Securing your retirement income takes less time than drinking a cup of coffee when you apply for Social Security benefits online. The Social Security Administration processes over six million retirement applications annually, and utilizing their digital portal eliminates long waits at local field offices. You can claim your earned benefits from your living room, complete the necessary forms in roughly fifteen minutes, and track your approval status in real time. This digital transformation means you no longer need to spend hours on hold or navigating traffic to secure your financial future. Claiming your retirement benefits is straightforward once you know exactly what documents to gather and which digital buttons to click.

Recent Policy Updates Influencing Your Retirement Timeline

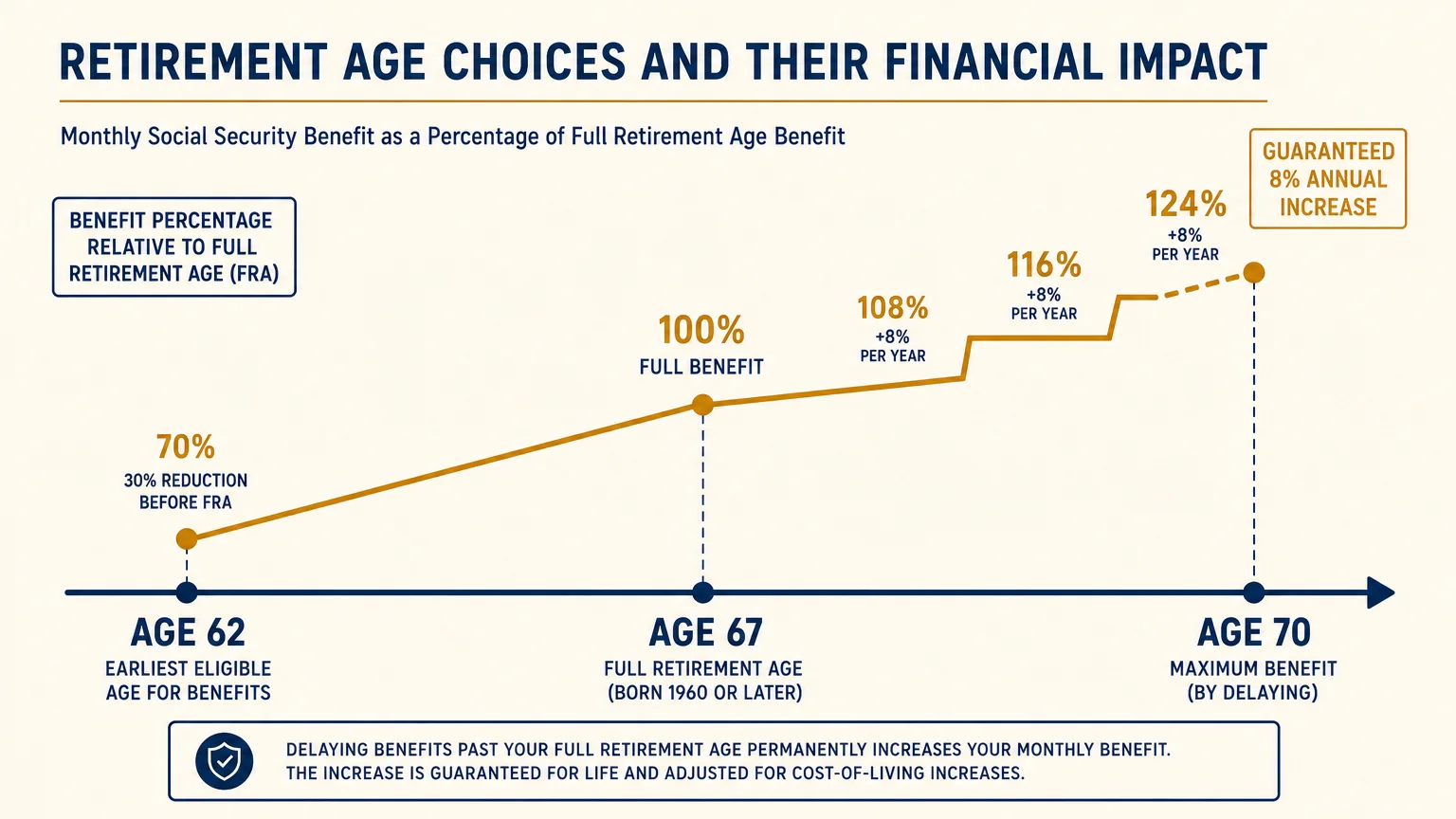

Understanding the current economic environment empowers you to make smarter decisions about when to officially file for your benefits. In recent years, inflation has pushed the cost of living significantly higher, prompting annual cost-of-living adjustments that directly impact your monthly checks. As of 2026, those born in 1960 or later face a full retirement age of exactly sixty-seven years old. Claiming even one month before reaching this milestone results in a permanent reduction of your monthly payout; conversely, delaying your application past your full retirement age guarantees an eight percent increase per year until age seventy. Securing that eight percent guaranteed return represents one of the most powerful financial strategies available to modern retirees, easily outpacing the predictable yields of traditional fixed-income investments.

