Your golden years should revolve around joy and comfort rather than constant financial anxiety over every dollar you spend. With Americans living an average of two decades past age 65, strategic investments in your daily quality of life are just as critical as preserving your nest egg. You might feel tempted to hold onto every penny, but financial planners universally agree that certain purposeful splurges actually protect your wealth and health over the long run. From proactive home modifications that prevent costly medical emergencies to professional fiduciary guidance that minimizes your lifetime tax burden, directing your resources toward five essential purchases guarantees an immediate and lasting return on your investment.

Navigating the Current Economic Landscape for Retirees

Before you decide where to allocate your resources, you must understand the broader financial environment shaping your retirement today. Recent policy shifts and market dynamics have fundamentally altered how you should approach your withdrawal strategies. For instance, the implementation of the SECURE 2.0 Act has pushed the required minimum distribution age to 73—and eventually 75—giving you a wider window to execute strategic tax planning. Meanwhile, although the Social Security Administration adjusts benefits for cost-of-living increases, those adjustments often lag behind the real-world inflation experienced in the healthcare and housing sectors. The rising costs of utility bills and property taxes frequently outpace the incremental boosts to your monthly fixed income, making every dollar you spend a critical decision.

These shifting economic tides require a transition from a saving mindset to a conscious spending mentality. Many retirees suffer from the habit of aggressive frugality, unnecessarily depriving themselves of comforts because they fear outliving their money. While you absolutely must maintain a balanced budget, hoarding funds at the expense of your health, safety, and happiness is counterproductive. Strategic spending actively mitigates future risks, ensuring you retain control over your lifestyle choices regardless of market volatility.

Purchase 1: Proactive Home Modifications for Aging in Place

Most retirees express a strong desire to remain in their own homes as they grow older, yet very few residential properties are designed to accommodate the physical realities of aging. Spending money upfront to modify your living space is one of the highest-yield investments you can make. Financial experts and gerontologists strongly advocate for installing barrier-free showers, widening doorways to accommodate mobility aids, and adding reinforced grab bars in high-risk areas like bathrooms and stairwells. Enhanced task lighting and slip-resistant flooring also dramatically reduce your daily hazards.

You should view these expenses as an insurance policy against catastrophic medical bills and forced facility care. A severe fall often initiates a cascade of health complications that drain your retirement savings far faster than the cost of a comprehensive bathroom remodel. By utilizing guidance from the National Institute on Aging, you can systematically assess your home for potential dangers and hire certified aging-in-place specialists to make elegant, functional updates that increase both your property value and your physical security.

Purchase 2: A Fee-Only Fiduciary Financial Planner

Navigating the complex maze of retirement taxation, investment withdrawal sequencing, and legacy planning is rarely a do-it-yourself endeavor. Hiring a fee-only fiduciary financial planner often pays for itself multiple times over. Unlike brokers who may earn commissions by selling you specific financial products, a fiduciary is legally obligated to act strictly in your best financial interest. They provide objective, comprehensive advice tailored specifically to your unique life circumstances and long-term goals.

These professionals excel at identifying expensive blind spots in your financial plan. They can help you execute strategic Roth IRA conversions during lower-income years, effectively minimizing the eventual tax burden on your required minimum distributions. Furthermore, they will structure your withdrawals to prevent you from unnecessarily triggering higher Medicare premiums through income-related monthly adjustment amounts. Knowing that a seasoned expert is actively monitoring legislative changes and your personal portfolio allows you to sleep soundly, freeing you to focus entirely on enjoying your daily life rather than stressing over economic charts.

