A recent federal court ruling could put thousands of dollars back in your pocket, but you must act before July 10, 2026, to secure your payout. If you paid IRS failure-to-file penalties, failure-to-pay fees, or excess interest between January 2020 and May 2023, you are likely eligible for a COVID-era tax refund. The pandemic forced many retirees to navigate chaotic disruptions, leading to unavoidable filing delays and steep IRS fees. Thanks to the Kwong v. United States decision, those years are officially recognized as a federally protected disaster period. Time is running out to preserve your legal right to this money. By filing a protective claim today, you safeguard your financial health and recover funds that belong to you.

The Policy Snapshot: Why the IRS Might Owe You Money

The story behind this potential windfall begins in late 2025 with a landmark federal court decision known as Kwong v. United States. For years, taxpayers argued that the COVID-19 pandemic severely hindered the public’s ability to meet strict federal deadlines. Courthouses were closed; accounting firms operated at half-capacity; and millions of older Americans isolated at home, unable to access professional help.

The federal court agreed, determining that the COVID-19 emergency qualified as a federally declared disaster under the tax code. Because tax law provides automatic deadline extensions during declared disasters, the ruling established a protected window from January 2020 through July 10, 2023. If the IRS charged you a failure-to-file penalty, a failure-to-pay penalty, or related interest during that time, those charges may have been assessed illegally.

However, the government is appealing the decision. The IRS will not automatically deposit this money. You must take an active role. Because refund claims are bound by a three-year statute of limitations, the deadline to challenge penalties assessed during the court-defined disaster period is July 10, 2026. Missing this date means surrendering your refund forever.

