Taking control of your shared financial future requires clear communication before a medical crisis forces your hand. You and your partner must detail account access, income continuity, and long-term care plans while you are both healthy to avoid devastating gaps in your retirement security. Research shows that in nearly half of American households, one spouse completely manages the money, leaving the other unprepared if cognitive decline strikes unexpectedly. Securing your mutual peace of mind means sitting down together to map out everything from healthcare choices to daily household budgeting. Having these crucial conversations today builds a resilient safety net that protects your lifestyle, preserves your wealth, and ensures neither of you ever faces financial darkness alone.

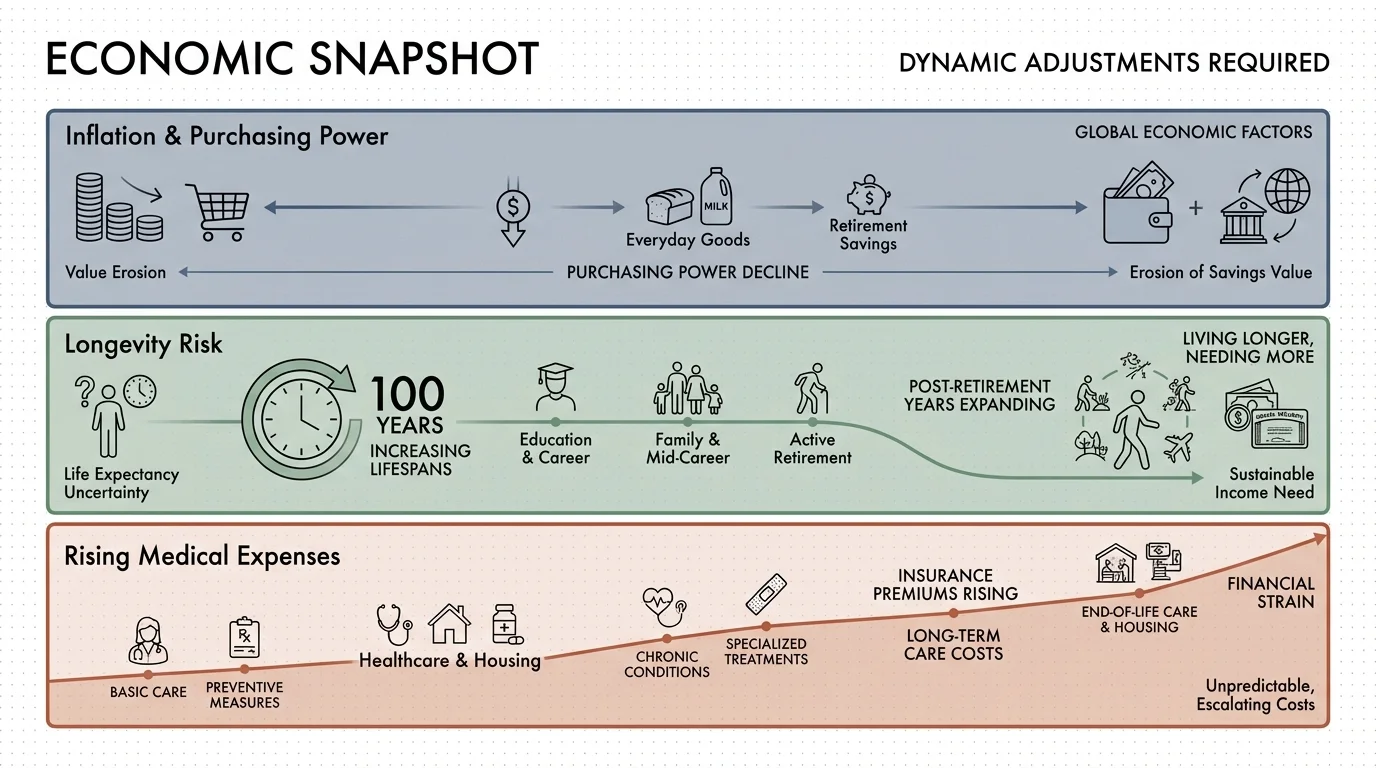

The Current Retirement Landscape and Economic Snapshot

Modern couples face an increasingly complex financial ecosystem that demands active participation from both partners. Decades ago, retirement planning often consisted of collecting a company pension and a Social Security check. Today, you must navigate fluctuating interest rates, prolonged periods of inflation, and sweeping changes to tax policies. When prices for groceries, utilities, and property taxes rise consistently, the purchasing power of your fixed income takes a direct hit. You can no longer set a budget at age sixty-five and expect it to serve you perfectly at age eighty-five. Surviving and thriving in this environment requires ongoing, dynamic financial adjustments.

