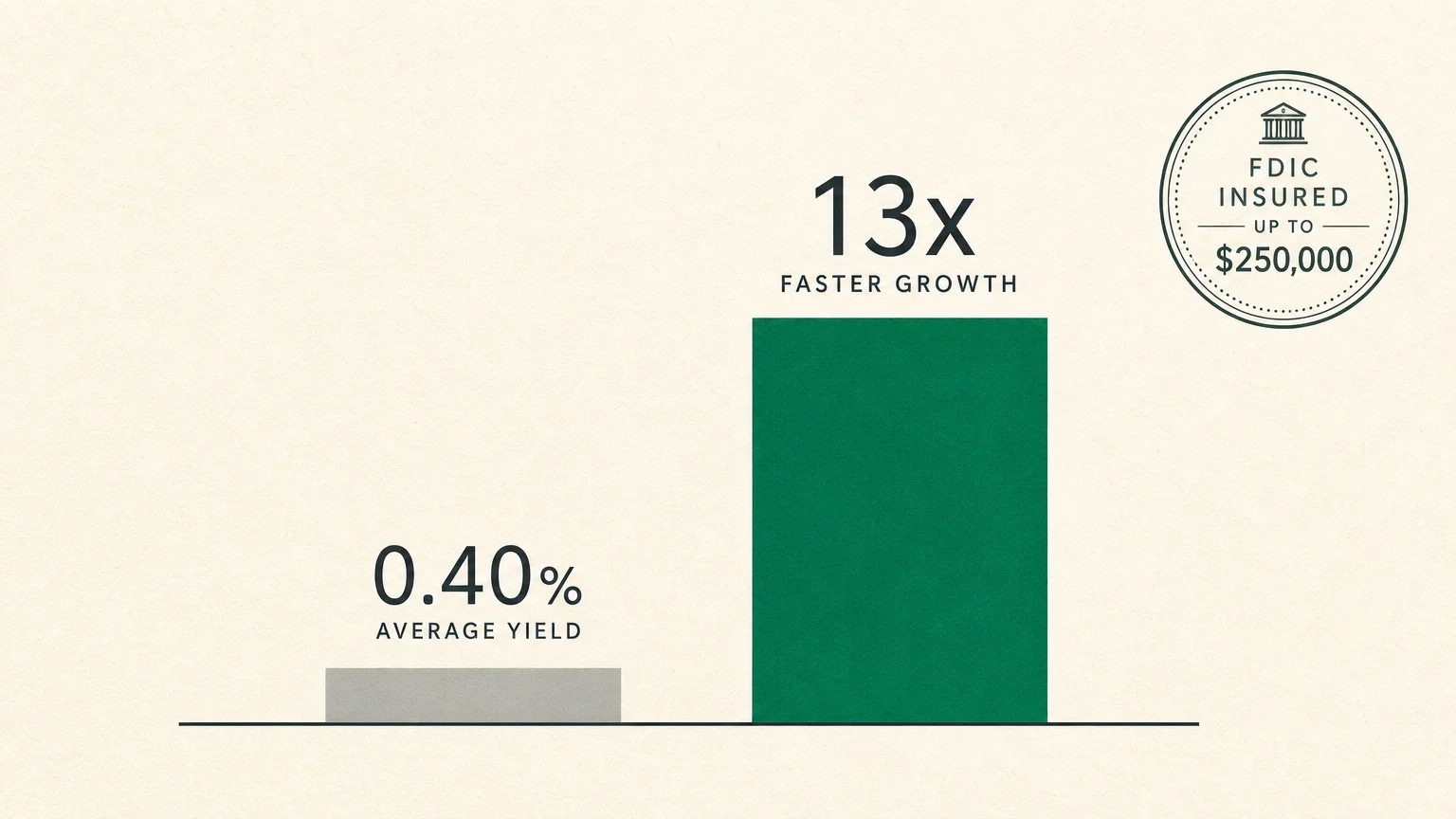

Trading your traditional bank savings account for a high-yield alternative can instantly grow your money up to 13 times faster without adding market risk. As traditional banks continue to offer a paltry 0.40 percent average yield, moving your cash into safe investment accounts creates an immediate, reliable income stream for your retirement. Inflation constantly threatens fixed-income budgets, meaning you need every dollar working at maximum efficiency to protect your purchasing power. Shifting your reserves into the right low-risk investments secures your financial baseline and funds your lifestyle design. You will uncover nine proven financial vehicles that protect your principal, leverage recent federal interest rate policies, and generate substantial returns to support a comfortable, stress-free future.