Income Planning: How to Secure Your Refund and Protect Your Cash Flow

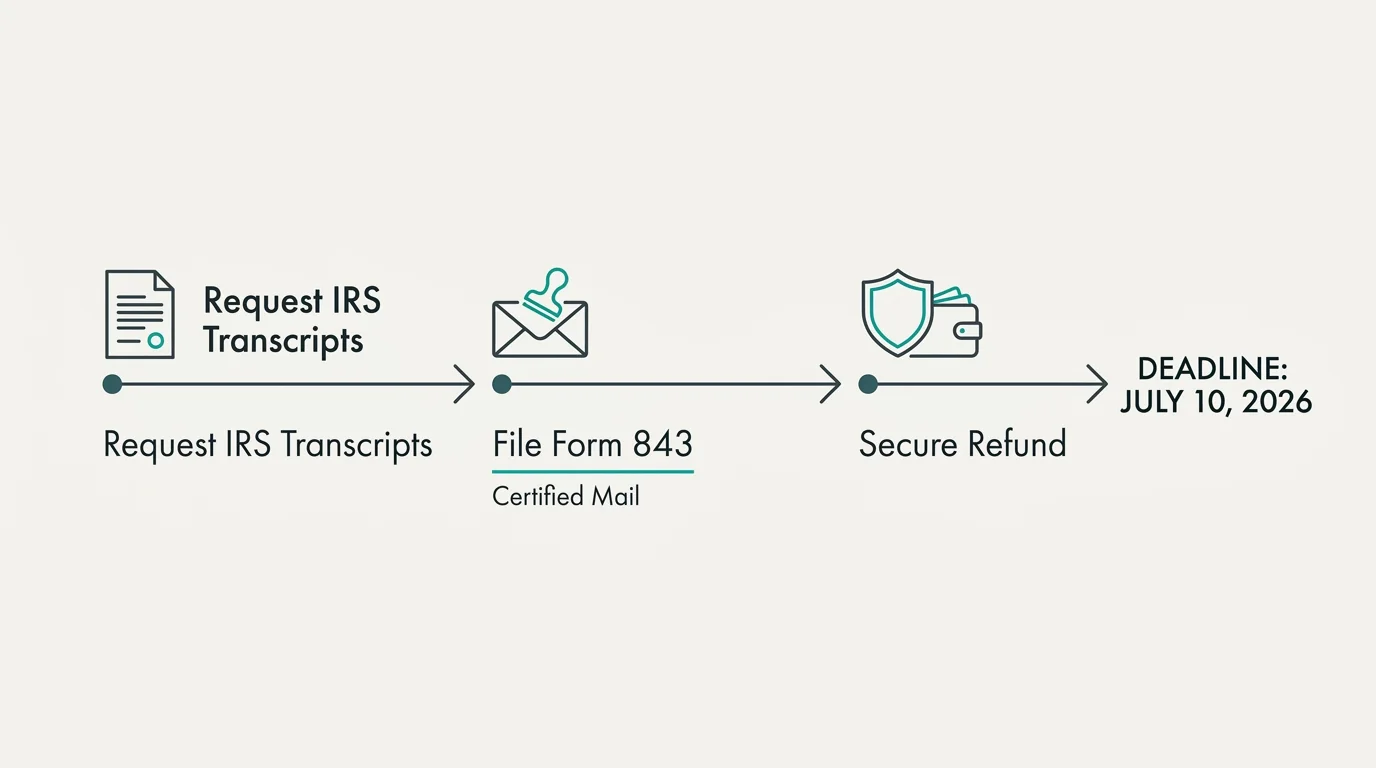

Locating old tax documents can feel overwhelming. Start by requesting your tax transcripts directly from the Internal Revenue Service (IRS) portal. Review your Account Transcripts for the tax years 2019, 2020, 2021, and 2022. Look for any line items indicating penalty assessments or interest charges.

Once you confirm you paid these penalties, your next step is filing Form 843, officially known as the Claim for Refund and Request for Abatement. Since the Kwong case is navigating appellate courts, tax professionals call this a protective claim. You are telling the IRS that if the courts rule in favor of taxpayers, you are on the record claiming your refund before the deadline expires. Mail your Form 843 via certified mail with a return receipt requested. Having a tracking number guarantees you can prove you met the July 10 deadline.

If successful, integrate the windfall into your broader income strategy. Data from the Bureau of Labor Statistics shows inflation continues to squeeze budgets. Earmark recovered funds to bolster emergency cash reserves. A robust cushion prevents you from liquidating investments during market downturns, preserving your portfolio’s earning power.

Lifestyle Design: Allocating Recovered Funds with Intention

Retirement should be a season of intentional living. When unexpected money arrives, it provides a rare opportunity to improve your quality of life without disrupting your budget. If you depend heavily on benefits from the Social Security Administration, recovering these funds offers a vital buffer against rising costs.

Consider how a penalty refund could fund home modifications. Installing grab bars, upgrading to a walk-in shower, or adding improved lighting significantly reduces fall risks. Upgrading your environment reduces long-term maintenance costs and preserves your personal autonomy. Small, intentional investments in your living space yield compounding benefits for your daily happiness and comfort. These upgrades enhance your independence, allowing you to remain in your home longer.

Alternatively, allocate this money toward experiences sacrificed during the pandemic. If you missed milestone events in 2020 and 2021, use recovered funds to rebuild those connections. Book a direct flight to visit grandchildren or secure a rental property for a family reunion. Be cautious about openly discussing a sudden financial windfall with extended family. Protect your financial autonomy by maintaining clear boundaries and prioritizing your own stability first.

Health and Wellness: Investing Your Tax Windfall in Longevity

Financial security and physical health are deeply intertwined. Chronic financial stress elevates cortisol levels, which can lead to hypertension and a weakened immune system. Reclaiming money from the IRS actively relieves psychological burdens.

If your protective claim results in a payout, reinvest those dollars into your health. Traditional Medicare leaves gaps in areas crucial to healthy aging—most notably dental, vision, and hearing care. A refund could fully cover custom dentures, specialized lenses, or copayments for modern hearing aids. Addressing hearing loss is vital, as peer-reviewed gerontology studies strongly link untreated hearing impairment to cognitive decline.

