Relocating to a state with exceptionally low property taxes provides an immediate and lasting boost to your fixed retirement income. By strategically choosing retirement towns where local tax burdens remain light, you preserve critical capital for travel, healthcare, and daily living expenses. Finding the right destination requires looking beyond the sticker price of a home to understand the ongoing carrying costs that dictate your long-term financial security. High property taxes can quietly erode your nest egg, forcing unwanted compromises in your golden years. We explore towns in low property tax states that combine fiscal responsibility with robust community amenities, accessible healthcare, and engaging lifestyle options tailored to retirees. Optimize your relocation strategy today to protect your wealth.

The Current Landscape of Retirement Relocation and Taxation

Property taxes represent one of the most volatile expenses in any retiree’s financial plan. Over the past several years, property values nationwide experienced historic appreciation. While rising home equity benefits your net worth on paper, it simultaneously triggers aggressive municipal tax reassessments that squeeze fixed-income households. If you rely primarily on distributions from an Individual Retirement Account, a pension, or Social Security, a sudden thirty percent spike in your annual property tax bill presents a severe threat to your long-term solvency. State legislatures constantly debate various property tax relief measures; however, the gap between high-tax and low-tax regions continues to widen dramatically.

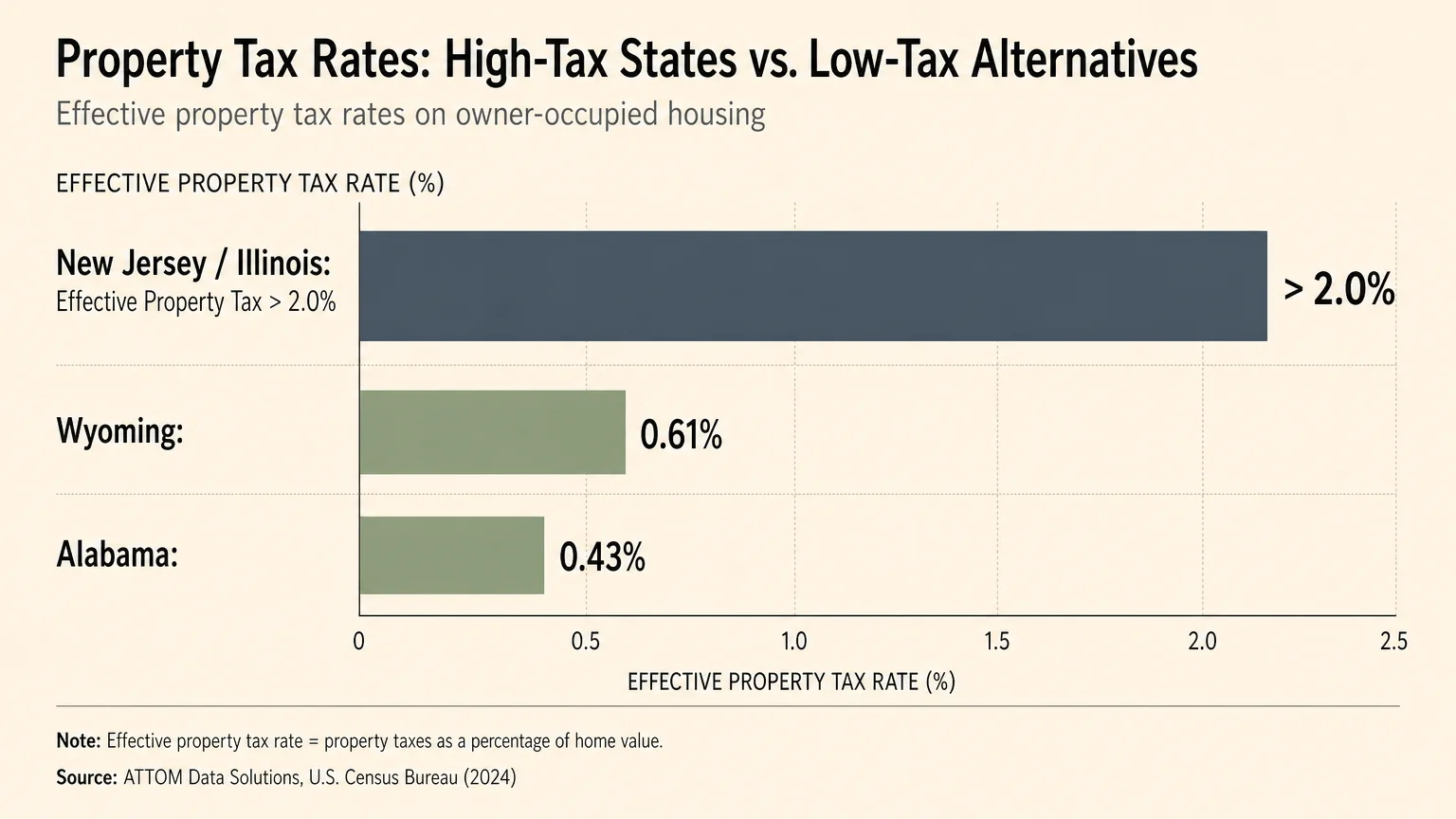

By relocating from a state where effective property tax rates routinely exceed two percent—such as New Jersey or Illinois—to a more tax-friendly environment, you effectively grant yourself a permanent pay raise. This strategic shift in capital allocation creates a robust buffer against future economic volatility and ensures your savings last significantly longer. Recent Bureau of Labor Statistics consumer price data confirms that shelter costs consistently outpace broader inflation metrics, making geographic tax arbitrage a highly effective tool for modern retirees. You must view your primary residence not just as a place to live, but as a heavily taxed asset that requires active management.