You must also consider the intersection of employment and claiming benefits. The Bureau of Labor Statistics tracks workforce participation, showing a steady increase in Americans choosing to work part-time well into their late sixties. If you file for Social Security online before reaching your full retirement age while continuing to earn a paycheck, you face the earnings test. Earning above a specific annual threshold triggers a temporary withholding of a portion of your benefits. These withheld funds are not permanently lost; the administration recalculates your monthly payment upward once you reach full retirement age to account for the months your benefits were reduced. Knowing these rules ensures you do not encounter sudden cash flow interruptions after successfully submitting your online application, allowing you to transition into partial retirement without accidentally undermining your household budget.

Pillar One: Income Planning and Your Online Application

Creating an account on the federal portal forms the absolute foundation of your income planning strategy. Before you even initiate the application, you need to review your earnings record for accuracy. Establishing a digital profile gives you immediate access to your personalized statements, allowing you to verify that every year of your employment history reflects your actual taxable income. Missing earnings from previous decades can permanently depress your monthly benefit calculation, making this verification step absolutely critical to your long-term financial health; you do not want an administrative error from twenty years ago reducing your income today. Once you confirm your earnings history, you can confidently begin the formal application process knowing your future checks will reflect your true lifetime contributions.

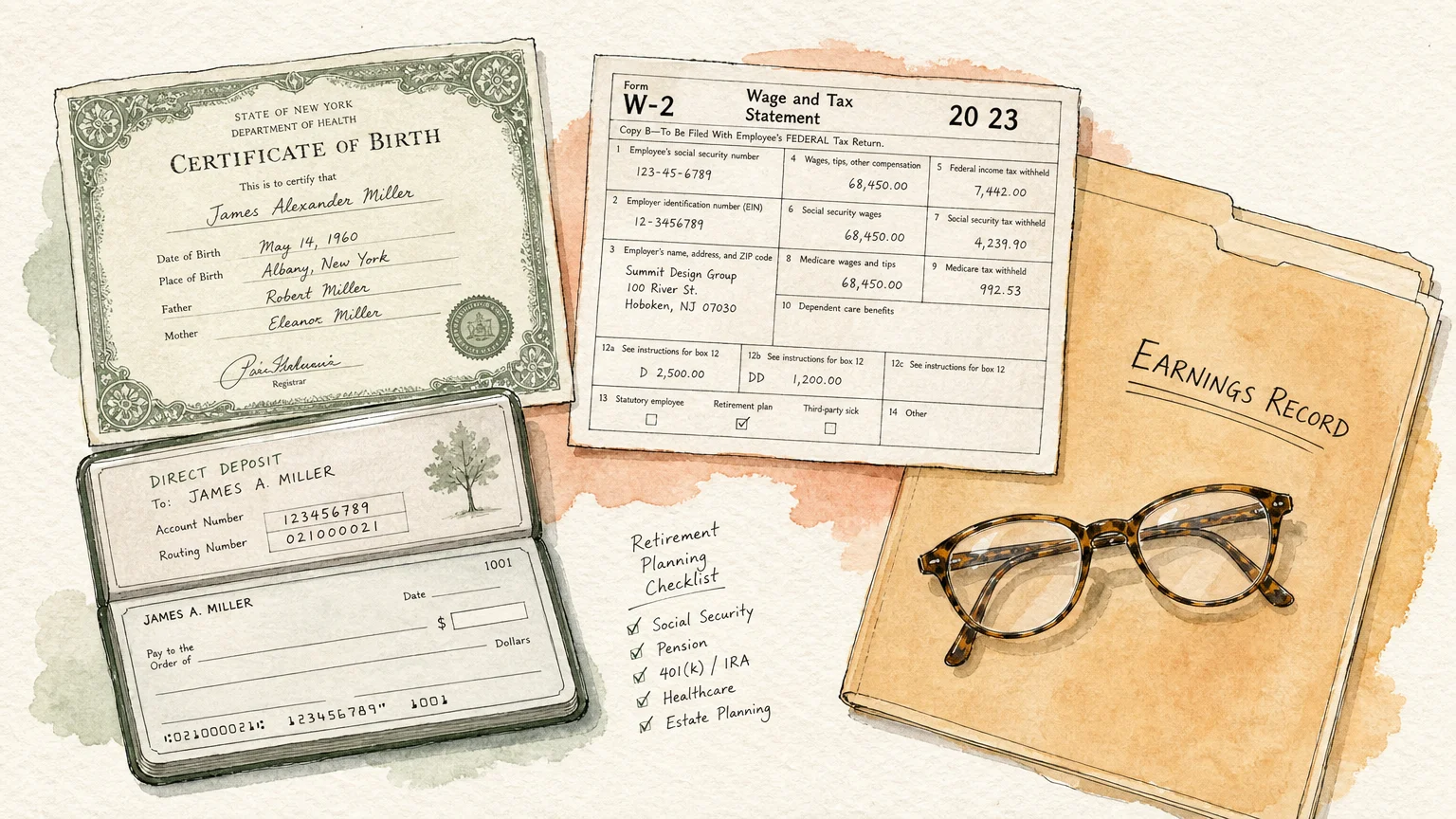

You should gather specific physical documents before you sit down at your computer to complete the forms. Ensure you have your birth certificate, your most recent W-2 forms or self-employment tax returns, and your banking details for direct deposit setup. The official online application portal guides you through a series of straightforward questions regarding your citizenship, marital history, and military service. The system automatically