You can also direct this money toward preventative wellness programs not fully covered by insurance. Consider the hidden costs of aging that standard coverage overlooks, such as specialized physical therapy. A targeted cash infusion allows you to prioritize these essential treatments without disrupting your monthly budget. Hiring a certified personal trainer specializing in senior mobility or investing in orthopedic footwear pays massive dividends. Proactively funding physical wellness minimizes the risk of catastrophic out-of-pocket expenses later.

Expert Voices: What the Professionals Are Advising Right Now

Financial planners and elder care advocates urge older adults not to ignore this narrow window of opportunity. The consensus among Certified Financial Planner professionals is that complacency is the biggest threat to securing your refund. Many assume that if the government owes them money, a check will automatically appear. With the COVID tax penalty refund, inaction guarantees zero results.

The pandemic forced countless seniors to take early IRA distributions or miss estimated quarterly payments because they physically could not reach their tax preparer, explains one independent financial advisor tracking the Kwong litigation. Filing a protective claim is a low-risk, high-reward strategy. You spend a few dollars on certified mail to potentially recover thousands.

Gerontologists echo this sentiment. Reclaiming these improperly assessed penalties is an act of restoring agency. Taking control over your tax records reinforces your financial independence and proves your economic rights matter.

Risks and Safeguards: Navigating Scams and Tax Traps

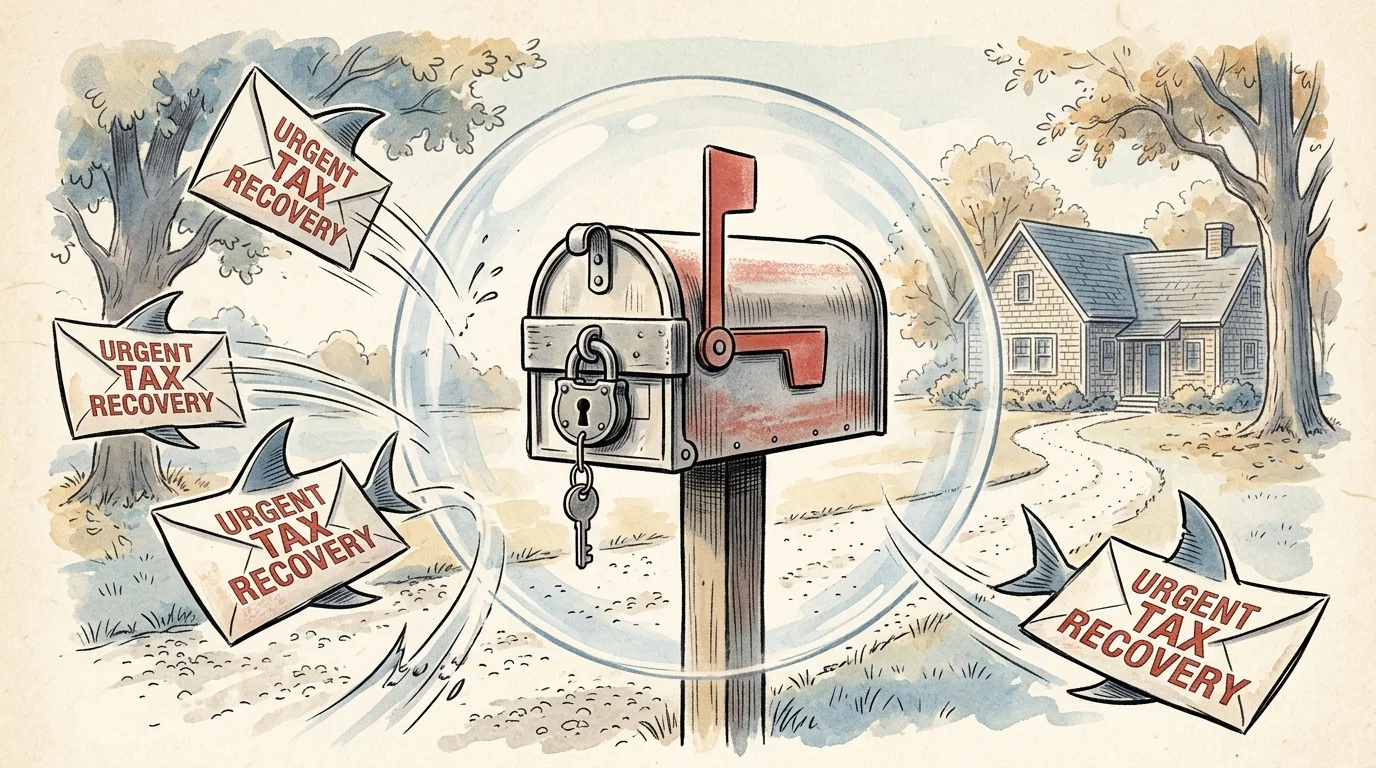

Where there is money, there are inevitably predators. Cybercriminals are ramping up targeted campaigns against retirees as the deadline approaches. Scammers are sending sophisticated emails and text messages claiming to be the IRS, offering to expedite your COVID penalty refund in exchange for a fee or your Social Security number.

The IRS will never initiate contact via text or email to discuss a refund. If you receive a suspicious communication, report it to AARP’s Fraud Watch Network. Additionally, understand the secondary tax implications of a successful claim. While a tax penalty refund is generally not taxable income, any interest the IRS pays you on that refund is taxable. This interest could inflate your Adjusted Gross Income.

For most retirees, this bump is negligible. However, if you are straddling an income threshold, a sudden spike could trigger an Income-Related Monthly Adjustment Amount (IRMAA) surcharge on your Medicare Part B and Part D premiums. Review current IRMAA brackets at Medicare.gov to ensure a windfall does not inadvertently increase your healthcare costs. Keep your tax advisor in the loop to offset unexpected taxable interest.

