Your vision of life after work shifts dramatically once the reality of endless free time and fixed incomes sets in, meaning you must stay flexible to thrive. Adjusting your expectations prevents financial stress and emotional burnout during a transition lasting decades. While sixty percent of workers imagine a perfectly curated leisure lifestyle, actual retirees quickly discover that full-time travel or constant family visits rarely match the fantasy. This pivot away from outdated ideals opens the door to deeper fulfillment and smarter money management. By examining the illusions most people abandon, you can bypass years of frustration and immediately build a resilient, purpose-driven future that honors your actual health, budget, and evolving personal interests.

Navigating the Current Retirement Landscape

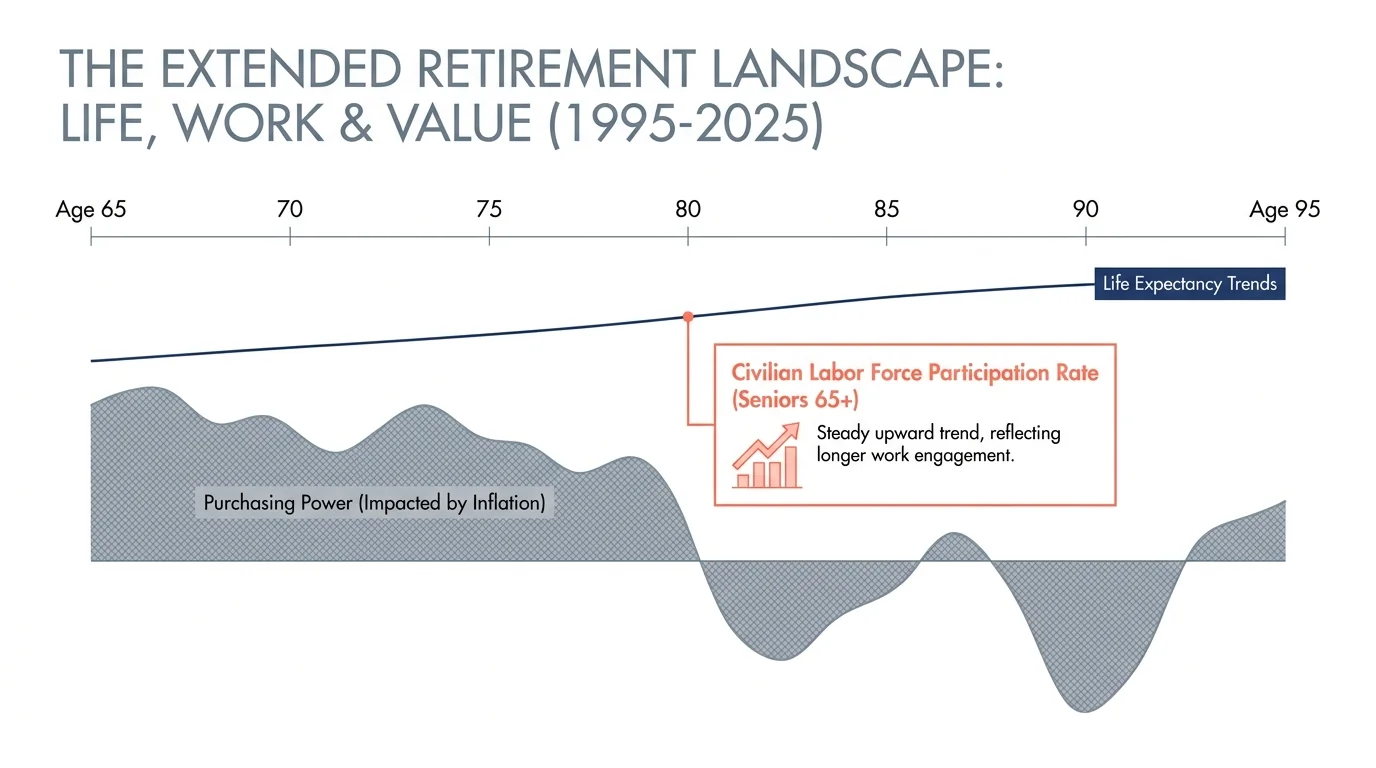

The economic environment defining your later years requires continuous adaptation rather than a set-it-and-forget-it mindset. Inflationary pressures constantly reshape purchasing power, forcing you to look critically at the feasibility of your initial lifestyle goals. Simultaneously, life expectancy continues to stretch longer, meaning your investment portfolio must sustain you for perhaps thirty years or more. Understanding these macroeconomic realities empowers you to make proactive, highly informed adjustments before a financial crisis forces your hand.