saves your progress as you move through the digital pages; if you need to pause and find a specific document in your filing cabinet, you can log out and return later without losing your previously entered data. Completing this digital process places you firmly in control of your incoming cash flow and eliminates the anxiety of relying on paper mail to deliver your financial lifeline. Taking ownership of this process online also bypasses the notoriously long wait times associated with calling the national toll-free number.

Pillar Two: Designing Your Lifestyle Around Guaranteed Income

Securing a predictable monthly deposit provides the psychological freedom necessary to design a fulfilling retirement lifestyle. Relying on market investments alone often forces retirees to obsessively monitor stock tickers and economic news, but Social Security offers a foundation of guaranteed income backed entirely by the federal government. You can allocate this dependable revenue stream toward your baseline expenses—such as property taxes, groceries, health insurance premiums, and utilities—freeing your personal savings to fund the lifestyle goals you dreamed about during your working years. Whether you want to fund cross-country road trips in a recreational vehicle, take up expensive hobbies, or sponsor educational accounts for your grandchildren, knowing your basic needs are covered changes your daily outlook and drastically lowers financial anxiety.

This guaranteed income also empowers you to explore purpose-driven activities without the relentless pressure of earning a substantial wage. Many retirees transition into consulting, mentoring, or volunteering within their local communities once their fixed costs are met. When your monthly living expenses are reliably funded by your benefits, you can afford to accept lower-paying passion projects or dedicate substantial hours to nonprofit organizations that champion causes you care about. Establishing this financial baseline early through a quick digital application effectively shifts your mindset from survival to contribution. You gain the autonomy to dictate exactly how you spend your energy and time, transforming your retirement years into a period of deep personal fulfillment rather than a stressful stretch of financial rationing.

