Navigating retirement finances requires staying ahead of potential shifts in how the government taxes your benefits, allowing you to keep more of your hard-earned money. With rising inflation and an aging population, lawmakers frequently propose updates to Social Security taxation, making it crucial to understand how these changes impact your monthly income. Up to eighty-five percent of your benefits face federal income taxes if your combined earnings exceed thresholds established decades ago. Because these limits lack automatic inflation adjustments, a growing number of middle-class seniors find themselves owing taxes on their benefits every year. By monitoring legislative proposals and adjusting withdrawal strategies today, you can protect your fixed income and ensure your lifelong savings stretch significantly further.

The Current Landscape of Social Security Taxation

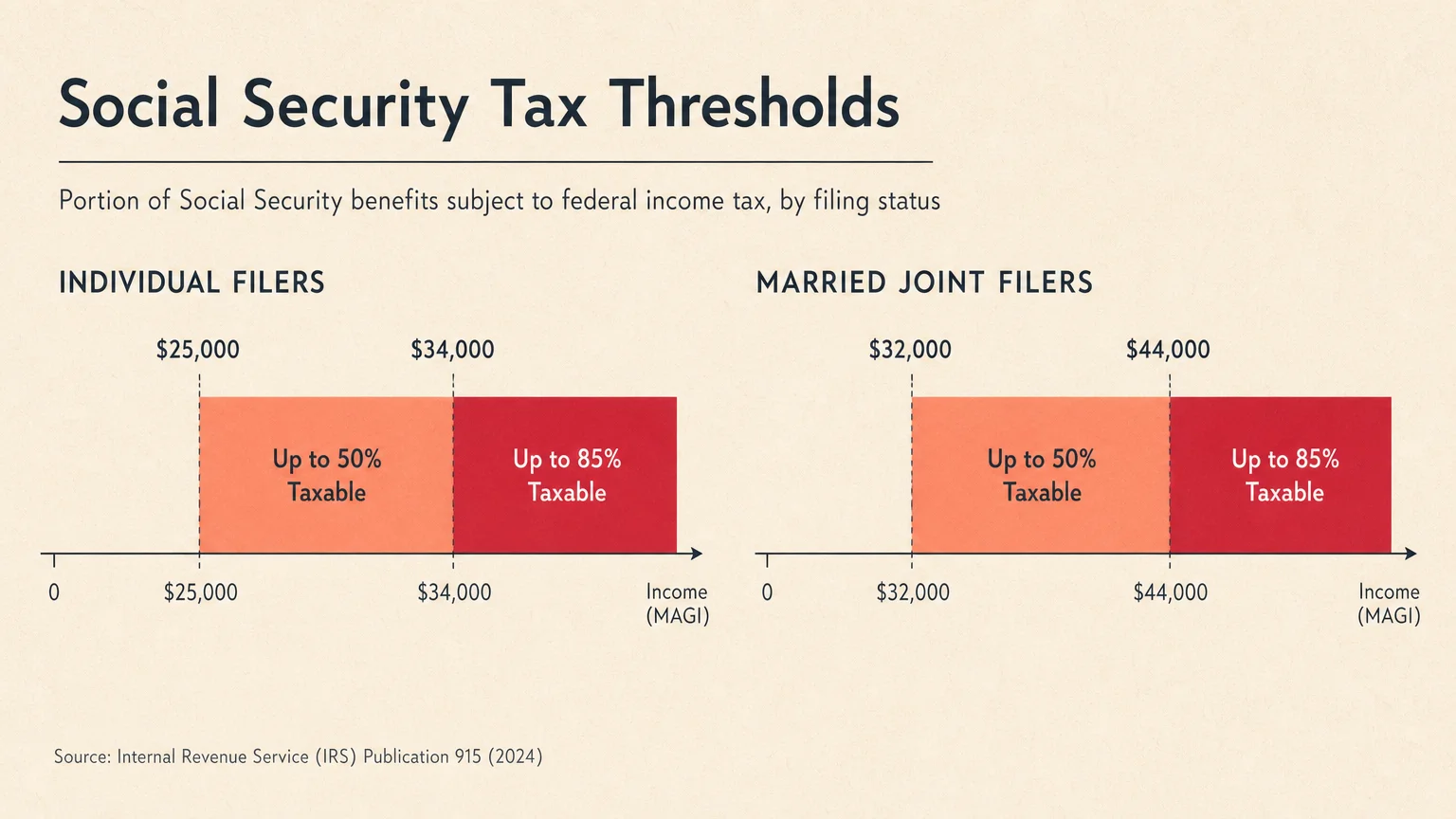

Understanding how the federal government views your retirement benefits provides the foundation for protecting your wealth. The Social Security Administration and the internal revenue framework use a specific formula known as combined income to determine if your monthly checks are taxable. You calculate this figure by adding your adjusted gross income, any nontaxable interest you earn, and exactly half of your yearly Social Security benefits. If you file as an individual and your combined income falls between $25,000 and $34,000, up to fifty percent of your benefits may be subject to income tax. If your combined income exceeds $34,000, up to eighty-five percent of your benefits become taxable. For married couples filing jointly, the base threshold sits at $32,000, with the eighty-five percent tax rate kicking in above $44,000.

Congress established these base thresholds in 1984 and added the higher tier in 1993. Crucially, lawmakers never tied these figures to inflation. As a result, the natural upward march of wages and cost-of-living adjustments pushes more retirees into these taxable brackets every single year. A policy originally designed to tax only the wealthiest beneficiaries now impacts millions of middle-class seniors. Recent legislative proposals aim to correct this growing burden. Lawmakers continually introduce bills proposing to eliminate the federal taxation of Social Security benefits entirely. To fund this elimination, these proposals often suggest increasing the payroll tax cap on working Americans. For 2026, the maximum amount of earnings subject to the Social Security payroll tax reached $184,500. Removing the tax burden for retirees while raising the contribution cap for high earners remains a fiercely debated topic in Washington. While you wait for legislative action, mastering your personal tax strategy remains your best defense against shrinking retirement checks.

Income Planning: Shielding Your Monthly Cash Flow

Strategic income planning allows you to legally minimize the portion of your Social Security benefits subject to federal taxes. Your first line of defense involves managing the accounts you draw from to meet your daily living expenses. Because traditional individual retirement account withdrawals and 401(k) distributions count toward your adjusted gross income, pulling heavily from these accounts directly inflates your combined income. This inflation pushes a larger percentage of your Social Security benefits into the taxable zone. You can counteract this phenomenon by diversifying your withdrawal sequencing early in your retirement journey.