Recent economic data indicates that the traditional concept of a hard stop at age sixty-five no longer applies to a vast segment of the population. Whether driven by financial necessity or a deep desire for continued mental engagement, a significant portion of older adults remain active in the modern labor force. You can explore the latest workforce participation trends through the Bureau of Labor Statistics to see how your peers navigate this extended professional phase. Recognizing that the structural landscape shifted drastically over the last decade allows you to abandon rigid expectations and successfully design a flexible, personalized approach to your post-career life.

8 Common Retirement Dreams You Might Abandon

1. The Endless Globetrotting Itinerary

Before leaving the workforce, you might envision hopping seamlessly from European capitals to tropical islands without ever looking back. Once reality hits, the physical toll of changing time zones, carrying heavy luggage, and navigating crowded airports becomes glaringly apparent. Travelers quickly discover they miss the quiet comfort of their own beds and the steady rhythm of their local communities. Financial constraints also emerge rapidly as global travel costs and travel insurance premiums surge. You will likely find that taking two highly curated, immersive trips each year provides far more genuine satisfaction than maintaining a grueling schedule of continuous, exhausting movement.

2. The Isolated Wilderness Cabin

Moving to a remote, picturesque location sounds like the ultimate escape from rush-hour traffic and noisy suburban neighborhoods. Yet, the novelty of deep isolation wears off when you face a forty-minute drive just to buy fresh groceries or attend a routine medical checkup. As you age, close proximity to comprehensive healthcare facilities transitions from a mere convenience into an absolute necessity. Maintaining a sprawling rural property requires immense physical labor that drains your daily energy and financial resources. Selecting a walkable community with strong medical infrastructure ultimately proves much more sustainable than hiding away in a remote forest cabin.

3. Providing Full-Time Childcare for Grandchildren

Providing daily childcare for your young grandchildren feels like a wonderful way to establish deep family bonds. However, this expectation frequently clashes with the immense physical stamina required to chase energetic toddlers for eight hours a day. You might quickly realize you essentially replaced a demanding corporate manager with a chaotic, unpaid babysitting schedule. Furthermore, your adult children might relocate for unexpected career opportunities, leaving you completely stranded in a neighborhood you chose strictly for family proximity. Establishing healthy boundaries—like committing to one dedicated afternoon a week—preserves your vital energy for your own personal pursuits.

4. The Abrupt Stop to All Work

Culture celebrates clocking out for the final time as the ultimate finish line; yet, a sudden, complete cessation of work frequently leads to profound identity loss. After you spend decades building professional expertise, facing zero intellectual demands triggers severe boredom and a loss of daily purpose. An increasing number of older adults actively engage in part-time consulting or phased workplace transitions. Working just ten to fifteen hours a week on your own terms provides vital social interaction and a helpful buffer against early portfolio depletion. Utilizing your unique skills brings immense joy when you remove the underlying financial desperation.

5. Extreme Downsizing to a Tiny Home

Trading a spacious family house for an RV or a tiny home promises drastically lower utility bills and effortless cleaning routines. While shedding decades of clutter feels liberating initially, extreme downsizing often introduces unexpected frustrations into your daily routine. Tiny living spaces lack room for visiting family members, make it difficult to pursue indoor hobbies comfortably, and eliminate separate areas for necessary quiet reflection. Instead of adopting a minimalist extreme, consider the strategy of right-sizing. This balanced approach involves finding a single-story home with just enough square footage to accommodate overnight guests without requiring constant exterior maintenance.

6. Mastering a Dozen Expensive Hobbies

Pre-retirees often compile massive lists of activities they plan to master, ranging from competitive golf and sailing to advanced pottery and classical piano. The sheer cost of buying specialized gear, paying exclusive club dues, and securing professional lessons for multiple high-end hobbies quickly drains your discretionary income. Trying to learn too many complex skills simultaneously scatters your focus and prevents true, satisfying mastery. You will naturally narrow your focus down to one active physical pursuit and perhaps one creative outlet. This targeted approach respects your financial parameters while delivering maximum psychological and physical rewards.