Beyond the macroeconomic factors, longevity introduces unique challenges. As life expectancy increases, your retirement savings must last significantly longer, making careful withdrawal strategies essential. Data from the Bureau of Labor Statistics highlights that older Americans allocate a massive portion of their annual budgets directly to medical expenses and housing. A simple division of labor—where one spouse cooks and gardens while the other handles the investments and taxes—works wonderfully until the financial manager faces a sudden health emergency. When a stroke, heart attack, or early-stage dementia strikes, the non-managing spouse often steps into a confusing labyrinth of tax filings, minimum distribution requirements, and account passwords without a map.

Gerontologists and financial professionals agree that cognitive decline poses one of the most severe risks to your long-term wealth. Minor memory lapses can rapidly evolve into missed premium payments, devastating late fees, or susceptibility to aggressive sales tactics. Democratizing the financial knowledge within your household transforms a precarious situation into a secure, shared strategy. Breaking out of your comfortable roles requires vulnerability and patience, but establishing a united front offers the ultimate protection against economic uncertainty.

Conversation One: Consolidating and Locating Everyday Accounts

You cannot manage what you cannot find. In the digital age, a typical retiree household maintains checking accounts, high-yield savings accounts, multiple credit cards, utility portals, and perhaps a mortgage servicer. If the spouse who pays the bills becomes incapacitated, the other partner needs immediate access to keep the household running smoothly. Begin by mapping out your entire digital and physical financial footprint. Detail every institution you do business with, including the physical location of checkbooks, safe deposit box keys, and critical tax documents.

Moving your operations to a centralized system reduces friction during high-stress moments. Discuss implementing a secure password manager that you both know how to access. Make sure your two-factor authentication methods do not trap the surviving spouse out of essential accounts. If security texts only route to a single smartphone, a lost or deactivated device can lock you out of your bank for weeks. Take the time to streamline your finances by closing old, unused accounts and consolidating your cash into a few easily manageable places.