Strategy Pillar One: Mastering Income Planning and Tax Relief

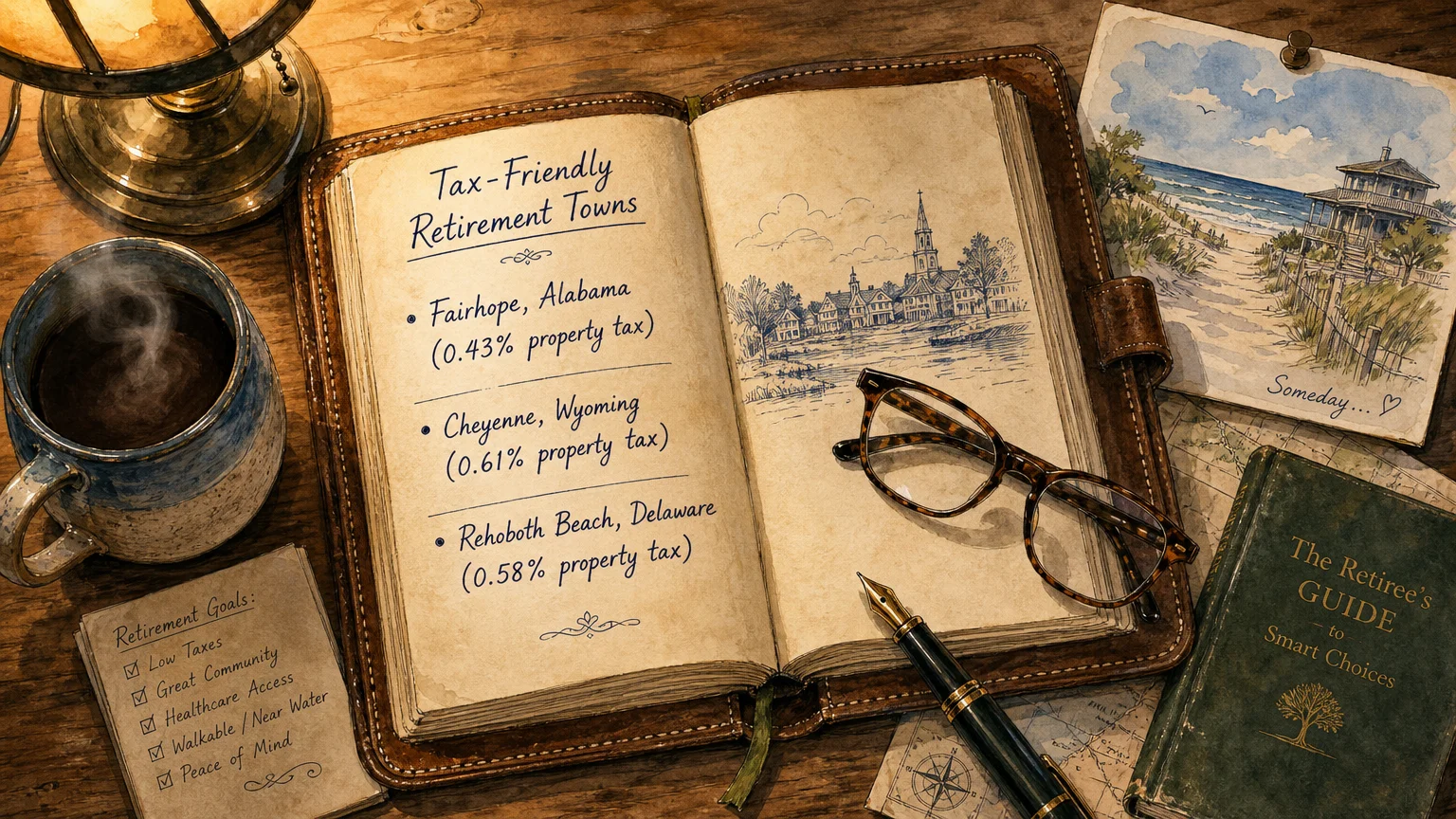

Selecting the right retirement town requires a deep dive into local tax structures to maximize your household income. Alabama currently holds the title for the lowest average effective property tax rate in the country, hovering around 0.43 percent. Towns like Fairhope offer a vibrant coastal setting on Mobile Bay without the crushing annual tax burden found in competing waterfront destinations. You can enjoy a thriving local economy and beautiful natural surroundings while keeping thousands of dollars in your pocket each year. Reallocating those funds provides immediate flexibility for your monthly budget.

Wyoming offers another compelling financial environment for retirees seeking aggressive tax relief. Cheyenne features an effective property tax rate of roughly 0.61 percent and completely lacks a state income tax. This dual benefit allows your retirement withdrawals to stretch much further. Similarly, Delaware presents a highly attractive profile for East Coast retirees who wish to remain near major metropolitan hubs. Rehoboth Beach boasts an effective property tax rate near 0.58 percent, levies zero state sales tax, and offers generous property tax exemptions for older adults who establish permanent residency.

