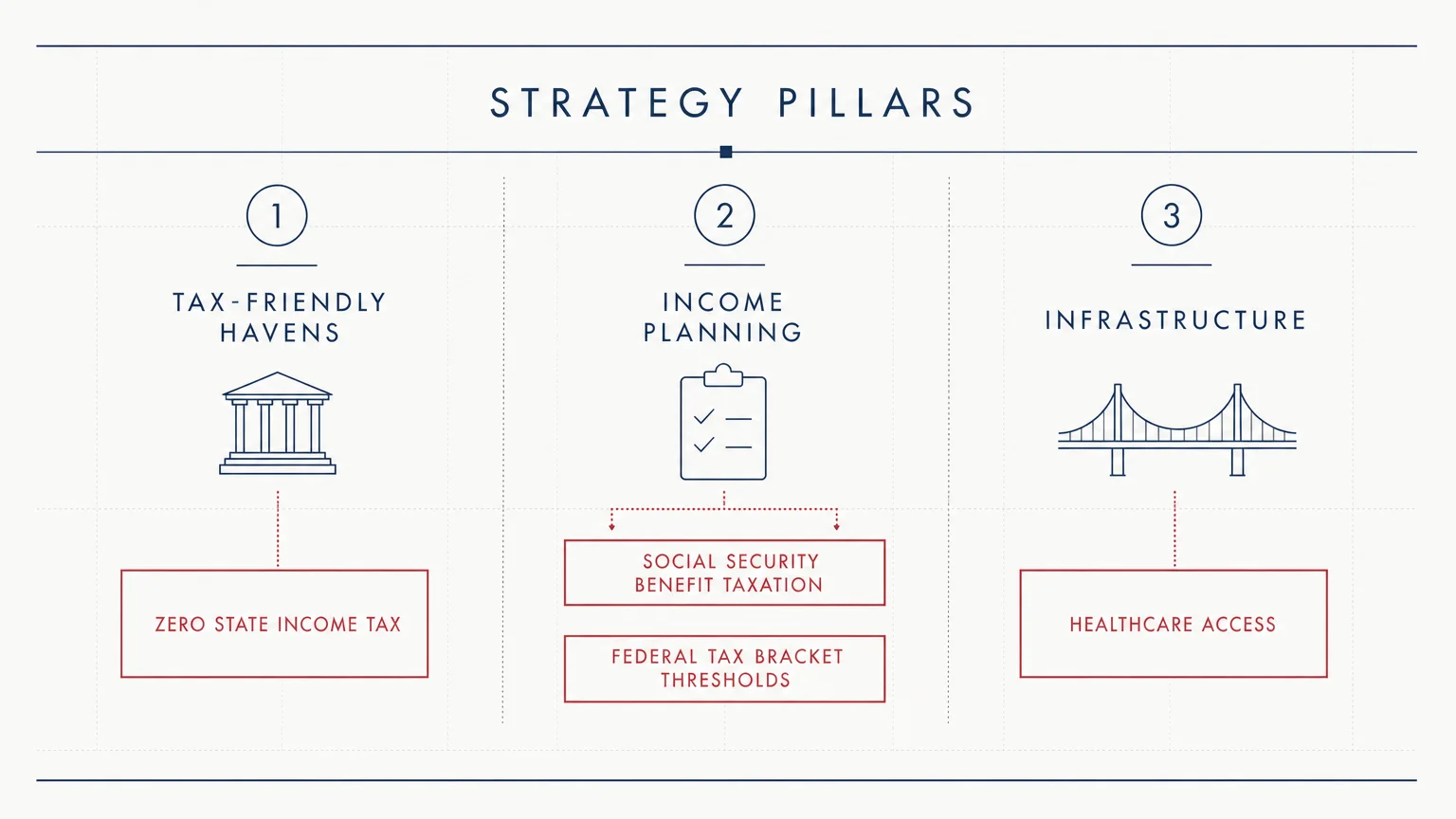

Core Strategy Pillars for Your Relocation

Tax-Friendly Havens and Income Planning

Protecting your wealth stands as the primary motivation for many relocation decisions. Several red states champion the zero-state-income-tax model, allowing you to keep a larger portion of your retirement account withdrawals and investment dividends. However, states must generate revenue to maintain essential services; they typically offset missing income taxes through higher sales taxes, elevated property taxes, or localized municipal fees. You must calculate your individual tax burden based on your specific spending habits and housing choices rather than relying on broad statewide averages.