Conversation Two: Navigating Social Security and Pension Continuity

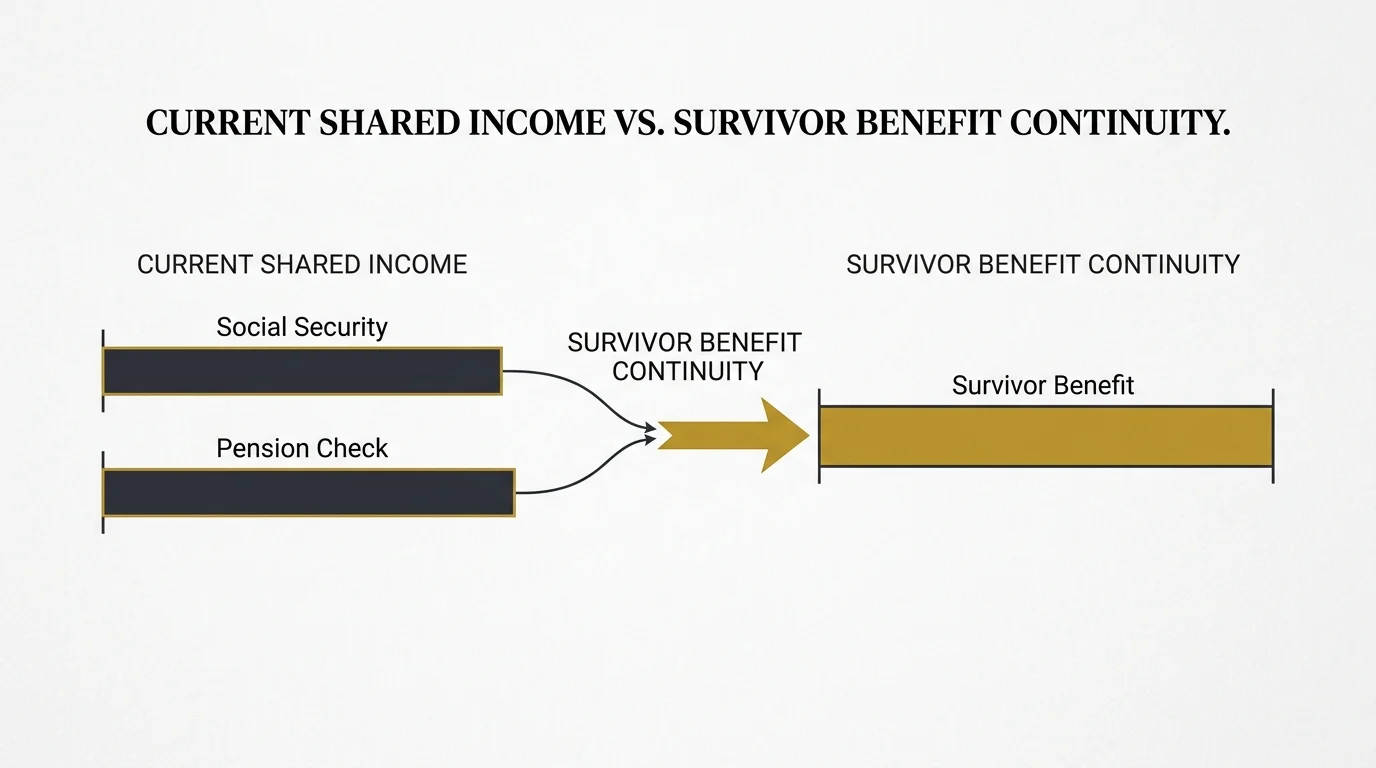

Many couples vastly underestimate the financial shock that occurs when one spouse passes away. You must discuss the specific mechanics of the widow’s penalty. When the first partner dies, the household income drops because the surviving spouse only retains the larger of the two Social Security checks; the smaller benefit disappears entirely. Despite this drastic drop in monthly revenue, your core household expenses—property taxes, home maintenance, and utilities—will remain largely the same. Review the official guidelines regarding survivor benefits to understand exactly what your future monthly income will look like.

Pensions require equal scrutiny. If one of you receives a corporate or government pension, you must verify the survivorship option selected at the time of retirement. Some pensions stop completely upon the death of the primary earner, while others offer a reduced percentage to the widow or widower. Sit down together and calculate your projected individual incomes. If a significant gap exists, discuss how you will bridge that shortfall using your investment portfolio, life insurance proceeds, or adjustments to your living arrangements.