Pillar Three: Navigating Health Care and Medicare Enrollment

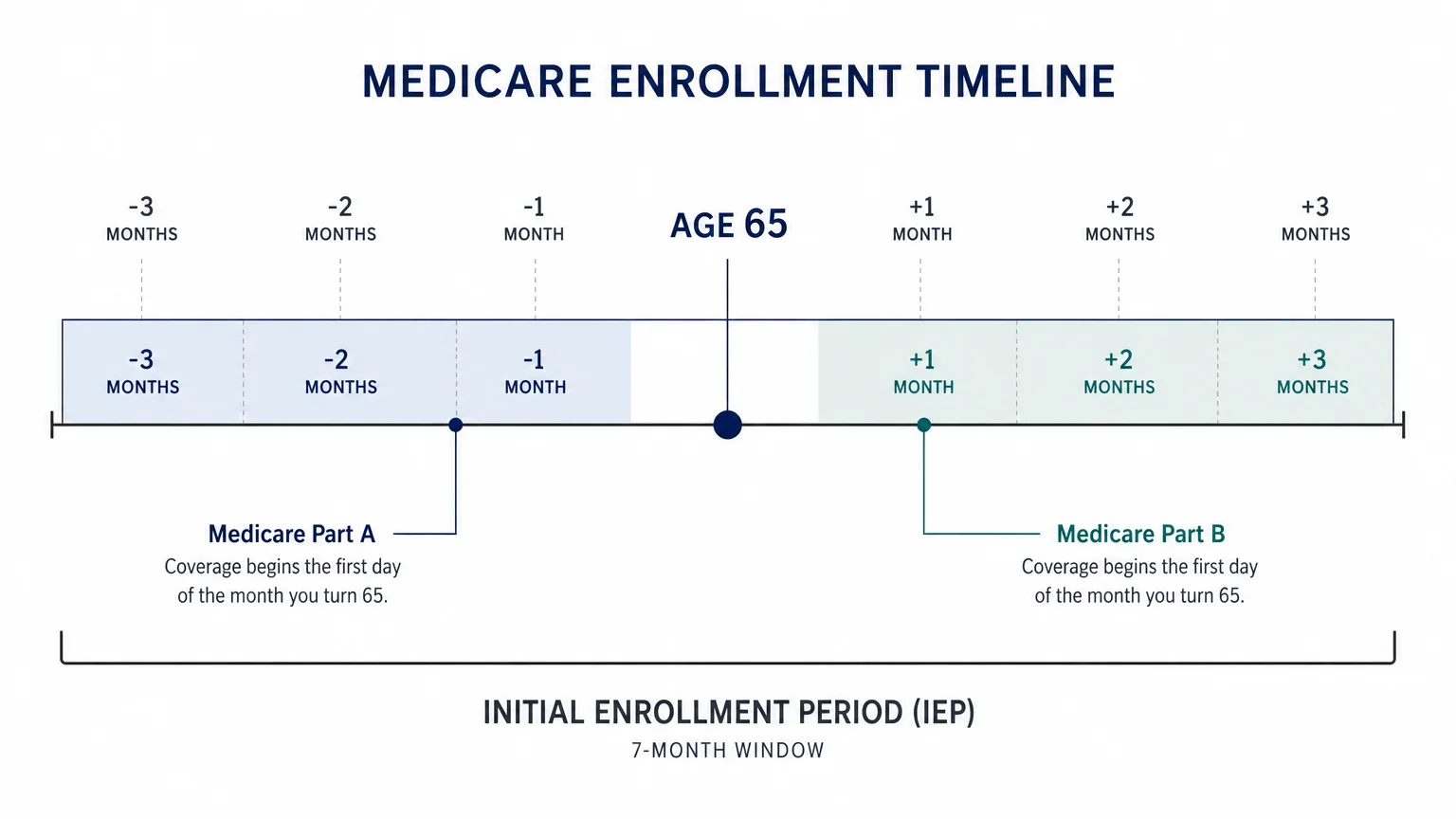

Filing for your retirement benefits directly intersects with your health care strategy, particularly regarding Medicare enrollment. If you apply for Social Security benefits at least four months before your sixty-fifth birthday, the government automatically enrolls you in Medicare Part A and Part B. You will simply receive your red, white, and blue card in the mail without completing a separate health care application. This seamless integration prevents you from missing crucial enrollment windows that could otherwise result in lifetime late penalties for your health coverage. Avoiding these permanent financial penalties remains one of the most compelling reasons to coordinate your income and health care timelines carefully.

However, if you choose to delay your Social Security application to maximize your monthly income, you must take proactive steps to secure your health insurance. You will need to visit the federal health insurance portal to manually enroll in Medicare when you approach your sixty-fifth birthday. Balancing your desired retirement income with your immediate healthcare needs requires precise calculation and foresight. Premiums for Medicare Part B are automatically deducted from your Social Security checks once you begin receiving them; understanding this deduction prepares you for the exact net amount that will hit your bank account each month. Addressing your health coverage simultaneously with your income planning ensures you remain physically and financially protected throughout your aging journey, safeguarding your nest egg from unexpected medical emergencies.

Expert Perspectives on Timing Your Claim

Financial planners and gerontologists consistently emphasize that claiming your benefits represents a highly personalized decision rather than a simple mathematical equation. Certified Financial Planner professionals often advise clients to evaluate their longevity expectations alongside their current portfolio balances and sequence of returns risk. If you possess robust investments and a family history of living well into your nineties, drawing down from your portfolio while allowing your Social Security benefits to grow until age seventy often maximizes your lifetime payout. Conversely, if you face immediate health challenges, lack sufficient private savings, or simply wish to preserve your investment capital during a market downturn, filing early provides the essential liquidity required to maintain your quality of life without liquidating assets at a loss.