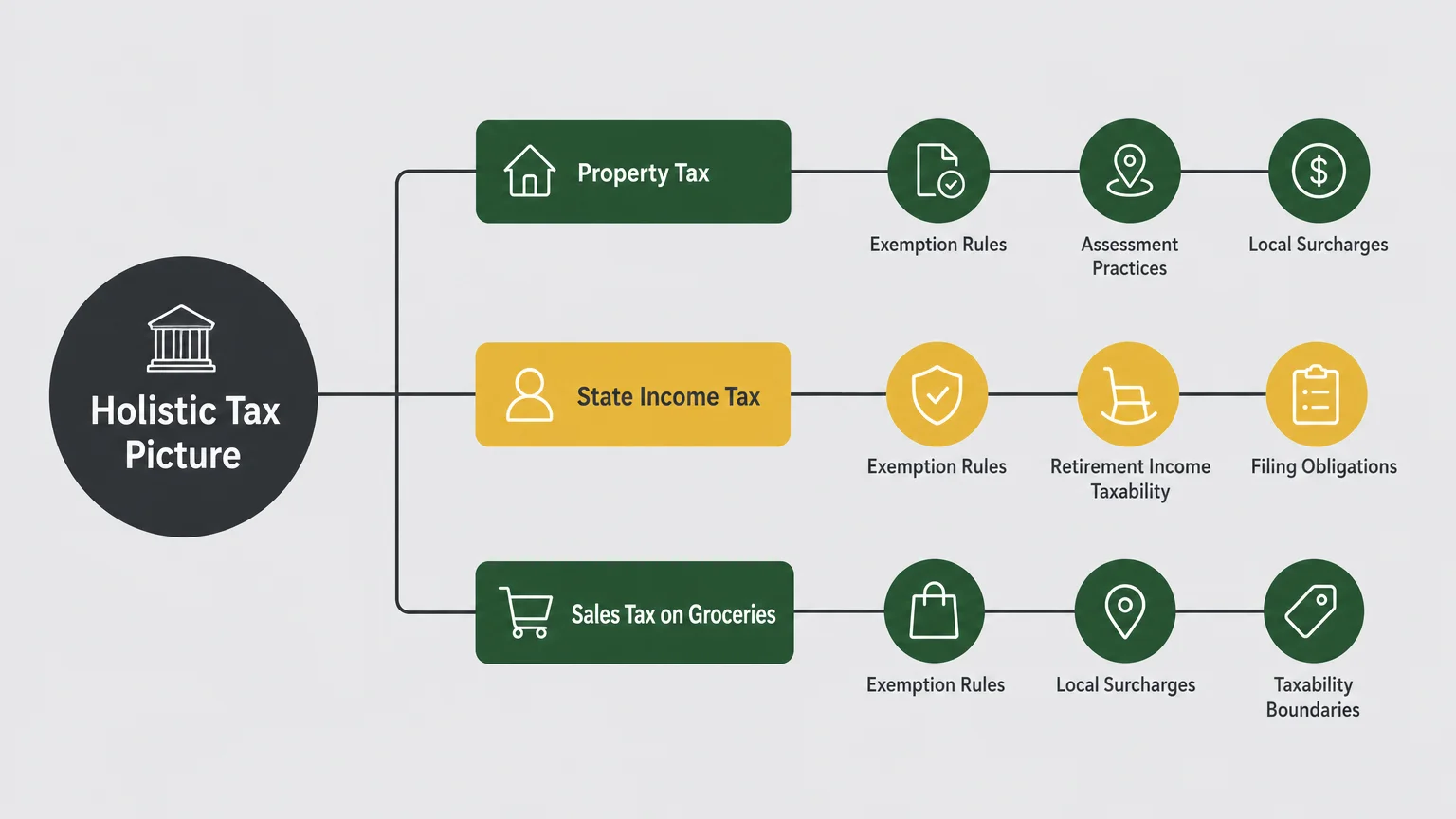

However, you must evaluate the comprehensive tax picture before packing your bags. A town might offer incredibly low property taxes, but if the state taxes your essential income streams or imposes massive sales taxes on everyday groceries, your net financial gain diminishes rapidly. Reviewing Social Security Administration taxation guidelines will help you determine exactly how your specific target state treats your hard-earned benefits. Balancing property tax relief with favorable income and sales tax conditions forms the essential foundation of a resilient retirement strategy.

Strategy Pillar Two: Engineering Your Ideal Lifestyle Design

Achieving financial affordability means very little if your new community fails to support a fulfilling daily life. Lowering your carrying costs frees up significant cash flow, allowing you to prioritize intentional lifestyle design. When you shed a massive property tax bill, you reclaim thousands of dollars annually that you can redirect toward passions that genuinely enrich your retirement experience. Towns like Fairhope and Rehoboth Beach host robust arts scenes, continuing education programs, and civic organizations that actively welcome older adults into their local social fabric.

Embracing these vibrant environments means engaging with diverse cultural backgrounds and finding neighbors who share your values and interests. Accessibility plays a foundational role in this lifestyle design; you want a town where daily necessities—grocery stores, social clubs, recreational spaces, and public parks—are easy to navigate regardless of varying mobility levels. Small but thriving communities often feature highly walkable downtown districts that naturally encourage daily social interaction and physical activity. By securing an affordable tax base, you ensure your social calendar remains full.

A low-tax town only serves your long-term needs if the day-to-day experience genuinely brings you joy and keeps you socially connected to the broader community. You should spend significant time visiting these towns during different seasons to verify that the local culture aligns with your personal expectations. By focusing on communities that offer a rich tapestry of activities and accessible physical infrastructure, you guarantee that your property tax savings translate directly into an elevated, active standard of living.