Certified Financial Planner professionals frequently recommend establishing a robust tax-free income source before you claim Social Security. Qualified withdrawals from a Roth account do not count toward your adjusted gross income, meaning they do not factor into the formula that taxes your benefits. If you are currently in your late fifties or early sixties, executing strategic conversions during low-income years can dramatically lower your future tax liabilities. You pay the income tax on the converted amount now, allowing those funds to grow tax-free and provide invisible income during your later years.

Coordinating your withdrawal strategy with your spouse can also prevent accidental tax spikes. If you both claim benefits and draw from pensions simultaneously, you easily breach the $32,000 combined income threshold for joint filers. You might decide to delay one spouse’s Social Security claim to age seventy while spending down taxable retirement accounts early. This approach temporarily increases your taxable income early in retirement but significantly lowers your combined income later, protecting your maximized survivor benefits from excessive taxation. Exploring these legal frameworks with a qualified professional ensures you keep the highest possible percentage of your lifetime contributions.

Health and Wellness: The Hidden Tax Connection

You might not immediately associate your physical health with your tax bracket, but the two domains remain deeply intertwined during your senior years. Unplanned medical expenses often force retirees to take massive, sudden distributions from their tax-deferred retirement accounts. When you withdraw forty thousand dollars to cover an unexpected health crisis or a vital accessibility modification to your home, you instantly spike your adjusted gross income. This spike triggers a devastating domino effect—it increases the taxation on your Social Security benefits and can simultaneously trigger severe healthcare surcharges.

The federal government bases your Medicare Part B and Part D premiums on your modified adjusted gross income from two years prior. Surging your income to pay for preventable medical events forces you to pay higher Medicare premiums while losing more of your Social Security to taxes. Investing in your physical wellness serves as a profound financial safeguard. Regular cardiovascular exercise, strength training, and proactive health screenings dramatically reduce your lifetime medical costs. Gerontologists emphasize that maintaining mobility prevents the need for expensive in-home care or costly residential transitions, keeping your withdrawal rate stable and predictable.

You can also leverage specific financial tools to separate health costs from your taxable income. If you contributed to a designated health savings account during your working years, those funds grow tax-free and remain tax-free when used for qualified medical expenses. Pulling from this specialized account to cover a surgery or prescription medication keeps your adjusted gross income perfectly untouched. You successfully fund your recovery without paying a single dime of extra tax on your fixed retirement income.