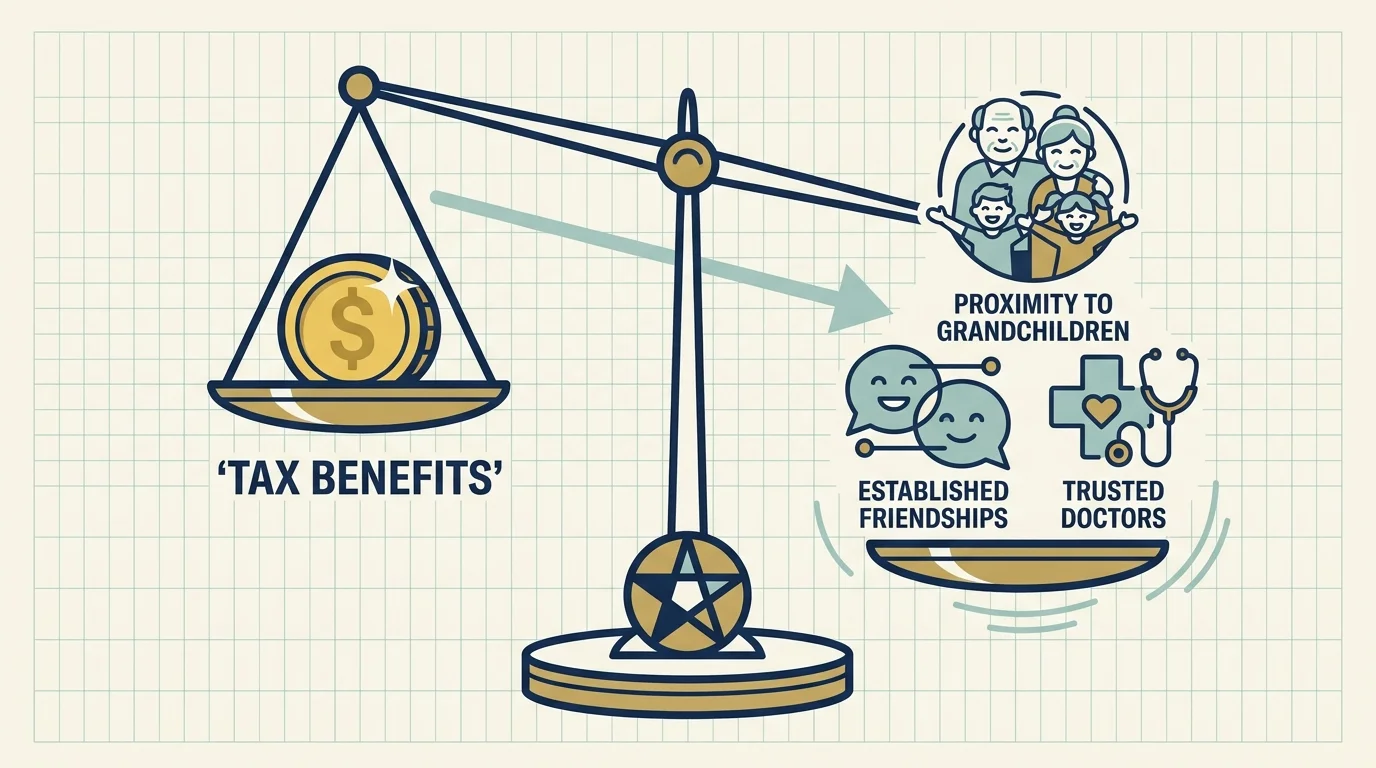

7. Choosing a Location Solely for Tax Benefits

Fleeing a high-tax state makes perfect mathematical sense when you look exclusively at a financial spreadsheet. However, choosing a primary residence strictly based on favorable tax codes ignores the critical social and cultural elements of your daily lifestyle. You might save thousands of dollars annually but feel deeply alienated if the new location lacks your preferred cultural events, outdoor environments, or community values. Furthermore, states without income taxes routinely compensate by levying incredibly high property or sales taxes. Conducting comprehensive, on-the-ground cost-of-living research prevents costly and emotionally draining relocation mistakes.