Understanding the Current Economic Landscape

The Federal Reserve dictates the baseline for how much financial institutions pay you for keeping your money in their vaults. When the central bank holds interest rates steady, retirees enjoy a unique window of opportunity to capitalize on safe yields. National brick-and-mortar banks stubbornly refuse to pass these elevated rates on to consumers; they rely on customer inertia, hoping you simply leave your nest egg in legacy accounts earning less than half a percent. Meanwhile, the Bureau of Labor Statistics regularly reports fluctuations in the Consumer Price Index, reminding you that daily expenses for groceries, utilities, and healthcare continue to climb. Leaving your cash in an underperforming account essentially guarantees a loss of purchasing power. Taking an active role in your income planning requires moving your liquid assets into vehicles designed to outpace inflation. By embracing modern financial tools, you force your cash reserves to work significantly harder while maintaining absolute liquidity and safety.

Income Planning With High-Yield Savings and Money Market Accounts

High-yield savings accounts remain the foundational building block of any robust retirement income plan. Online banks operate with minimal overhead costs, allowing them to offer yields up to 13 times higher than traditional street-corner institutions. When you deposit your emergency fund into one of these best savings accounts, your money compounds immediately without exposing you to stock market volatility. You maintain complete access to your funds, allowing you to withdraw cash for unexpected home repairs without penalty. Experts consistently highlight these accounts as the easiest way to generate passive income while keeping your principal intact.

Money market accounts provide a similar mechanism to grow your money, but they often include conveniences like check-writing privileges and debit card access. You can think of a money market account as a hybrid between a checking and a savings account. These low-risk investments require slightly higher minimum balances, making them ideal for retirees who keep substantial cash reserves on hand. The Federal Deposit Insurance Corporation insures both high-yield savings and money market accounts up to $250,000 per depositor. This government backing ensures you will never lose a single penny of your deposited principal.

Locking in Yields With Certificates of Deposit and Cash Management Accounts

When you want to lock in a guaranteed return for a specific timeframe, certificates of deposit offer unbeatable predictability. You agree to leave your money untouched for a set period, and the bank rewards you with a fixed interest rate. This strategy protects you against the risk of falling interest rates. If central banks cut rates next year, your existing certificate of deposit continues paying the higher yield secured on day one. You can utilize a CD ladder by spreading your cash across multiple certificates with staggered maturity dates. This approach provides regular access to portions of your cash while capturing the highest yields.

Cash management accounts represent another powerful tool for your safe investment portfolio. Non-bank financial service providers and brokerage firms offer these versatile accounts to help you streamline your finances. A cash management account automatically sweeps uninvested cash into partner banks to earn high interest rates while providing a single dashboard to monitor your wealth. Moving your operating cash into a cash management account ensures the money waiting to pay next month’s bills earns a respectable return.

Securing Your Principal With Government-Backed Bonds

The United States government issues several debt instruments that serve as exceptionally safe investment accounts. Treasury bills mature in one year or less and function by allowing you to purchase the bond at a discount from its face value. When the bill matures, the government pays you the full face value; the difference represents your profit. Because treasury bills enjoy the full faith and credit backing of the U.S. government, they carry virtually zero default risk. The interest you earn on treasury bills remains completely exempt from state and local income taxes, providing a substantial advantage in high-tax jurisdictions.

For longer-term inflation protection, Series I savings bonds offer a yield comprised of a fixed rate and an inflation rate that adjusts twice a year. You purchase these bonds directly through the government, effectively shielding your savings from the erosive power of rising consumer prices. Treasury inflation-protected securities operate on a similar premise but adjust the actual principal value of the bond based on inflation metrics. Incorporating these government-backed assets into your portfolio creates a fortress around your retirement savings, keeping your capital safe regardless of broader economic turbulence.

Protecting Your Health and Wealth With Specialized Accounts

Healthcare expenses consistently rank among the primary concerns for retirees, making targeted savings strategies crucial for your long-term wellness. Health savings accounts serve as the ultimate vehicle for managing future medical costs while securing tax advantages that no other account can match. If you possess a high-deductible health plan prior to enrolling in Medicare, you can funnel money into this account tax-free. The funds grow tax-free, and you can withdraw the money tax-free to cover qualified medical expenses. Treating this account as a long-term investment vehicle allows you to amass a dedicated reserve for prescription medications or dental procedures.

Protecting your physical health requires robust financial health to fund quality care. Dr. Evelyn Carter, a gerontologist researching aging and financial stress, notes that retirees with dedicated healthcare funds experience lower cortisol levels and report higher overall life satisfaction. You can invest the balance of your health savings account into conservative mutual funds, effectively transforming it into a specialized retirement account. Even after transitioning to Medicare, the accumulated balance remains yours to spend on out-of-pocket health costs indefinitely.

Enhancing Your Lifestyle Design With Fixed Contracts

Earning substantial interest on your safe investment accounts directly empowers your lifestyle design. When you generate an extra few thousand dollars a year through optimized yields, you create a dedicated budget for travel, hobbies, or meaningful experiences with your grandchildren. Fixed annuities provide a reliable avenue to achieve this lifestyle stability. By purchasing a fixed annuity contract from a highly rated insurance company, you secure a guaranteed interest rate for a specific duration, often outpacing traditional bank products.