Gerontologists approach the claiming decision from a psychological perspective, noting that financial stability drastically reduces cortisol levels and stress-related illnesses in older adults. Experts in aging research highlight that the certainty of a monthly deposit often provides substantially more mental health benefits than the mathematical optimization of waiting for a slightly larger check years down the road. If delaying your application causes daily anxiety about paying bills, forces you to skip necessary medical care, or prevents you from enjoying your healthiest active years, the emotional cost far outweighs the financial gain. Ultimately, the best time to fire up your computer and submit your online application depends entirely on balancing your unique physical health, psychological comfort, and available financial resources.

Safeguarding Your Benefits from Scams and Financial Pitfalls

The convenience of applying for benefits online unfortunately coincides with a massive rise in sophisticated cybercrime targeting older adults. Criminals frequently utilize phone calls, text messages, and deceptive emails claiming your Social Security number has been suspended due to fraudulent activity or that your application requires an immediate processing fee. You must understand that federal agencies will never call you demanding immediate payment via gift cards, wire transfers, or cryptocurrency. Protecting your financial identity requires strict vigilance; you should routinely monitor your bank accounts and report any suspicious contact directly to the fraud watch network resources available through reputable aging advocacy organizations. Never click on unverified links embedded in text messages that pretend to offer status updates on your pending benefit application.

Beyond outright theft, you must also navigate legitimate financial pitfalls like the taxation of your benefits. Many new retirees assume their monthly checks are entirely tax-free, leading to incredibly unpleasant surprises during tax season. The Internal Revenue Service guidelines for seniors specify that up to eighty-five percent of your Social Security income becomes taxable if your combined income exceeds certain federal thresholds. If you draw significant funds from a traditional individual retirement account, sell highly appreciated real estate, or continue working part-time, you could easily trigger these taxes. To avoid this steep benefit cliff, you can request that the government withhold a percentage of your monthly check for federal taxes during your initial online application, ensuring you do not face a massive tax bill the following April.

Frequently Asked Questions About the Digital Application

How long does it take for the administration to process my online application?

The processing time typically ranges from two to four weeks after you hit the submit button on the digital portal. The administration will mail you a formal award letter detailing your exact monthly benefit amount and the date of your first scheduled payment. If the agency requires additional documentation—such as an original birth certificate, naturalization papers, or proof of military service—they will contact you directly, which can significantly extend the processing timeline. Applying three to four months before you want your payments to officially begin provides an ample buffer for any unforeseen delays and ensures your cash flow remains uninterrupted.

Can I change my mind after I submit my application online?

You have exactly one opportunity to withdraw your application and reverse your claiming decision within twelve months of your initial approval. If you unexpectedly return to the workforce or realize you claimed too early and want to build delayed credits, you can file a formal withdrawal request. However, you must completely repay every single dollar you and your family members received from your earnings record, including any Medicare premiums deducted from your checks. After this strict twelve-month window closes, your decision to claim benefits becomes permanent, though you can still voluntarily suspend payments at your full retirement age to earn delayed credits moving forward.

Is the online application portal fully secure for my personal data?

The federal government employs exceptionally robust encryption and strict identity verification protocols to protect your sensitive personal information during the digital application process. When you create your account, you must complete multi-factor authentication, which requires you to actively confirm your identity using a secondary device like your mobile phone or a secure email address. This layered security approach makes it exceedingly difficult for unauthorized individuals to access your earnings record, view your personal history, or reroute your direct deposits. Always ensure you are using a secure, private internet connection at home—rather than public Wi-Fi at a coffee shop or library—when submitting your application.

What happens if I make a mistake while filling out the online forms?

The digital application features intelligent, built-in error checking mechanisms that immediately alert you if you leave a required field blank or input conflicting biographical information. If you realize you submitted inaccurate data after fully completing the application, you cannot simply log back into the system and edit the finalized document. Instead, you must contact the administration directly by phone or visit a local field office to speak with a representative who possesses the authority to officially amend your file. Taking your time, double-checking your banking routing numbers, and meticulously reviewing your answers before clicking the final submission button prevents these stressful administrative headaches.

Take Your Next Step Today

Taking control of your retirement timeline requires decisive action rather than passive contemplation. You now possess the strategic knowledge required to navigate the digital application process with complete confidence and protect your hard-earned benefits. In the next forty-eight hours, commit to establishing your secure digital account on the federal portal and thoroughly verifying your lifetime earnings record. This single proactive step takes less than ten minutes but sets the operational stage for decades of financial security. Gather your documents, secure your internet connection, and claim the benefits you spent your entire working life building. Your future self will deeply appreciate the peace of mind that comes from proactively securing your guaranteed income today.