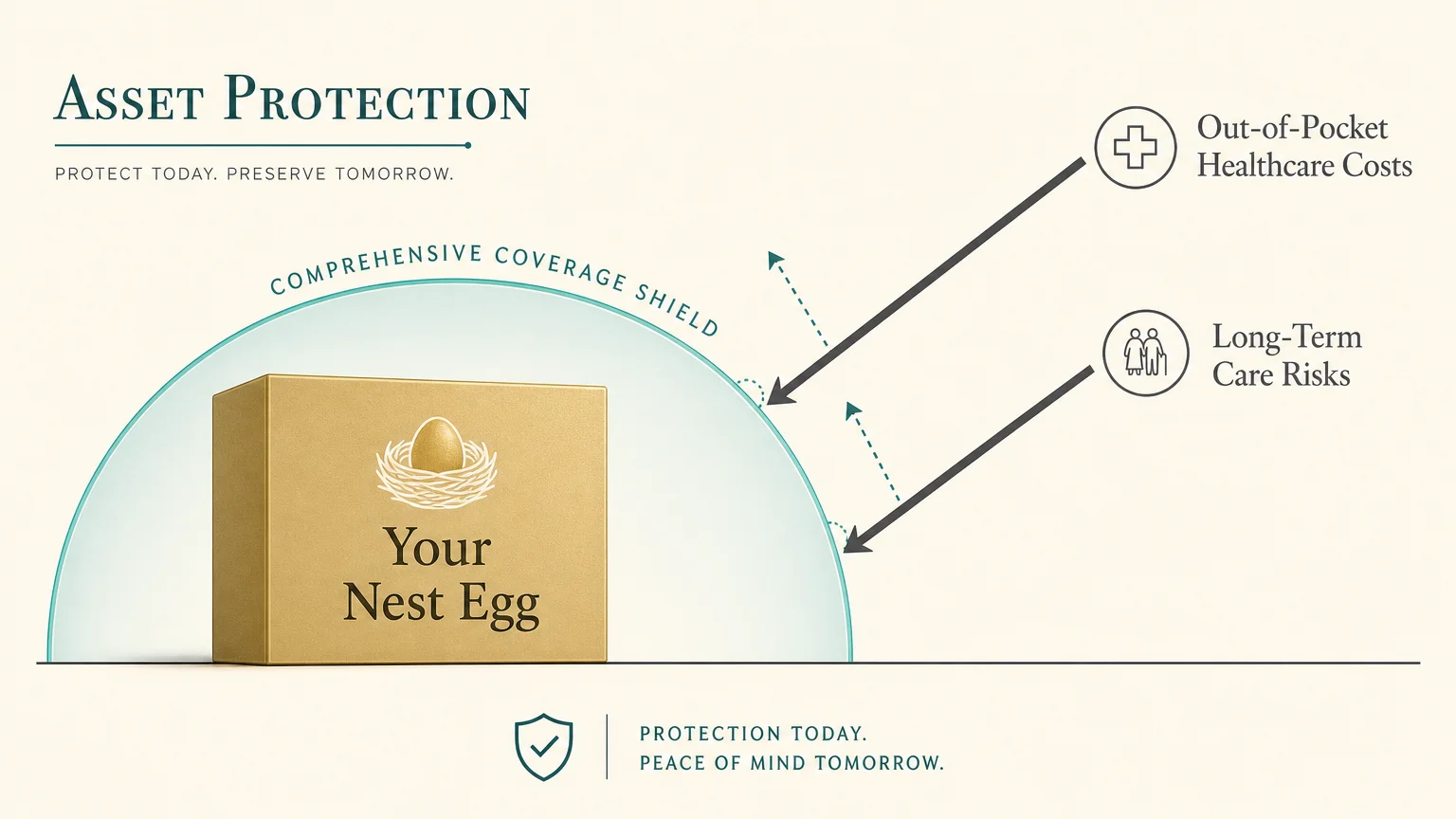

Purchase 3: Comprehensive Health and Long-Term Care Coverage

Healthcare ranks among the most significant expenses you will face in retirement, making comprehensive insurance coverage an absolute necessity rather than an optional luxury. While basic Medicare provides a foundational safety net, it features significant coverage gaps, including deductibles, copayments, and a complete lack of coverage for extended custodial care. Financial experts consistently recommend purchasing a robust Medigap policy or thoroughly researching comprehensive Medicare Advantage plans to explicitly cap your potential out-of-pocket medical expenses.

Beyond standard medical care, securing protection for extended care is crucial. Traditional long-term care insurance or modern hybrid life insurance policies that include long-term care riders are frequently worth the hefty premiums. Relying solely on your investment portfolio to fund a potential multi-year stay in an assisted living facility can rapidly decimate your estate and leave your surviving spouse in a precarious financial position. Exploring your coverage options via the official Medicare portal allows you to transfer these catastrophic financial risks to an insurance provider, effectively safeguarding your hard-earned assets.

Purchase 4: Preventive Health and Wellness Programs

Investing in your physical vitality directly translates to protecting your financial assets. Routine physical activity and proper nutrition are the most effective interventions for maintaining independence and warding off expensive chronic diseases. Spending your retirement dollars on a high-quality gym membership, hiring a personal trainer who specializes in senior mobility, or consulting with a registered dietitian are excellent uses of your capital. Many modern wellness centers even offer aquatic therapy and specialized balance classes designed specifically for older adults. Participating in these group activities also provides a valuable avenue for social connection, combating the isolation that frequently accompanies the post-career transition.