8. Managing Investments Entirely Alone

Self-reliance serves as an admirable trait during your intense wealth accumulation years. However, the financial landscape of later life presents incredibly complicated tax strategies, Required Minimum Distributions, and strict Medicare surcharges. Managing everything entirely alone increases your risk of making irreversible errors, especially if subtle cognitive decline eventually impairs your complex decision-making abilities. Transitioning to a collaborative approach by assembling a team of trusted professionals provides immense, enduring peace of mind. Allowing a fiduciary financial planner to navigate these strict regulations frees you to simply enjoy the wealth you diligently built.

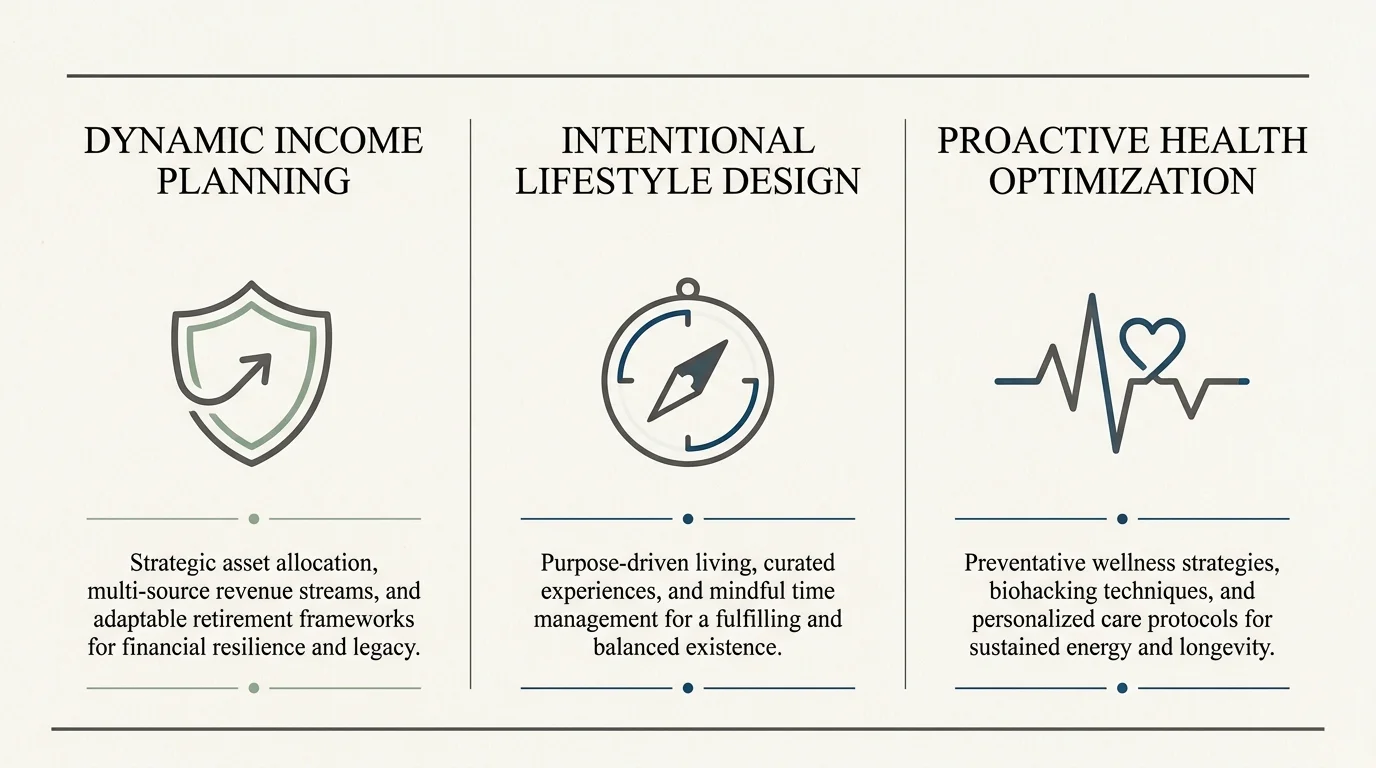

Three Strategy Pillars for a Resilient Future

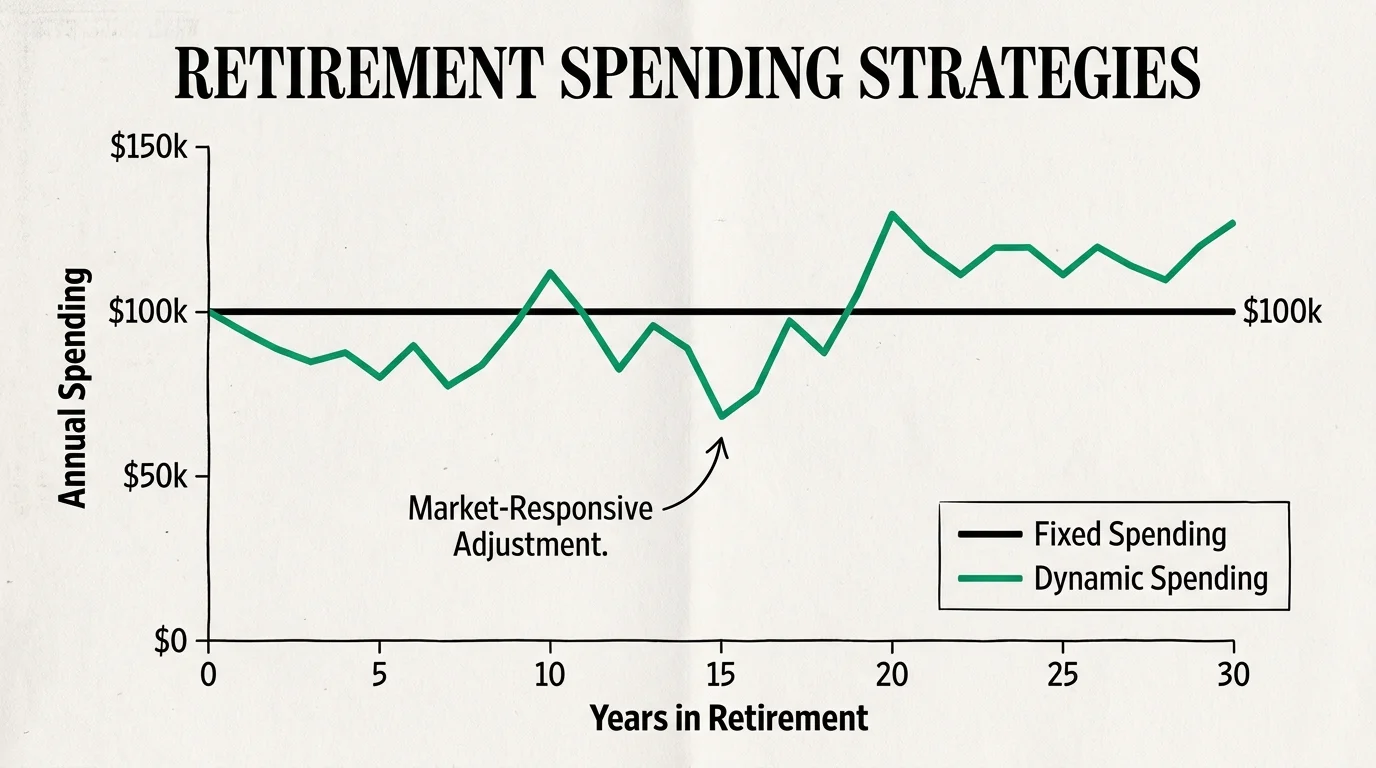