Conversation Three: Planning for Long-Term Health and Medicare Costs

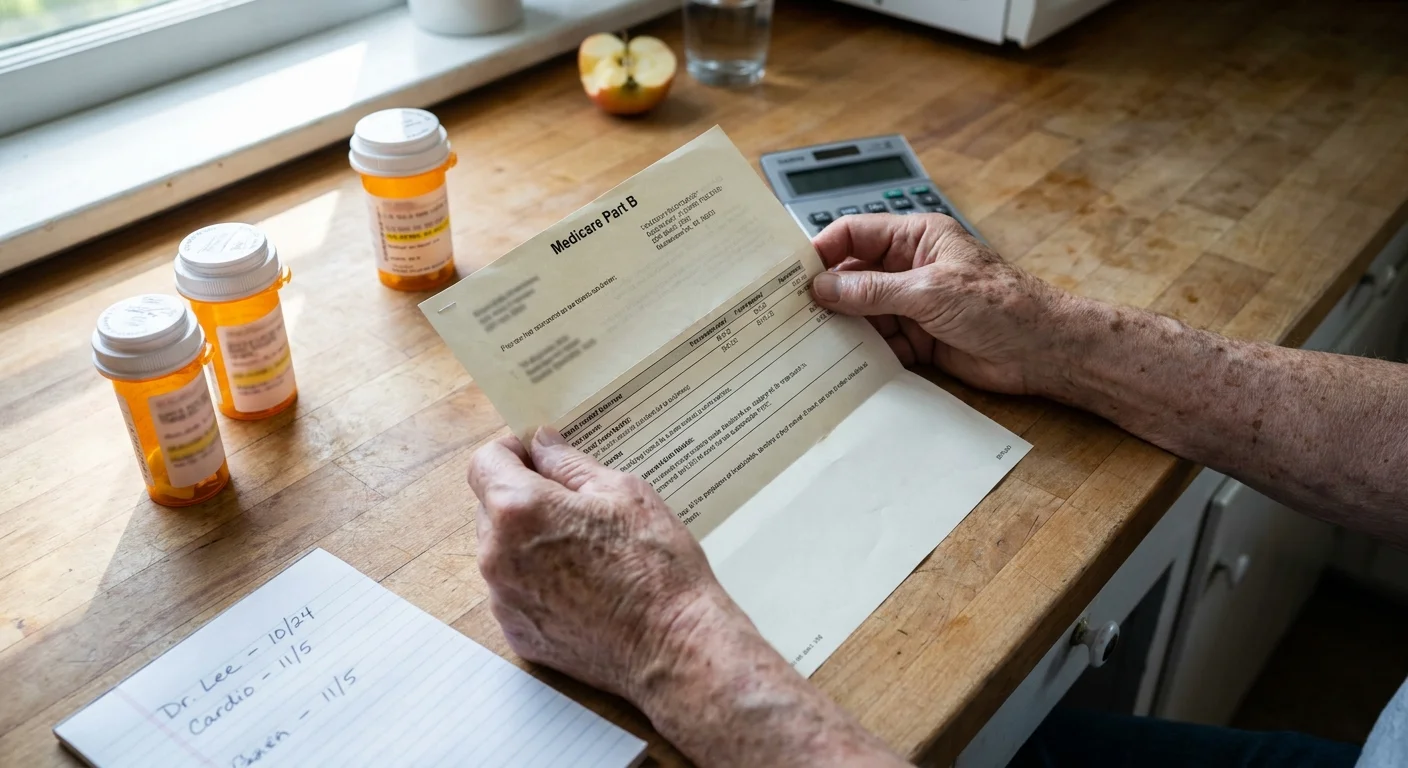

Health events dictate financial outcomes more aggressively than stock market corrections. You and your partner must openly discuss your preferences for aging and how you intend to pay for them. Do you want to age in place with the assistance of a home health aide, or do you prefer the community environment of an assisted living facility? These choices carry massive financial implications that can drain a lifetime of savings if you ignore them.

A common and dangerous misconception is that the government will cover all aging-related health expenses. While traditional health insurance covers hospital stays and physician visits, you should review the actual Medicare cost guidelines to understand that the program does not pay for long-term custodial care—such as help with bathing, dressing, or eating. Detail exactly how you will fund potential long-term care needs. Evaluate whether drawing down home equity, utilizing a long-term care insurance policy, or self-funding from a dedicated brokerage account makes the most sense for your shared goals.