Frequently Asked Questions About the 2026 COVID Tax Refund

Navigating tax law is rarely straightforward, especially when it involves retroactive changes and ongoing court battles. To help clarify the process, here are answers to the most common questions retirees are asking about this unique refund opportunity.

Do I qualify for this specific COVID tax refund?

You are likely eligible if you paid failure-to-file, failure-to-pay, or estimated tax penalties on your federal returns for tax years 2019 through 2022. You must have incurred these charges between January 2020 and May 2023. If you always paid your taxes on time and never faced IRS penalties during the pandemic, this opportunity does not apply to you.

How much money will I actually get back?

Your potential refund mirrors the exact amount you paid in qualifying penalties, plus any interest the IRS charged you. For some retirees, this means recovering $150 for a minor late-payment fee. For retirees who liquidated large assets and missed quarterly payments, the refund could exceed $5,000. Check your IRS account transcripts for exact figures.

What if I already paid the penalties years ago?

The purpose of this protective claim is to recover money you already surrendered. The Kwong ruling asserts the IRS should not have collected those penalties during a federally recognized disaster period. By filing Form 843, you formally ask the government to return the money you already paid.

How do I file a protective claim by the deadline?

Submit IRS Form 843 by July 10, 2026. At the top of the form, clearly write Protective Refund Claim Pursuant to Kwong Case. You must file a separate form for each tax year you are contesting. Mail the completed paperwork via certified mail to your typical IRS service center. If you are uncomfortable handling this, consult a tax professional immediately.

Your Next 48 Hours: Take Action Before the Window Closes

Knowledge without action is merely trivia. You now possess the insight to potentially recover thousands of dollars, but the clock is ticking toward the July 10, 2026 deadline. Do not wait for the IRS to knock on your door. Within the next 48 hours, commit to one concrete step. Either log into your digital IRS account to download your tax transcripts, or call your tax preparer and ask if you paid any IRS penalties between 2020 and 2023. Taking this proactive measure puts you in control of your financial destiny. Safeguard your retirement by demanding every dollar you are legally owed—your future self will thank you for the effort.