Strategy Pillar Three: Prioritizing Health and Wellness Accessibility

Favorable tax codes cannot compensate for a lack of life-saving medical care. When you explore retirement towns with exceptionally low property tax rates, you must rigorously scrutinize the local health infrastructure. Rural havens in states like Wyoming or Alabama might offer spectacular scenery and rock-bottom tax bills, but they frequently lack specialized medical facilities. You must evaluate your prospective town’s immediate proximity to major regional hospitals, comprehensive emergency services, and dedicated specialty clinics that can actively manage complex chronic conditions.

Furthermore, your health insurance coverage depends heavily on your geographic location. Changing your primary residence can drastically alter your provider network, potentially severing ties with doctors you have trusted for decades. You should utilize Medicare care comparison tools to verify the quality and availability of healthcare facilities in your desired zip code before committing to a permanent move. Confirming that your specific coverage translates to your new state prevents catastrophic out-of-pocket expenses.

Ensuring that your new town can easily support varying mobility needs and provide highly reliable outpatient services is a non-negotiable step in your relocation process. Consider exactly how easy it will be to attend routine check-ups, secure prescription refills, or access physical therapy without driving for hours. A truly optimal retirement destination seamlessly balances aggressive property tax savings with immediate, uncompromising access to high-quality healthcare networks.

Expert Voices on Relocation Realities

Financial planners consistently warn against a dangerous phenomenon known as property tax tunnel vision. This cognitive bias occurs when retirees fixate entirely on a state’s headline property tax rate while completely ignoring income taxes, sales taxes, and local municipal fees. Certified Financial Planner professionals strongly advise running a comprehensive mock tax return for your prospective new state; this vital exercise reveals the true financial impact of your relocation by accounting for all local levies. Your financial health ultimately depends on your total tax burden, not just the single bill you receive from the county assessor.