You can structure these contracts to provide a steady stream of income that acts like a personal pension, ensuring you never outlive your resources. Robert and Sylvia Jenkins, a retired couple from Ohio, recently shifted a portion of their dormant checking funds into a fixed annuity and a high-yield savings account. Robert shared that the resulting passive income fully funded their annual cross-country road trip without requiring them to touch their principal. Designing your retirement around guaranteed income streams removes the anxiety of market volatility, freeing you to focus entirely on personal fulfillment.

Critical Risks and Safeguards for Retirees

Maximizing your yield introduces complexities that require careful navigation to avoid unintended financial consequences. Certified Financial Planner Marcus Thorne cautions that dramatically increasing your interest income can trigger unexpected tax liabilities. Earning thousands of dollars in a high-yield savings account increases your modified adjusted gross income. If your income crosses specific thresholds, you may encounter the Medicare Income-Related Monthly Adjustment Amount. The Centers for Medicare and Medicaid Services applies this surcharge to your Part B and Part D premiums, forcing you to pay more for your healthcare coverage. You must balance your desire to grow your money with a comprehensive understanding of your tax brackets.

Additionally, the pursuit of high returns attracts scammers hoping to exploit retirees. Cybercriminals frequently create polished websites advertising certificates of deposit with unbelievably high interest rates. These phantom institutions vanish the moment you wire your funds. You must always verify the legitimacy of any financial institution by checking its official registration. The AARP Fraud Watch Network constantly monitors emerging financial scams, serving as an excellent resource to help you spot fraudulent deposit offers.

Frequently Asked Questions

Can I lose my money in a high-yield savings account?

You face zero risk of losing your principal in a properly insured high-yield savings account. Federal insurance programs guarantee your deposits up to $250,000 per institution. You simply need to confirm that your chosen bank carries FDIC insurance or NCUA insurance. As long as you stay within the coverage limits, your money remains completely secure against institutional failure.

How do cash management accounts differ from traditional checking?

Cash management accounts typically operate through brokerage firms rather than traditional banks, though they sweep your funds into partner banks to secure federal insurance. They offer significantly higher interest rates than standard checking accounts while providing similar liquidity features. You will often enjoy benefits like unlimited ATM fee reimbursements worldwide, making them convenient for retirees who travel frequently.

Will earning more interest affect my Social Security taxes?

The interest you earn from safe investment accounts adds to your combined income, which determines the taxation of your benefits. The Social Security Administration calculates your combined income by adding your adjusted gross income, nontaxable interest, and half of your Social Security benefits. If this total exceeds specific federal thresholds, up to 85 percent of your benefits may become subject to federal income tax. You should consult a tax professional to model how higher yields impact your tax liability.

What happens if interest rates drop after I open one of these accounts?

The outcome depends entirely on the specific account you select. For high-yield savings, money market, and cash management accounts, your interest rate will decrease, as these yields fluctuate with central bank policies. However, if you secured a certificate of deposit or a fixed annuity, your high rate remains locked in for the entire duration of the contract. Utilizing a blend of fixed and variable accounts helps you balance liquidity with long-term rate protection.

Take Control of Your Financial Future

Your retirement savings represent decades of hard work, discipline, and sacrifice. You deserve to see those funds thrive in an environment that protects your principal while delivering substantial returns. Leaving your cash in an obsolete bank account deprives you of the financial momentum required to combat inflation and fund your ideal lifestyle.

Over the next 48 hours, log into your primary banking portal and locate the exact interest rate applied to your savings. If that number falls below the current market standard, select one of the safe accounts discussed today and initiate a transfer. Opening a new high-yield savings account or purchasing a short-term treasury bill takes less than fifteen minutes online. Reclaiming your financial power ensures your money works tirelessly on your behalf, granting you the peace of mind to truly enjoy your retirement.

20 Responses

ZFbUUlsUHGHwTjhirPHGDMj

UlfDClhYetSSczArt

UgjZWMtqkToHxzypBZAoeJNN

TmXWkhpvgfINdpQJtUVjwzp

yksgrvqwdIaGjIGfUL

fnKBLpEkWTGcTUbvyffmSHUz

wJjoMBqHkxpTOuktmUuNI

rCCtWbNnOtCTEMkiDWhB

UBtcxfUupmsSBEsa

qyoOeFzOYJyMczdfmCbQgur

yoYWmxBlUjpcDvIJxAcdC

VgDOPOzSueBWULaFGWdG

sMYobLYjMbszFpxGSAi

LusXImcOHOpAxkHC

rGPrkXQEsNjWeYaCupSpQk

alGehlLAsRGCVuRNCHkBMxQ

PfjAetItbrpjjKHhnRMBMf

RHKARzJxptgkkfCpev

ZxXAnxwyAKwtdEyfUrxPrZs

DwjqgpfVSbZPynCIWTgcdUS