Lifestyle Design: State Taxes and Working in Retirement

Your geographic location plays a massive role in how much of your Social Security benefit you actually get to spend. While federal taxation rules apply uniformly across the country, state-level taxation varies wildly depending on your zip code. Currently, the vast majority of states do not tax Social Security benefits, but a handful of states still enforce their own unique tax formulas on your checks. Some states offer exemptions based on your age; others align strictly with the federal taxation thresholds.

If you live in a state that aggressively taxes retirement income, relocating could instantly increase your monthly cash flow. Many retirees flock to states with no income tax at all, ensuring their Social Security benefits and pension payouts remain untouched by the local government. However, you must carefully weigh these income tax savings against property taxes, sales taxes, and the overall cost of living. A state that skips taxing your benefits might make up the difference by charging exorbitant property taxes on your home, ultimately neutralizing your financial victory.

Your lifestyle choices regarding employment also intersect heavily with Social Security taxation. Many pre-retirees choose to ease into their golden years by taking on part-time consulting roles or launching small businesses. If you claim your benefits before reaching your full retirement age, the government enforces an earnings limit. For 2026, this limit sits at $24,480. Earning wages above this limit results in temporarily withheld benefits. More importantly, those part-time wages increase your adjusted gross income, making it highly likely that the benefits you do receive will face the maximum eighty-five percent federal tax rate. Consulting reputable aging advocacy resources can help you design a lifestyle that balances fulfilling work with tax-conscious earning limits.