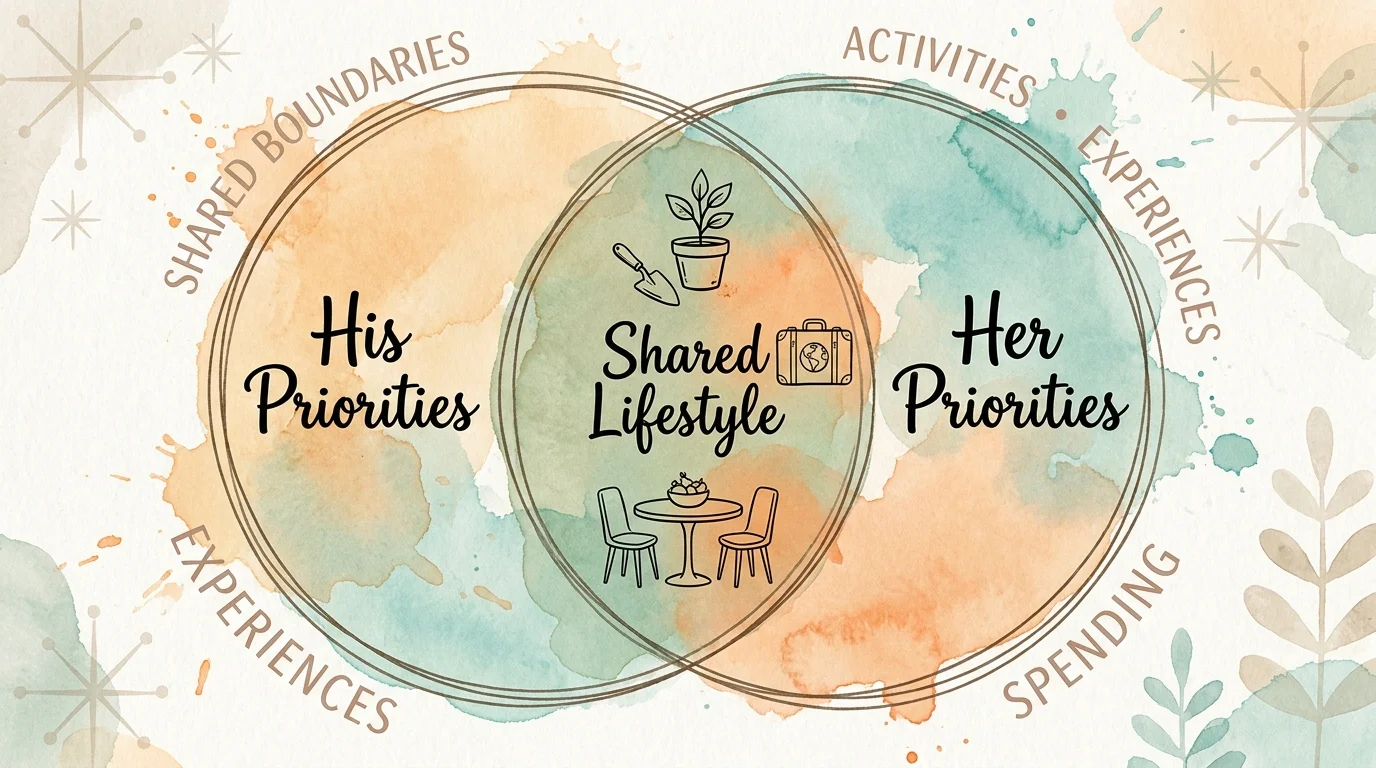

Conversation Four: Defining Your Shared Lifestyle and Spending Boundaries

Retirement offers the freedom to spend your time and money exactly as you see fit, but differing priorities can quietly breed resentment. You might envision spending your savings on international travel and luxury cruises, while your spouse prefers to renovate the kitchen, buy a recreational vehicle, or aggressively fund a grandchild’s college savings plan. Set clear, unambiguous boundaries around discretionary spending so that both of you feel fulfilled and respected.

Family support often triggers the most intense financial disagreements. Many older adults jeopardize their own economic stability by over-supporting adult children who request help with down payments, credit card debt, or living expenses. You must establish a unified policy regarding family loans and gifts. Determine a monthly or annual safe-to-spend number that protects your portfolio while allowing you to enjoy the fruits of your decades of labor. Aligning your lifestyle vision ensures that every dollar spent brings you closer together rather than driving a wedge between you.

Conversation Five: Protecting Wealth Against Fraud and Financial Abuse

A harsh reality of aging is an increased vulnerability to financial exploitation. Scammers specifically target older adults using highly sophisticated phishing emails, artificial intelligence voice cloning, and text message fraud. A single moment of confusion can result in thousands of dollars wired directly into the hands of a criminal. You must acknowledge this risk openly and build defensive strategies to protect the wealth you worked so hard to accumulate.