1. Dynamic Income Planning

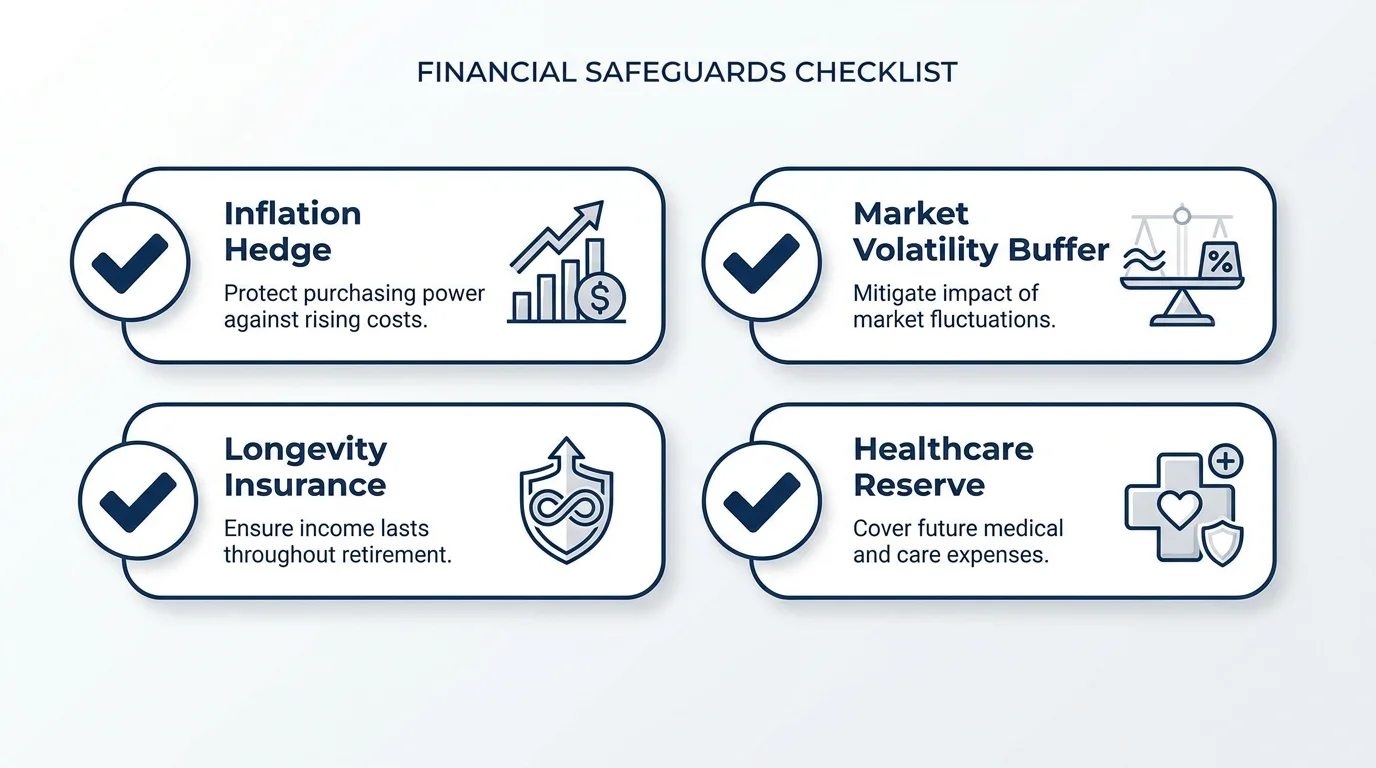

Your withdrawal strategy requires built-in flexibility to withstand volatile market conditions. Relying exclusively on a rigid withdrawal rate ignores the mathematical reality of sequence of returns risk, where early market downturns permanently cripple the longevity of your portfolio. By utilizing dynamic withdrawal strategies, you can consciously reduce discretionary spending during bear markets and comfortably increase your lifestyle budget during aggressive bull markets. Furthermore, understanding how to optimize your claiming strategy through the Social Security Administration guarantees you maximize your guaranteed income streams based on your specific longevity projections and spousal benefits. Failing to optimize these baseline income floors forces your investment portfolio to work significantly harder than necessary.

2. Intentional Lifestyle Design

Structure serves as the hidden engine driving a successful post-career life. Without the external framework provided by a demanding employer, your days easily blur together into a fog of television, passive internet scrolling, and lethargy. You must intentionally design your weeks to include scheduled socialization, dedicated physical movement, and engaging intellectual challenges. Treat your newly established routines with the exact same respect you once gave to mandatory corporate meetings. Whether you dedicate your Tuesdays to a local volunteer organization or strictly reserve Thursday mornings for a specialized group fitness class, concrete scheduling staves off the profound loneliness that catches many older adults entirely off guard.