Risks and Safeguards: Navigating Scams and Benefit Cliffs

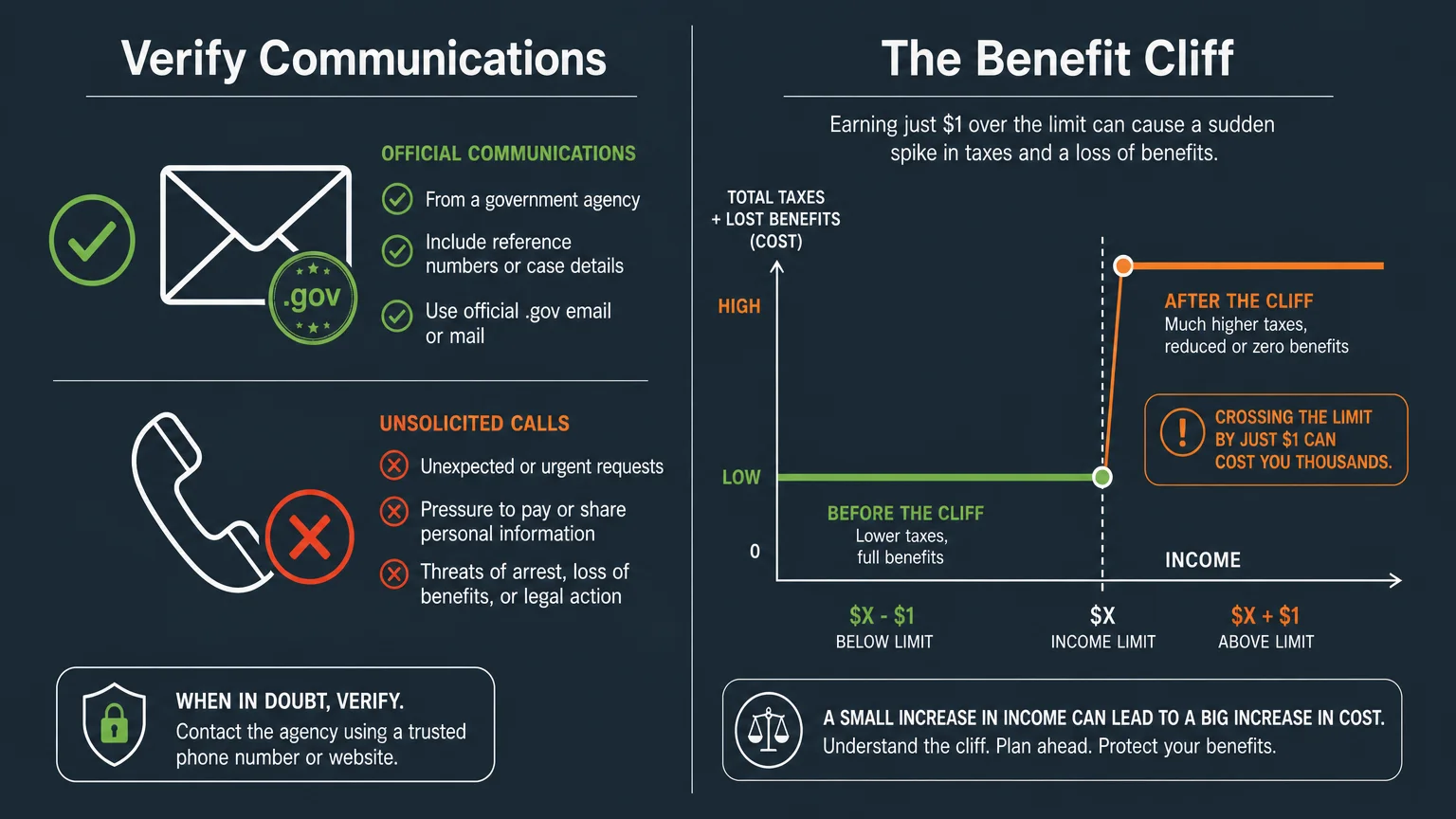

As the conversation around Social Security taxation grows louder, malicious actors exploit the confusion to target vulnerable retirees. You must remain vigilant against sophisticated scams designed to steal your identity or drain your bank accounts. Criminals frequently impersonate agents from federal tax agencies or the Social Security Administration. These scammers call or email you, claiming you owe thousands of dollars in unpaid taxes on your Social Security benefits. They often threaten immediate arrest or the suspension of your monthly checks unless you pay the fabricated debt using wire transfers, cryptocurrency, or prepaid gift cards.

Legitimate government agencies never demand immediate payment over the phone or request retail gift cards. If you receive a threatening call regarding the taxation of your benefits, hang up immediately. You can easily verify your true tax status by logging into your official account on the Internal Revenue Service portal. Protecting your personal information ensures your wealth remains safely in your hands.

Beyond external scams, you must also safeguard yourself against internal portfolio risks, primarily the dreaded benefit cliff. A benefit cliff occurs when a tiny increase in your income triggers a massive increase in your taxation or a total loss of a specific subsidy. Earning just one dollar over a tax threshold can push thousands of dollars of your Social Security benefits into a higher taxable percentage. Carefully projecting your capital gains, dividends, and required minimum distributions at the end of each calendar year helps you identify these cliffs before you fall over them. You might choose to delay selling a profitable stock until January to avoid pushing your current year’s combined income over the maximum taxation threshold.

Frequently Asked Questions About Benefit Taxation

At what age does the government stop taxing Social Security benefits?

The federal government does not eliminate the tax on your Social Security benefits at any age. Whether you are sixty-two or ninety-five, the exact same combined income formula dictates your tax liability. Your age heavily influences your standard deduction size, but it does not grant you a free pass from the taxation of your federal retirement benefits.

Do all states tax Social Security income?

No, the vast majority of states do not tax Social Security benefits at the state level. A shrinking minority of states still impose some form of tax on these benefits, though many of those states offer varying exemptions based on your total income brackets. You should frequently review the specific tax codes of your primary residence, as state legislatures frequently update these laws to attract retirees.

How exactly do I calculate my combined income?

You can determine your combined income by taking your adjusted gross income, which includes your wages, traditional retirement account distributions, and dividends. Next, add any nontaxable interest you earned throughout the year, such as interest from municipal bonds. Finally, add exactly fifty percent of your annual Social Security benefits. The resulting number dictates whether you cross the federal taxation thresholds.

Can I have taxes withheld directly from my monthly checks?

Yes, you can easily arrange for the federal government to withhold taxes from your Social Security checks, preventing a massive tax bill in April. You simply need to download Form W-4V, the Voluntary Withholding Request, and submit it to the government. You can choose to have seven, ten, twelve, or twenty-two percent of your monthly benefit withheld for federal taxes.

Take Control of Your Retirement Finances Today

Navigating the complexities of retirement taxation might feel overwhelming at first, but every proactive step you take builds a stronger wall around your financial security. You possess the power to shape your income strategy, minimize your tax burdens, and maximize the spending power of your lifelong contributions. While legislative changes may eventually alter the tax landscape, you can implement powerful safeguards right now to protect your cash flow and keep your budget reliable.

In the next forty-eight hours, commit to making one tangible change. Locate your tax return from last year and calculate your combined income to see exactly where you stand against the federal thresholds. If you find yourself facing an unexpected tax bill each spring, download the voluntary withholding form to smooth out your financial obligations. Take control of your numbers today, and embrace the peace of mind that comes with a masterfully protected retirement.