Comfortable retirees do not rely on luck; they build daily routines that transform savings into lifelong security and purpose. You can secure a thriving future by adopting the specific financial, health, and lifestyle habits proven to prevent common post-career struggles. Recent data from the Federal Reserve indicates that while older Americans hold record wealth, nearly half risk outliving their assets due to inflation and healthcare costs. Navigating this landscape requires more than just a well-funded retirement account; it demands proactive management of your daily choices. Whether you manage a fixed budget or navigate complex Medicare options, mastering these practical routines will help you maintain independence and peace of mind for decades to come.

The New Retirement Reality: Market and Policy Shifts

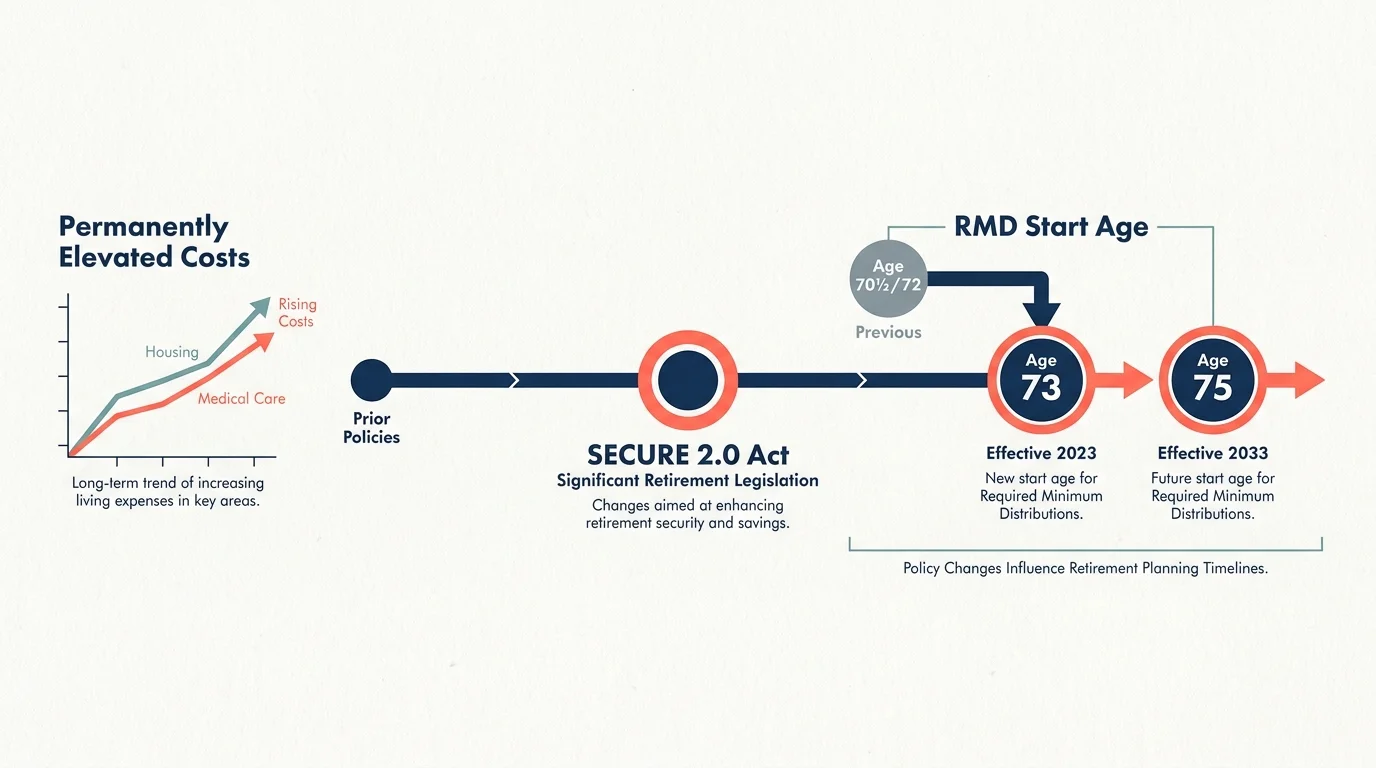

The economic environment of 2026 presents unique challenges and opportunities that demand your attention. Inflation has stabilized from the severe spikes of the early 2020s, but the baseline cost of everyday goods, housing, and medical care remains permanently elevated. You must account for this new pricing reality when projecting your future living expenses. Furthermore, legislative changes like the SECURE 2.0 Act have altered the timeline for Required Minimum Distributions, pushing the starting age to 73—and eventually to 75. This shift provides you with a longer runway for tax-deferred growth, but it also creates a steeper tax burden when those distributions finally begin.