Simultaneously, gerontologists emphasize the critical importance of the physical built environment. Aging in place successfully requires homes and communities that adapt to your changing physical needs over time. Experts suggest prioritizing towns that score well on standardized livability indices, ensuring that your low-tax destination also provides highly accessible public spaces, robust community support networks, and adequate transportation options. Reviewing resources like AARP community livability standards provides a highly structured framework for evaluating potential neighborhoods. By synthesizing hard financial analysis with practical gerontological insights, you can identify retirement towns that protect your wallet while fully supporting your physical independence.

Navigating Risks and Building Safeguards

Relocating to a new state introduces several distinct financial risks that demand your immediate attention and proactive planning. First, you must consider the hidden costs of homeownership that can quietly neutralize your carefully calculated property tax savings. Homeowners association fees, special community assessments, and soaring property insurance premiums—particularly in coastal towns that routinely experience severe weather patterns—can quickly inflate your monthly housing budget well beyond your initial projections. You must request comprehensive historical data on these localized expenses before finalizing any property purchase.

Additionally, you must remain highly vigilant against real estate fraud and deceptive marketing practices. Out-of-state buyers frequently fall victim to predatory developers or investment scams that misrepresent the physical condition of a property, the true cost of local municipal utilities, or the timeline for promised community amenities. Always hire independent local inspectors and secure your own legal representation to verify every detail of your transaction. The Federal Trade Commission provides essential alerts regarding common real estate schemes that aggressively target relocating retirees.

Finally, be acutely aware of the benefits cliff in certain jurisdictions. Many states offer localized property tax breaks specifically for senior citizens, but these generous exemptions often phase out abruptly if your retirement income exceeds strict, predetermined thresholds. You must understand exactly how your specific income streams will interact with local exemption rules to avoid sudden, unexpected tax liabilities that derail your budget.

Frequently Asked Questions

Do states with low property taxes make up for it with high income taxes?

Sometimes they do, but this is not a universal rule. States like Texas and Florida levy zero state income tax but offset that municipal revenue loss with significantly higher property taxes. Conversely, states like Wyoming and Nevada offer both exceptionally low property tax rates and zero state income tax, making them highly efficient financial environments for retirees. You must thoroughly evaluate the aggregate tax burden rather than viewing property taxes in strict isolation to understand the true cost of residency.

How does my age affect my property tax assessments?

Many states and local municipalities offer senior citizen property tax freezes, generous exemptions, or deferral programs once you reach age sixty-five. These localized programs can permanently lock in your home’s assessed value at a specific baseline or provide a substantial flat deduction directly from your annual tax bill. However, these programs frequently feature strict income limitations, meaning you must carefully verify your long-term eligibility based on your projected retirement distributions.

Are there hidden financial costs to relocating for a lower tax rate?

Yes; you must diligently account for peripheral expenses that accompany a major geographic move. Relocating far from your established support network often results in significantly increased annual travel costs to visit family and friends. Furthermore, moving to certain low-tax regions might expose you to much higher property insurance premiums if the area is vulnerable to specific climate risks, or it might require joining a mandatory homeowners association that charges steep monthly fees to cover municipal services lacking in the broader jurisdiction.

Will changing my primary residence affect my health insurance and Medicare coverage?

If you utilize Traditional Medicare alongside a standardized Medigap policy, your geographic mobility remains highly flexible across the entire country. However, if you rely heavily on a Medicare Advantage plan, relocating to a new county or a completely different state typically forces you to select an entirely new health plan with a completely different network of local medical providers. You must actively research the provider networks available in your target destination to prevent unexpected and costly gaps in your medical coverage.

Your Next Steps for a Financially Sound Relocation

The prospect of relocating to dramatically reduce your tax burden should fill you with strategic optimism rather than financial anxiety. By conducting thorough, multifaceted research and carefully balancing your economic metrics with your lifestyle priorities, you can seamlessly design a retirement that is both financially secure and deeply fulfilling. Finding a vibrant community that highly respects your budget while actively supporting your physical well-being represents the ultimate victory in modern retirement planning.

Your next step is clear and straightforward. Within the next forty-eight hours, select two low-tax states that genuinely pique your interest and aggressively research their specific community amenities, property tax exemption rules, and regional healthcare networks. Taking this single, highly actionable step will instantly build necessary momentum and put you firmly on the path toward a more affordable, engaging, and socially enriching retirement destination.