The financial return on investment for physical fitness is undeniable. Maintaining your muscle mass and cardiovascular health delays the onset of mobility issues, reducing your dependence on costly medical interventions and prescription medications. Furthermore, prioritizing premium, nutrient-dense foods over cheaper, highly processed alternatives provides immediate benefits to your cognitive function and energy levels. By treating your daily wellness regimen as a non-negotiable line item in your monthly budget, you actively purchase extra years of healthy, active, and independent living.

Purchase 5: Meaningful Travel and Experiential Spending

Retirement is the ultimate opportunity to transition from accumulating assets to accumulating experiences. Financial planners frequently encourage their clients to spend generously on travel, family experiences, and lifelong learning, especially during the early, active years of retirement. Whether you dream of renting a villa in Tuscany, taking your grandchildren on an educational heritage trip, or simply enrolling in specialized art history courses at a local university, experiential spending yields profound psychological dividends. Your mobility and energy levels will naturally fluctuate as the years progress, making the first decade of your retirement the optimal window for demanding travel itineraries.

Gerontological research consistently demonstrates that social engagement and a strong sense of purpose drastically reduce the risk of cognitive decline and depression in older adults. When you spend money to create enduring memories with your loved ones or to pursue a long-dormant passion, you are investing directly in your mental health. Your financial legacy encompasses more than just the inheritance you leave behind; it includes the shared joy and enriching experiences you cultivate today. Do not let the fear of running out of money rob you of the adventures you worked so diligently to afford.