Simultaneously, longevity trends continue to stretch the typical retirement timeline. Planning for a twenty-year retirement is no longer sufficient; you must financially and physically prepare for a lifespan that could easily extend into your late nineties. Comfortable retirees acknowledge these shifting parameters rather than ignoring them. They understand that a static plan crafted a decade ago cannot survive today’s dynamic economic forces. By staying informed about policy changes and adjusting their strategies accordingly, successful retirees protect their purchasing power and maintain their standard of living regardless of external market volatility.

Income Planning: Habits That Protect Your Cash Flow

Habit 1: Dynamic Withdrawal Management

Struggling retirees often adhere rigidly to outdated withdrawal strategies, pulling exactly four percent from their portfolios every year regardless of market conditions. Comfortable retirees practice dynamic withdrawal management. When the stock market experiences a prolonged downturn, they tighten their discretionary spending and reduce their withdrawal rate to avoid selling assets at a steep loss. Conversely, during sustained bull markets, they may grant themselves a slight increase in spending. This flexible approach preserves the core principal of your portfolio, ensuring your money continues compounding and supporting you through decades of market cycles.

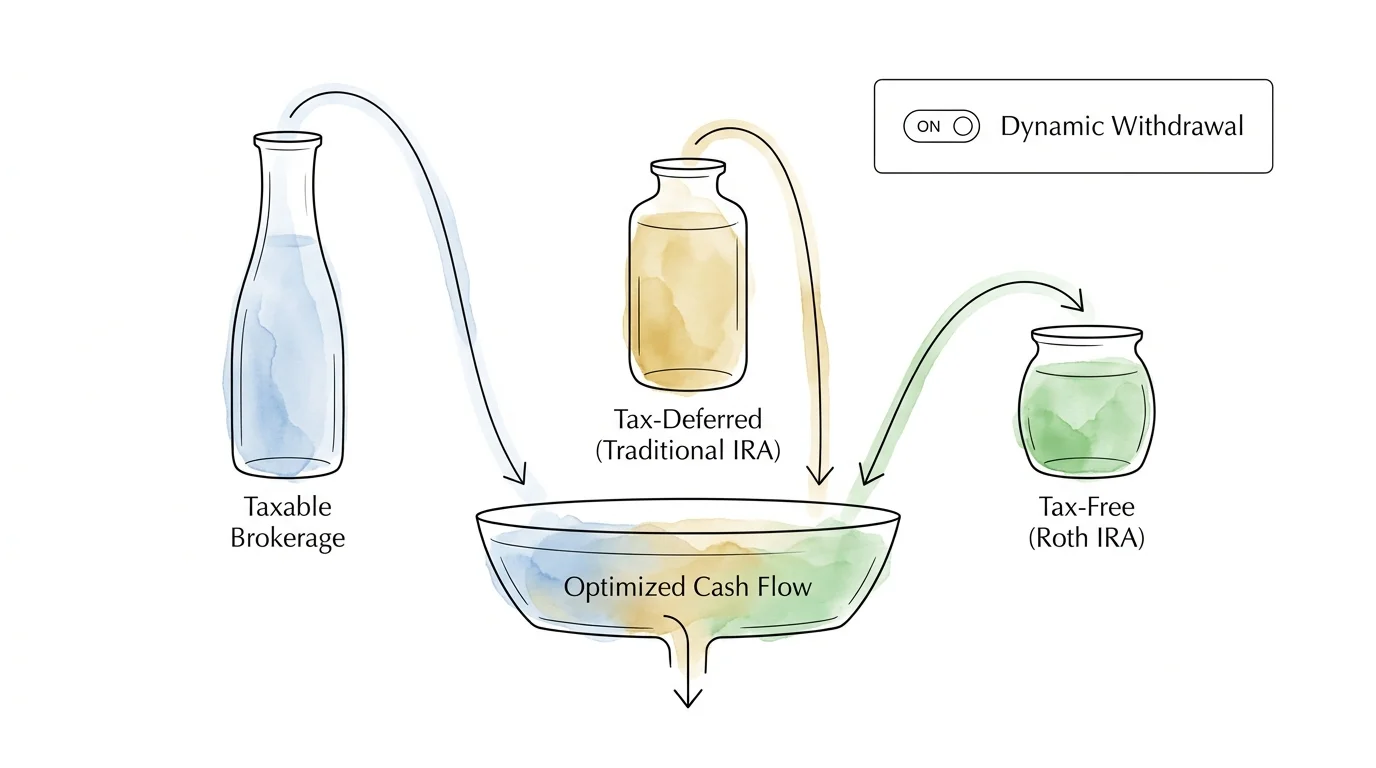

Habit 2: Strategic Tax Diversification

Managing your tax liability in retirement is just as crucial as generating robust investment returns. Comfortable retirees habitually optimize their asset location, maintaining a deliberate mix of taxable brokerage accounts, tax-deferred accounts like Traditional IRAs, and tax-free vehicles like Roth IRAs. By pulling funds from different buckets strategically each year, you can control your taxable income. This proactive management keeps you in lower marginal tax brackets and prevents you from unnecessarily triggering costly Medicare Income-Related Monthly Adjustment Amount surcharges. Viewing your accounts holistically allows you to keep more of your hard-earned wealth.

Habit 3: Proactive Benefit Optimization

Many individuals passively accept their government benefits without exploring strategies to maximize their lifetime payout. Thriving retirees treat Social Security as foundational longevity insurance. They habitually verify their projected benefits and coordinate claiming strategies with their spouses. Delaying your claim past your full retirement age guarantees an eight percent annual increase in your benefit amount until age 70. You can establish this habit early by reviewing your earnings record through the Social Security Administration well before your planned exit from the workforce. Correcting clerical errors on your earnings record today prevents permanent reductions in your monthly income tomorrow.

Health and Wellness: Habits That Preserve Your Independence

Habit 4: Routine Healthcare Coverage Reviews