Create a household pact right now: neither of you will wire money, purchase gift cards, or provide account passwords over the phone without consulting the other partner first. Set up instant transaction alerts on all your checking accounts and credit cards so you can spot unauthorized charges the moment they occur. Take advantage of established fraud prevention resources to stay updated on the latest deceptive tactics. Freezing your credit files with the major reporting bureaus offers an additional, highly effective layer of defense against identity theft.

Conversation Six: Designating Trusted Contacts and Updating Beneficiaries

Estate planning extends far beyond drafting a simple will. The beneficiary designations on your individual retirement accounts, 401(k) plans, annuities, and life insurance policies dictate the flow of your money. These forms legally override any instructions written in your will. If you neglect to update an account after a major life event, your assets could transfer to an ex-spouse or bypass a new grandchild entirely. Reviewing the federal beneficiary rules ensures your legacy passes exactly as you intend.

Pull the records for every financial product you own and verify the primary and contingent beneficiaries. While you are communicating with your financial institutions, add a trusted contact to your accounts. A trusted contact gives your broker or bank permission to reach out to a designated family member or friend if they suspect you are the victim of financial exploitation or if they cannot reach you during an emergency. Furthermore, consider adding Transfer on Death designations to your taxable brokerage and savings accounts to help your surviving spouse bypass the costly, public, and time-consuming probate process entirely.

Conversation Seven: Establishing a Transition Plan for Financial Control

The final crucial conversation centers on the actual handover of financial power. The spouse who currently manages the investments and taxes will eventually need to step back. Identify the clear trigger events that indicate it is time to relinquish control. Will the transition happen at a specific age, upon a specific medical diagnosis, or through a mutual agreement that managing the daily portfolio has simply become too stressful?

Do not wait until cognitive decline accelerates to introduce the non-managing spouse to your professional team. Schedule a joint meeting with your certified public accountant, estate attorney, and financial advisor this year. The supporting spouse must build a rapport with these experts in a calm, low-stakes environment. Engaging a certified financial planning professional creates a neutral space for this transition, ensuring the surviving partner always has a trusted fiduciary to call when they need objective guidance.

Frequently Asked Questions About Couples Finance in Retirement

When should we start having these financial conversations?

You need to initiate these discussions immediately. Waiting for a medical diagnosis or a sudden hospitalization forces you to make complex financial decisions under extreme emotional duress. Approach the topic during a quiet, relaxed weekend morning when you both feel clear-headed and calm. Treat this process as a gradual, ongoing dialogue rather than a single, exhausting marathon meeting.

How do we handle a situation where one partner refuses to talk about money?

Resistance usually stems from fear, anxiety, or a desire to maintain independence. Approach your partner with empathy rather than accusations. Frame the conversation around mutual protection; explain that you want to understand the finances so you can honor their wishes and avoid burdening your children. If your spouse remains entirely closed off, suggest hiring a neutral third-party mediator, such as a financial therapist or a fiduciary advisor, to guide the discussion safely.

What documents do we absolutely need to have in place immediately?

Your protective foundation relies on four critical documents. You must establish a durable power of attorney for finances, allowing your partner to pay bills and manage accounts if you become incapacitated. You also need an advance healthcare directive, an updated last will and testament, and a comprehensive master list of all account logins, passwords, and institutional contacts. Keep these original documents in a secure, fireproof location that you both can access effortlessly.

How can a financial advisor help us facilitate these discussions?

A fiduciary financial advisor removes the deep emotional baggage that often derails money conversations between spouses. They provide objective, data-driven frameworks to resolve disagreements about spending, legacy planning, and risk management. Furthermore, an experienced advisor will identify blind spots in your strategy—such as looming tax liabilities or inadequate long-term care coverage—ensuring your joint plan remains fully optimized for whatever the future holds.

Take Action Now

Knowing what to discuss represents only the first step; your security depends entirely on execution. Choose just one of the seven conversations outlined above to tackle this weekend. Pour a cup of coffee, sit down at the kitchen table, and gently open the dialogue with your partner. Whether you decide to consolidate an old checking account, verify your life insurance beneficiaries, or write down the login credentials for your utility provider, taking a single, concrete action builds immediate momentum. Protecting your lifestyle and your spouse begins with the courage to start talking today.