Discovering an error on your Social Security statement today can save you thousands of dollars in lost retirement income tomorrow. Most workers assume the government flawlessly records their lifetime earnings, but clerical mistakes and unreported wages silently drain future benefits for millions of Americans. By reviewing your personal earning history annually, you take control of your financial foundation and guarantee you receive every dollar you earned. You need to scrutinize your documented wages, understand the formula determining your primary insurance amount, and initiate timely corrections with federal agencies. Taking just thirty minutes to evaluate your record protects your long-term security, ensuring your fixed income properly supports your lifestyle and health care costs.

The Current Retirement Landscape: Why Your Record Matters Now

The government recently shifted aggressively toward digital records, meaning paper statements no longer arrive in the mail for most workers under the age of sixty. This modernization cuts administrative costs but places the burden of verification entirely on your shoulders. Today, navigating retirement requires more than just passive participation; it requires active auditing of your financial footprint. Inflation adjustments, such as the annual Cost of Living Adjustment, strictly multiply your base benefit amount. If your base benefit sits artificially low due to an undocumented year of work from a decade ago, every subsequent inflation adjustment will underpay you for the rest of your life. Recent data from federal oversight agencies suggests millions of earnings records contain discrepancies, often stemming from name changes after marriage, employer reporting mistakes, or simple typographical errors on a wage form. As economic pressures force many pre-retirees to reevaluate their savings, maximizing your guaranteed government benefits serves as your strongest defense against market volatility. Protecting this income stream is essential for individuals on fixed budgets and those facing varying mobility challenges, ensuring everyone can access the resources needed for a dignified and stable retirement.

Income Planning: Rooting Out Errors on Your Social Security Statement

Your ultimate benefit relies entirely on your highest thirty-five years of earnings. When the system registers a missing year of income, that specific year gets recorded as a zero. A single zero drastically pulls down your lifetime average, permanently shrinking your monthly checks. You must create a secure online account through the federal portal to access your annual statement and meticulously review the column detailing your taxed earnings. Compare these figures against your personal tax returns or tax forms from previous years. If you notice a discrepancy, you must take immediate action. The process begins with gathering proof of income, which can include old pay stubs, tax documents, or a tax transcript retrieved directly from the Internal Revenue Service. Once you have your documentation, submit a Request for Correction of Earnings Record to the administration. Do not wait until you apply for benefits to fix these mistakes. Resolving a bureaucratic error takes time, and attempting to correct an omission on the eve of your retirement can delay your initial payments and cause unnecessary financial stress. By verifying your income data each spring, you safeguard your future earnings.

Lifestyle Design: Budgeting Around Accurate Benefit Projections

Accurate benefit projections serve as the absolute bedrock of your lifestyle design in retirement. When you know precisely how much fixed income you will receive, you can confidently make decisions about where to live, how to travel, and how to spend your time. Many retirees dream of relocating to communities that offer better climates or closer proximity to family members. However, signing a new lease or securing a mortgage requires absolute certainty about your monthly cash flow. If your benefit estimate is flawed due to an underlying earnings error, your entire household budget rests on a precarious foundation. Fixing these mistakes provides the financial clarity you need to design a life that accommodates your unique goals and varying mobility needs. Whether you plan to retrofit your current home with accessibility features or immerse yourself in local cultural organizations, every additional dollar recovered expands your options. Furthermore, understanding your true income allows you to strategically sequence your withdrawals from other retirement accounts. You can draw down taxable investments much more efficiently when you know exactly how much government support you will receive each month.

Health and Wellness: Coordinating Income with Medicare Costs

Securing the correct benefit amount also empowers you to navigate the complexities of future health care expenses. Your monthly income directly influences your medical coverage, specifically regarding your Medicare Part B premiums. The federal government uses your modified adjusted gross income from two years prior to determine if you must pay an Income-Related Monthly Adjustment Amount, commonly known as IRMAA. If you underestimate your baseline income because of an unresolved statement error, you might accidentally push yourself into a higher Medicare tax bracket when you eventually take distributions from your retirement accounts. Beyond the mathematics of premiums and deductibles, securing your maximum rightful income directly impacts your physical and mental wellness. Financial anxiety remains a leading cause of chronic stress among older adults, which can exacerbate cardiovascular issues, disrupt sleep patterns, and diminish cognitive function. By ensuring your income streams are fully optimized and accurate, you alleviate a massive psychological burden. That peace of mind frees up your energy to focus on preventative health measures, such as maintaining a nutritious diet, joining a fitness center, or participating in community wellness programs.