Healthcare expenses represent one of the most significant threats to retirement security. Struggling retirees often allow their Medicare Advantage or Part D prescription drug plans to auto-renew year after year, unaware that formularies and provider networks change annually. Comfortable retirees ruthlessly audit their coverage during the Open Enrollment period every autumn. By using the official plan finder tool on Medicare.gov, you can input your current medications and discover plans that offer better coverage or lower premiums. This single annual habit can save you thousands of out-of-pocket dollars and guarantee you retain access to your preferred medical specialists.

Habit 5: Consistent Physical Conditioning

Financial wealth loses its value if you lack the physical capability to enjoy it. Comfortable retirees prioritize their physical autonomy by treating exercise as a non-negotiable daily appointment. They move beyond simple aerobic activities like walking and incorporate dedicated resistance and balance training into their routines. Maintaining muscle mass and bone density drastically reduces the risk of debilitating falls—a leading cause of lost independence among older adults. You can begin building this routine by researching safe exercise protocols provided by the National Institute on Aging, ensuring your physical foundation remains strong regardless of your current mobility level.

Habit 6: Preventive Healthcare Engagement

Reacting to health crises only after they occur leads to severe physical and financial distress. Successful retirees operate on a model of aggressive prevention. They schedule and attend all recommended annual screenings, from cardiovascular assessments to vision and dental checkups. They do not ignore minor symptoms, understanding that early intervention often turns potential catastrophes into manageable inconveniences. Cultivating a collaborative, honest relationship with your primary care physician ensures that small issues are resolved before they compound into expensive, life-altering emergencies.

Lifestyle Design: Habits That Cultivate Purpose and Connection

Habit 7: Structured Social Interaction

The sudden loss of workplace camaraderie can plunge unprepared retirees into deep isolation; research continually links chronic loneliness to severe cognitive and physical decline. Comfortable retirees engineer their social environments with extreme intentionality. They schedule regular lunches with friends, join special interest clubs, and integrate themselves into multi-generational community groups. By consistently putting dates on the calendar, you force yourself to stay connected and engaged. You can easily find local engagement opportunities by accessing community and volunteer resources through AARP, ensuring your days remain vibrant and populated with meaningful conversations.

Habit 8: Purpose-Driven Routines

Without the structure of a nine-to-five career, days can quickly blend into a shapeless void of television and idle time. Thriving retirees cultivate a robust post-career identity by pursuing challenging, purpose-driven activities. Whether you launch a small consulting gig, dedicate twenty hours a week to a local food bank, or master a complex new skill like a foreign language, engaging in difficult tasks provides profound psychological satisfaction. Defining a clear purpose gives you a reason to get out of bed each morning and keeps your cognitive faculties sharp over the long term.