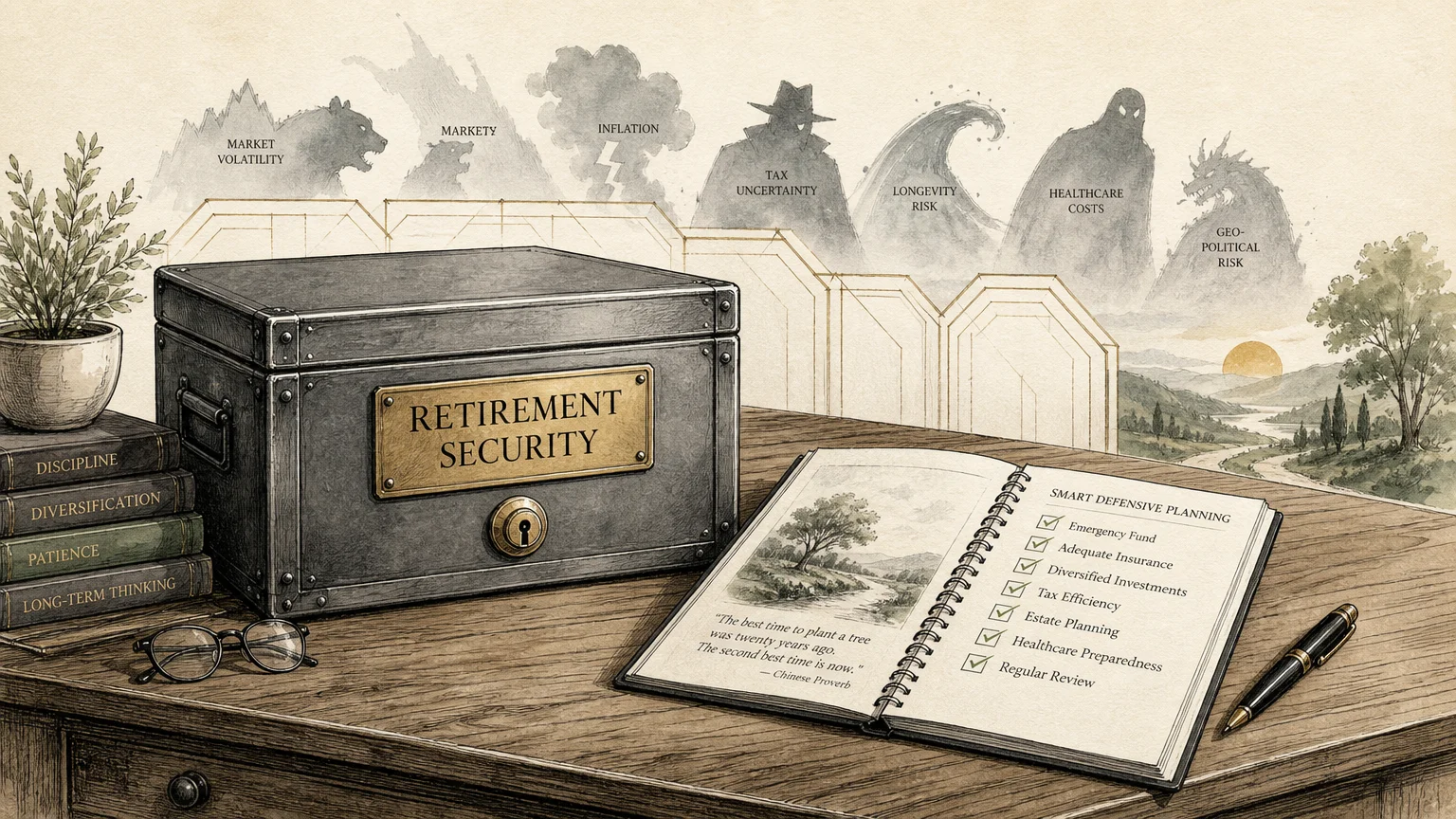

Safeguarding Your Wealth: Risks, Scams, and Benefit Cliffs

While strategic spending enhances your retirement, you must remain vigilant against external threats that seek to compromise your financial security. Older adults are disproportionately targeted by sophisticated financial scams, ranging from cryptocurrency frauds to panicked calls from criminals impersonating grandchildren in distress. You must protect yourself by independently verifying any unexpected requests for money and utilizing the consumer protection resources provided by the IRS to identify emerging impostor schemes. Never rush a financial transaction under pressure, no matter how urgent the request appears.

In addition to outright fraud, you need to navigate systemic financial pitfalls known as benefit cliffs. Taking large, unplanned lump-sum withdrawals from traditional tax-deferred accounts can inadvertently bump you into a higher tax bracket for the year. More importantly, this sudden spike in your adjusted gross income can trigger surcharges on your Medicare Part B and Part D premiums two years down the line. Working closely with your fiduciary planner ensures that your strategic splurges are properly timed and sourced, preventing a single luxury purchase from unraveling your broader financial stability.

Frequently Asked Questions About Retirement Spending

How do I know if I can safely afford to spend more money?

Determining your safe spending capacity requires running detailed cash flow projections using conservative estimates for market returns and inflation. Financial professionals typically utilize Monte Carlo simulations, which test your portfolio against thousands of potential economic scenarios. If your plan demonstrates a high probability of success even in poor market conditions, you have the green light to increase your discretionary spending without jeopardizing your future security. You should update these projections annually to account for actual market performance and changes in your personal health, ensuring your spending remains permanently aligned with reality.

Are proactive home modifications tax deductible?

Under certain circumstances, home modifications made specifically for medical purposes can be deducted from your taxes. If you install a wheelchair ramp, widen doorways, or lower kitchen cabinets to accommodate a physical disability, the IRS may classify these as deductible medical expenses. However, the costs must exceed a specific percentage of your adjusted gross income, and modifications made purely for aesthetic reasons do not qualify. Always consult a certified public accountant to verify your eligibility and keep meticulous records in the event of an audit.

Should I completely pay off my mortgage before spending on travel or experiences?

The decision to eliminate a mortgage depends heavily on your interest rate and psychological comfort. If you hold a fixed-rate mortgage with a historically low interest rate, your money might earn a higher return remaining invested in the market than it would by paying off the debt early. However, many retirees find the emotional relief of living completely debt-free outweighs the mathematical advantages of keeping the mortgage, freeing up their monthly cash flow for travel and experiences. Ensure your reliable fixed income comfortably covers the monthly payment if you choose to keep the debt.

How does pulling money for a large purchase affect my Medicare premiums?

Medicare bases your Part B and Part D premiums on your modified adjusted gross income from two years prior. If you fund a major purchase by taking a significant withdrawal from a tax-deferred account, such as a traditional IRA, that withdrawal counts as taxable income. If this pushes your income above specific threshold tiers, you will be subject to the Income-Related Monthly Adjustment Amount, temporarily increasing your healthcare costs. Planning these withdrawals across multiple tax years helps mitigate this hidden surcharge.

Take Control of Your Retirement Strategy Today

Achieving a fulfilling retirement requires you to actively direct your wealth toward the things that matter most—your safety, your health, and your happiness. Instead of viewing every expense as a depletion of your resources, recognize that thoughtful spending is the ultimate realization of your decades of hard work. Do not wait for a health crisis or a sudden wake-up call to start living the life you planned. Within the next forty-eight hours, review your budget, identify one area where a strategic purchase could immediately improve your daily life, and take the first concrete step toward making it happen.