Your Social Security benefits also require careful attention during this planning phase. While the federal government taxes a portion of these benefits depending on your combined income, many red states completely exempt them from state-level calculations. You can explore the exact mechanics of Social Security benefit taxation to project your monthly net income accurately. Furthermore, you should consult the current federal tax bracket thresholds to ensure your withdrawal strategies align efficiently with your new state’s tax environment, preventing unexpected liabilities during tax season.

Healthcare Access and Wellness Infrastructure

Your physical well-being dictates your quality of life, making healthcare infrastructure a non-negotiable factor in your relocation strategy. The availability of high-quality medical care varies drastically across regions, particularly within geographically expansive states. Metropolitan areas in Texas, Florida, and Tennessee host some of the nation’s most prestigious research hospitals and geriatric specialty centers. Conversely, rural counties in these same states often struggle with physician shortages and extended emergency response times. You need to map the exact distance from your prospective neighborhood to the nearest comprehensive stroke center or specialized cardiology clinic.

Insurance networks introduce another layer of complexity to your move. Moving to a new geographic rating area forces you to re-evaluate your supplemental health coverage. You should diligently investigate Medicare Advantage plan availability in your target zip code, as network strength and out-of-pocket maximums fluctuate significantly by county. Prioritize locations where multiple competing health systems drive up the quality of care while keeping premium costs manageable for patients on fixed incomes.

Lifestyle Design and Community Engagement

A successful retirement extends far beyond financial spreadsheets and medical appointments; it requires purpose, social connection, and an environment that encourages active living. The most popular red states generally offer warmer climates, allowing you to maintain an outdoor lifestyle year-round. Consistent physical activity directly correlates with extended mobility and delayed cognitive decline. You should seek communities offering extensive walking trails, accessible recreational facilities, and robust adult education programs.

Cultural alignment and civic engagement also play vital roles in preventing senior isolation. Many retirees choose to offset inflation by participating in the gig economy or securing part-time consulting roles. You can monitor local consumer price index trends to gauge the economic vitality of a prospective region. Additionally, reviewing comprehensive livability indices helps you identify towns that prioritize pedestrian safety, reliable public transit options, and diverse volunteer networks, ensuring you remain an integral part of the local social fabric.

Top Senior-Friendly Red State Destinations for 2026

Florida: The Evolving Standard

Florida remains a dominant force in the retirement landscape due to its entrenched senior culture and highly specialized medical infrastructure. The state levies no personal income tax, protecting your investment yields and pension distributions entirely. You will find endless community options tailored specifically to active adults, ranging from sprawling resort-style developments to quiet coastal enclaves. However, you must realistically budget for the state’s volatile property insurance market. Premium costs for coastal homes require substantial financial padding. You can mitigate these risks by targeting newly constructed homes built to the latest hurricane resilience codes or by exploring inland communities located on higher ground.

Texas: Expansive Spaces and Economic Might

Texas appeals to independent retirees seeking vast landscapes, a fiercely pro-business climate, and exceptional healthcare hubs like the Texas Medical Center in Houston. Like Florida, Texas does not tax personal income, giving your retirement distributions maximum purchasing power. You must, however, prepare for some of the highest property taxes in the nation. To protect older residents, Texas offers a school district property tax ceiling for homeowners over the age of sixty-five, effectively freezing a significant portion of your tax bill. You will find the best balance of affordability and amenities in the Texas Hill Country, which provides a temperate climate, thriving cultural scenes, and rapid access to major urban centers.

Tennessee: Mountain Charm and Fiscal Prudence

Tennessee strikes an ideal balance for retirees who want distinct, manageable seasons without the punishing winters of the Northeast or Midwest. The state recently phased out its final taxes on investment income, rendering it completely free of state income taxes. You can enjoy a relatively low overall cost of living, particularly in towns outside the immediate Nashville metropolitan radius. Communities in East Tennessee offer unparalleled access to the Great Smoky Mountains, fostering an incredibly active, nature-oriented lifestyle. You will encounter higher local sales taxes, but careful spending on groceries and prescription medications—which often carry reduced or zero tax rates—keeps daily living expenses highly competitive.