Expert Voices: Perspectives from Financial Planners and Gerontologists

Certified Financial Planner professionals consistently warn that clients overlook the vital step of auditing their lifetime earnings records. Financial advisors frequently note that pre-retirees will spend hours analyzing mutual fund expense ratios while completely ignoring a government clerical error that could cost them tens of thousands of dollars over a twenty-year retirement. Wealth managers stress that guaranteed income forms the most crucial pillar of a stable retirement plan, acting as a financial shock absorber when stock markets tumble. Gerontologists and aging specialists also emphasize the importance of financial self-advocacy for older adults. Research in the field of aging shows that individuals who actively manage their resources and maintain control over their financial narratives report much higher levels of life satisfaction. When you actively correct an error on your official record, you reinforce a sense of agency and independence. Experts at leading advocacy groups provide extensive retirement planning guidance, reminding seniors that the system is massive and impersonal. Bureaucracies do not catch their own mistakes; they rely entirely on citizens to report anomalies and advocate for themselves.

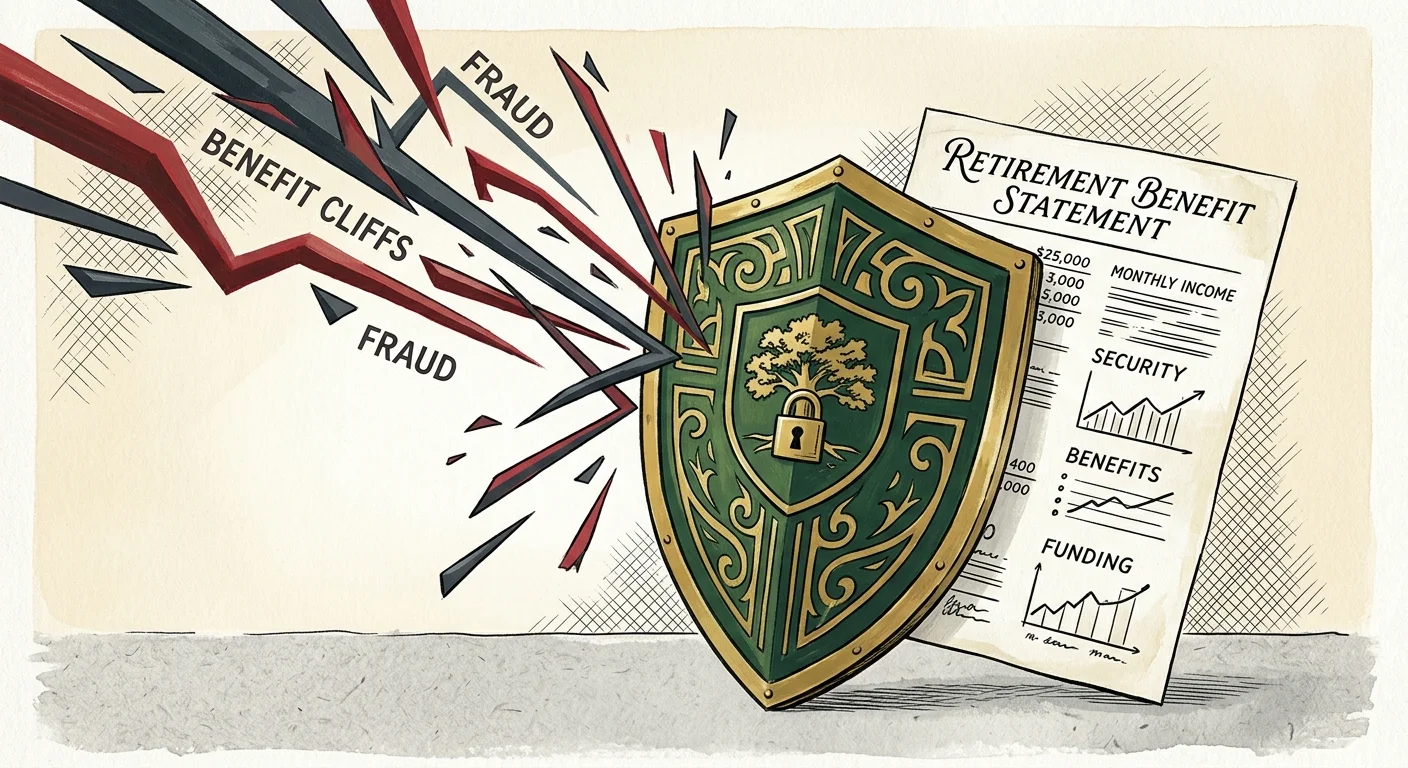

Risks and Safeguards: Navigating Scams and Benefit Cliffs

As you take charge of your retirement benefits, you must remain incredibly vigilant against the pervasive scams currently targeting older adults. Fraudsters frequently impersonate government officials, calling unsuspecting citizens to claim their identity has been suspended due to fraudulent activity. These criminals often demand immediate payment via gift cards or wire transfers to restore the account. You must remember that federal agencies will never call you demanding money or threatening immediate arrest. If you receive a suspicious call, hang up immediately and report fraudulent calls to the proper consumer protection authorities. Beyond malicious scams, you also need to protect yourself from structural pitfalls within the retirement system itself, such as the earnings test benefit cliff. If you decide to claim your benefits before reaching your full retirement age while continuing to work, the government places a strict limit on how much you can earn. Earning above this annual threshold results in a temporary withholding of your benefits. An inaccurate earnings record can further complicate this scenario, as the administration might miscalculate your allowable limits based on faulty historical data.

Frequently Asked Questions

How often should I check my earnings record?