Habit 9: Budgeting for Joy

A surprising number of affluent retirees struggle with an intense fear of spending, hoarding their wealth instead of enjoying the fruits of their lifelong labor. Conversely, those who experience a deeply satisfying retirement build specific allocations for joy directly into their financial plans. They earmark funds for travel, hobbies, family experiences, or charitable giving, and they spend that money without guilt. Recognizing that you saved diligently for decades precisely so you could afford these experiences allows you to transition from a mindset of accumulation to one of intentional, joyous distribution.

Expert Voices: Insights from the Field

Professionals who guide individuals through their golden years observe distinct patterns among their most successful clients. Certified Financial Planners consistently note that the smoothest transitions occur when clients view retirement not as a finish line, but as a completely new phase of active management. Planners emphasize that behavioral discipline—such as ignoring sensationalist financial news and sticking to a long-term strategy—matters far more than picking the perfect stock.

Gerontologists echo this sentiment regarding lifestyle and health. Leading longevity researchers argue that cognitive decline is not an absolute certainty of aging, but rather a risk that can be mitigated through continuous environmental stimulation. They find that retirees who view themselves as active contributors to society rather than passive consumers of leisure report drastically higher levels of life satisfaction. The consensus across both financial and psychological disciplines is clear: active engagement with your money, your health, and your community generates resilience.

Safeguarding Your Golden Years: Risks to Watch

As you build these positive habits, you must also construct defenses against the hidden hazards that target older Americans. Cybercrime and financial fraud have grown alarmingly sophisticated. Scammers routinely utilize artificial intelligence to clone the voices of loved ones, attempting to extort emergency funds over the phone. You must establish strict verification protocols with your family and commit to never transferring funds based on an unsolicited call. Combat these threats by staying vigilant and reporting suspicious financial requests to the Federal Trade Commission immediately.

You must also remain aware of sudden financial cliffs, particularly regarding the death of a spouse. The widely documented tax penalty for widows and widowers occurs when a surviving spouse inherits the entire estate but must immediately file taxes under the less favorable single-filer brackets. This transition can thrust the surviving spouse into a significantly higher tax bracket, reducing their net income just when they need stability most. Proactive planning—such as executing Roth conversions during the lower-tax joint filing years—can heavily mitigate this devastating financial trap.

Frequently Asked Questions

How much cash should I keep on hand in retirement?

Financial experts generally recommend keeping one to two years of living expenses in highly liquid, safe accounts like high-yield savings or short-term certificates of deposit. This cash buffer prevents you from being forced to sell your invested assets at a steep loss during sudden market corrections. By covering your immediate lifestyle needs with cash reserves, you grant your equity portfolio the time it needs to recover from temporary dips.

Does working part-time affect my Social Security benefits?

If you choose to claim your Social Security benefits before reaching your full retirement age, the government will temporarily withhold a portion of your monthly payout if your earned income exceeds a specific annual limit. However, these withheld funds are not lost permanently; your benefit will be recalculated upward once you hit your full retirement age. Furthermore, if you wait until your full retirement age to claim, you can earn an unlimited amount of income from part-time work without facing any reduction in your Social Security benefits.

Should I prioritize paying off my mortgage before retiring?

Entering retirement completely debt-free drastically lowers your baseline monthly expenses, providing profound psychological relief and reducing the amount of income you need to generate from your portfolio. However, if you hold a mortgage with a remarkably low interest rate, maintaining the loan while keeping your capital invested in assets that yield higher returns might be mathematically superior. You must weigh the emotional comfort of owning your home outright against the potential loss of investment growth.

How can I protect my savings against persistent inflation?

You can effectively defend your purchasing power by maintaining a well-diversified portfolio that includes an appropriate allocation of equities, as stocks historically outpace inflation over the long run. Additionally, integrating Treasury Inflation-Protected Securities into your bond allocation provides a direct hedge against rising consumer prices. Finally, delaying your Social Security claim ensures a higher guaranteed baseline income, which makes the annual cost-of-living adjustments significantly more impactful in real dollars.

Your Next Step

The difference between struggling and thriving in retirement ultimately comes down to execution. Reading about sound financial and health strategies will not protect you; you must put these concepts into practice. In the next forty-eight hours, pick just one habit from this list to implement. You might log into your health insurance portal to review your current drug coverage, schedule a deferred medical screening, or simply text a friend to lock in a weekly coffee date. Taking immediate, concrete action creates momentum, placing you firmly on the path to a secure, vibrant, and incredibly comfortable retirement.