South Carolina: Coastal Elegance and Targeted Exemptions

South Carolina provides a gentler, more historic alternative to the bustling retirement hubs further south. While the state does levy an income tax, it offers incredibly generous deductions specifically targeted at retirees. Residents over sixty-five can deduct substantial amounts of retirement income, and Social Security benefits remain entirely exempt. Property taxes sit well below the national average, making homeownership highly sustainable on a fixed budget. You will find robust healthcare systems clustered around Charleston and Greenville, alongside a deep-rooted culture of hospitality that makes integrating into new social circles remarkably easy.

Expert Perspectives on Strategic Relocation

Certified Financial Planners consistently emphasize the necessity of running a localized cash-flow analysis before committing to a move. Experts warn against making relocation decisions based on a single variable, such as zero income tax. You must factor in the hidden costs of moving away from your established support networks. Gerontologists note that family proximity serves as an informal insurance policy against future caregiving costs. If you move thousands of miles away from your adult children to save on taxes, you might eventually spend those exact savings on private in-home care or frequent cross-country flights. You achieve the best outcomes when you balance fiscal efficiency with deep, reliable social connections.

Navigating Risks and Building Safeguards

Relocating in your later years exposes you to specific vulnerabilities that require proactive defense mechanisms. Moving scams frequently target older adults transitioning across state lines; you must thoroughly vet relocation companies through federal registries and demand binding, in-person estimates. Furthermore, you should prepare for potential healthcare benefit cliffs. Medicaid eligibility criteria and expansion statuses vary wildly among conservative-leaning states. If you anticipate needing long-term nursing care and potentially spending down your assets, you must understand your destination state’s specific Medicaid look-back periods and asset recovery policies.

You also need to account for localized climate risks that directly impact your financial stability. Many of the most popular retirement destinations face increasing threats from extreme heat, hurricanes, or localized flooding. You must carefully assess the long-term viability of the local utility grids and the exact cost of specialized hazard insurance. Building safeguards means overestimating your initial housing budget to accommodate comprehensive insurance policies, installing necessary home modifications immediately upon arrival, and establishing relationships with primary care physicians before you officially change your residency.

Frequently Asked Questions

What makes conservative-leaning states financially appealing to retirees?

Conservative-leaning states frequently design their fiscal policies to attract private wealth and business development, resulting in lower regulatory burdens and minimal taxation on personal income. For retirees, this usually translates to zero state income taxes, comprehensive exemptions on Social Security benefits, and specialized property tax freezes for senior citizens. You benefit directly from these policies by retaining a much higher percentage of your mandatory IRA distributions, private pensions, and investment dividends compared to living in high-tax jurisdictions.

How do zero-income-tax states make up their revenue, and will it affect me?

States without an income tax must fund roads, schools, and emergency services through alternative revenue streams. They typically rely heavily on elevated sales taxes, higher corporate taxes, aggressive property tax assessments, or special municipal utility district fees. This affects you directly based on your lifestyle; if you buy an expensive home and consume a high volume of taxable goods, you might end up paying more in combined local taxes than you saved by escaping your previous state’s income tax. You must calculate your total expected tax burden based on your specific consumption habits.

Are rural healthcare systems in these states reliable for aging adults?

Rural healthcare presents a significant challenge across the entire country, but expansive states face particularly acute physician shortages outside major cities. While the metropolitan centers of Texas, Florida, and Tennessee offer world-class, cutting-edge geriatric care, their rural counties frequently experience hospital closures and severe lacks of specialists. You should only consider rural retirement if you maintain excellent baseline health and are willing to drive an hour or more for specialized treatments, cardiology appointments, or comprehensive emergency care.

How should I evaluate climate risks when moving to states like Florida or Texas?

You must treat climate risk as a direct financial liability. When considering a property, you should pull historical flood data, review the age of the home’s roof, and request previous insurance premium statements from the seller. Extreme heat requires reliable, efficient HVAC systems, while coastal areas necessitate impact-resistant windows and robust structural reinforcements. You need to contact an independent insurance broker licensed in your destination state before making an offer on a home to ensure the property remains insurable at a price that fits your fixed monthly budget.

Your Next 48 Hours

Take control of your relocation strategy today by initiating one concrete step within the next two days. Open a blank document and list your three non-negotiable living requirements—whether that means being within twenty miles of a top-tier hospital, living in a zero-income-tax jurisdiction, or securing a property with minimal climate risk. Next, reach out to your certified financial planner to request a tax-impact analysis comparing your current state with your top two destination choices. You remove the guesswork from your retirement transition by putting hard data behind your daydreams. Secure your financial future by making informed, proactive decisions right now.