You should review your official earnings record at least once every twelve months. The most strategic time to perform this audit is in the spring, shortly after you file your annual income taxes and receive your wage documents for the previous year. Making this an annual habit ensures that recent employer reporting errors are caught immediately while the relevant financial documents are still easily accessible on your desk.

What documentation do I need to prove missing wages?

To successfully correct a missing or inaccurate year of income, you must provide primary evidence of your earnings. The most effective documents include original tax forms, old pay stubs showing year-to-date totals, or official tax transcripts from the federal revenue service. If your employer went out of business and you lost your records, you might need to supply secondary evidence, such as personal wage logs or letters from former supervisors, though these take significantly longer to process.

Can an error reduce my spouse’s survivor benefits?

Yes, an error on your personal record can absolutely devastate the survivor benefits left to your spouse. Survivor benefits are directly calculated based on the primary earner’s lifetime record. If your statement contains zeros that artificially lower your primary insurance amount, your surviving spouse will inherit that permanently reduced monthly payment. Correcting your record today is a profound act of care and protection for your family’s financial future.

Is there a time limit to correct my earnings history?

The government generally imposes a strict time limit of three years, three months, and fifteen days following the year in which the wages were earned to correct an error. However, several vital exceptions exist to this rule. You can correct an error at any time if the wages were entirely omitted from your record by an employer, or if you have undeniable tax returns proving the income was indeed reported to the revenue service.

Your Next Steps

Taking control of your financial destiny requires immediate, focused action. Within the next forty-eight hours, commit to logging into your online account and downloading your most recent statement. Print the document, grab a pen, and trace your earnings history line by line to verify that every year of your hard work is accurately represented. If you spot a discrepancy, immediately gather your supporting tax documents and initiate the correction process. This simple thirty-minute exercise represents one of the highest returns on investment you will ever make regarding your personal time. Protecting your baseline income ensures you can confidently step into your next chapter, fully equipped to enjoy the security, health, and dynamic lifestyle you spent a lifetime building.