3. Proactive Health and Wellness Optimization

Physical vitality dictates your ultimate capacity to actually enjoy your accumulated wealth. Prioritizing consistent strength training and cardiovascular endurance directly correlates with your ability to remain independent and avoid devastating medical expenses later in life. Beyond the gym, you must actively manage your preventative care by understanding the complex nuances of your ongoing insurance coverage. Reviewing your specific options annually via Medicare ensures your current plan adequately covers your specific prescriptions and preferred local medical providers, effectively shielding your household budget from unexpected out-of-pocket pricing shocks.

Critical Safeguards and Risk Management

Protecting your hard-earned assets requires constant vigilance against evolving external threats. Cybercriminals specifically target older adults with sophisticated phishing campaigns, romance scams, and fraudulent investment schemes designed to drain lifelong savings in a matter of days. You must implement strict digital hygiene immediately, utilizing encrypted password managers and mandatory multi-factor authentication across all of your financial accounts. Resources provided by advocacy groups like AARP offer up-to-date tracking of the latest fraud tactics currently circulating in your local community.

Beyond external fraud, you must ruthlessly guard against internal planning pitfalls like the Medicare Income-Related Monthly Adjustment Amount. A sudden, unexpected spike in your taxable income—perhaps from selling a large physical property or executing a massive Roth conversion—can instantly push you over specific government income thresholds. This sudden jump triggers massive surcharges on your monthly healthcare premiums. Consulting a qualified, proactive tax professional before making large portfolio liquidations prevents these hidden penalties from quietly sabotaging your monthly cash flow.

Frequently Asked Questions About Evolving Retirement Goals

How do I practically test a relocation idea before selling my current home?

Instead of relying on fond vacation memories, commit to a long-term rental in your target destination during its absolute worst weather season. If you plan to move to Florida or Texas, rent an apartment during the peak humidity and hurricane threats of August. If you desire a quiet mountain retreat, spend February navigating the heavy snow, freezing temperatures, and limited road access. Experiencing the harsh off-season reality prevents you from making a massive real estate commitment based entirely on idealized tourist experiences. Renting first also reveals the true local culture and medical infrastructure quality before you sink your equity into a permanent purchase.

What happens if I miscalculate my early healthcare costs?

Failing to account for the actual price of comprehensive medical care before you reach age sixty-five can quickly devastate your early retirement budget. If you leave your robust employer plan early, you must rely on the open market, where high-deductible premiums routinely cost thousands of dollars a month. Establishing a dedicated health savings account during your working years and aggressively funding it provides a crucial financial bridge. If you severely underestimate these baseline costs, you may need to re-enter the workforce temporarily just to secure employer-sponsored insurance until you reach the standard eligibility age.

Will working part-time completely ruin my Social Security benefits?

Earning income while claiming benefits before your full retirement age triggers the federal earnings test, which temporarily withholds a specific portion of your monthly payout. However, those withheld funds do not vanish permanently; the administration eventually recalculates your benefit amount upward once you finally reach your full retirement age. If you already passed that critical milestone age, you can earn an absolutely unlimited amount of money without facing any reduction whatsoever in your current monthly checks.

How can I find a new sense of purpose after leaving a highly structured career?

Purpose rarely arrives in a sudden flash of profound inspiration; rather, it emerges organically through active, daily experimentation. Start by auditing the specific aspects of your career you genuinely loved, such as mentoring junior staff, analyzing complex data sets, or organizing large community events. Seek out local nonprofit organizations or community boards that desperately need those exact skill sets. Transitioning your developed professional superpowers into community service provides immediate value to others while restoring your sense of personal significance and establishing a healthy daily structure.

Your Next Step Toward a Fulfilling Transition

Revising your vision for the future does not signify failure; instead, it demonstrates deep emotional maturity and highly practical financial wisdom. By letting go of outdated expectations, you actively clear the path for a lifestyle that actually aligns with your current resources and physical realities. Choose one specific area of your master plan—whether it involves realistically adjusting your annual travel budget or signing up for a single trial class instead of buying expensive hobby gear—and take decisive action within the next forty-eight hours. Embracing flexibility today guarantees a richer, far more sustainable tomorrow.